Formula Errors Caught Early

I used to worry one broken formula would throw off the whole model. This template made it easier to spot issues fast, and I cut my checking time by about 3 hours.

I used to worry one broken formula would throw off the whole model. This template made it easier to spot issues fast, and I cut my checking time by about 3 hours.

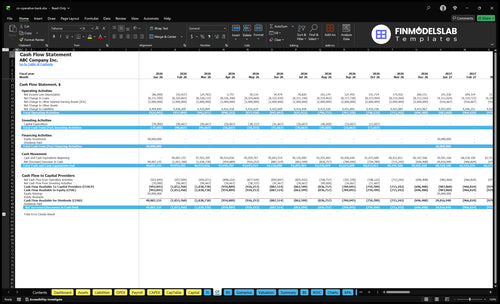

The cash flow view finally showed me when pressure could hit, instead of guessing. I mapped runway and shortfalls in one sitting, which saved me a full day of spreadsheet work.

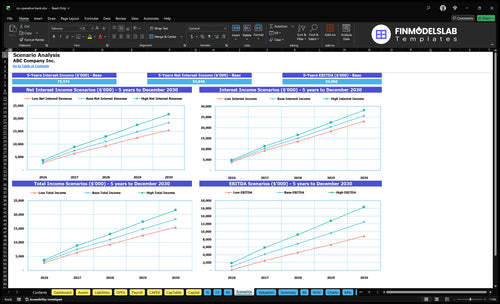

Low, base, and high cases used to take forever to rebuild. Here, I switched assumptions cleanly and had all three scenarios ready for a meeting the same afternoon.

Get started on your financial planning right away with our instant download excel template for credit union financial analysis.

Core inputs and core outputs

Three scenario analysis

Presentation ready

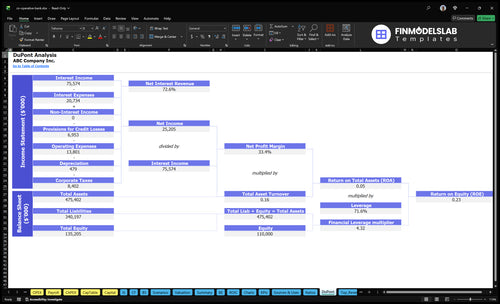

DuPont analysis

Researched revenue assumptions

Lender-friendly financial outputs

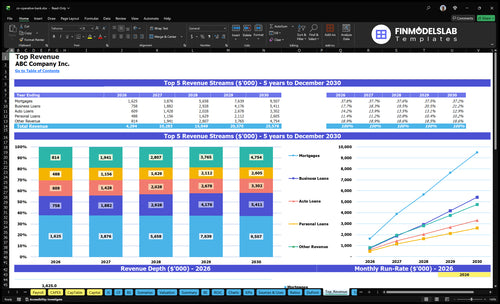

Revenue stream detailed view

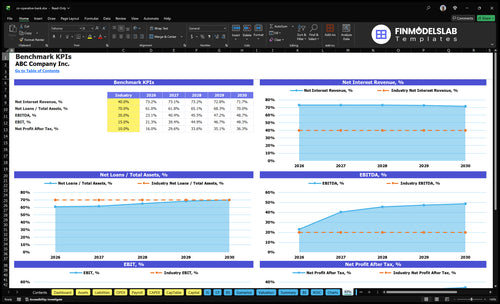

Performance metrics benchmark

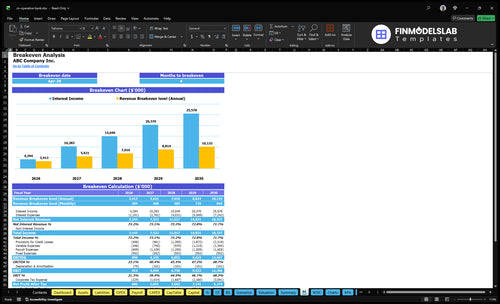

We built this cooperative bank financial model with our own industry research to give you a running start. Key assumptions for a new member-owned banking institution—like loan portfolio mix, deposit costs, staffing, and capital investments—are pre-populated but fully editable. For instance, the model projects reaching break-even by April 2026 and growing EBITDA to over $4.1 million by the second year, providing a solid baseline for your financial feasibility study cooperative bank template.

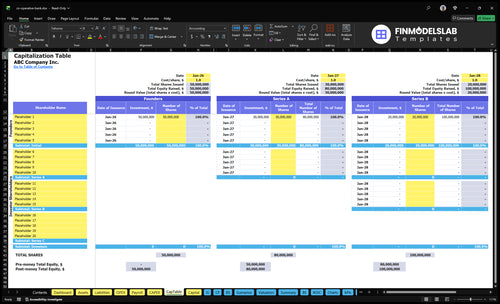

How much startup capital is needed?

To get your cooperative bank off the ground, you'll need an initial investment of approximately $505,000. This covers all major one-time capital expenditures required before opening your doors. The largest costs are the branch build-out and the core banking software license, which are essential for establishing a physical presence and the technological backbone of your operations. This defintely helps in creating a financial model for a community bank.

What are the cash flow dynamics?

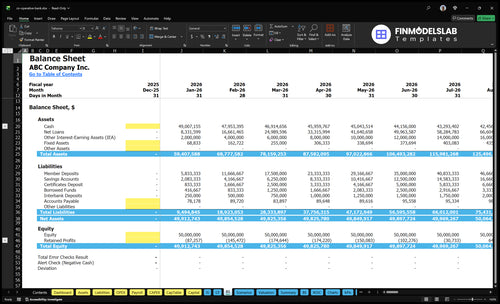

Managing liquidity is paramount for any bank. This financial model provides detailed monthly cash flow projections to ensure you can meet obligations and regulatory requirements at all times. The forecast shows your lowest cash point occurring in December 2026 with a minimum balance of $39.5 million, giving you a clear target for managing your capital reserves during the critical first year of operations.

What is the profitability outlook?

Profitability is projected to be achieved quickly, with a break-even date of April 2026, just four months after launch. The key is managing the spread between asset yields and funding costs while controlling operating expenses. The model shows EBITDA growing steadily from $990,000 in the first year to over $12.4 million by year five, demonstrating a strong path to sustainable financial performance for your member-owned financial institution.

Your cooperative's revenue is primarily driven by Net Interest Income—the spread between the interest you earn on assets and the interest you pay on liabilities. The model calculates this by forecasting average balances and yields for assets like mortgages and business loans, then subtracting the cost of funds from member deposits and other borrowings. In the first year, total loans are projected at $100 million, growing to $335 million by year five.

What are the main operating costs?

Your ongoing operational costs are driven by staff salaries, technology, and premises. The model projects total year-one payroll at $735,000 for a team of 8.5 full-time equivalents (FTEs). Fixed monthly expenses, including rent, utilities, and software licensing, total $46,000. Variable costs like marketing are modeled as a percentage of revenue, starting at 8.0% and decreasing as the bank scales.

How is the staffing plan structured?

The model outlines a phased staffing plan that grows with your institution. You start in 2026 with a core team including a CEO, Branch Manager, two Loan Officers, and three Tellers. The plan scales headcount methodically, adding a Compliance Officer in 2027 and expanding the number of tellers and loan officers in subsequent years to support a growing member base and loan portfolio, ensuring your credit union budget planning is realistic.

What are the key financial metrics?

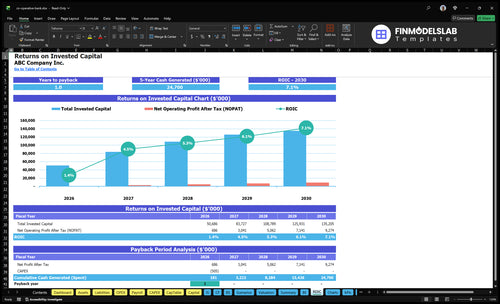

This model provides a clear snapshot of your cooperative's projected financial health and investment potential. The payback period is estimated at just 12 months, showing a rapid path to recovering initial investments. While the initial Internal Rate of Return (IRR) is -0.11%, reflecting heavy upfront investment, the Return on Equity (ROE) of 0.23% in the first year indicates positive underlying profitability for members once operations are established.

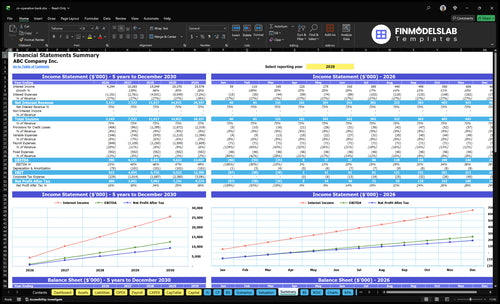

Planning for the long term is critical for any financial institution. Our cooperative bank financial model provides a complete five-year forecast, including detailed income statements, balance sheets, and cash flow statements. This helps you understand your mutual bank's financial trajectory, test different growth scenarios, and present a clear, data-driven vision to members and regulators.

Detailed monthly and annual forecasts

Integrated three-statement financial model

Scenario planning for interest rate changes

Valuation based on long-term performance

Your team needs to collaborate effectively, regardless of their preferred software. This excel financial model for banks is designed to work seamlessly in both Microsoft Excel and Google Sheets. This flexibility ensures everyone on your team can access, edit, and share the financial plan in real-time, making your credit union budget planning process much smoother.

Works on both Windows and Mac

Share and collaborate with your team online

No complex software installation required

Maintains formatting and formulas across platforms

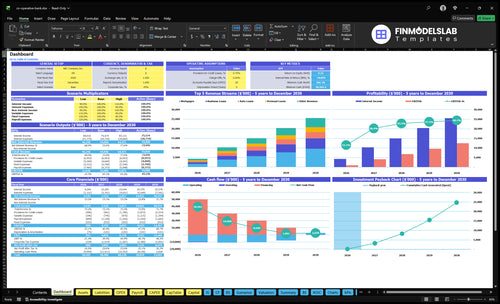

You need to see the big picture at a glance. The model includes a dynamic dashboard that visualizes your most important financial metrics. With charts and graphs for revenue trends, profitability, and cash flow, you can easily track your progress and present key insights to your board or potential investors without getting lost in spreadsheets.

Visualize key performance indicators (KPIs)

Track loan portfolio and deposit growth

Monitor profitability and break-even analysis

At-a-glance view of your bank's financial health

You need a model that fits your specific cooperative bank, not a generic template. This credit union financial template is 100% editable, allowing you to easily adjust all key assumptions, from loan portfolio growth to deposit interest rates. This saves you from building a complex banking financial projections model from scratch while giving you total control to reflect your unique strategy.

Adjust loan types and interest rates

Modify deposit mix and cost of funds

Customize staffing and operational costs

Input your own capital expenditure plan

Getting a handle on your costs is the first step to profitability. This template provides a clear breakdown of both initial startup investments and ongoing operational expenses. You can easily budget for one-time costs like a branch build-out and plan for recurring expenses like core system licensing and staff salaries, ensuring your cooperative bank startup financial plan is grounded in reality.

Detailed capital expenditure (CAPEX) schedule

Separate sections for fixed and variable costs

Staffing plan with salary and FTE forecasts

Clear assumptions for all major expenses

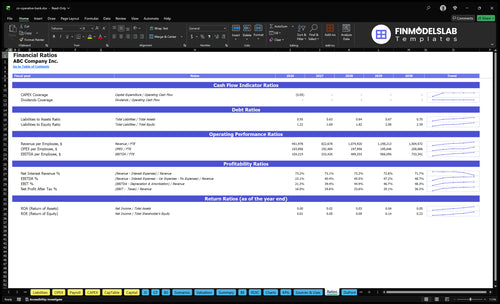

How do you know if your projections are realistic? We've built this model with key banking sector analysis metrics in mind. You can track critical Key Performance Indicators (KPIs) like Net Interest Margin, Return on Equity (ROE), and efficiency ratios. This allows you to compare your performance against industry standards and make informed adjustments to your strategy.

Track Net Interest Margin (NIM)

Monitor Return on Assets (ROA) and ROE

Analyze loan-to-deposit ratios

Assess capital adequacy and liquidity

When you're seeking funding or presenting to stakeholders, appearances matter. This template is formatted for a clean, professional presentation that meets the high standards of investors and regulators. The clear layout, organized assumption tabs, and polished charts ensure your cooperative banking business plan financial projections are credible and easy to follow.

Clean and organized financial statements

Print-ready reports and summaries

Designed to answer investor questions

Consistent and professional design throughout

After your purchase, simply download the files and open them with your preferred software, such as Microsoft Office or Google Docs. No special setup or technical expertise required—just get started right away.

Update any details, text, or numbers to reflect your specific business idea or scenario. The templates are fully editable, allowing you to personalize content, add or remove sections, and adjust formatting as needed.

Once your templates are customized, save your final versions in your preferred folders or cloud storage. Organize your files for quick access and future updates, making it easy to keep your business documents up to date.

Export, print, or email your finalized files to showcase your document. Present your professional documents in meetings or submissions, supporting your business goals and decision-making process.

It delivers investor-ready design packed with pro KPIs like ROE at 0.23 and EBITDA hitting $12,467K in year 5. You'll get polished P&L statements and cash flow forecasts that match what stakeholders expect, no guesswork. Plus, detailed assumptions section lets you tweak everything transparently. Breakeven lands in just 4 months.