Owner income$85K

Owner income$85KHow Much Carpenter Ant Control Owners Make: $85K Pay To Year 5 Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$85K  Net margin-71% to 28%

Net margin-71% to 28% Revenue for target pay~$41K/mo

Revenue for target pay~$41K/mo Business difficultyHard

Business difficultyHard

This page estimates owner pay from a carpenter ant control business using a five-year operating model, not a guaranteed salary It covers revenue, margins, job volume, technician costs, marketing, callbacks, reserves, and the move from -$207K EBITDA in Year 1 to $513K EBITDA in Year 5

Owner income$85KNet margin-71% to 28%Revenue for target pay~$41K/moBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target owner pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the income model for Carpenter Ant Control Service?

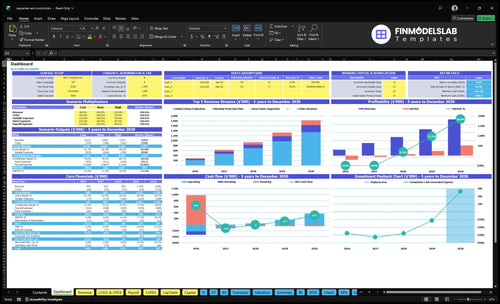

The screenshot shows the dashboard, assumptions, costs, margins, owner pay, cash need, breakeven, and low/base/high cases in the Carpenter Ant Control Service Financial Model Template; open it to test assumptions.

Owner-income model highlights

- Owner pay is built in

- Revenue and margin outputs

- Test low/base/high cases

What revenue is needed to pay a carpenter ant control owner?

You do not start with owner pay; you start with the business load. For Carpenter Ant Control Service, the provided break-even point is about $41K per month at a $450 initial-treatment ticket, which is roughly 91 treatment-equivalent jobs per month before plan revenue, inspections, callbacks, and CAC (customer acquisition cost).

Revenue floor

- $6,850 fixed overhead per month

- $232K payroll per month

- $375K marketing per month

- Owner take-home comes after this

Job math

- $450 initial treatment ticket

- ~91 treatment-equivalent jobs monthly

- Before inspections and callbacks

- Before recurring plan revenue

How much can I make with a carpenter ant control business?

With a Carpenter Ant Control Service, your early owner take-home is best viewed as the model’s $85K general manager pay, not extra profit; for startup cost context, see How Much To Start Carpenter Ant Control Service?. Profit distributions are weak at first because EBITDA is -$207K in Year 1 and -$56K in Year 2, with breakeven around Month 24.

Owner take-home

- Use $85K as early compensation

- Expect no Year 1 distributions

- Watch EBITDA, not sales alone

- Breakeven lands near Month 24

Scale upside

- Year 5 revenue reaches $1.828M

- Year 5 EBITDA reaches $513K

- EBITDA margin is about 28%

- Technicians add payroll pressure

What carpenter ant treatment profit margin should I expect?

If you’re pricing a Carpenter Ant Control Service, expect a thin first-year margin: on a $450 colony-eradication job, the provided math leaves about $371 in contribution before technician labor, marketing, callbacks, insurance, rent, software, and admin payroll. If you’re planning the offer, see How To Write A Business Plan For Carpenter Ant Control Service? Hard-to-access nests, long inspections, warranty visits, and retreatments can eat that take-home fast.

Margin drivers

- Charge more for tough nests.

- Keep inspections fast and clean.

- Cut callbacks with accurate diagnosis.

- Track every retreatment by job.

Profit risks

- Long inspections raise labor.

- Warranty visits lower take-home.

- Fuel and maintenance move fast.

- Retreatments can erase margin.

What moves owner income most?

1

$225Lead Close

More booked jobs at a lower Year 1 CAC keep the top line growing without wasting ad spend.

2

85%-95%Recurring Plan

A bigger monthly protection share smooths cash flow, and the plan price rises from $45 to $55.

3

$450-$550Ticket Size

Higher initial colony jobs lift revenue fast because each first visit is worth far more than a plan payment.

4

2-6 FTETech Utilization

Adding senior technicians grows capacity, but only if route and schedule fill those hours.

5

8.5%-6.5%Callbacks

Every redo burns labor and materials, so keeping treatment cost near the low end protects margin.

6

9.0%-7.0%Route Density

Tighter routes cut fuel and drive time, and vehicle spend falls from 9.0% to 7.0% of revenue.

Carpenter Ant Control Service Core Six Income Drivers

Lead Flow And Close Rate

Lead Flow and Close Rate

More leads only help if they turn into booked inspections and paid treatments. With a $45K Year 1 marketing budget and $225 CAC, the model implies about 200 acquired customers if spend performs as planned. If the close rate is weak, marketing turns into cash burn instead of owner pay, especially before Month 24 breakeven.

Here’s the quick math: lead volume matters, but cost per booked job and revenue per acquired customer decide profit. By Year 5, marketing rises to $140K and CAC improves to $190, so growth is only good if each lead still produces enough treatment revenue to cover labor, fuel, and overhead.

Track Bookings, Not Just Leads

Measure booked inspections, treatment close rate, cost per booked job, and revenue per acquired customer. That tells you whether the funnel is buying income or just buying calls. If close rate drops, pause spend fast and fix the sales script, inspection timing, or follow-up speed before scaling lead volume.

Use a simple rule: every lead source should show profit after CAC, not just activity. A lead that never closes still costs cash, and a low close rate can wipe out the margin from good jobs. Track by source, then cut anything that does not pay back inside the current year.

1

Average Treatment Ticket

Average Treatment Ticket

This driver is the average price collected per job, including colony eradication, inspections, and any first-month protection fee. At $450 for Year 1 eradication, $175 for a real estate inspection, and $45 per month for protection, every quote has to match nest access, moisture damage, property size, and inspection time. One low quote can erase the profit from several clean jobs.

By Year 5, prices rise to $550, $215, and $55, which helps offset labor, fuel, materials, and callback risk. The owner’s take-home income improves when the average ticket covers the true job scope and warranty exposure, because underpriced work turns into unpaid labor and weak cash flow.

Price to the job scope

Track realized ticket by job type, not just booked price. Compare eradication, inspection, and protection-plan revenue separately, then add a warranty reserve for hard-to-reach nests or moisture issues. If a job needs more inspection time or follow-up visits, the quote should move up before work starts. That keeps gross margin closer to plan.

- Quote by access and nesting depth

- Log inspection time and callbacks

- Separate one-time and monthly revenue

- Build warranty risk into pricing

Here’s the quick math: higher ticket size raises revenue without adding new leads, so it directly lifts cash for payroll, overhead, and owner draw. If pricing ignores structural complexity, the business may win the job and still lose money on labor, materials, and return visits.

2

Recurring Prevention Revenue

Recurring Prevention Revenue

Recurring prevention revenue is the monthly protection plan, starting at $45 and moving to $55 by Year 5. It smooths cash beyond one-time eradication jobs and helps cover the $6,850 monthly fixed overhead. When retention is strong, the owner gets steadier cash for payroll, fuel, and draw; when cancellations rise, lifetime value drops and the business leans back on new sales.

The key inputs are active plans, monthly price, retention, service frequency, and cancellation rate. The model also says allocation rises from 850% to 950%; that figure needs a label check before forecasting. In this line, service quality matters more than signups alone, because weak follow-through pushes churn up and cash flow down.

Improve Retention and Visit Cadence

Track cohort retention, monthly churn, and revenue per active plan. If each plan needs regular checks, build tight routes and log every service visit, because missed visits turn into cancellations. Retention beats raw signups. One clean rule: keep the plan easy to understand and easy to use.

- Measure churn by signup month.

- Price for follow-up labor.

- Record cancellation reasons.

Use fast callbacks and clear visit notes to build trust. That protects recurring income, lifts lifetime value, and makes owner pay less dependent on seasonal eradication work. If service quality slips, refunds and cancellations hit margin fast, even if monthly billing looks healthy.

3

Technician Utilization

Technician Utilization

Utilization is how much of a paid technician day turns into billable work. For this carpenter ant control service, owner income rises when completed jobs per technician day stay high and callback time stays low, because senior certified tech payroll is a big fixed bet. At 20 FTE in Year 1 and 60 FTE in Year 5, at $62K each, payroll scales from about $1.24M to $3.72M.

That means idle drive time, slow inspections, and free return visits hit profit fast. Owner-operator labor savings can help early cash flow, but once hired capacity grows, pay depends on how tightly the route is packed and how often the first treatment finishes the job. More billable visits per day lifts margin; more unplanned callbacks eats it.

Track Jobs Per Tech Day

Measure jobs per technician day, average treatment time, drive time, and callback rate. Those four inputs tell you if labor is turning into revenue or just payroll. If a tech spends too much time on the road or returns for free, utilization drops and owner draw shrinks.

- Pack routes by zip code.

- Cap unbillable drive time.

- Standardize inspection steps.

- Review callbacks weekly.

Use the same dashboard for staffing forecasts. If demand cannot fill a $62K tech, delay hiring; if routes stay dense and callbacks stay low, add capacity faster because each extra productive day supports more gross profit and steadier owner pay.

4

Callbacks And Warranty Cost

Callback Cost

Callbacks hit owner pay fast because each free revisit uses technician time, vehicle cost, materials, and schedule capacity without new revenue. For carpenter ant work, poor diagnosis, incomplete colony control, moisture damage, or hard-to-reach nests can push warranty work up. Model this with callback rate, retreatment labor hours, materials percent, and a warranty reserve.

Here’s the quick math: if pre-labor contribution is 825%, profit still depends on keeping warranty work low. A rising callback rate cuts cash flow twice: it adds direct cost and crowds out billable jobs. That lowers the owner’s draw even when top-line revenue looks steady.

Track Warranty Drag

Track callbacks by job type, technician, and cause. Separate true re-treatments from moisture or access issues, because those are different fixes and different margins. Set a reserve per job so warranty cost is priced into the ticket, not pulled from profit later.

Use one simple test each month: callback cost ÷ job revenue. If it rises, tighten inspection notes, pre-treatment photos, and access checks before quoting. Fewer callbacks protect schedule density, which protects take-home income.

- Callback rate

- Retreatment labor hours

- Materials percent

- Warranty reserve

5

<

/div>Route Density And Seasonality

Route Density and Seasonality

Route density is how many jobs you can do in one local area before drive time eats the day. For carpenter ant control, dense routes turn billable time into cash, while spread-out jobs cut jobs per day and add travel cost. With 90% Year 1 vehicle fuel and maintenance drag, every extra mile lowers margin and pushes breakeven out.

Seasonality matters just as much. Peak demand fills the schedule, but off-season gaps leave payroll and overhead uncovered, especially with $6,850 per month in fixed overhead. Property-manager accounts, real estate inspections, and protection plans matter because they can smooth demand if they are booked tightly and grouped by area.

Book by zip, not by chance

Track jobs per day, average drive time, route miles, and off-season booked volume. The goal is simple: keep technicians in one area long enough that travel does not dominate the day. Here’s the quick math: fewer dead miles means more billable stops, less fuel burn, and faster cash conversion from each labor hour.

- Group inspections and treatments by zip.

- Schedule recurring plans on fixed days.

- Use property-manager routes to fill gaps.

- Measure off-season days below target.

If routes stretch too far, jobs per day falls and payroll sits idle. Tight scheduling protects gross margin, keeps cash coming in during slower months, and makes owner pay less dependent on one-time treatment spikes.

6

Compare lean, base, and high-performance owner income scenarios

Owner income scenarios

Owner income swings hard here because revenue ramps slowly at first, CAC stays high, and staffing plus fixed overhead eat cash before volume builds.

| Scenario | Low CaseLean case | Base CaseModeled path | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lean earnings path when sales stay under the modeled break-even run rate and owner draws stay tight. | This is the modeled path that follows the research case and keeps owner pay at the $85,000 General Manager level if budgeted. | This is the stronger earnings path where Year 5 scale supports distributions only after reserves and reinvestment. |

| Typical setup | Revenue stays below the $41K monthly break-even run rate, CAC stays high, callbacks rise, and owner distributions remain limited. | Year 1 revenue is $293K, EBITDA is -$207K, breakeven lands in Month 24, and minimum cash need reaches $489K. | Year 5 revenue reaches $1.828M, EBITDA reaches $513K, the team reaches 6 senior technicians, marketing hits $140K, and CAC falls to $190. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No distributions yetCapital tight | $85K budgeted payCore plan | Post-reserve distributionsScale upside |

| Best fit | Use this to stress-test the first 24 months and check cash strain. | Use this as the main planning case for cash, hiring, and lender checks. | Use this to test upside if volume, CAC, and staffing all scale cleanly. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Carpenter Ant Control Service Porter's Five Forces Analysis

- Carpenter Ant Control Service BCG Matrix

- Carpenter Ant Control Service Business Model Canvas

- What Are The 5 KPIs For Carpenter Ant Control Service?

- Carpenter Ant Control Service Business Plan Template in Pre-Written Word

- How Increase Profits For Carpenter Ant Control Service?

- What Are Operating Costs For Carpenter Ant Control Service?

- How Much It Costs To Start A Carpenter Ant Control Service: $489K

- Carpenter Ant Control Financial Model Template in Excel

- How To Start A Carpenter Ant Control Service In 6–12 Weeks

- How To Write A Business Plan For Carpenter Ant Control Service?

- Carpenter Ant Control Service Marketing Mix

- Carpenter Ant Control Service Marketing Plan

- Carpenter Ant Control Service Business Proposal

- Carpenter Ant Control Service PESTEL Analysis

- Carpenter Ant Control Service Pitch Deck Example Editable PPTX

- Carpenter Ant Control Service Business SWOT Analysis

- Carpenter Ant Control Service Value Proposition Canvas

Frequently Asked Questions

The researched model supports $85K of pre-tax general manager pay if the owner fills that role It does not support early profit distributions because EBITDA is -$207K in Year 1 and -$56K in Year 2 Breakeven is modeled around Month 24