Owner income$175k+

Owner income$175k+How Much Chargeback Management Service Owners Make At $126M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$175k+  Net margin-62% to 48%

Net margin-62% to 48% Revenue for target pay$368k

Revenue for target pay$368k Business difficultyHard

Business difficultyHard

A chargeback management service owner can model $175,000 in CEO salary, but that is not the same as guaranteed owner income The business shows EBITDA of -$617,000 in Year 1, -$136,000 in Year 2, then $1024M in Year 3, $2825M in Year 4, and $5975M in Year 5 Revenue scales from $1002M to $12554M as average revenue per merchant rises from about $724 to $934 per month Real take-home comes after payroll, software, marketing, reserves, debt service, reinvestment, and personal taxes

Owner income$175k+Net margin-62% to 48%Revenue for target pay$368kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Chargeback Management Service model?

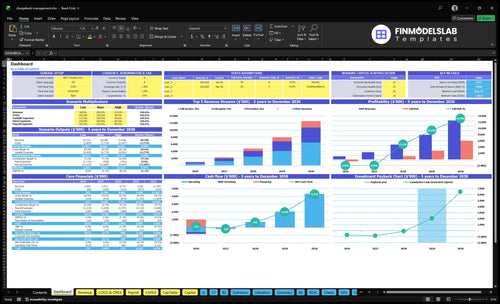

This dashboard shows revenue, EBITDA, cash, breakeven, payback, and owner income; open the Chargeback Management Service Financial Model Template.

Owner-income model highlights

- CEO salary separate from distributions

- Year 1 revenue: $1002M

- Assumptions test pricing, CAC, payroll

What margins do chargeback management services have?

For a Chargeback Management Service, the margin story improves fast as volume scales: after analyst labor, cloud, CRM, and commissions, gross margin is about 60% in Year 1 and about 79% in Year 5, but net owner income is a different test; if you’re sizing the launch, see How Much To Start A Chargeback Management Service Business?. EBITDA margin moves from negative in Year 1 to about 48% in Year 5. Reserves still matter, because minimum cash reaches -$150,000 in Month 20.

Gross margin drivers

- Cloud/data processing falls from 80% to 55% of revenue

- Sales commissions and success fees fall from 100% to 80%

- Analyst payroll rises from $195,000 to $975,000

- Gross margin reaches about 60% in Year 1

Cash and owner income

- EBITDA margin starts negative in Year 1

- EBITDA margin reaches about 48% in Year 5

- Minimum cash hits -$150,000 in Month 20

- Reserves matter before profit catches up

How many merchants does a chargeback management service need to make money?

A Chargeback Management Service needs roughly 257 active merchants to start making money, with breakeven in Month 20, not at the first signed client; see How Increase Chargeback Management Service Profitability? for the profit levers behind that timing. Here’s the quick math: Year 1 weighted ARPA is about $724/month, rising to $934/month by Year 5, while merchants must cover $186,000 in annual fixed overhead plus analyst, support, cloud, and sales work.

Merchant Count

- Year 1: about 115 active merchants

- Year 2: about 257 active merchants

- Year 3: about 481 active merchants

- Year 5: about 1,120 active merchants

Profit Levers

- Breakeven: Month 20

- ARPA: $724/month to $934/month

- Fixed overhead: $186,000 per year

- CAC: starts at $650, so retention matters

How much revenue does a chargeback management service need to pay the owner?

Chargeback Management Service can’t be sized from owner pay alone: the model starts with a $175,000 CEO salary, then adds payroll, fixed costs, marketing, variable costs, reserves, and profit. The quick rule is owner pay ÷ contribution margin, but with negative EBITDA in Year 1 and Year 2, that salary is not “safe” unless outside cash covers the early losses. Year 1 revenue is $1,002M, Year 2 is $2,311M, and Year 3 turns to $1,024M EBITDA.

Target-pay math

- Start with $175,000 owner pay

- Add payroll and fixed overhead

- Add marketing and variable costs

- Add reserves before profit

Cash reality

- Year 1 EBITDA is negative

- Year 2 EBITDA is negative

- Year 3 reaches $1,024M EBITDA

- Use funding to cover early losses

Want the six drivers that move owner income most?

1

115-1,120Merchant Retention

Keeping merchants active grows recurring revenue and spreads fixed costs over more accounts.

2

$724-$934Pricing ARPA

Higher monthly price per merchant lifts revenue without adding much extra labor.

3

-$617K-$5.98MDispute Economics

Better win rates and recovery fees can move EBITDA from a first-year loss to a fifth-year profit.

4

3-15 FTEAnalyst Productivity

More disputes per analyst keep wage growth below revenue growth.

5

20/70/10Risk Mix

A heavier mix of full service and enterprise raises revenue per account, but it also raises support load.

6

$650-$450CAC Efficiency

Lower CAC and tighter marketing spend let each new merchant pay back faster.

Chargeback Management Service Core Six Income Drivers

Active Merchant Retention

Active Merchant Retention

If merchants stay on, monthly fee revenue keeps compounding and fixed payroll gets spread across more accounts. Here’s the quick math: implied average active merchants rise from 115 in Year 1 to 1,120 in Year 5, so EBITDA should improve once fixed costs are covered; losing merchants also wastes CAC, which starts at $650 and falls to $450.

This driver depends on churn, onboarding quality, case volume, and support load. The key metric is retained active merchants by tier, because steady retention keeps recurring cash coming in and makes the owner’s draw less dependent on constant new sales.

Track Retention by Tier

Measure monthly retained merchants, churn, and retention by tier, then tie that to onboarding time and support tickets. If a merchant stays long enough to spread the fixed cost of sales and support, the business keeps more of each monthly fee and replaces fewer lost accounts.

Keep CAC honest against retention. When a merchant churns early, the business pays acquisition cost without getting enough recurring revenue back, which hurts cash flow and owner pay. Watch whether support load is rising faster than retained merchant count, because that is where margin gets squeezed.

1

Pricing And Average Revenue Per Merchant

Pricing Mix and ARPA

Your income here is driven by the mix of $249, $749, and $2,499 monthly tiers. As the mix shifts toward Full Service from 50% to 70% by Year 5, weighted ARPA rises from about $724 to $934, so revenue per merchant improves. That helps owner pay only if the extra revenue does not bring more cases than analysts can handle.

Here’s the quick math: higher ARPA lifts monthly cash in, but it can also lift review time, support load, and payroll. So the real test is gross margin per tier, not just top-line price. A tier that looks rich on paper can still hurt take-home income if it slows response times or pushes overtime.

Track Tier Margin, Not Just Price

Measure ARPA, gross margin per tier, and retention by tier every month. Also track disputes per merchant, because the higher-priced tiers only help if case volume stays inside analyst capacity. If a tier adds revenue but raises cost per case too much, it lowers owner profit, not raises it.

Use tier-level forecasting. Compare retained merchants at each price point, then test whether the $749 and $2,499 plans produce better margin after labor and support. One clean rule: if higher ARPA requires more analyst hours than you planned, the price is too low or the service scope is too wide.

2

Dispute Volume And Win Rate

Dispute Volume And Win Rate

Dispute volume is the number of chargebacks handled per merchant, and win rate is the share won through representment, meaning evidence is submitted to challenge the chargeback. This driver changes owner income because more cases can raise success-fee revenue, but only if per-dispute fee and cost per case stay under the value recovered. More cases can help margin, but only with tight control.

Model disputes per merchant, per-dispute fee, success fee rate, win rate, recovered revenue, and cost per case. Treat win rate as a sensitivity, not a promise. If review time, analyst labor, or evidence quality slips, margin and cash flow drop fast, and that lowers the owner’s draw.

- Disputes per merchant

- Per-dispute fee

- Success fee rate

- Win rate range

- Cost per case

Track Case Economics Weekly

Price for workload, not just volume. If disputes rise faster than analyst capacity, handling cost climbs and turnaround slows, which can hurt win rate. Build a monthly forecast that ties recovered revenue to actual dispute counts and a conservative win-rate range, then test whether the margin still covers payroll and overhead.

Watch merchant mix too. Some accounts create more disputes and more rework, so the same success fee can produce very different profit. One clean rule helps: if the fee from a case does not beat the fully loaded handling cost, it reduces owner pay instead of improving it.

3

Analyst Productivity

Analyst Productivity

When each analyst closes more accurate cases with strong evidence, the business keeps more recovered revenue and protects margin. The pressure point is payroll: analyst pay rises from $195,000 in Year 1 to $975,000 in Year 5, so productivity has to rise faster than headcount if owner take-home is going to hold up.

Here’s the quick math: that is a $780,000 payroll increase. If automation speeds intake, evidence checks, merchant data pulls, and case routing, you can absorb more disputes per analyst without adding weak files. Do not assume software cuts jobs; the real test is whether cost per case falls while merchant outcomes stay strong.

Track Quality, Not Just Volume

Measure disputes per analyst, review error rate, response time, and cost per case every month. If volume rises but error rate or merchant losses rise too, the team is just moving faster into bad work. Better productivity means more cases handled with clean evidence and less rework.

- Route simple cases first.

- Use evidence checklists.

- Pull merchant data automatically.

- Review win quality by merchant.

That keeps analyst payroll from outrunning revenue. Strong productivity shows up as faster turnaround, fewer rejected files, and better merchant outcomes, which supports cash flow and leaves more profit for owner pay.

4

Merchant Risk Mix

Merchant Risk Mix

If your merchant base skews to high-chargeback accounts, revenue can look stronger but owner pay can drop. Merchant risk mix is the blend of low- and high-risk clients, and it changes dispute volume, support load, compliance work, reserve holds, and churn.

The key test is risk-adjusted margin: monthly revenue minus analyst time, support time, compliance effort, and cash tied up in reserves. Low-risk merchants usually bring steadier retained revenue and fewer escalations, so the same dollar of sales can produce more usable profit.

Screen Risk Before You Sign

Score merchants before onboarding, then tie that score to pricing, service tier, contract terms, and reserve policy. One clean rule helps: if a higher-risk client needs more analyst hours than their fee covers, reprice it or pass on the deal.

Track dispute rate by risk tier, support tickets, reserve days, churn , and analyst minutes per merchant. Forecast separate bands for low- and high-risk clients so you can see whether a mix shift grows income or just adds workload. Higher owner take-home comes when risk-adjusted margin beats workload.

5

Customer Acquisition Efficiency

Customer Acquisition Efficiency

When CAC drops from $650 in Year 1 to $450 in Year 5, less cash is spent replacing churned merchants, so more money can reach owner pay and free cash flow. The catch is the annual marketing budget still rises from $150,000 to $850,000, so growth only helps if new merchants stay long enough to cover the acquisition cost.

This driver includes paid channels, referral partners, payment consultants, and ecommerce agencies. To estimate it, track channel CAC, close rate, churn by channel, and lifetime gross profit per merchant.

Track payback by channel

Measure CAC payback by source, not just total spend. Referral partners, payment consultants, and ecommerce agencies can shorten payback when merchant quality is strong, because they send better-fit accounts that stay longer and produce recurring margin. Poor-fit channels can still grow revenue, but they often cut owner distributions because cash gets tied up replacing lost merchants.

6

Compare lean, base, and high-growth owner income scenarios

Owner income scenarios

Owner income changes with merchant growth, tier mix, staffing, and marketing spend. The model turns positive in Month 20, but it still hits a $150k cash low before payback in Month 40.

| Scenario | Low CaseMinimum cash -$150k | Base CaseBreakeven Month 20 | High CasePayback Month 40 |

|---|---|---|---|

| Launch model | This is the lean owner-income case, with slower merchant growth and limited profit distributions. | This is the modeled owner-income case, with salary plus distributions tracking the forecast path. | This is the upside owner-income case, with faster merchant growth and stronger distributions. |

| Typical setup | Revenue stays below plan, retention is slower, the owner stays hands-on, and salary carries most of the income while draw capacity stays tight. | Revenue follows $1.002M, $2.311M, $4.770M, $7.942M, and $12.554M over Years 1 to 5, EBITDA moves from -$617k and -$136k to $1.024M, $2.825M, and $5.975M, and the owner takes salary plus measured profit draws. | The mix shifts toward Full Service, more analysts are added, marketing spend rises, and cash stays tighter while revenue and EBITDA run above the base path. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary only, limited distributionsLow case | Salary plus measured distributionsBase case | Salary plus stronger distributionsHigh case |

| Best fit | Use this to test the downside if sales ramp slowly or churn stays high. | Use this as the planning case for budgets, hiring, and cash tracking. | Use this to test what happens if acquisition and service mix improve faster than planned. |

Planning note: Scenario figures are researched planning assumptions for budgeting only; they are not guaranteed earnings, salary promises, tax advice, or a promise of distributions.

Related Products

- Chargeback Management Service Porter's Five Forces Analysis

- Chargeback Management Service BCG Matrix

- Chargeback Management Service Business Model Canvas

- What Are The 5 Core KPIs For Chargeback Management Service Business?

- Chargeback Management Service Business Plan Template in Pre-Written Word

- How Increase Chargeback Management Service Profitability?

- What Are Chargeback Management Service Operating Costs?

- Chargeback Management Service Startup Costs: $240K CAPEX And Month 20 Breakeven

- Chargeback Management Service Financial Model Template in Excel

- How To Open A Chargeback Management Service In 6 To 10 Weeks

- How To Write A Business Plan For Chargeback Management Service?

- Chargeback Management Service Marketing Mix

- Chargeback Management Service Marketing Plan

- Chargeback Management Service Business Proposal

- Chargeback Management Service PESTEL Analysis

- Chargeback Management Service Pitch Deck Example Editable PPTX

- Chargeback Management Service Business SWOT Analysis

- Chargeback Management Service Value Proposition Canvas

Frequently Asked Questions

The model includes a $175,000 CEO salary, but early take-home may be funded by outside cash because EBITDA is -$617,000 in Year 1 and -$136,000 in Year 2 The real profit pool appears later, with EBITDA of $1024M in Year 3 and $5975M in Year 5 before taxes, reserves, and distributions