Owner income$150k

Owner income$150kC2C Platform Owner Income: $0 Distributions on $3525k GMV

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k  Net margin-18%

Net margin-18% Revenue for target pay$4.2M

Revenue for target pay$4.2M Business difficultyHard

Business difficultyHard

<

div class="step-circle step5">5

A C2C platform owner can draw the modeled $150k CEO salary if the business is funded, but Year 1 does not support profit distributions Here’s the quick math: $4348k revenue less 11% variable costs leaves about $3880k contribution, then $888k fixed overhead, $505k visible payroll, and $350k acquisition budgets drive operating profit to about negative $5558k In Year 2, the model reaches about $941k before reserves and owner distributions These are researched planning assumptions, not guaranteed earnings, salary advice, or tax advice

Owner income$150kNet margin-18%Revenue for target pay$4.2MBusiness difficultyHardWant to test your C2C marketplace owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the C2C Platform financial model?

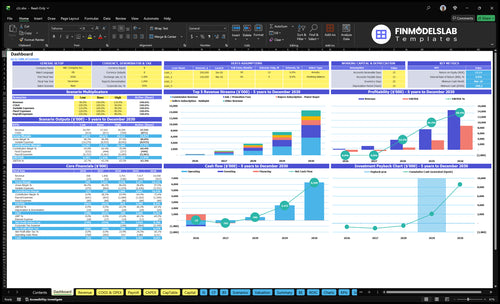

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the C2C Platform Financial Model Template; open it.

Owner-income model highlights

- Y1 GMV $3.525M, revenue $4.348M

- Y1 operating loss -$5.558M

- Y2 GMV $154M, revenue $174M

- Y2 pre-distribution profit $941k

- Owner income sensitivity charts

What costs reduce C2C marketplace owner income?

C2C Platform income gets cut fast when operating costs run high; if you’re sizing the setup, see How Much Does It Cost To Open And Launch Your C2C Platform Business?. In Year 1, the visible load is $74k/month in fixed overhead, or $888k/year, plus $505k in payroll and $350k for seller and buyer acquisition. Source costs also include 25% payment processing, 15% third-party API services, 50% digital advertising, and 20% transactional support.

Year 1 drains

- $74k monthly overhead

- $888k annual overhead

- $505k visible payroll

- $350k acquisition budgets

Margin cuts

- 25% payment processing

- 15% third-party API services

- 50% digital advertising

- 20% transactional support

Refunds, fraud losses, chargebacks, and dispute costs are not provided, so keep them as separate calculator inputs. They directly reduce contribution margin and owner take-home.

How does a C2C platform make money?

A C2C Platform makes money through transaction fees, subscriptions, and seller promotions, but the quality signal is recurring and optional revenue, not just GMV. In Year 1, What Is The Current Growth Trend Of Your C2C Platform? matters because $3,525k GMV produces only $391k commission revenue, while subscriptions and promotions produce $3,957k.

Year 1 Money Sources

- $391k commission revenue

- $959k seller subscriptions

- $1,798k buyer subscriptions

- $1,200k seller promotion fees

Margin Watchouts

- $0.50 fixed order fee

- 100% variable commission in source data

- $0 listing and payment-related seller fees

- Owner income comes after all operating costs

How much GMV does a C2C platform need to pay the owner?

If the C2C Platform wants to pay the owner $150k on top of $888k fixed overhead, $505k payroll, and $350k acquisition spend, it needs about $2.13M in revenue after the 11% variable cost load. Using the Year 1 commission stream of $391k on $3.525M GMV, that means about $19.2M GMV from commission alone. Subscriptions and promoted listings have to fill the gap.

Owner pay math

- $888k fixed overhead

- $505k payroll

- $350k acquisition budget

- $150k owner draw

GMV check

- Total need: $1.893M

- After 11% cost load: $2.13M

- Year 1 commission: $391k

- Implied GMV: about $19.2M

Want the six drivers of C2C marketplace owner income?

1

$3.5MGMV Volume

More orders and larger baskets push year 1 GMV to about $3.5M, and that is the base every fee line grows from.

2

$4.3MTake Rate

The fee mix turns that GMV into about $4.3M of year 1 revenue, so small pricing changes move income fast.

3

0.5-4.5xRepeat Usage

Repeat buyers are the real engine here: occasional users average 0.5 orders, while power buyers reach 4.5, so liquidity lifts lifetime value.

4

11%Loss Control

The model shows an 11% variable cost load, but refund, fraud, and chargeback losses are not provided, so those must be added as user inputs.

5

$350KCAC Efficiency

Seller and buyer acquisition budgets total $350K in year 1, so CAC control decides how fast growth turns into cash payback.

6

$888KOverhead Load

Fixed overhead is about $888K in year 1, with visible payroll at $505K, so labor and support discipline sets the floor for profit.

C2C Platform Core Six Income Drivers

GMV and Transaction Volume

GMV and Paid Orders

GMV is the top income driver because the platform earns on completed transactions, not the full sale value. With $3,525k in Year 1 GMV from 7,750 modeled orders, the average order is about $455 ($3,525,000 / 7,750). If orders do not finish, or refunds rise, activity can look strong while owner cash stays weak.

Order depth matters. Occasional buyers drive 0-50 repeat orders, regular buyers 150, and power buyers 300. More repeat buying lifts GMV without paying for new traffic each time, so it supports profit and owner draws. Traffic alone does not fund distributions.

Track Paid Volume First

Measure paid orders, completed orders, and refund rate weekly, not just signups or visits. Then break GMV by buyer segment so you can see where order depth comes from. If the mix shifts toward repeat buyers, each acquisition dollar works harder and cash flow gets steadier.

- Paid GMV versus traffic

- Completion rate by segment

- Refunds and chargebacks

Test anything that raises completed orders before it lifts marketing spend. A higher order count only helps if the platform keeps its slice, keeps fees low enough to hold buyers and sellers, and avoids low-quality traffic that never settles into cash.

1

Effective Take Rate

Effective Take Rate

Effective take rate is the share of GMV the platform keeps before costs. In Year 1, the model shows $391k in commission revenue on $3,525k GMV, plus $959k seller subscriptions, $1,798k buyer subscriptions, and $1,200k seller promotion fees. That puts total Year 1 revenue at $4,348k and sets the cash available for payroll and owner draw.

Higher fees can raise revenue, but they can also cut seller supply or buyer demand. If conversion or repeat orders drop after a fee change, the owner’s take-home can fall even if the take rate looks stronger on paper.

Test Fees on Real Cohorts

Track take rate by buyer and seller cohort, not just as one blended number. Measure completed orders, subscription attach, promoted-listing use, and refund rate before and after any pricing move. A fee lift only helps if GMV and repeat use stay intact.

- Watch conversion after fee changes.

- Watch seller supply by segment.

- Watch repeat orders and refunds.

2

Marketplace Liquidity and Repeat Usage

Marketplace Liquidity and Repeat Usage

Liquidity is the match rate: buyers find enough relevant listings, and sellers see enough real demand. In this model, the buyer mix shifts from 80% occasional, 15% regular, and 5% power in Year 1 to 40% / 35% / 25% by Year 5, so more revenue comes from people who buy again instead of one-off traffic.

Here’s the quick math: repeat orders rise from 0.50 to 0.80 for occasional buyers, 1.50 to 2.20 for regular buyers, and 3.00 to 4.50 for power buyers. That lifts profit because each repeat order needs less new acquisition spend, which helps cash flow and the owner’s draw.

Measure Repeat Depth, Not Just Sign-Ups

Track repeat orders per buyer segment, not just new users. If liquidity is weak, buyers search longer, sellers list less, and acquisition spend gets wasted on traffic that never converts to paid orders.

- Watch segment repeat depth monthly.

- Track active listings versus demand.

- Test features that raise return visits.

- Forecast profit on repeat contribution.

What this estimate hides: if new-user costs stay high while repeat usage stalls, owner income stays thin even when top-line volume rises. Better matching and trust tools should push more buyers into the regular and power groups, where each extra order carries more margin.

3

Payment, Refund, and Fraud Losses

Payment, Refund, and Fraud Losses

For a marketplace, payment and trust costs hit income fast. The model shows 25% of revenue goes to payment processing and 15% to third-party API services, for 40% combined COGS, or about $174k on $4348k revenue. That cuts the cash left for owner pay before any staff or marketing spend.

Refunds, chargebacks, and fraud losses are not given, so they should be modeled as separate deductions. Use paid orders, average order value, dispute rate, refund rate, and chargeback rate. If the platform is near break-even, even small loss rates can wipe out the owner’s draw.

Track net payout per order

Measure what stays after fees, reversals, and fraud. The useful number is net revenue per completed order, not gross sales. If payment fees rise or dispute losses tick up, contribution margin falls and the business can still look busy while owner cash stays weak.

Model this each month with GMV, completed orders, payment fee %, API cost %, refund dollars, chargeback dollars, and fraud write-offs. A small lift in dispute losses can matter more than a small lift in volume when fixed costs are already high.

- Track refunds by order cohort.

- Separate chargebacks from refunds.

- Test fraud rules by seller type.

- Watch net cash, not gross revenue.

4

Customer Acquisition Efficiency

Customer Acquisition Efficiency

When acquisition is efficient, growth adds profit. On the model, Year 1 seller CAC is $75 against a $150k seller marketing budget, so the platform acquires 2,000 sellers. Buyer CAC is $20 against a $200k buyer budget, or 10,000 buyers. If CAC stays high, new users can look busy on paper but still drain cash before repeat orders pay back.

By Year 5, CAC improves to $50 for sellers and $10 for buyers, which raises the number of users each marketing dollar can buy. The key test is not first-sale revenue. It’s whether repeat contribution from later orders covers CAC fast enough to leave room for owner pay, support, and platform overhead.

Measure CAC Against Repeat Contribution

Track CAC by channel and by side of the market: seller budget, buyer budget, acquired users, and cost per activated user. Then compare that cost with repeat contribution, meaning the profit from later orders after fees and variable costs. If a cohort only pays back on the first order, acquisition is buying volume, not income.

Here’s the quick rule: lower CAC or lift repeat order count. In this model, seller CAC falls from $75 to $50, and buyer CAC falls from $20 to $10. That should free cash for profit draw, but only if retention holds and paid users keep transacting. Watch payback period, repeat rate, and refund loss together.

Support, Tech, and Team Overhead

Support, Tech, and Team Overhead

Overhead is the cash floor the platform has to clear before the owner can take money out. That includes CEO, CTO, marketing, engineering, and support payroll, plus tools and admin. With $74k in monthly fixed costs, or $888k a year, and $505k of visible Year 1 payroll, profit gets thin fast if volume slips.

Transactional support is another drag: at 20% of revenue in Year 1, it scales with sales, so more orders help only if service work stays efficient. On $4.348M of revenue, that support load is about $869.6k; weak moderation or slow product work can turn that into lost trust, refunds, and less owner pay.

Keep Overhead Tight

Track overhead by function, not as one lump sum. The key inputs are payroll, support tickets, moderation backlog, and monthly revenue. Delay hiring with owner labor where you can, but only if response times and trust stay intact. Here’s the quick math: every extra dollar of fixed cost has to be covered before distributions, so overhead discipline directly protects take-home income.

Watch fixed cost per month.

Track support cost as revenue percent.

Measure backlog age and reply time.

Review payroll before each hire.

6

Compare lean, base, and high-growth C2C platform owner income scenarios

Owner income scenarios

GMV, commission mix, CAC, payroll, and fixed overhead swing owner income fast in this model. The high case only holds if growth outpaces spend.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | Lower case assumes Year 1 traction only, so owner income stays at zero. | Base case assumes Year 2 scale, where GMV and revenue are much larger and owner payouts start to appear. | High case assumes Year 3 scale with strong volume and a much larger payout base. |

| Typical setup | Year 1 stays small: $3.525M GMV, $4.348M revenue, about $350k acquisition spend, $888k fixed overhead, $505k visible payroll, and negative $5.558M operating profit before distributions. | Year 2 reaches about $154M GMV and $174M revenue, with about $750k acquisition spend, $620k visible payroll, and roughly $941k before reserves. | Year 3 reaches about $511M GMV and $538M revenue, with about $1.35M acquisition spend, $805k visible payroll, and roughly $262M before reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0Low case | $941k pre-reserveBase case | $262M pre-reserveHigh case |

| Best fit | Use this to stress-test launch burn and see how much time you have before owner payouts start. | Use this as the working plan for a steady marketplace that is growing but still fee-sensitive. | Use this to test the upside if the platform reaches strong network effects and payout capacity expands fast. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions; reserve percentage is user-entered.

Related Products

- C2C Platform Porter's Five Forces Analysis

- C2C Platform BCG Matrix

- C2C Platform Business Model Canvas

- 7 Critical KPIs to Scale Your C2C Platform

- C2C Platform Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Profitability of Your C2C Platform

- How Much Does It Cost To Run A C2C Platform Monthly in 2026?

- C2C Platform Startup Costs: Plan Beyond $350K Year 1 Marketing

- C2C Platform Financial Model Template in Excel

- How To Start A C2C Platform In 10 To 20 Weeks With First Sales

- How to Write a C2C Platform Business Plan in 7 Steps

- C2C Platform Marketing Mix

- C2C Platform Marketing Plan

- C2C Platform Business Proposal

- C2C Platform PESTEL Analysis

- C2C Platform Pitch Deck Example Editable PPTX

- C2C Platform Business SWOT Analysis

- C2C Platform Value Proposition Canvas

Frequently Asked Questions

In Year 1, the model supports a $150k CEO salary only if funded, but it does not support profit distributions The business shows $4348k revenue, 11% variable costs, $350k acquisition budgets, and about negative $5558k operating profit before distributions Owner distributions should wait until reserves and reinvestment needs are covered