Owner income$150k–$1.74M

Owner income$150k–$1.74MHow Much Can a Cash Flow Forecasting Service Owner Make? $150K+

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k–$1.74M  Net margin-18% to 39%

Net margin-18% to 39% Revenue for target pay$385k

Revenue for target pay$385k Business difficultyHard

Business difficultyHard

Key Takeaways

- Raise retainer price with forecast complexity and advisory depth.

- Protect margin by keeping recurring clients above fixed costs.

- Standardize onboarding to cut cleanup and review time.

- Expand add-ons to stabilize cash and owner pay.

Owner income$150k–$1.74MNet margin-18% to 39%Revenue for target pay$385kBusiness difficultyHardWhat could your owner income be?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

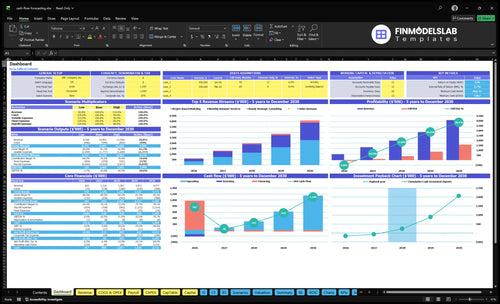

Want to check owner income in the Cash Flow Forecasting Service model?

The article already shows the dashboard, income outputs, assumptions tab, and scenario testing; use the Cash Flow Forecasting Service Financial Model Template as backup to test owner pay capacity, Month 9 breakeven, $739,000 minimum cash in Month 17, and 31-month payback. Open the model.

Owner-income model highlights

- Owner pay capacity

- Breakeven in Month 9

- Cash runway to Month 17

What should a cash flow forecasting service charge?

A Cash Flow Forecasting Service should charge for hours, complexity, and decision support, not a random markup. A practical range is $1,750 per month for a Year 1 retainer, rising to $2,200 per month by Year 5, with project work at $5,000 to $6,250 and strategic consulting at $1,250 to $1,625. If the forecast needs more cleanup, tighter reporting, or more advisory calls, the price should move up.

Retainer pricing

- $175 per hour in Year 1

- 10 hours equals $1,750 monthly

- $220 per hour by Year 5

- 10 hours equals $2,200 monthly

Project and advisory pricing

- 25-hour model: $5,000 to $6,250

- $200 to $250 per hour for modeling

- 5-hour advisory block: $1,250 to $1,625

- Charge more for data cleanup and cadence

Can a cash flow forecasting service scale beyond the owner?

Yes, the Cash Flow Forecasting Service can scale beyond the owner, but the near-term tradeoff is real: owner take-home can dip while you fund hiring, systems, quality control, and retention. The model starts lean with 1 principal consultant, 1 senior FP&A consultant, 1 junior analyst, and a half-time administrative coordinator; by Year 5 it expands to 1 principal, 5 senior FP&A consultants, 4 junior analysts, 1 business development manager, and 1 administrative coordinator. That growth lifts revenue from $602,000 to $4.077 million, while payroll rises from $367,500 to $1.165 million.

Owner-led to contractor-led

- Lower fixed cost, slower scale

- Owner control stays high

- Take-home is more variable

- Quality depends on the founder

Staffed model at Year 5

- Revenue reaches $4.077 million

- Payroll reaches $1.165 million

- More systems improve consistency

- Retention and coverage get better

What profit margin can a cash flow forecasting service have?

A Cash Flow Forecasting Service can start with weak margins, then turn very strong as the work repeats; EBITDA margin moves from -176% in Year 1 to 105% in Year 2, then 210%, 302%, and 390% by Year 5. Gross margin also improves as software and data costs fall from 120% of revenue in Year 1 to 75% in Year 5, while sales, referral, travel, and client meeting costs fall from 150% to 110%. If you want the setup path, see How Do I Launch A Cash Flow Forecasting Service?—the margin jump comes when recurring retainers rise from 600% to 800% of customer allocation and delivery gets more repeatable.

Gross margin drivers

- 120% to 75% software/data cost load

- 150% to 110% sales cost load

- Repeat work makes delivery cheaper

- Recurring retainers lift margin mix

EBITDA and owner take-home

- EBITDA margin starts at -176%

- Then hits 105% in Year 2

- Rises to 210%, 302%, 390%

- Owner take-home improves as EBITDA turns positive

What drives owner income most?

1

$602K-$4.08MClient Count

More active clients push revenue from the first year to the mature year and set the ceiling for owner pay.

2

$367.5K-$1.165MLabor Leverage

Payroll scales fast, so take-home improves only when revenue grows faster than headcount.

3

$1.75K-$2.2KRetainer Pricing

Higher monthly retainers lift revenue on the same work, and that extra spread flows straight to profit.

4

60%-80%Retention Mix

A bigger retainer share steadies cash flow and cuts the scramble to replace one-off project work.

5

88%-92.5%Delivery Efficiency

Lower tool and data costs keep gross margin high, so more of each dollar stays after delivery.

6

$6.3K/moOverhead Control

Fixed overhead is light, but every extra dollar of waste still eats owner pay before growth does.

Cash Flow Forecasting Service Core Six Income Drivers

Retainer Pricing

Retainer Pricing

Retainer pricing matters because recurring cash funds payroll and owner pay. At 10 hours per client, a $175 hourly rate gives a $1,750 monthly retainer in Year 1; at $220 per hour, that becomes $2,200 in Year 5. That is $450 more per client each month, or $5,400 a year, if workload stays at 10 hours.

What this driver includes: billable hours, forecast complexity, advisory meetings, data integrations, reporting cadence, and decision support. The risk is simple: raising price without cutting client pain or improving forecast usefulness. Price should rise only when the service produces clearer cash timing, fewer surprises, and better decisions.

Raise Price With Proof

Track hours per client, scope changes, and client response time. If a retainer takes more than 10 hours, or adds more meetings and reporting, reprice it before margin erodes. One clean rule: if the work grows, the retainer should too.

- Measure hours against the retainer fee.

- Price extra meetings and integrations.

- Link increases to clearer forecasts.

- Drop low-value work fast.

The goal is higher revenue per client without letting delivery time run wild. When the forecast is useful and workload is controlled, the owner gets better cash flow, steadier profit, and more room to pay themselves.

1

Active Client Count

Active Client Count

Owner income rises when active recurring clients cover payroll, fixed overhead, and marketing. With $50,200 in Year 1 monthly revenue and $1,750 per monthly retainer, that is about 29 retainer-equivalent clients. Each retainer uses 10 billable hours, while project work uses 25 hours, so the mix matters as much as the headcount.

Here’s the quick math: more clients help only if delivery stays tight. Fixed costs are $6,300 per month before payroll, marketing, and variable costs, so churn hits fast if updates slow down or client communication slips. One line says it all: count matters, but retained cash matters more.

Keep Recurring Clients Stable

Track active retainers, project clients, and hours per client every month. If project work keeps taking 25 hours, it can crowd out retainer work and weaken recurring cash. Use the client count to test whether revenue is enough to cover fixed costs, then leave room for payroll and owner pay.

Watch monthly close cycles, forecast reviews, and client calls for strain. If those touchpoints slip, churn risk rises before revenue does. The best control is simple: keep a clean update cadence, so clients see value, stay longer, and keep the monthly cash base steady.

2

Delivery Efficiency

Delivery Efficiency

If each client needs the same forecast every month, speed becomes a margin lever. Standard onboarding, data templates, accounting integrations, repeatable reporting, and a monthly forecast checklist cut cleanup and review time. That matters because software and data costs are 120% of revenue in Year 1 and 75% in Year 5, so wasted hours hit owner pay fast.

The key inputs are client count, number of data sources, cleanup time, update frequency, and review cycles. Automation helps with updates, but it does not replace judgment on cash timing, collections, payroll, debt service, or vendor payments. The main risk is over-automating messy client data, which creates rework and weak forecasts.

Cut Cleanup Time

Track hours per client, revision count, and days from month-end close to forecast delivery. If cleanup time falls and forecast quality holds, each consultant can handle more work, and the owner keeps more room for profit draw.

- Use one onboarding template.

- Pull data from accounting systems.

- Keep a fixed monthly checklist.

- Flag cash gaps early.

- Review exceptions, not every line.

Measure whether the forecast still drives real actions on payroll, debt service, and vendor payments. If it does, efficiency is improving income instead of just speeding up busywork.

3

Labor Leverage

Labor Leverage

Labor leverage means pushing data prep and recurring updates off the owner so senior staff can spend more time on sales, advisory calls, and quality control. In this model, headcount grows from 1 senior FP&A consultant and 1 junior analyst to 5 seniors and 4 juniors, while payroll rises from $367,500 in Year 1 to $1,165 million in Year 5.

The income effect is more capacity, lower owner delivery hours, and better service coverage. But the timing matters: if hiring runs ahead of booked work, cash gets tighter and the owner’s take-home can dip while utilization builds. The real test is whether new staff are filling billable work fast enough to cover payroll.

Hire to billable load

Track billable hours, utilization, and owner hours spent on delivery versus selling. If seniors are doing data cleanup, that’s expensive labor on low-value work. The owner should know how many client hours each role can support before the next hire lands.

Use templates, repeat update checklists, and clear handoffs so juniors handle prep and seniors handle judgment calls like cash timing, collections, payroll, debt service, and vendor payments. If utilization is still soft, delay the next hire; that protects cash flow and keeps owner pay from getting squeezed.

4

Operating Overhead

Keep Fixed Overhead Tight

Operating overhead is the monthly spend that stays on even before new client work lands: co-working space, professional liability insurance, CRM and productivi ty tools, legal and accounting retainers, telecom, internet, and content subscriptions. Here, fixed monthly costs are $6,300, so every extra dollar above that comes out of gross profit and cuts the cash available for owner pay.

Track Spend Against Billable Demand

Use client count, billable hours, and forecasted revenue to decide when overhead can grow. Annual marketing rises from $45,000 to $140,000, and startup capex totals $82,500, so adding tools before revenue density supports them can squeeze cash fast. The rule is simple: if a tool does not help deliver, sell, or collect faster, it can wait.

- Track fixed costs monthly.

- Approve tools only with demand.

- Delay nonessential software.

- Protect owner draw first.

5

Retention and Expansion Revenue

Retention and Expansion Revenue

Recurring revenue matters here because it smooths owner pay. In the model, monthly retainer allocation rises from 600% in Year 1 to 800% in Year 5, while project-based modeling falls from 300% to 100%. That shift lowers revenue swings, keeps consultant hours more predictable, and makes it easier to pay the owner from steady cash instead of lumpy project fees.

This driver includes retainers plus add-ons like scenario planning, lender package support, budgeting support, and cash runway reviews. To estimate it, track renewal rate, add-on conversion rate, billable hours per client, and how often project work turns into ongoing support. The risk is treating add-ons as one-off work, so the extra revenue disappears after the first month.

Turn add-ons into renewals

Price expansion work as part of a monthly cadence, not as a loose task list. If a client asks for a runway review or lender package, attach a follow-up review date and a clear next deliverable. That keeps revenue recurring and helps avoid idle gaps in consultant schedules. One clean rule: every project should point to the next month’s retainer scope.

- Track renewal and expansion separately.

- Convert one-offs into monthly reviews.

- Set next-step dates in every scope.

- Watch billable hours by client.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income changes fast here because revenue mix, staffing, and marketing spend drive EBITDA. Early losses can still support a founder salary, but only after cash reserves cover the gap.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path, where Year 1 stays negative before the founder can take much beyond a modest salary. | This is the modeled middle path, where the business starts paying the owner more as EBITDA turns solidly positive. | This is the stronger earnings path, where the owner benefits from scale but still does not take all EBITDA as income. |

| Typical setup | It reflects $602,000 of Year 1 revenue, -$106,000 EBITDA, and a $150,000 principal salary, so owner pay capacity is about $44,000 before taxes and reserves. | It reflects Year 3 at about $1.987 million revenue and $418,000 EBITDA, with 70% retainers, 20% project work, and 10% hourly consulting. | It reflects Year 5 at about $4.077 million revenue and $1.592 million EBITDA, with 80% retainers, 10% project work, and a larger team. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $44,000Low case band | $568,000Base case band | $1,742,000High case band |

| Best fit | Use this to test the first-year cash gap and how long reserves must last. | Use this as the planning case for budgeting owner draw and hiring. | Use this to test upside if sales scale and delivery stays efficient. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Cash Flow Forecasting Service Porter's Five Forces Analysis

- Cash Flow Forecasting Service BCG Matrix

- Cash Flow Forecasting Service Business Model Canvas

- What Are The 5 Core KPIs For Cash Flow Forecasting Service?

- Cash Flow Forecasting Service Business Plan Template in Pre-Written Word

- How Increase Profits For Cash Flow Forecasting Service?

- How Increase Profitability Of Cash Flow Forecasting Service?

- Cash Flow Forecasting Service Startup Costs: $825K CAPEX

- Cash Flow Forecasting Service Financial Model Template in Excel

- How to Start a Cash Flow Forecasting Service in 6 Launch Lanes

- How Will [Business Name] Cashflow Forecast Work?

- Cash Flow Forecasting Service Marketing Mix

- Cash Flow Forecasting Service Marketing Plan

- Cash Flow Forecasting Service Business Proposal

- Cash Flow Forecasting Service PESTEL Analysis

- Cash-Flow Forecasting Pitch Deck Example Editable PPTX

- Cash Flow Forecasting Service Business SWOT Analysis

- Cash Flow Forecasting Service Value Proposition Canvas

Frequently Asked Questions

The model includes a $150,000 principal consultant salary, but Year 1 EBITDA is -$106,000, so true pay capacity is tight If the owner adds salary plus EBITDA before taxes and reserves, capacity is about $44,000 in Year 1, $288,000 in Year 2, and $1742 million in Year 5