Owner income$115k

Owner income$115kHow Much Canada Goose Control Owners Can Make: $365K Year 1 Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$115k  Net margin-18% to 51%

Net margin-18% to 51% Revenue for target pay$365k+

Revenue for target pay$365k+ Business difficultyHard

Business difficultyHard

Key Takeaways

- Recurring contracts stabilize income better than one-off assessments.

- Clustered routes cut fuel, wear, and labor waste.

- Hire only when density supports added payroll.

- Keep reserves for Month 8 cash dips.

Owner income$115kNet margin-18% to 51%Revenue for target pay$365k+Business difficultyHardWant to test your own goose control owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income will change with revenue, margins, payroll, reserves, debt, taxes, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in Canada Goose Population Control?

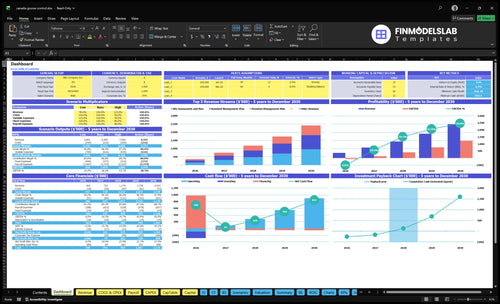

The Canada Goose Population Control Financial Model Template dashboard shows $365,000 Year 1 revenue, -$66,000 EBITDA, Month 9 breakeven, $683,000 minimum cash in Month 8, 35-month payback, and $241 million Year 5 revenue—open the model.

Owner-income model highlights

- Owner salary is tracked

- Cash reserve floor shown

- Scenario charts test pay

Can a goose control owner pay themselves year round?

Yes, Canada Goose Population Control can pay an owner year round in the model, but only because it includes a $115,000 annual CEO salary and a big cash cushion. Even then, Year 1 EBITDA is still -$66,000, minimum cash hits $683,000 in Month 8, breakeven lands in Month 9, and payback takes 35 months. The real pressure is seasonality, since nuisance demand, contract timing, weather, winter slowdowns, and municipal approval delays can all push cash out.

Cash pay test

- $115,000 CEO pay is already in model

- -$66,000 Year 1 EBITDA still shows

- Month 8 cash need peaks at $683,000

- Breakeven starts in Month 9

Risk control moves

- Set owner pay below cash capacity

- Build reserves before hiring ahead

- Use recurring contracts to smooth slow months

- Plan for weather and approval delays

What costs most reduce Canada goose control business profit margin?

For Canada Goose Population Control, the biggest profit-margin drag is payroll, not field supplies. On the KPI side, see What Are The 5 KPI Metrics For Canada Goose Population Control Business? for the operating measures that keep these costs in line. Direct service costs stay lighter: supplies and dog care are 5% of revenue in Year 1 and fall to 3% by Year 5, while fuel and vehicle maintenance drop from 7% to 5%.

Direct service costs

- Supplies and dog care: 5% to 3%

- Fuel and maintenance: 7% to 5%

- These costs scale with jobs

- Lower than payroll pressure

Fixed cost pressure

- Fixed overhead: $6,200 per month

- Year 1 payroll: $249,000

- Year 5 payroll: $644,000

- Startup capex: $194,500

How much can a solo Canada goose control business owner earn?

Canada Goose Population Control is not a true solo-owner model in the provided plan: Year 1 includes a $115,000 CEO and lead consultant salary, plus $55,000 for a lead canine handler, $48,000 for a wildlife technician, and $31,000 for a half-time sales and account manager, for $249,000 total payroll. A solo version could save that $134,000 of non-owner payroll early, but it would also cap route capacity and sales follow-up. Here’s the quick math: the small-crew model scales to $2.41 million in revenue and $1.226 million in EBITDA by Year 5 only if labor utilization and pricing hold.

Year 1 pay mix

- $115,000 owner salary

- $55,000 canine handler

- $48,000 wildlife technician

- $31,000 sales support

Solo tradeoff

- $134,000 payroll saved early

- Less route capacity

- Less sales follow-up

- Growth depends on labor use

Want to see the six biggest income drivers?

1

$14.4K-$30KRecurring Value

A standard plan runs $1,200-$1,400 a month and premium runs $2,500-$2,900, so each account adds recurring cash fast.

2

88%-92%Route Density

Tighter routes protect the 88%-92% gross margin before payroll and overhead by cutting drive time, fuel, and dead stops.

3

20%-40%Service Mix

Premium share rises from 20% to 40% while site assessments stay at 100%, so average ticket climbs with the same customer base.

4

$249K-$644KLabor Utilization

Payroll scales from about $249K to $644K, so crew scheduling and technician load decide what is left after the CEO salary.

5

Month 9Seasonality

Breakeven lands in Month 9, so early sales have to carry the slower ramp before cash turns positive.

6

$6.2K/moOverhead Guardrail

Fixed overhead runs about $6.2K a month, and the $683K minimum cash shows how much slack you need during the buildout.

Canada Goose Population Control Core Six Income Drivers

Recurring Account Value

Recurring Account Value

Recurring goose control contracts make income predictable. A standard plan at $1,200 per month annualizes to $14,400, while premium at $2,500 per month annualizes to $30,000 before churn, seasonality, and service costs. That spread drives owner pay because retained revenue is steadier than one-off work.

When premium mix rises from 20% in Year 1 to 40% in Year 5, average account value should climb if renewals hold. Higher retained account value also helps route planning, staffing, and cash flow. Weak renewals turn a high-revenue plan into a constant sales treadmill.

Protect renewals and raise retained value

Track active contracts, plan mix, monthly fee, renewal rate, and churn. Here’s the quick math: $1,200 × 12 = $14,400 and $2,500 × 12 = $30,000. What this estimate hides is churn, seasonality, and service costs, so forecast revenue by retained accounts, not just new sales.

- Measure renewals by plan

- Watch premium mix monthly

- Forecast retained annual value

1

Route Density

Route Density

Route density means how many billable goose control stops sit close together. When clustered jobs let one handler and technician cover more visits, fuel and vehicle maintenance stay at 7% of revenue in Year 1 and can fall to 5% by Year 5, which lifts gross margin and owner take-home.

Scattered one-off sites burn time and cash in the truck. Clustered HOAs, golf courses, parks, and commercial sites beat wide service areas because they cut windshield time, reduce wear, and keep labor on billable work instead of driving.

Keep Routes Tight

Track billable visits per day, route miles, and fuel plus maintenance as a share of revenue. Here’s the quick math: more close-together accounts means the same payroll covers more on-site work, so contribution margin improves before you add headcount.

- Group accounts by zip or corridor.

- Delay expansion until repeat density builds.

- Watch drive time before hiring.

- Charge extra for far-out sites.

If you expand service area too early, costs rise before recurring stops catch up, and that can squeeze the cash left for owner pay.

2

Service Method Mix

Service Method Mix

Service mix changes what each dollar of revenue can keep after labor, gear, and compliance costs. Here’s the quick math: direct service supplies and dog care drop from 5% of revenue in Year 1 to 3% in Year 5, so margin improves if premium work takes a bigger share. The real lever is mix, not just volume.

$2,500/month premium programs have more room to recover trained-dog care, lasers, kayaks, water gear, and site plans than $850 assessments. What this estimate hides: compliance-sensitive work can’t be priced like a generic markup, so local review time and rules can change take-home income fast.

Price by method, not by guess

Track revenue by service type: premium program, assessment, and any compliance-heavy work. Measure labor hours, dog care, gear use, and local review time per job so you can see which method actually funds owner pay. If assessments stay at $850, they need tight scope control or they drag margin.

Use a simple test: compare gross margin on $2,500/month plans versus assessments, then shift sales toward the method with better recovery of labor and equipment. Keep compliance-sensitive pricing separate until local rules are checked, because that cost is part of the job, not extra profit.

3

Labor Utilization

Labor Utilization

Labor utilization is the share of paid time that turns into billable work. Year 1 payroll is $249,000, including the $115,000 owner salary, $55,000 lead canine handler, $48,000 wildlife technician, and $31,000 half-time sales role. By Year 5, payroll reaches $644,000, so weak route density pushes labor into fixed overhead and cuts owner pay.

Keep Labor Tied to Route Density

Track owner field hours, active routes, billable work per handler and technician, and sales capacity. Owner time can protect early cash, but technician leverage only helps when routes stay full. If sales lag, delay hiring; if routes are clustered, add labor faster. That keeps payroll tied to revenue instead of consuming it.

4

Seasonality Management

Seasonality and Cash Timing

Seasonal goose control income is uneven, so owner pay can feel tight even when the year looks profitable. The source model flags the cash low point at Month 8, with breakeven in Month 9, so monthly draw should be based on cash timing, not annual revenue divided by 12.

Recurring contracts matter more than one-time site assessments because they smooth demand and protect retained accounts. The payback period is 35 months, so slow months and churn can stretch recovery fast. Adjacent wildlife work can fill gaps, but it should not pull attention away from retained goose accounts.

How to smooth owner income

Track active recurring contracts, monthly fees, churn, and the cash reserve needed to survive to Month 8. Line up contracts before peak demand, then hold enough cash to cover the low months without starving payroll, fuel, or the owner draw. That’s the real test of income quality.

- Book renewals before peak season.

- Separate assessment cash from recurring cash.

- Keep reserves through Month 8.

- Protect retained accounts first.

If the business leans too hard on one-time assessments, income will spike and fade. Better to price and schedule for repeat service, because steady contracts support route planning, staffing, and a more stable take-home pay.

5

Overhead And Reserve Discipline

Reserve-First Overhead

Overhead and reserve discipline decides how much cash the owner can actually keep. Fixed overhead is $6,200 per month, and the business also needs a $683,000 cash floor in Month 8, so owner pay has to come after reserves, debt service, reinvestment, and replacement planning.

Here’s the quick math: $3,500 rent, $1,200 insurance, $450 software and CRM, $250 dues, and $800 utilities and kennel maintenance. Marketing rises from $25,000 in Year 1 to $80,000 in Year 5, so cash need grows even if revenue looks steady. If reserves are thin, take-home pay gets cut first.

Protect Cash Before Pay

Track cash runway, not just profit. A practical reserve target is 3 to 6 months of fixed overhead plus planned marketing and debt service. That means the owner should model the $6,200 base cost, then layer in the marketing ramp from $25,000 to $80,000 before setting any draw.

Keep one reserve for operations and one for replacement. Separate the monthly owner draw from the cash needed for kennel upkeep, insurance, and future capex, so a good month does not erase next quarter’s safety buffer. If Month 8 cash starts to dip, cut draws before cutting compliance or service quality.

- Review runway every month.

- Lock reserve transfers first.

- Set owner pay last.

- Track marketing by season.

6

Compare lean, base, and mature owner income scenarios

Owner income scenarios

Owner income stays tight in Year 1, then improves as revenue and EBITDA scale. The big issue here is that EBITDA is not the same as cash you can take home.

| Scenario | Low CaseRamp case | Base CaseScaled case | High CaseHigh output |

|---|---|---|---|

| Launch model | This is the early ramp case, with Year 1 revenue at $365,000 and EBITDA at -$66,000. | This is the scaled operating case, with Year 3 revenue at $1.179 million and EBITDA at $409,000. | This is the mature upside case, with Year 5 revenue at $2.410 million and EBITDA at $1.226 million. |

| Typical setup | The business is still absorbing launch costs, with a $115,000 planned owner salary, 88% gross margin before payroll and overhead, and the Month 8 cash low point. | The model carries a $115,000 owner salary, 90% gross margin before payroll and overhead, about $431,000 of payroll, and $50,000 of marketing. | The business still assumes a $115,000 owner salary, 92% gross margin before payroll and overhead, about $644,000 of payroll, and $80,000 of marketing. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $115,000Salary only | $115,000Modeled pay | $115,000Upside case |

| Best fit | Use this if you want the cautious case where owner pay is funded by salary, not distributions. | Use this as the core planning case for a business that has reached steady field demand and growing crew capacity. | Use this to test strong execution, but keep in mind EBITDA is not automatic owner distribution. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Canada Goose Population Control Porter's Five Forces Analysis

- Canada Goose Population Control BCG Matrix

- Canada Goose Population Control Business Model Canvas

- What Are The 5 KPI Metrics For Canada Goose Population Control Business?

- Canada Goose Population Control Business Plan Template in Pre-Written Word

- How Increase Canada Goose Population Control Profits?

- What Are Operating Costs For Canada Goose Population Control?

- Canada Goose Population Control Startup Costs: $683k Funding Plan

- Canada Goose Population Control Financial Model Template in Excel

- How To Start A Humane Canada Goose Control Business In 6–12 Weeks

- How To Write Canada Goose Population Control Business Plan?

- Canada Goose Population Control Marketing Mix

- Canada Goose Population Control Marketing Plan

- Canada Goose Population Control Business Proposal

- Canada Goose Population Control PESTEL Analysis

- Canada Goose Population Control Pitch Deck Example Editable PPTX

- Canada Goose Population Control Business SWOT Analysis

- Canada Goose Population Control Value Proposition Canvas

Frequently Asked Questions

In this model, the owner has a planned $115,000 pre-tax salary The business itself starts at -$66,000 EBITDA on $365,000 revenue in Year 1, then reaches $137,000 EBITDA in Year 2 By Year 5, revenue is $241 million and EBITDA is $1226 million before taxes, debt service, reserves, and distributions