Owner income$180K

Owner income$180KHow Much Can A Supply Chain Software Owner Make? $180K+

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180K  Net margin40%

Net margin40% Revenue for target pay$450K

Revenue for target pay$450K Business difficultyHard

Business difficultyHard

A supply chain collaboration tools owner can model $180,000 of CEO pay in Year 1, plus possible distributions only if the business has cash after costs, taxes, reserves, and reinvestment Under the researched assumptions, Year 1 revenue is about $352 million if 1,000 paid customers are active for a full year Gross margin after hosting and API costs is 91%, and contribution after commissions and onboarding support is about 80% What this estimate hides: churn, taxes, debt service, reserve policy, and the missing customer success FTE schedule can materially change owner take-home

Owner income$180KNet margin40%Revenue for target pay$450KBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

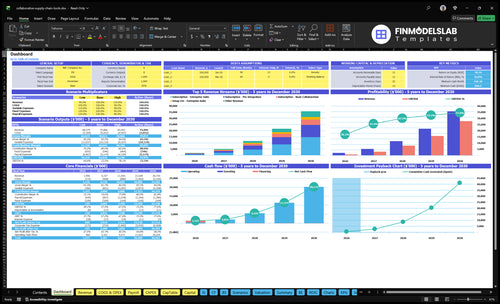

Want to pressure-test the Supply Chain Collaboration Tools model?

The dashboard shows assumptions, income outputs, scenarios, charts, and tables in the Supply Chain Collaboration Tools Financial Model Template.

Owner-income model highlights

- Revenue build and COGS

- ARR and pricing mix

- Churn and implementation capacity

- Hosting, API, commissions, onboarding

- Payroll, marketing, owner pay

How much revenue does a supply chain collaboration tools business need?

For Supply Chain Collaboration Tools, break-even is about $862K in annual revenue at an 80% contribution margin. Here’s the quick math: fixed costs divided by 0.80 gets you there, so the business does not need huge volume just to cover Year 1 overhead. A $352M revenue model creates profit capacity, but it is not owner income; taxes, debt, churn, reserves, and reinvestment decide what you can actually take out.

Break-even math

- $862K annual break-even

- 80% contribution margin

- $180K CEO salary included

- Missing CS FTE can move it

Profit, not pay

- $352M shows scale capacity

- Revenue is not owner take-home

- Taxes, debt, churn cut cash

- Keep a reserve policy first

When can a supply chain collaboration tools owner pay themselves?

A Supply Chain Collaboration Tools owner can pay themselves once recurring revenue covers product, hosting, support, sales, marketing, admin, and customer success costs; see What Is The Most Critical Measure Of Success For Your Supply Chain Collaboration Tools Business? for the KPI lens. The model includes a $180K CEO salary from Month 1, but that’s a planning assumption, not guaranteed cash.

Pay trigger

- Cover all core operating costs

- Protect customer success staffing

- Maintain product and hosting spend

- Use recurring revenue, not hope

Cash guardrails

- $352M Year 1 revenue model

- 91% gross margin planned

- 80% contribution after support costs

- Delay distributions if churn rises

Can a supply chain collaboration tools business scale without the owner?

Yes, but only after the founder stops being the bottleneck. For Supply Chain Collaboration Tools, that means onboarding, integrations, supplier setup, support, and renewals all need to run without the owner. The model keeps a $180K CEO role throughout, with engineering rising from 10 lead engineer FTE in Year 1 to 20 FTE in Year 5, while sales and marketing move from 0.5 FTE each in Year 1 to 1.0 FTE each later.

Owner-free only after repeatability

- Standardize onboarding steps first

- Automate supplier setup workflows

- Document support handoffs clearly

- Make renewals trackable by team

Hiring can pressure income

- Hire before retention, income can dip

- More engineering supports scale

- 10 to 20 FTE lifts product capacity

- 0.5 to 1.0 FTE expands go-to-market

Want the six main income drivers?

1

$310M-$7.7BARR Growth

Annual recurring revenue drives the model, and the jump from Year 1 to Year 5 is what turns fixed cost into real owner take-home.

2

$25.8K-$51.6KMix Power

A richer contract mix lifts monthly recurring revenue per customer, so each sale brings in more cash without adding the same overhead.

3

HighRetention

Churn has no source value here, but it still matters a lot because lost customers drag down recurring revenue and force more selling just to stay flat.

4

$419-$74.9KSetup Fees

Implementation efficiency lifts one-time fees, which improves early cash and helps offset onboarding work before recurring revenue scales.

5

20%↓CAC Drop

Customer acquisition cost falls from $150 to $120, so each new customer costs less and payback gets faster.

6

$1.5M-$1.8MPayroll Load

Fixed overhead and payroll set the burn floor, so staffing pace decides how much gross profit is left for the owner.

Supply Chain Collaboration Tools Core Six Income Drivers

Annual Recurring Revenue

Annual Recurring Revenue

ARR funds owner income because subscriptions and usage repeat. Here’s the quick math: Year 1 ARR is about $309.7M from 1,000 customers at $25.81M MRR; by Year 3 it reaches $2.016B; by Year 5, $7.734B. That supports pay only if recurring revenue stays real after churn, not just booked sales.

The risk is counting acquired customers as full-year active accounts without churn data. If churn is higher than assumed, ARR inflates and owner draw gets ahead of cash. ARR should be tied to active renewals, not just new logos.

Track True Recurring ARR

Use a model built on active customers, monthly recurring revenue, usage fees, and churn. Split one-time setup revenue from recurring revenue so you do not fund owner pay with non-repeat cash. If the business keeps more customers each month, ARR rises faster and fixed costs take a smaller share of each dollar.

Track gross and net retention.

Reconcile ARR to active renewals.

Test churn before scaling sales.

1

Pricing And Contract Value

Pricing Mix Drives Profit

If most customers stay on Basic, owner income stays tight even if costs shrink. Year 1 prices range from $99 to $999 a month, with 60% Basic and 10% Enterprise; by Year 5, Basic falls to 25% and Enterprise rises to 25%, pushing weighted monthly recurring revenue (MRR) per customer from $25,810 to $51,560.

That mix shift does more for profit than small cost cuts. Treat pricing as a scenario input, not a fixed recommendation, because discounting, churn, and free pilots can mute the cash benefit and slow owner pay.

Track Mix, Not Just List Price

Measure contract value by plan mix, not just total logos. Track new bookings, upgrades, downgrades, renewals, and average deal value by cohort, then rebuild MRR each month from active accounts. If Enterprise share moves from 10% to 25%, the same customer count can produce far more recurring cash for payroll and owner distributions.

- Track plan mix by month

- Test discount impact on close rate

- Separate new sales from renewals

- Watch upgrade and downgrade rates

- Model churn before raising prices

Run three cases before you change price: base, discount-heavy, and Enterprise-led. If higher list prices slow sales, the owner may need more pipeline to protect income even when contract value looks better.

2

Customer Retention And Churn

Customer Retention And Churn

Retention protects owner income because each retained account lowers replacement sales pressure. For a recurring SaaS model, the key numbers are ARR, renewal rate, net revenue retention (NRR), and expansion revenue. Since no churn rate is supplied, the model should use editable churn and renewal assumptions, or the owner can overstate cash that never repeats.

This driver includes integrations, supplier adoption, transaction volume, and customer success. If a customer leaves before onboarding cost is recovered, CAC and implementation labor eat profit twice. With $91K per month of fixed overhead already in the model, weak retention quickly cuts the cash left for payroll, product work, and owner pay. Long life beats constant replacement.

Track churn before it eats margin

Measure logo churn, renewal rate, and NRR monthly by cohort. Cohort means customers signed in the same period. Separate basic users from higher-value accounts, since pricing mix changes matter. If renewal slips, expansion revenue may not fill the gap, and ARR can look healthy while cash income stalls.

- Logo churn by customer cohort

- Renewal rate by tier

- NRR and expansion revenue

- Onboarding days to first use

- Integration count per account

Build forecasts with editable churn assumptions and test what happens when retention falls a few points. If implementation takes too long, retention risk rises before the setup fee is fully earned. The point is simple: keep customers long enough for recurring revenue to cover service cost and support the owner’s draw.

3

Implementation And Onboarding Efficiency

Implementation and Onboarding Efficiency

Implementation can add cash or drain it. The model shows a weighted one-time setup fee of $419 per new customer in Year 1, rising to $74,975 in Year 5. Onboarding support runs at 4% of revenue in Year 1 and 3% in Year 5. If supplier setup, training, or system integrations cost more than that, the extra work cuts owner income.

Here’s the quick math: owner take-home should separate one-time implementation revenue from recurring subscription margin. A strong setup fee helps cash flow, but only if delivery cost stays below the fee. If the team spends too many hours on custom onboarding, revenue can rise while profit and free cash fall.

Track Setup Margin, Not Just Revenue

Measure implementation margin per new customer. Track setup fee billed, onboarding labor, integration hours, and support time against each account. Use 4% of revenue in Year 1 and 3% in Year 5 as the baseline support load, then compare actuals monthly. If onboarding cost beats the fee, growth hurts owner pay.

- New customers started

- Setup fee collected

- Onboarding hours used

- Integration and training overruns

- Support cost as revenue percent

- Net cash per customer

If complex supplier setups need extra work, price that separately or cap the scope in the contract. That protects gross margin and keeps founder pay from being funded by unpaid service time.

4

Customer Acquisition Cost And Sales Cycle

CAC and Sales Cycle Timing

When customer acquisition cost (CAC) is $150 in Year 1 and $120 in Year 5, the bigger issue is cash timing, not just spend. $150K of annual marketing implies 1,000 paid customers in Year 1; the model also states $15M of marketing and 12,500 paid customers in Year 5. Long pilots, demos, procurement reviews, and founder-led sales can delay cash even when the funnel looks strong.

Sales commissions falling from 7% to 5% of revenue helps margin, but only if deals close fast enough to fund payroll and support. If the cycle drags, CAC sits out longer before renewals compound, so owner draw gets pushed back. The key test is whether new revenue pays back acquisition spend before churn or slow onboarding eats the first year.

Track the payb ack clock

Measure CAC by source, not as one blended number. Use marketing spend, paid customers, sales commissions, and days from first demo to first invoice to see whether acquisition is turning into cash fast enough for the owner.

- Track CAC by channel.

- Separate pilots from closed deals.

- Watch commission rate monthly.

- Record first invoice date.

- Flag procurement delays early.

- Compare paid customers to spend.

For this model, $150K ÷ $150 = 1,000 paid customers in Year 1, so the math is clean there. Year 5 is a scenario case: $15M marketing, $120 source CAC, and 12,500 paid customers are the stated inputs, so treat CAC as a planning assumption, not a fixed result.

5

Staffing, Support, And Reinvestment

Staffing And Reinvestment Pressure

Owner pay is squeezed early because payroll, support coverage, uptime, security, integrations, and roadmap work come before distributions. Fixed overhead is $91K per month ($1.092M per year), before known payroll of $430K in Year 1 and $680K in Year 5. Add $700 per month for cybersecurity and compliance tools, and profit has to cover the team first.

Here’s the quick math: when support tickets rise or integrations take longer, cash stays inside the business instead of reaching the owner. That’s not bad if reserves and reinvestment are planned. The real risk is paying yourself too early, then missing uptime, security, or product work that keeps customers from leaving.

Track Headcount Against Service Load

Measure support tickets, integration hours, and uptime together, then tie them to headcount. Use $91K monthly overhead as the guardrail. If payroll grows faster than subscription cash, owner take-home gets delayed. Each added role should improve coverage, retention, or implementation speed.

Keep a reserve plan before any owner draw. Put security, compliance, and product fixes ahead of distributions while the platform is still maturing. If support and roadmap work rise faster than recurring revenue, reinvest profit until service quality and cash flow are steady.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income rises as the mix shifts toward higher tiers and more customers convert from trial to paid. Higher revenue helps, but support staff and commissions still shape take-home results.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower-earnings path built on Year 1 assumptions and a lean customer base. | This is the modeled path built on Year 3 assumptions and a more balanced mix. | This is the stronger-earnings path built on Year 5 assumptions and a heavier enterprise mix. |

| Typical setup | Year 1 assumptions produce about $352M revenue from 1,000 customers, with 91% gross margin, 80% contribution, and $6.892M known operating costs before reserves. | Year 3 assumptions produce about $2,273M revenue from 4,615 customers, with 92.5% gross margin and 83% contribution. | Year 5 assumptions produce about $8,671M revenue from 12,500 customers, with 94% gross margin and 86% contribution. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | ~$212MLow Case | ~$1,755MBase Case | ~$7,228MHigh Case |

| Best fit | Use this to stress-test slower adoption and tighter early support capacity. | Use this as the planning case for budget, hiring, and cash control. | Use this to test enterprise adoption, staffing scale, and upside cash needs. |

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; reserve percentage, churn, taxes, debt, and owner distributions stay editable.

Related Products

- Supply Chain Collaboration Tools Porter's Five Forces Analysis

- Supply Chain Collaboration Tools BCG Matrix

- Supply Chain Collaboration Tools Business Model Canvas

- 7 Essential KPIs for Supply Chain Collaboration Tools

- Supply Chain Collaboration Tools Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Supply Chain Collaboration Tools Profitability

- Running Costs for Supply Chain Collaboration Tools: A 2026 Financial Guide

- Supply Chain Collaboration Tools Startup Costs: Plan Beyond $727K

- Supply Chain Collaboration Tools Financial Model Template in Excel

- How to Start Supply Chain Collaboration Tools in 16–36 Weeks

- How to Write a Business Plan for Supply Chain Collaboration Tools

- Supply Chain Collaboration Tools Marketing Mix

- Supply Chain Collaboration Tools Marketing Plan

- Supply Chain Collaboration Tools Business Proposal

- Supply Chain Collaboration Tools PESTEL Analysis

- Supply Chain Collaboration Tools Pitch Deck Example Editable PPTX

- Supply Chain Collaboration Tools Business SWOT Analysis

- Supply Chain Collaboration Tools Value Proposition Canvas

Frequently Asked Questions

The model includes $180,000 of CEO pay in Year 1 On the business side, Year 1 revenue is about $352 million under the full-year active customer assumption, with 91% gross margin after hosting and API costs Extra owner take-home depends on taxes, reserves, debt, churn, and reinvestment, not revenue alone