Owner income$110k/yr

Owner income$110k/yrHow Much a Channel Letter Sign Business Owner Can Make on $125M

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$110k/yr  Net margin75%

Net margin75% Revenue for target pay≈$78k/mo

Revenue for target pay≈$78k/mo Business difficultyHard

Business difficultyHard

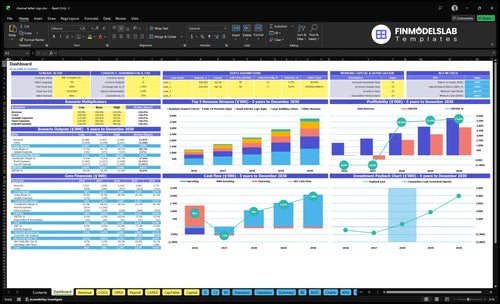

This covers a US channel letter sign manufacturer from first year through mature year, using revenue, gross margin, fixed costs, payroll, and owner pay assumptions In the supplied model, first-year revenue is $125M, with $110,000 of owner-operator pay if the owner fills the General Manager role

Owner income$110k/yrNet margin75%Revenue for target pay≈$78k/moBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, labor, overhead, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

How do I check owner income in the Channel Letter Sign Manufacturing model?

The Channel Letter Sign Manufacturing Financial Model Template shows first-year revenue of $125M and mature-year revenue of $378M, plus gross margin, operating profit, payroll, fixed costs, and owner pay. Open the model to test revenue, COGS, overhead, capex, cash flow, and owner pay.

Owner-income model highlights

- Units by product

- Margin by job type

- Owner-pay scenarios

What is the profit margin on channel letter signs?

If you’re pricing Channel Letter Sign Manufacturing, the first-year gross margin is about 794%, and standard channel letters run near 792%; for startup cost context, see How Much To Start Channel Letter Sign Manufacturing Business?. That’s gross margin, not net profit or owner income, so direct unit costs and revenue-based factory costs still matter a lot.

Margin by sign type

- Halo-lit signs: 816% gross margin

- Interior logo signs: 838% gross margin

- Large building letters: 752% gross margin

- Service work: 650% gross margin

Main cost drivers

- Aluminum affects unit cost

- Acrylic affects unit cost

- LEDs and power supplies add cost

- Fabrication labor, permit admin, heavy equipment, and electrical testing also matter

How much revenue does a channel letter sign business need?

For Channel Letter Sign Manufacturing, the revenue need is not one fixed number. Using the first-year assumptions, $614,200 of known payroll and fixed overhead divided by a 654% contribution margin points to about $940,000 a year, or $78,000 a month, before reserves or owner distributions. One universal target would be misleading.

Break-even math

- $614,200 known payroll and fixed overhead

- 654% contribution margin assumption

- About $940,000 annual revenue

- About $78,000 monthly revenue

What changes it

- Gross margin moves the target

- Debt adds cash needed

- Reserves raise the bar

- $125M revenue leaves about $204,000 operating profit

Is a channel letter sign business more profitable retail or wholesale?

For Channel Letter Sign Manufacturing, retail usually earns more per project, but wholesale can win on volume and steadier shop use. Since the model doesn’t split retail and wholesale pricing, the real choice is how much margin you trade for speed, repeat work, and cash timing.

Retail upside

- Turnkey jobs can price higher.

- Permit fees hit the margin.

- Sales costs can run higher.

- Site surveys add labor time.

Wholesale tradeoff

- Higher volume smooths fabrication.

- Pricing power usually drops.

- Cash may come in slower.

- Scaled shops need tighter control.

Want the six owner-income drivers?

1

79.4%Gross margin

At about 79.4% gross margin, every job keeps more cash for owner pay after direct build costs.

2

310-900 unitsProject volume

The unit count rises from 310 to 900, and more jobs spread fixed costs across the shop.

3

$20.4K/moFixed overhead

The $20.4K monthly base keeps break-even high, so wasted rent or admin goes straight against owner pay.

4

$4.0K-$4.2KAverage price

Average ticket stays near $4.1K, so even small price moves change cash on every order.

5

8-18 FTEShop capacity

Staffing grows from 8 to 18 FTE, and capacity has to keep up or backlog turns into lost sales.

6

2.5%-5.0%Install costs

Engineering, rigging, and permit fees can take 2.5% to 5.0% of sales on field-heavy work.

Channel Letter Sign Manufacturing Core Six Income Drivers

Project Volume and Qualified Pipeline

Project Volume

Owner income starts with signed jobs that keep fabrication and install crews busy. At 310 units in year one, that is about 26 units per month; the mature year target of 900 units only pays off if the qualified pipeline stays full and jobs keep converting on time.

The big risk is timing. Permitting delays and install slots can push sold work into the next month, so cash can lag even when sales look strong.

Track Booked Work

Watch booked revenue, deposit coverage, and scheduled production hours every week. If deposits are thin, you fund materials and labor before cash lands, and that squeezes owner pay.

- Count signed jobs by month

- Match installs to shop hours

- Collect deposits before ordering materials

- Flag permit delays fast

1

Average Project Value and Pricing Discipline

Average Project Value

Your take-home starts with the project mix. First-year average revenue is about $4,039 per unit, but jobs run from $850 service work to $12,500 large building letters. That spread means pricing discipline matters more than a headline rate, because a few underpriced custom jobs can pull down the average and leave less cash for payroll, overhead, and owner pay.

The upside comes from halo-lit upgrades, raceways, and larger storefront packages. Still, higher prices only help if win rate, specs, and cost estimates stay tight. If the quote misses labor or site complexity, the extra revenue gets eaten by rework, install surprises, and weak gross margin.

Quote the Right Mix

Track quoted price by job type, not just total sales. Compare service work, halo-lit, raceway, and storefront packages so you can see which mix lifts margin. One clean rule: if a job can’t cover materials, quoted fab hours, and install time with room left for overhead, don’t sign it.

- Measure close rate by package.

- Compare estimate vs actual labor.

- Watch change orders and revisions.

- Protect deposits before materials.

Fewer underpriced custom jobs usually beats chasing every quote. The goal is a mix that keeps cash moving, supports steady production, and leaves enough profit for owner draw after labor, materials, and fixed costs are paid.

2

Gross Margin on Materials and Shop Labor

Material and Shop Labor Margin

This driver is the gap between project revenue and the direct cost of materials and fabrication labor. The model shows $993,515 of direct gross profit on $125M of revenue, with a stated 794% benchmark. One bad estimate on aluminum, acrylic, LEDs, power supplies, paint, waste, rework, or shop hours can push owner pay down fast.

Cost pressure is not the same across jobs. Standard channel letters carry $800 of unit cost plus 30% revenue-based factory costs; halo-lit signs carry $1,050 plus 30%; large building letters carry $2,600 plus 40%. The mix matters because higher-cost jobs need tighter pricing and cleaner labor control to protect cash and profit.

Control Cost Per Job

Track cost per unit by job type, not just total shop spend. Compare quoted fabrication hours to actual hours, then flag overruns from rework, scrap, and extra paint or component use. Here’s the quick math: if labor or materials slip on a high-cost building letter, the owner absorbs the hit before overhead and pay.

- Price by unit and scope.

- Track hours by job.

- Measure scrap and rework.

- Lock material specs early.

- Review margin by sign type.

If aluminum, LEDs, and shop hours stay on budget, the owner keeps more of each project dollar as take-home income. If quoting is loose, gross margin drops first, and that leaves less room for payroll, rent, and profit draw.

3

Installation, Permits, and Subcontractor Control

Installation, Permits, and Wall-Side Cost Control

When permit filing, municipal fees, and install extras run 30% of revenue in year one and 25% in the mature year, take-home pay shrinks fast if the wall needs more work than quoted. Large building letters can also carry structural review, heavy equipment rental, rigging supplies, site survey, and permit admin at 40% of revenue plus $2,600 per unit.

Here’s the quick math: the inputs are permit count, municipal fee, access equipment, electrical scope, travel, and rework. On a $12,500 job, the install-and-permit load can hit $5,000 before fabrication margin matters. If the field surprise shows up after signing, cash gets tied up and owner pay takes the hit.

Price the wall before you sign

Use a pre-sign checklist for access equipment, electrical scope, travel, rework, and permit admin. Track actual install cost as a share of revenue by job type, and force every quote to carry the benchmark you disclosed: 30% in year one, 25% in the mature year, and 40% + $2,600 on large building letters.

- Quote structural review up front.

- Separate permit fees from fabrication.

- Pad rigging and lift rental.

- Log rework by installer and job.

If a site survey is missing, don’t book production yet. Permits and wall access decide whether deposits turn into profit, or just cover extra labor and delays.

4

Production Capacity and Labor Productivity

Labor Productivity

This driver is how many finished sign units the shop gets from each payroll dollar. Payroll rises from $370,000 in year one to $705,000 in the mature year, while output rises from 310 to 900 units. That lifts productivity from about 84 units per $100,000 of payroll to 128, so more labor dollars can turn into profit if scrap and rework stay low.

Here’s the quick math: 310 ÷ $370,000 × $100,000 ≈ 84, and 900 ÷ $705,000 × $100,000 ≈ 128. The owner wins when workflow is tighter, fabricators are trained, and bottlenecks shrink. But that gain only holds if equipment payments, maintenance, quality control, and scrap do not rise faster than output.

Track Output per Payroll Dollar

Measure units per labor dollar by shop team, not just total payroll. Split standard work from custom jobs, then watch where hours get burned on rework, wait time, and machine downtime. If payroll grows without a matching jump in finished units, owner pay gets squeezed because labor cost per unit rises and cash comes in slower.

- Track units per $100,000 of payroll.

- Log scrap and rework weekly.

- Separate standard and custom jobs.

- Check machine uptime and idle time.

- Train to reduce handoff delays.

5

Fixed Overhead, Reserves, and Owner Role

Fixed Overhead and Reserve Discipline

Fixed expenses are $20,350 per month, or $244,200 per year, before payroll. With first-year known payroll and f ixed overhead at $614,200, the business needs steady project flow just to cover the base load. The owner’s $110,000 pay is shown through the General Manager role if the owner does that work, but operating profit still is not fully spendable because taxes, debt service, working capital, maintenance, seasonality, and reserves come first.

Build the Cash Buffer Into Forecasts

Track fixed cost per month, owner pay, and an editable reserve rate separately so you can see what is truly available to draw. Here’s the quick math: every month, the business must clear overhead before owner income is safe to take home. A simple control is a cash plan that sets aside reserves before any profit draw, especially when installs slip or collections lag.

- Forecast taxes and debt first

- Set a reserve percentage

- Watch seasonal cash gaps

- Match draws to free cash

6

Compare low, base, and high owner-income scenarios

Owner income scenario table

Owner pay is tight early because minimum cash hits month 24 and breakeven lands in month 25. Later years can support salary plus profit draws as volume grows.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the cash-tight path where the shop stays below first-year volume and owner pay stays under pressure. | This is the modeled path at year 1 output, with the owner drawing the $110,000 General Manager salary while the shop works toward breakeven. | This is the stronger path where mature-year volume can support salary plus profit draws. |

| Typical setup | Volume runs below the year 1 model, the shop has spare capacity, and fixed lease, payroll, and equipment costs still sit on cash flow. | Year 1 revenue is $1.252M, EBITDA is -$45k, and the owner role is mostly working pay rather than profit distributions. | Year 5 revenue reaches $3.775M, EBITDA reaches $2.83M, and the owner can start layering distributions on top of pay. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $110,000Low Case | $110,000Base Case | Salary plus distributionsHigh Case |

| Best fit | Use this to stress-test a slow ramp and owner pay pressure before breakeven. | Use this as the core planning case for a steady operating ramp with salary-only owner income. | Use this to test a faster ramp, better mix, and a shop that stays busy enough to fund owner draws. |

Planning note: These owner-income ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions.

Related Products

- Channel Letter Sign Manufacturing Porter's Five Forces Analysis

- Channel Letter Sign Manufacturing BCG Matrix

- Channel Letter Sign Manufacturing Business Model Canvas

- What Are The 5 KPIs For Channel Letter Sign Manufacturing Business?

- Channel Letter Sign Manufacturing Business Plan Template in Pre-Written Word

- How Increase Channel Letter Sign Manufacturing Profits?

- What Are Channel Letter Sign Manufacturing Operating Costs?

- Channel Letter Sign Manufacturing Startup Costs: $689K Opening Budget

- Channel Letter Sign Financial Model Template in Excel

- How To Open A Channel Letter Sign Manufacturing Business In 10 To 18 Weeks

- How To Write A Business Plan For Channel Letter Sign Manufacturing?

- Channel Letter Sign Manufacturing Marketing Mix

- Channel Letter Sign Manufacturing Marketing Plan

- Channel Letter Sign Manufacturing Business Proposal

- Channel Letter Sign Manufacturing PESTEL Analysis

- Channel Letter Sign Manufacturing Pitch Deck Example Editable PPTX

- Channel Letter Sign Manufacturing Business SWOT Analysis

- Channel Letter Sign Manufacturing Value Proposition Canvas

Frequently Asked Questions

The supplied model supports $110,000 of salary-style owner pay in the first year if the owner fills the General Manager role It also shows about $204,000 of operating profit on $125M revenue That profit is not automatic take-home because taxes, debt service, reserves, and reinvestment still come first