Owner income$78.6k/mo

Owner income$78.6k/moHow Much Does a Catering Business Owner Make? $943K Pre-Tax

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$78.6k/mo  Net margin33.0%

Net margin33.0% Revenue for target pay$238k/mo

Revenue for target pay$238k/mo Business difficultyHard

Business difficultyHard

You’re planning owner pay before the event calendar is proven, so revenue is not the same as take-home This five-year model estimates $942,885 in first-year pre-tax operating profit before debt service, taxes, and reserves, based on researched covers, per-guest pricing, payroll, food cost, and overhead assumptions

Owner income$78.6k/moNet margin33.0%Revenue for target pay$238k/moBusiness difficultyHardWant to test your catering owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, operating costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, labor, taxes, debt, and reserves. Not guaranteed salary, tax advice, or owner distribution advice.

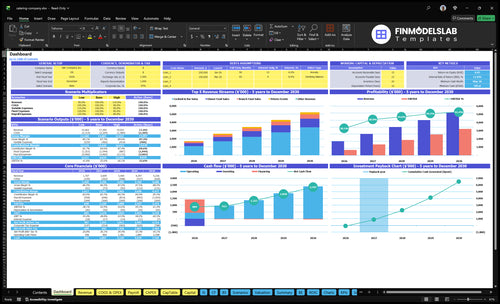

Can you check owner income in the Catering Service model?

The Catering Service Financial Model Template dashboard shows revenue, gross margin, EBITDA, owner income, and cash outputs. Open the model.

Charts compare $197 million first-year revenue, $942,885 pre-tax operating profit, $495,000 launch capex, and $17,400 monthly fixed overhead.

Owner-income model highlights

- Owner take-home and cash

- Revenue, margin, EBITDA

- Covers and price per guest

- Sales mix and ingredient cost

- Fees, supplies, payroll, overhead

- First-year, ramp, mature scenarios

What is a good profit margin for a catering business?

A good profit margin for a Catering Service is not just a strong food margin; it has to leave room for payroll, event labor, rentals, debt, taxes, reserves, and owner distributions. If you also need the startup math, see What Is The Estimated Cost To Open A Catering Service Business?. In this model, ingredient cost improves from 14% of sales in year one to 12% in the mature year, processing and supplies are shown at 3% combined, and payroll rises from $483,000 to $811,000 as volume grows. Food waste, prep labor, event staffing, rentals, and menu mix can compress that fast, so gross margin and net profit are not the same thing.

Margin math

- Ingredient cost: 14% to 12%

- Processing and supplies: 3% combined

- Payroll: $483,000 to $811,000

- EBITDA margin: 479% to 684%

What squeezes it

- EBITDA comes before debt and taxes

- Owner distributions are separate

- Food waste cuts cash fast

- Prep labor and staffing shift margins

How does catering pricing affect owner income?

For Catering Service, owner income rises when revenue per guest and margin rise, not just when menu prices go up. In year 1, pricing is $55 midweek and $75 on weekends; in the mature year it moves to $67 and $87, so a Saturday proxy jumps from 150 covers × $75 = $11,250 to 350 covers × $87 = $30,450. Mix matters too: beverages move from 65% to 60% and private events from 5% to 10%, but larger events can need more staff, rentals, delivery, and cleanup.

Revenue per guest

- $55 midweek in year 1

- $75 weekend in year 1

- $67 midweek mature year

- $87 weekend mature year

Margin and mix

- 150 covers at first-year Saturday pricing

- 350 covers in the mature year

- Beverages move from 65% to 60%

- Private events rise from 5% to 10%

Can a catering business make money without the owner at every event?

Yes, Catering Service can make money without the owner at every event, but only if booked volume covers the management layer and the handoff is tight. In year one, staffing starts at 100 FTE and $483,000 in payroll, then scales to 180 FTE and $811,000 payroll as revenue grows from $197 million to $597 million, so payroll as a share of sales falls. The catch is timing: if bookings lag after hiring a General Manager at $85,000, a Head Mixologist at $70,000, and a Chef at $65,000, owner income drops before revenue catches up.

Can it run owner-free?

- Yes, with enough booked volume.

- Management must cover each event.

- Handoffs need tight checklists.

- Staffing starts at 100 FTE.

Where the risk sits

- Payroll starts at $483,000.

- Payroll rises to $811,000.

- Revenue grows from $197M to $597M.

- Bookings lagging hurts owner income.

Want the six income drivers that matter most?

1

$1.97MEvent Volume

Year 1 sales land around $1.97M at 565 covers a week, so more booked events spread rent and staff across more revenue and lift owner take-home before taxes and reserves.

2

$55-$75Event Price

Midweek runs at about $55 per cover and weekends at $75, so small price gains flow through fast after food and labor.

3

86%Menu Margin

With ingredient cost at 14% in Year 1, every point of margin saved stays in the business and raises cash for the owner.

4

$483KLabor Efficiency

Payroll starts at $483K, so tighter staffing and better scheduling protect profit when event demand moves around.

5

$17.4K/moOverhead Control

Fixed overhead is $17.4K a month, and keeping it steady matters because these costs hit even when bookings slow.

6

5%-10%Referral Bookings

Private events grow from 5% to 10% of sales mix, and repeat corporate or venue referrals help fill weak days with better-margin work.

Catering Service Core Six Income Drivers

Event Volume

Event Volume

More catering events only raise owner pay when the kitchen, staff, and delivery flow can handle the load. In this plan, weekly volume rises from 565 covers in year 1 to 1,445 covers in the mature year, so more sales can spread rent and other fixed costs across more guest meals. That helps margin, but only if weekend demand does not overload service or force costly overtime.

Here’s the quick math: revenue rises from $197 million to $597 million as volume grows. The upside is higher fixed-cost absorption and steadier owner pay, but the risk is lopsided booking: weekends fill up while midweek capacity sits idle. If the calendar is not balanced, more revenue can still leave profit thin.

Track covers and calendar balance

Measure event count, covers per event, staff hours, and delivery turns. A cover is one guest served, so volume is not just bookings; it is how many meals the operation can actually deliver well. Watch weekday versus weekend fill, because that mix drives labor use, waste, and how much fixed cost gets covered.

- Set a cover limit by day.

- Track overtime by event.

- Compare booked vs. staffed capacity.

- Push midweek corporate fills.

What this estimate hides: extra events can still hurt cash flow if they need more prep time, more cleanup, or a new shift. The goal is not just a full calendar; it is a calendar that fills without breaking service quality or owner take-home income.

1

Average Event Value

Average Event Value

Average event value is the revenue you make per booking, based on guest count, service tier, beverage packages, rentals, and add-ons. In this model, first-year pricing is $55 midweek and $75 weekend, then rises to $67 and $87. Higher event value helps owner income only when the extra revenue adds more margin than it adds labor, supplies, or delivery time.

Here’s the quick math: a Saturday revenue proxy grows from $11,250 to $30,450. That kind of lift can improve cash and profit fast, but it can also backfire if the team has to staff a large event with custom food, rentals, and long cleanup. The key question is simple: does each bigger event leave more gross profit in dollars, not just more sales?

Track Price, Mix, and Margin

Track covers, average check per event, add-on rate, and gross margin per booking. Use them together, because a high-price event can still hurt income if it needs extra kitchen hours, weekend labor, or special rentals. A clean pricing grid for midweek versus weekend work makes owner pay easier to forecast.

Watch these inputs on every quote: guest count, service tier, beverage package, rentals, and staffing hours. If a larger event does not require equal extra staffing and supplies, profit per event rises. If it does, raise price or walk away. That keeps revenue growth tied to take-home income, not just busier weekends.

2

Menu Gross Margin

Menu Gross Margin

Menu gross margin is the cash left after food, beverage, and supply costs. With ingredients at 14% of sales in year one and 12% in the mature year, a 2-point drop lifts gross profit by $2,000 per $100,000 of sales before labor and overhead.

The risk is quoting complex menus without pricing prep time, disposables, and waste. If processing and supplies are really 3% in year one and 25% by maturity, that line must be tracked separately because it can move owner pay as much as food cost. Inputs: guest count, menu mix, recipe yields, buy prices, and waste.

Control the menu, not just the recipe

Measure cost per cover, not just the food invoice. Tie each menu to portion size, waste, and the full supply list, including disposables and prep items. When the quoted menu cost rises, raise price before the event, not after service.

- Track ingredient cost as sales %.

- Test portions on every menu.

- Quote prep, waste, disposables.

- Review purchasing on each event.

One clean rule: if a menu needs more labor or waste control, it needs a higher price. That protects contribution margin, keeps cash in the business, and makes owner draws more reliable.

3

Labor Efficiency

Labor Efficiency

Labor efficiency covers kitchen prep, event setup, service, delivery, and cleanup. It is a direct owner-income driver because payroll is $483,000 in year one and $811,000 in the mature year, while payroll as a share of revenue drops from 245% to 136% as volume scales. Labor only helps take-home pay when each event uses the right crew size and the right number of hours.

Here’s the quick math: if overtime rises, prep is messy, or small events get too many staff, payroll eats margin fast and cash gets tight. Owner labor should be tracked separately from paid labor, or take-home income gets overstated. One clean rule: if the event can run with fewer hands, profit should show it.

Track Hours, Not Just Headcount

Measure labor by event type and by task: prep, setup, service, delivery, and cleanup. Track paid hours, overtime, labor cost per cover, and owner hours separately. Use those inputs in each forecast, because a 20-cover breakfast and a wedding reception do not need the same crew mix or the same margin.

Watch for overtime, weak prep systems, and overstaffed small events. Set labor targets by event size, then test staffing plans against actual hours. If payroll per event stays flat while covers rise, owner income improves; if hours rise faster than sales, take-home pay gets squeezed.

- Track paid hours by event.

- Split owner labor from payroll.

- Flag overtime on small events.

- Standardize prep and cleanup steps.

4

Fixed Overhead Control

Fixed Overhead Control

Fixed overhead is the monthly cost floor the catering business pays even before owner pay starts. Here that floor is $17,400 a month, and $12,000 rent is about 69% of it. If booked events do not cover that base, cash gets tight fast and profit for the owner shrinks.

First-year payroll and overhead together run $57,650 per month, so the real risk is signing for space, vehicles, or licenses before bookings support them. Every fixed dollar added raises the br eak-even revenue needed to reach take-home pay, so overhead control matters as much as sales.

Track the cost floor weekly

Build the fixed-cost stack from $12,000 rent, $2,000 utilities, $750 insurance, $600 permits, $350 software, $200 music licensing, $800 maintenance, and $700 accounting and legal. Then compare those costs to booked events, not hoped-for demand. If bookings slip, pause new commitments before overhead eats gross profit.

Use a simple rule: no new lease, vehicle, or license unless current bookings can support the extra monthly burn. One clean test is whether the new fixed cost would push the business past what already booked events can cover. That keeps more cash available for operations and owner draw.

5

Repeat Corporate And Venue Bookings

Repeat Corporate And Venue Bookings

Repeat demand makes revenue easier to forecast because recurring office orders, planners, and venue referrals keep the calendar moving without starting from zero each week. In this model, private events rise from 5% of sales mix in year one to 10% in the mature year, so more income comes from repeatable business and less from one-off selling.

The owner gets steadier bookings, cleaner staffing plans, and fewer last-minute margin surprises. The main risk is depending on one venue or one corporate account; if either slows, weekly volume and take-home pay can swing fast.

Track repeat share, not just total bookings

Measure the share of sales from repeat clients, the number of active accounts, and how much comes from each planner or venue. Use those inputs to forecast weekly volume, labor, and ingredient buys. If one account drives too much revenue, the business looks busy but stays fragile.

- Track monthly repeat sales mix

- Watch one-account concentration

- Compare bookings to staff capacity

- Review margin on repeat jobs

Here’s the quick math: more repeat volume cuts marketing waste and smooths cash flow, but only if each job still covers food, labor, and delivery. If repeat clients push rushed, low-margin work, owner income can still fall even with a full calendar.

6

Compare lean, base, and high catering owner income scenarios

Owner income scenarios

Owner income moves with event mix, weekend volume, and labor load. These cases show how a slow launch, a planned year, and a mature run rate change pre-tax profit.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the tighter earnings path with lower event density and thinner profit. | This is the planned operating path with steadier demand and fuller event mix. | This is the stronger earnings path with mature volume and better pricing power. |

| Typical setup | Year 1 uses 565 weekly covers, about $1.97M annual revenue, $55 midweek AOV, $75 weekend AOV, and $17,400 monthly fixed overhead. | Year 3 uses 955 weekly covers, about $3.62M annual revenue, $61 midweek AOV, $81 weekend AOV, and the same fixed overhead base. | Year 5 uses 1,345 weekly covers, about $5.52M annual revenue, $67 midweek AOV, $87 weekend AOV, and the highest staffing load. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $650kYear 1 EBITDA | $1.88MYear 3 EBITDA | $3.21MYear 5 EBITDA |

| Best fit | Use this to stress-test launch months and slow booking periods. | Use this as the most likely run-rate case for planning and lender talks. | Use this to test upside if bookings stay full and pricing holds. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions, and they are shown before debt, taxes, reserves, and distributions.

Related Products

- Catering Service Porter's Five Forces Analysis

- Catering Service BCG Matrix

- Catering Service Business Model Canvas

- 7 Critical KPIs to Scale Your Catering Service

- Catering Service Business Plan Template in Pre-Written Word

- How to Increase Catering Service Profitability in 7 Practical Strategies

- Running Costs for a Catering Service: A Monthly Financial Breakdown

- How Much It Costs To Start A Catering Business: $585k Cash Plan

- Catering Financial Model Template in Excel

- How to Open a Catering Service in 8–16 Weeks and Book Events

- How to Write a Catering Service Business Plan: 7 Actionable Steps

- Catering Service Marketing Mix

- Catering Service Marketing Plan

- Catering Service Business Proposal

- Catering Service PESTEL Analysis

- Catering Service Pitch Deck Example Editable PPTX

- Catering Service Business SWOT Analysis

- Catering Service Value Proposition Canvas

Frequently Asked Questions

It needs about $69,458 in monthly revenue to cover first-year payroll and fixed overhead before owner pay Here’s the quick math: $57,650 in monthly payroll and overhead divided by 83% margin after ingredients, card fees, and supplies The model’s first-year revenue is $164,125 per month, leaving room before taxes, debt, and reserves