Owner income$7.2M-$36.9M

Owner income$7.2M-$36.9MCLT Construction Owner Income On $109M To $500M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$7.2M-$36.9M  Net margin66.7%-73.7%

Net margin66.7%-73.7% Revenue for target pay$10.9M

Revenue for target pay$10.9M Business difficultyHard

Business difficultyHard

A cross-laminated timber construction business owner can make only what remains after direct project costs, operating expenses, reserves, debt service, reinvestment, and taxes In the researched assumptions, revenue grows from $1086M in Year 1 to $5005M in Year 5 Listed direct gross profit is $884M to $4163M, or 813% to 832%, before overhead and owner withdrawals Actual CLT construction business owner income is not fixed because overhead, bonding, working capital, and owner role are not provided

Owner income$7.2M-$36.9MNet margin66.7%-73.7%Revenue for target pay$10.9MBusiness difficultyHardWant to test your CLT owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

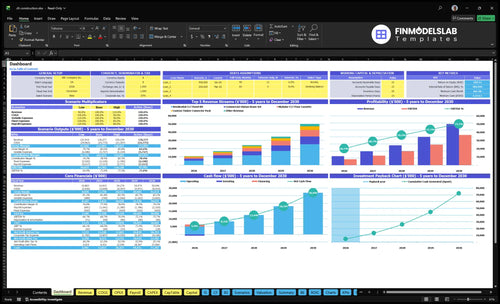

How do owner income assumptions look in Cross-Laminated Timber Construction?

The dashboard shows revenue build-up, product assumptions, COGS, reserves, and owner take-home scenarios in the Cross-Laminated Timber Construction Financial Model Template; open it.

Owner-income model highlights

- Owner take-home scenarios

- Revenue climbs $1.086B to $5.005B

- Direct gross margin 813%-832%

- Product-level contribution view

- Unit COGS, variable costs

- Overhead, reserves, assumptions

How much can a CLT construction business owner make?

A Cross-Laminated Timber Construction owner’s pay isn’t a fixed salary; it depends on how much gross profit survives overhead, reserves, debt, taxes, and reinvestment. In the modeled case, revenue grows from $1.086M in Year 1 to $5.005M in Year 5, with direct gross profit rising from $884K to $4.163M; see How Launch Cross-Laminated Timber Construction Business? for the setup path.

Owner Pay Logic

- Year 1 revenue: $1.086M

- Year 1 gross profit: $884K

- Year 3 gross profit: $1.997M

- Year 5 gross profit: $4.163M

What Reduces Take-Home

- Project managers and estimators

- Bonding and working capital

- Debt, taxes, and reserves

- Up to 30% faster build time

Is CLT construction profitable for a small owner-led company?

Yes, Cross-Laminated Timber Construction can look profitable on paper, but cash timing can block owner payouts in Year 1. The Year 1 view shows $1086M revenue and $884M direct gross profit before overhead, so the real question is whether completed work gets collected fast enough to fund operations.

What helps profit

- Owner-led management can keep overhead lean.

- Margin-positive jobs support paper profit.

- Backlog conversion drives real revenue.

- Preconstruction accuracy protects job margins.

What can break it

- Working capital can trap cash in projects.

- Bonding capacity can limit larger jobs.

- Scaled teams add payroll and software costs.

- Coordination risk rises as volume grows.

What CLT construction profit margin should owners watch?

For Cross-Laminated Timber Construction, What Is Your Business Idea Name?, owners should watch gross margin first, then net profit and owner take-home separately. The model’s listed direct gross margin is 813% in Year 1, 823% in Year 3, and 832% in Year 5, but that is not cash in hand yet. Here’s the quick math: unit COGS includes $7,000 residential panel kits, $4,500 beam sets, $2,600 staircases, $1,500 floor cassettes, and $640 connector packs, and direct revenue-based costs add 20%.

Gross margin watch

- Track 813% in Year 1.

- Track 823% in Year 3.

- Track 832% in Year 5.

- Do not call markup profit.

Cash reality

- Use $7,000 for panel kits.

- Use $4,500 for beam sets.

- Use $2,600 for staircases.

- Use 20% for added costs.

Want to see the main CLT income drivers?

1

745-3,050Project Volume

More project units push revenue from about $10.9M in Year 1 to $50.0M in Year 5, so take-home scales with job count.

2

$14.6K-$16.4KAvg Contract

Raising revenue per unit lifts cash per job without needing the same jump in sales effort, which helps owner profit faster.

3

81%-83%Gross Margin

Keeping direct gross margin in this range leaves more gross profit after timber, labor, and freight before overhead cuts into take-home.

4

124-161/FTELabor Productivity

Higher output per full-time employee spreads labor across more units, so scaling does not eat the owner's profit.

5

$35K/moOverhead Control

Holding fixed overhead near this level keeps the break-even load low and leaves more profit after the shop is staffed.

6

$1.1MCash Reserves

This cash floor protects the business in Month 1 and helps avoid forced borrowing or rushed cuts that would hit owner income.

Cross-Laminated Timber Construction Core Six Income Drivers

Completed project volume and backlog conversion

Completed Revenue From Backlog

Owner income rises only when backlog turns into completed, collected, margin-positive revenue. Modeled unit volume grows from 745 in Year 1 to 3,050 in Year 5, and revenue rises from $1,086M to $5,005M. If work is signed but not built, billed, and collected, it does not pay the owner.

Here’s the quick math: more projects help only if crews, subcontractors, bonding, and cash can absorb them. Push backlog too fast and you get margin leaks, delays, and working-capital strain. One clean rule: volume that can’t be delivered on time is not income.

Track Conversion and Cash Timing

Track booked units, completed units, collected revenue, and backlog aging every month. The gap between signed work and finished work shows whether growth is real or just paper. Also watch labor availability, subcontractor capacity, and bonding headroom before you accept more volume.

- Compare booked vs. completed monthly.

- Track billed but uncollected amounts.

- Cap backlog to crew capacity.

- Flag jobs with margin leaks early.

If cash gets tight, owner pay should wait until the work is billed and collected. Higher volume only lifts take-home income when it stays cash-positive and does not force expensive overtime, rework, or emergency financing.

1

Average contract value and project mix

Average Contract Value and Project Mix

Product mix drives revenue quality. In Year 1, a residential panel kit is $45,000, a beam set is $28,000, a staircase is $12,500, a floor cassette is $8,500, and a connector pack is $3,200. A heavier mix of panel kits and beam sets lifts average contract value and owner income more than a connector-heavy backlog.

By Year 5, those prices rise to $50,648, $31,514, $14,069, $9,567, and $3,602, or about 12.6% higher across the board. Bigger packages bring bigger revenue, but they also raise coordination risk, working capital exposure, and owner management load, so cash and profit only improve if billing keeps pace with fabrication and site work.

Track Mix, Protect Cash

Measure the share of each package type, then calculate weighted average contract value as booked value divided by project count. Use the mix to test whether more high-ticket work is actually improving collected revenue, not just signed work. If bigger packages extend the cash cycle, owner pay gets squeezed even when sales look strong.

- Track units by package type.

- Track billed value by project.

- Track days from order to cash.

Set pricing and approval rules for larger jobs, then compare margin and cash impact before taking more of them. The right mix is the one that lifts revenue without forcing the owner to fund too much work in progress.

2

Gross margin after direct job costs

Direct Job Margin

Gross margin is the first filter on owner pay. In cross-laminated timber construction, direct job costs include certified panels, fabrication labor, CNC machine time, freight, beam stock, brackets, lifting inserts, and connector fabrication. With listed unit COGS plus 20% revenue-based direct costs, the model shows 81.3% Year 1 gross margin and 83.2% Year 5 gross margin.

Here’s the quick math: if a job bills $100 and $17 to $19 goes to direct cost, the rest has to cover overhead, reserves, debt service, and reinvestment before owner draw. If panel yield, freight, or labor hours slip, gross profit falls even when revenue looks strong.

Track Job Cost Leakage

Track margin by job, not just by month. Compare budget versus actual for material takeoffs, fabrication hours, CNC time, freight, and install waste on every project. The key inputs are revenue, direct cost dollars, and direct cost %; that tells you whether each unit is earning cash or just creating volume.

Improve it by locking specs early, reducing rework, and pricing freight and special hardware separately. One clean rule: if direct job cost rises faster than invoice value, gross margin falls and the owner gets paid later or less.

3

Labor productivity and installation efficiency

Labor Efficiency

This driver covers fabrication and install labor for panel kits, beam cutting, staircase assembly, insulation layering, and connector welding/machining. The listed direct labor totals $3,080 per comparable package. If crews cut wasted hours and rework, that drops job cost fast; if they miss the schedule, overtime and idle equipment can erase margin.

Estimate it with actual hours per unit, crew size, rework rate, and downtime. A 10% labor gain saves $308 on that $3,080 bucket, but only if the job is built with the same output and no hidden delays. One line matters most: paid hours should fall before revenue does.

Track Hours, Not Just Output

Watch labor hours per panel, beam, stair, and connector, plus rework and equipment idle time. If the crew is on site but waiting on materials or crane time, gross margin can look fine while cash flow gets weak. Productivity only helps owner income when it lowers real job cost or protects the close date.

Keep a simple job log: budgeted hours, actual hours, delay causes, and overtime. Use it to price repeat work, size crews, and plan the install sequence. If one trade or lift step keeps slipping, fix that handoff first, because poor coordination is usually where profit leaks out.

4

Overhead, preconstruction, and fixed cost control

Overhead and fixed cost control

Overhead is the spend that keeps the company running but does not sit on one job: estimating, project management, building information modeling (BIM) coordination, insurance, bonding, office staff, software, sales, and administration. Because the source data does not list these costs, owner income cannot be finalized yet. No overhead split, no clean owner draw.

Lean overhead lifts take-home pay because more gross profit stays above the line. But if fixed cost is too heavy, the business needs enough gross profit from $1,086M to $5,005M in revenue to support the team. If overhead grows faster than collected margin, cash gets tight and owner pay gets pushed out.

Track overhead by job and by month

Separate direct job costs from overhead in the model. That means one view for panels, labor, freight, and installation, and another for preconstruction, PM, BIM, insurance, bonding, office, software, sales, and admin. If you mix them, you can’t tell whether a project is truly profitable or just covering payroll.

Set a monthly overhead cap and test it against collected gross profit, not signed backlog. Track the overhead ratio, the preconstruction burn rate, and how many projects each PM can handle. If headcount rises before revenue is collected, owner distributions usually slip first. Keep this line sharp: more overhead only works when gross profit scales with it.

- Track overhead by cost bucket

- Review it monthly

- Separate job cost from admin

- Match staff to collected revenue

5

Reserves, cash timing, and reinvestment

Cash reserves and timing

Profitable CLT jobs can still limit owner pay when cash is tied up in material deposits, progress billing, retainage, bonding, debt service, or equipment buys. Year 5 revenue of $5005M needs far more working capital than Year 1 revenue of $1086M, so reserve policy has to sit between gross profit and owner take-home. Profit is not cash.

The owner’s draw depends on contract value, deposit timing, billing schedule, retainage %, direct material outlays, loan payments, and planned equipment needs. If reserves are too thin, the business can show profit but still run short on cash. The practical result is lower near-term distributions but safer delivery capacity and fewer project delays.

Measure the cash gap

Track cash collected versus cash spent every month, and hold back distributions until the reserve covers the gap. Here’s the quick math: if progress billing lags purchases or retainage is still open, the reserve should fund that delay before any owner draw goes out.

- Progress billing timing

- Retainage balance

- Debt service due

- Equipment needs

- Month-end cash reserve

Use the reserve field to answer one question: can the next build start without borrowing stress? If not, reinvest first and distribute second. That keeps cash available for labor, freight, and the next project wave.

6

Scenario objective

Scenario table

Owner income moves with volume, product mix, and cost control, but the final take-home still depends on overhead, debt, taxes, reserves, and reinvestment.

| Scenario | Lean CaseLean | Base CaseBase | High-Growth CaseHigh Growth |

|---|---|---|---|

| Launch model | Lean Case is the lower take-home path. | Base Case is the modeled middle path. | High-Growth Case is the stronger take-home path. |

| Typical setup | Year 1 output is 745 units, with about $10.86M revenue, $8.84M direct gross profit, and 81.3% gross margin. | Year 3 output is 1,610 units, with about $24.28M revenue, $19.97M direct gross profit, and 82.3% gross margin. | Year 5 output is 3,050 units, with about $50.05M revenue, $41.63M direct gross profit, and 83.2% gross margin. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Lean take-home bandLean case | Base take-home bandBase case | Upside take-home bandHigh growth |

| Best fit | Use this to stress-test cash when volume starts slow or costs run hot. | Use this as the working plan for lender, investor, and owner planning. | Use this to test the upside if throughput scales cleanly and overhead stays controlled. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Cross-Laminated Timber Construction Porter's Five Forces Analysis

- Cross-Laminated Timber Construction BCG Matrix

- Cross-Laminated Timber Construction Business Model Canvas

- What Are The 5 Core KPIs For Cross-Laminated Timber Construction Business?

- Cross-Laminated Timber Business Plan Template in Pre-Written Word

- How Increase Profits Cross-Laminated Timber Construction?

- How Increase Profitability Of Cross-Laminated Timber Construction?

- CLT Construction Startup Costs: $84K Opening-Month Burn Before CAPEX

- Cross-Laminated Timber Construction Financial Model Template in Excel

- How To Start A CLT Construction Company In 6 To 12 Months

- How To Write A Business Plan For Cross-Laminated Timber Construction?

- Cross-Laminated Timber Construction Marketing Mix

- Cross-Laminated Timber Construction Marketing Plan

- Cross-Laminated Timber Construction Business Proposal

- Cross-Laminated Timber Construction PESTEL Analysis

- Cross-Laminated Timber Construction Pitch Deck Example Editable PPTX

- Cross-Laminated Timber Construction Business SWOT Analysis

- Cross-Laminated Timber Construction Value Proposition Canvas

Frequently Asked Questions

Owner income cannot be stated from revenue alone The source model shows $1086M in Year 1 revenue and $5005M in Year 5 revenue, with direct gross profit from $884M to $4163M The owner’s actual take-home depends on overhead, reserves, debt service, taxes, reinvestment, and whether the owner takes payroll