Owner incomeN/A

Owner incomeN/AHow Much Cocoa Processing Owners Make: $960K Year 1 Revenue Case

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeN/A  Net margin-7.9% to 52.8%

Net margin-7.9% to 52.8% Revenue for target pay$960k-$3.41m

Revenue for target pay$960k-$3.41m Business difficultyHard

Business difficultyHard

Using the provided assumptions, a US cocoa processing business can generate $960,000 in Year 1 revenue from 33,000 finished units, rising to $341 million in Year 5 from 104,000 units Listed COGS produces about $872,460 gross profit in Year 1 and $312 million in Year 5, before unprovided fixed overhead, loan payments, taxes, and reserves Owner income is the cash left after those items, so it should be planned as a scenario, not a guaranteed salary The biggest swing factors are throughput, product mix, cocoa bean cost, pricing, labor, utilities, compliance, and working capital timing

Owner incomeN/ANet margin-7.9% to 52.8%Revenue for target pay$960k-$3.41mBusiness difficultyHardWant to test your cocoa processing take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Cocoa Processing forecast?

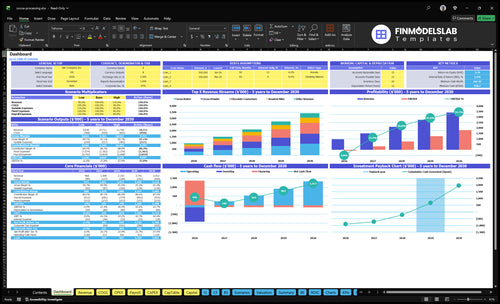

This dashboard shows revenue, gross profit, margin, costs, reserves, and owner pay; open the Cocoa Processing Financial Model Template.

Owner-income model highlights

- Owner pay output

- Revenue rises to $3.41M

- Year 1 to 5 scenarios

How do cocoa powder, cocoa butter, cocoa liquor, and chocolate margins differ?

Margins differ mainly by sale price and unit COGS, and on the supplied Year 1 fields Cocoa Processing shows a negative paper spread; for startup context, see How Much Does It Cost To Open, Start, Launch Your Cocoa Processing Business?. Cocoa powder is $25 vs $195 COGS, butter is $35 vs $290, couverture is $40 vs $365, Cocoa Liqueur is $30 vs $295, and roasted nibs are $20 vs at least $130. Don’t rank one product as best: yield loss, demand, grade, packaging, certifications, channel, and buyer terms can change take-home.

Price gaps

- Powder: $25 vs $195

- Butter: $35 vs $290

- Couverture: $40 vs $365

- Cocoa Liqueur: $30 vs $295

Margin drivers

- Roasted nibs: $20 vs at least $130

- Yield loss changes take-home fast

- Packaging adds cost per unit

- Buyer terms can move net margin

How do small-batch and commercial cocoa processing income differ?

Small-batch Cocoa Processing income is driven by owner labor, batch scheduling, premium pricing, and tight cash, while commercial profit depends on utilization, buyer contracts, equipment uptime, and cash to fund beans and receivables. On the path from 33,000 finished units in Year 1 to 104,000 in Year 5, bigger volume can help, but it does not guarantee more owner take-home if discounts, labor, repairs, compliance, or debt service absorb the added gross profit. The real test is whether each added unit still leaves enough margin after all the fixed and working-capital costs.

Small-batch income

- Owner labor drives earnings.

- Premium pricing matters most.

- Batch timing limits cash flow.

- Tight working capital slows growth.

Commercial profit

- Utilization sets unit cost.

- Buyer contracts stabilize sales.

- Equipment uptime protects output.

- Beans and receivables need cash.

How much can a cocoa processing owner pay themselves?

A Cocoa Processing owner can pay themselves only from cash left after profitable throughput, fixed overhead, debt service, taxes, reserves, and reinvestment; the model shows $872,460 Year 1 gross profit and $3,121,060 Year 5 gross profit before those items, so that is not take-home pay. Track What Is The Most Critical Measure Of Success For Your Cocoa Processing Business? before setting salary or draws, because inventory buys and receivables can trap cash even when profit looks strong.

Pay comes last

- Start with $872,460 Year 1 gross profit

- Subtract fixed overhead first

- Cover debt service and taxes

- Fund reserves and reinvestment

Cash rules pay

- Use salary for payroll consistency

- Use draws for excess owner cash

- Retain cash for bean inventory

- Receivables can delay withdrawals

Want to see what really moves cocoa processing income?

1

33K-104KThroughput Utilization

Output rises from 33K units in Year 1 to 104K in Year 5, so fixed costs get spread over far more product and owner income improves fast.

2

$20-$40Product Mix

Pushing more volume into the $40 couverture and $35 butter lines lifts margin more than leaning on lower-price powder and nibs.

3

$48K-$155KBean Cost

Raw cocoa bean spend scales with volume, and tighter buying matters because bean inputs run from $1.00 to $2.00 per unit across products.

4

$960K-$3.41MPricing Power

The same operating plan moves revenue from $960K in Year 1 to $3.41M in Year 5, so channel mix and price discipline drive take-home.

5

$1.55-$3.65Cost Control

Per-unit COGS runs from $1.55 for roasted nibs to $3.65 for couverture, plus 0.9% of revenue in production costs.

6

$439KCash Discipline

Minimum cash bottoms at $439K in Month 13, so inventory, receivables, repairs, debt, and certification spend can delay owner income before taxes and distributions.

Cocoa Processing Core Six Income Drivers

Throughput Utilization

Throughput Utilization

Throughput utilization means turning plant capacity into sellable output. Here, production rises from 33,000 units in Year 1 to 104,000 units in Year 5, and revenue climbs from $960,000 to $3,410,000. That extra volume can raise owner income because fixed costs get spread over more units, but only if customers actually buy the output.

Here’s the quick math: revenue increases by $2.45 million, or about 3.5x. The risk is producing ahead of sales, which traps cash in inventory and can delay owner pay even if output is up. Utilization helps only when demand, pricing, and collections hold.

Track sell-through, not just output

Watch units produced, units sold, inventory days, and days sales outstanding. If production rises faster than orders or cash collection, you are funding stock instead of income. That is where higher utilization stops helping and starts tying up working capital.

- Match batch size to open orders.

- Check inventory by SKU weekly.

- Sell into firm customer forecasts.

- Protect cash before adding shifts.

1

Product Mix And Yield

Product Mix And Yield

This driver is about which cocoa products sell, and how much finished product you get from each batch. In Year 1, revenue is $280,000 butter, $250,000 powder, $200,000 couverture, $140,000 nibs, and $90,000 liqueur, or $960,000 total. Butter is about 29% of sales, so a small shift in mix can move gross profit and owner pay fast.

Listed prices run from $20 to $40, but yield loss, quality grade, packaging, and certification costs can wipe out that spread. If more output sells into higher-demand products, revenue rises; if yield falls or compliance costs rise, margin can drop even when sales stay flat. That makes this driver more sensitive to profit than to top-line growth alone.

Track mix by margin, not just volume

Measure unit yield, net selling price, and product-level gross margin for each line. The key inputs are pounds produced, pounds sold, sale price, yield loss, packaging cost, and certification cost. If a product sells at a higher price but loses more weight in processing, it may still pay less than a simpler line.

- Track margin by product weekly.

- Flag yield loss above budget.

- Test price after quality upgrades.

- Separate packaging and certification costs.

- Watch mix shifts in orders.

Here’s the quick test: if a higher-priced product does not lift gross margin after added yield loss and compliance cost, it is hurting cash available for owner draw. Keep the mix moving toward the products that clear the most dollars per batch, not just the highest sticker price.

2

Raw Bean Procurement Cost

Raw Bean Cost

Raw bean procurement cost is the cash you pay for cocoa beans before they become powder, butter, couverture, liqueur, or nibs. At the listed input levels of $120, $180, $200, $150, and $100 per unit, any change in freight, origin, quality, certification, minimum order size, or waste cuts gross margin right away and can delay owner pay.

When bean cost rises before selling prices reset, profit shrinks on the next batch. That means less cash left after direct costs, even if volume stays flat. Here’s the quick math: higher bean cost compresses gross margin first, then reduces the cash available to cover fixed costs and owner draw.

Track Landed Bean Cost

Measure bean cost as landed cost per finished unit, which is the bean price plus freight, certification, and waste. Compare each SKU to the listed input levels so you can spot margin drift early and avoid buying inventory that does not earn back its cash cost.

- Track landed cost by SKU.

- Log waste and yield loss.

- Watch minimum order size.

- Reprice when costs move.

If supplier cost moves up and sales terms stay fixed, owner cash drops fast. Forecast bean buys against confirmed orders, so you do not trap cash in raw inventory and then wait for sales to catch up.

3

Pricing Power And Sales Channels

Pricing Channel Mix

Sales channel changes the real price, volume, buyer concentration, and cash timing. For Year 1, listed prices are $25 powder, $35 butter, $40 couverture, $30 liqueur, and $20 nibs. Wholesale can move more pounds, but it usually tightens margin and payment terms, so income only improves if the volume gain beats the slower cash and lower net price.

Measure Net Price by Channel

Track units sold, realized price, packaging cost, compliance labor, support hours, and days to collect for each channel. Specialty, foodservice, private label, and direct can lift price, but the owner’s take-home income rises only when those added costs stay below the channel premium and no single buyer becomes too large a share of sales.

- Compare net margin by channel.

- Watch receivables aging each week.

- Cap exposure to one buyer.

4

Operating Cost Control

Operating Cost Control

Operating cost control is the gap between gross profit and what the owner can actually draw. In this cocoa processor, unit COGS include raw beans, direct labor, packaging, energy, quality testing, pressing, filtration, deodorization, sugar, emulsifiers, and conching energy. Revenue-based production costs add 9%, so at $960,000 Year 1 revenue, that is $86,400 before fixed overhead.

Fixed overhead is not provided, so payroll, rent, insurance, admin, maintenance, and food safety costs have to be modeled separately. Here’s the hard truth: if those fixed costs rise faster than throughput, owner take-home drops even when sales look strong. More output only helps if the plant stays full and waste, energy, and labor per pound stay in check.

Track cost per pound, not just total spend

Measure COGS per unit, production cost as % of revenue, and fixed overhead per month. Tie each batch to bean cost, labor, packaging, testing, and energy, then compare actual vs. plan. If a line misses yield or uses extra conching energy, the margin leak shows up fast and cuts cash available for owner pay.

Keep a weekly view of throughput and overhead absorption. The same rent and payroll hurt less at higher volume, but only if sales collect on time and inventory does not build. One clean rule: control waste first, then scale volume.

5

Working Capital And Reserves

Working Capital And Reserves

Accounting profit is not the same as cash you can pay yourself. Cocoa processing ties money up in beans, packaging, work-in-process inventory, finished goods, receivables, repairs, certifications, and loan payments, so Year 1 gross profit of $872,460 can still feel tight if cash moves slowly.

The owner’s take-home falls when buyers pay late or stock builds before sales catch up. Here’s the quick math: profit on paper is only spendable after inventory turns and invoices clear, so cash draw should wait until the next production cycle is funded and reserves are safe.

Track Cash Before You Draw

Measure cash tied up in raw beans, packaging, WIP, finished goods, and receivables every week. Also watch due dates for repairs, certifications, and loan payments, because those bills hit before customer cash does. If receivables stretch or production runs ahead of sales, owner pay should slow first.

- Track inventory by stage.

- Watch invoice aging weekly.

- Hold cash for fixed payments.

- Only draw after reserve checks.

Use a simple cash forecast that starts with gross profit, then subtracts purchases, labor, overhead, and payment timing gaps. That shows whether the business can fund the next run without borrowing more. What this estimate hides: if buyers pay late, reported profit stays high while cash available to the owner drops fast.

6

Compare low, base, and high cocoa processing owner-income planning cases

Owner income scenarios

Owner income rises as cocoa volume, product mix, and pricing improve from ramp to mature production. The three cases show what the business can support at each stage before overhead, debt, taxes, and reserves.

| Scenario | Low CaseRamp | Base CaseScaling | High CaseMature |

|---|---|---|---|

| Launch model | This is the lower earnings path built on the Year 1 ramp. | This is the modeled mid-case earnings path at the Year 3 scaling stage. | This is the stronger earnings path modeled for the Year 5 mature stage. |

| Typical setup | Year 1 volume totals 33,000 units with $960,000 revenue and $87,540 listed COGS before overhead, debt, taxes, and reserves. | Year 3 volume reaches 68,000 units with $2,101,500 revenue and $185,664 listed COGS before overhead, debt, taxes, and reserves. | Year 5 volume reaches 104,000 units with $3,410,000 revenue and $288,940 listed COGS before overhead, debt, taxes, and reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | About $872,460 gross profitRamp case | About $1,915,837 gross profitScaling case | About $3,121,060 gross profitMature case |

| Best fit | Use this to stress test a slow start or weak demand setup. | Use this as the planning case for a steadier build and normal execution. | Use this to test upside if output, pricing, and throughput all hold. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Cocoa Processing Porter's Five Forces Analysis

- Cocoa Processing BCG Matrix

- Cocoa Processing Business Model Canvas

- 7 Manufacturing KPIs to Master for Cocoa Processing Success

- Cocoa Processing Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Cocoa Processing Profit Margins

- How Much Does It Cost To Run Cocoa Processing Monthly?

- Cocoa Processing Startup Costs For A $960K Year 1 Plan

- Cocoa Processing Financial Model Template in Excel

- How to Open a Cocoa Processing Business in 6–12 Months

- How to Write a Cocoa Processing Business Plan in 7 Steps

- Cocoa Processing Marketing Mix

- Cocoa Processing Marketing Plan

- Cocoa Processing Business Proposal

- Cocoa Processing PESTEL Analysis

- Cocoa Processing Pitch Deck Example Editable PPTX

- Cocoa Processing Business SWOT Analysis

- Cocoa Processing Value Proposition Canvas

Frequently Asked Questions

Using the provided case, the business produces $960,000 in Year 1 revenue and $872,460 in gross profit after listed COGS That is not owner take-home Pay depends on fixed payroll, rent, insurance, maintenance, debt service, taxes, reserves, and reinvestment By Year 5, revenue reaches $341 million with $312 million gross profit before those items