Owner income$145k base

Owner income$145k baseHow Much Category Management Consulting Owners Make: $145k+ Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145k base  Net margin35% to 65%

Net margin35% to 65% Revenue for target pay$1.5M

Revenue for target pay$1.5M Business difficultyHard

Business difficultyHard

A category management consulting owner can model first-year pre-tax take-home around the planned $145,000 owner salary, but the business may still show an operating loss if revenue ramps slowly Using the researched assumptions, first-year revenue is about $686,250 from a $45,000 marketing budget and $1,200 CAC, with about 78% contribution after data, cloud, commissions, and travel After $405,000 of modeled payroll, $108,000 of fixed expenses, and marketing, operating profit is about -$22,000 before reserves In the mature-year assumption, owner salary plus available profit before reserves reaches about $310 million, but only if client acquisition, pricing, staffing, and retention hold

Owner income$145k baseNet margin35% to 65%Revenue for target pay$1.5MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

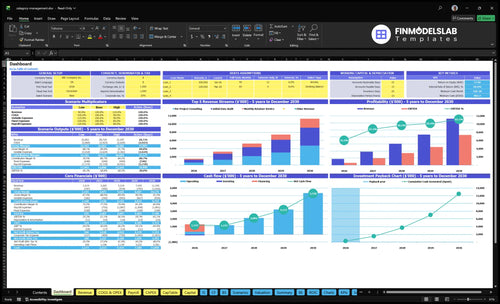

Want to check owner income in the model?

The Category Management Consulting Financial Model Template dashboard shows assumptions, revenue, costs, reserves, and owner take-home—open it.

Owner-income model highlights

- Separate revenue and profit

- Show salary, reserves, distributions

- Test CAC and margin

How much revenue does a category management consulting business need?

If Category Management Consulting has to cover a $145,000 owner salary in Year 1, it needs about $715,000 of revenue to break even before reserves. Here’s the quick math: $558,000 in fixed payroll, overhead, and marketing divided by a 78% contribution margin equals about $715,000. The researched Year 1 revenue assumption is $686,250, so it falls short by about $29,000; at $18,300 revenue per customer, break-even is about 39 customers, not 375.

Revenue target

- Need $715,000 to break even

- Use 78% contribution margin

- Fixed costs equal $558,000

- Owner salary is $145,000

Customer math

- Year 1 revenue model is $686,250

- Short by about $29,000

- Each customer приносит $18,300

- Break-even needs about 39 customers

Can a category management consulting business scale beyond the owner?

Yes—Category Management Consulting can scale beyond the owner, but only if delivery shifts from founder-led projects to standardized retainers, repeat analytics, and analyst-supported work. In the mature-year case, headcount grows from 10 FTE in Year 1 to 60 FTE by Year 5, with Senior Data Scientists rising from 10 to 20 FTE. That setup can lift revenue to about $516 million, but payroll, training, quality control, client concentration, retailer access, data quality, and lumpy demand can still cut distributions.

What helps it scale

- Use retainers instead of one-off projects.

- Repeat analytics across many clients.

- Add analysts, not just founder hours.

- Grow from 10 FTE to 60 FTE.

What can slow it down

- Payroll rises fast with headcount.

- Training takes time and cash.

- Quality control can break at scale.

- Lumpy demand and data gaps hurt margins.

How much can a solo category management consultant make?

A solo Category Management Consulting owner can keep more margin, but this model doesn’t support a clean solo income estimate because it starts with a CEO/Principal Consultant plus delivery and sales staff; for setup context, see How Do I Launch A Category Management Consulting Business?. The key math is simple: removing $260,000 in Year 1 non-owner payroll saves about $21,667/month, but it also removes analyst, retail operations, and account capacity.

Solo upside

- Keep more gross margin per client

- Avoid $260,000 Year 1 payroll

- Save about $21,667/month

- Control sales, analysis, and delivery

Solo ceiling

- Lose Senior Data Scientist capacity

- Lose Retail Operations Consultant capacity

- Lose 0.5 sales/account role

- Founder becomes the main bottleneck

Want the six income drivers?

1

$18.3K-$35KPricing Power

Per-client revenue sits around $18,300 to $35,000, so small price gains flow straight to owner income.

2

$1.5M-$11.3MClient Volume

More active clients drive the jump from $1.519M to $11.292M in revenue as marketing rises from $45K to $140K and CAC falls from $1,200 to $950.

3

8.5-10.5hUtilization

Each active client uses 8.5 to 10.5 billable hours a month, so tighter scheduling lets the same team earn more.

4

60%-80%Retainers

The mix shifts toward monthly retainers from 60% to 80%, which steadies cash and raises repeat revenue.

5

78%-84%Cost Control

Data fees fall from 8% to 6% and cloud costs from 5% to 3%, helping keep contribution margin near 78% to 84%.

6

$145KFounder Leverage

The $145K owner salary is a cost, so take-home improves when delivery shifts from founder hours to the growing team.

Category Management Consulting Core Six Income Drivers

Pricing Model And Revenue Per Client

Revenue Per Client

Category management consulting income rises when each client includes a retainer, a project, and an initial data audit. In Year 1, pricing is $175/hour for retainers, $225/hour for projects, and $200/hour for audits, which produces about $18,300 in weighted revenue per client.

By Year 5, revenue per client can reach $35,000 as the retainer mix rises to 80%, retainer hours rise to 15, and project pricing reaches $260/hour. The owner’s take-home improves when pricing tracks assortment, shelf productivity, and measurable category outcomes, not just hours logged.

Price to Measurable Retail Results

Track three inputs on every account: retainer hours, project hours, and audit fees. Here’s the quick math: revenue per client is the mix of those three services, so a better mix lifts margin without needing more logos. One clean rule: price the outcome, not the meeting.

Protect owner income by reviewing whether each client can show changes in assortment, shelf productivity, or category profit. If a client only buys low-value hours, the revenue per client falls fast and cash gets choppy. Use a simple test: if the work can’t point to a measurable shelf or category result, re-scope it or reprice it.

- Track service mix monthly

- Compare rate by work type

- Link fees to category outcomes

- Watch retainer renewal quality

1

Active Client Count And Account Quality

Active Clients and Account Quality

Active clients help income only when scope, data access, and decision speed keep delivery lean. On the stated inputs, $45,000 ÷ $1,200 ≈ 38 acquired accounts, and $140,000 ÷ $950 ≈ 147. More logos can lift revenue, but weak-fit clients add meeting drag and rework, so gross margin and owner pay can fall even as sales rise.

Qualify Accounts Early

Qualify every account on scope, data quality, and decision speed. Track active clients, hours burned, and revenue concentration by account, then price extra cleanup or pause low-fit work. If one retailer or brand starts to dominate revenue, cash flow gets fragile and renewal risk hits the owner’s draw fast.

2

Billable Capacity And Founder Utilization

Billable Capacity

Founder-led consulting income rises only if billable hours stay high without choking off sales and account care. Here, service workload per active customer runs 85 hours/month in Year 1 to 105 hours/month in Year 5, so the owner’s pay depends on turning those hours into cash while still covering proposals, meetings, cleanup, admin, hiring, and quality review.

That tradeoff matters because burnout is not a strategy. If the founder spends too much time delivering, non-billable work grows and new work slows. The real input set is active customers, billable hours per customer, retainer hours, project hours, audit hours, and the share of time lost to non-billable work.

Protect Founder Time

Track billable utilization as billable hours divided by total work hours, then watch it next to sales time and renewal work. If utilization climbs but proposals, stakeholder meetings, and follow-up slip, the business can look busy while owner income stalls.

- Set weekly billable hour limits.

- Reserve time for sales and renewals.

- Separate retainer, project, audit work.

- Measure non-billable hours by task.

A useful check is whether the mix stays close to the modeled workload: 10 to 15 retainer hours, 40 to 50 project hours, and 15 audit hours. If non-billable work keeps rising, founder pay gets squeezed even when revenue looks strong.

3

Gross Margin And Delivery Cost Control

Gross Margin and Delivery Cost Control

If data subscriptions, cloud, sales commissions, and travel stay controlled, more consulting revenue turns into cash the owner can pay out. In Year 1, those direct costs total 22% and leave 78% contribution before payroll and overhead; by Year 5, they drop to 16%, so every $100,000 of revenue keeps $84,000 before fixed costs.

The catch is simple: don’t cut core data or planogram tools just to save a few points. If analysis gets weaker, recommendations get weaker too, and churn can erase the margin you saved. One bad client renewal can cost more than a cheap tool ever did.

Track Direct Cost per Revenue Dollar

Measure direct delivery cost as (data + cloud + commissions + travel) / revenue each month. Keep the tools that drive assortment and shelf decisions, and test cuts only where client results stay intact. If travel or commissions run hot, shift more work remote and tighten sales terms before touching the analysis stack.

- Year 1 direct cost: 22%

- Year 5 direct cost: 16%

- Margin gain: 6 points

- Risk: weaker analysis raises churn

4

Retainers, Repeat Work, And Renewal Risk

Retainer Mix And Renewal Risk

Recurring work matters because it smooths owner pay. In this model, monthly retainer work rises from 60% in Year 1 to 80% in Year 5, while per-project consulting falls from 30% to 20%. That shift makes cash flow easier to forecast, but the owner’s draw depends on renewals, active retainers, project share, and how much work must be redone after each review.

Here’s the quick math: a higher retainer mix usually means less sales pressure and fewer empty months between jobs. Still, renewals are not guaranteed. If a client drops after a category review, revenue falls fast because the next month’s income is supposed to be repeat work, not a new sale. More recurring revenue helps stability, but weaker retention can hit take-home pay right away.

Protect Renewal Revenue

Track retainer share, renewal rate, and client ROI by account. Quarterly reviews, implementation follow-up, and clear ROI reporting are the main controls here because they show whether the shelf changes actually lifted sales per square foot or inventory turn. If clients can see the gain, renewals are easier to defend and the owner can plan staffing with less guesswork.

Also watch concentration risk. If too much recurring revenue sits with a few retailers, one lost renewal can cut owner pay and force a late scramble for new work. Build simple service logs for each account, tie updates to measurable category outcomes, and flag any client that has not seen a review in 90 days. Retention is the lever that keeps profit from wobbling.

5

Team Leverage And Standard ized Delivery

Team Leverage

Delivery leverage matters when the firm can add clients without adding founder hours one for one. With Retail Operations Consultant capacity moving from 10 to 60 FTE, more work can shift off the founder, but only if each engagement follows the same review steps, dashboard set, and report format. That is operating leverage: more billings per hour of leadership time.

The catch is cash. Payroll, training, management time, and quality control usually rise before new revenue does, so take-home can dip even while top line grows. To estimate the effect, track active clients, billable hours, consultant utilization, rework time, and owner hours spent on sales and review. One messy client can erase the gain from several clean ones.

Standardize Delivery Fast

Start with a repeatable delivery stack. Standardize category review agendas, repeat dashboards, and reusable reporting templates so each consultant handles more accounts with less setup work. The best test is whether a Senior Data Scientist can hand off a file and get the same output every time. If not, scale will mostly add payroll, not profit.

Watch gross margin, not headcount alone. Model payroll against expected billings, then add a buffer for onboarding and quality control. If you hire faster than the work can be standardized, owner pay drops in the near term. The goal is simple: make each new FTE raise delivered revenue faster than it raises supervision and fix-it time.

6

Compare lean, base, and mature owner income scenarios

Owner income scenarios

Owner income moves with client volume, billable hours, and team size. The low case stays lean; the high case assumes stronger recurring work and more delivery capacity.

| Scenario | Low CaseDownside case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | Lean start with modest income and a tight operating footprint. | Modeled mid-case with steadier recurring work and fuller team use. | Stronger earnings path with more clients, more billable hours, and higher profit. |

| Typical setup | Year 1 runs at $1.519 million revenue and $535,000 EBITDA, with 60% retainer work, 30% project work, and a small support team. | Year 2 reaches $3.265 million revenue and $1.667 million EBITDA as the retainer mix rises to 65% and the team expands. | Year 5 reaches $11.292 million revenue and $7.346 million EBITDA, with 80% retainer work and a much larger delivery bench. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $680kLean income | $1.812MCore income | $7.491MUpside income |

| Best fit | Use this if demand is slow and the owner still does most client work. | Use this as the working plan for budgeting and hiring. | Use this to test what happens if growth stays ahead of staffing. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Category Management Consulting Porter's Five Forces Analysis

- Category Management Consulting BCG Matrix

- Category Management Consulting Business Model Canvas

- How Increase Category Management Consulting Profitability?

- Category Management Business Plan Template in Pre-Written Word

- How Increase Profits In Category Management Consulting?

- What Are Operating Costs For Category Management Consulting?

- Category Management Consulting Startup Costs: $802k Funding Plan

- Category Management Consulting Financial Model Template in Excel

- How To Start A Category Management Consulting Business In 6 To 12 Weeks

- How To Write A Business Plan For Category Management Consulting?

- Category Management Consulting Marketing Mix

- Category Management Consulting Marketing Plan

- Category Management Consulting Business Proposal

- Category Management Consulting PESTEL Analysis

- Category Management Consulting Pitch Deck Example Editable PPTX

- Category Management Consulting Business SWOT Analysis

- Category Management Consulting Value Proposition Canvas

Frequently Asked Questions

The model starts with a $145,000 owner salary in Year 1 Under the researched assumptions, revenue is about $686,250 and operating profit is about -$22,000 before reserves, so distributions are not supported yet In the mature-year case, owner salary plus profit before reserves reaches about $310 million if acquisition, staffing, and pricing hold