Owner income$0–$54K

Owner income$0–$54KHow Much Commercial Office Building Owners Make: $395K Monthly Rent Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0–$54K  Net margin1.1%

Net margin1.1% Revenue for target pay$4.74M

Revenue for target pay$4.74M Business difficultyHard

Business difficultyHard

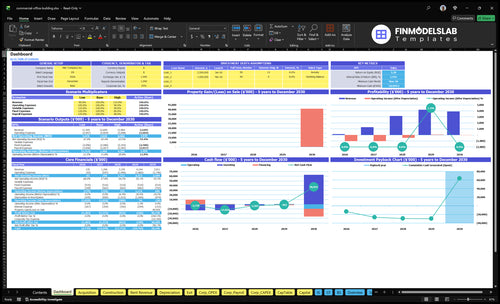

In this researched assumption set, the owner does not see reliable distributable cash flow in the early years EBITDA is -$1018M in Year 1, -$1019M in Year 2, -$480K in Year 3, $54K in Year 4, and -$28K in Year 5 The model reaches breakeven in Month 26, but minimum cash still falls to -$18995M in Month 59 These are planning assumptions, not guaranteed commercial office building owner income

Owner income$0–$54KNet margin1.1%Revenue for target pay$4.74MBusiness difficultyHardWant to test your office building cash flow?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Commercial Office Building pro forma?

This Commercial Office Building model shows dashboard, rent-roll assumptions, timing, budgets, debt, reserves, and owner income—open the Commercial Office Building Financial Model Template; planning support only.

Owner-income model highlights

- Owner income: 60-month payback

- Rent track: $395K stabilized

- Cash floor: -$18995M minimum cash

- Returns: 002% IRR, 538% ROE

How big does an office building need to be to make target owner income?

For a Commercial Office Building, size is not the real target; rentable square feet, rent per square foot, occupancy, leverage, management choice, and reserve policy drive owner income. In this portfolio, $395K of scheduled monthly rent still only produced $54K EBITDA in Year 4 and -$28K in Year 5, so the income goal has to be solved backward after debt service and reserves.

What sets the size

- Rentable area sets gross rent.

- Occupancy cuts or lifts cash fast.

- Rent per square foot matters more than raw size.

- Leverage changes the cash left for owners.

Why income can still miss

- Tenant rollover can break cash flow.

- Buildout costs eat rent gains.

- Vacancy can absorb monthly income.

- Reserves reduce owner take-home pay.

How much cash flow can an office building owner keep?

A Commercial Office Building owner can keep cash only after rent collection, operating costs, reserves, retained cash, and debt service; here, EBITDA is negative in Years 1, 2, 3, and 5, with only $54K positive EBITDA in Year 4, so owner cash flow is likely limited. For context, see What Is The Current Growth Rate Of The Commercial Office Building Business?, but remember: the $200K managing partner salary is payroll, not guaranteed owner profit.

Cash owner may keep

- Keep cash after rent is collected

- Pay operating costs first

- Fund reserves before distributions

- Cover debt service if applicable

Key cash limits

- Negative EBITDA in 4 of 5 years

- $54K EBITDA only in Year 4

- Debt service is not provided

- $200K salary is payroll

How much revenue does a commercial office building generate?

A Commercial Office Building generates revenue from rentable space leased at market rent, not from profit. If total rent fees reach $395K per month at full portfolio activity, that is about $4.74M annualized. At the building level, monthly rent can run from $25K to $90K, and occupancy, lease escalations, parking, reimbursements, free rent, and downtime all change what gets collected; keep revenue separate from NOI and owner income.

Revenue base

- $395K monthly at full activity

- $4.74M annualized revenue

- $25K–$90K per building monthly

- Market rent sets the top line

What changes collected cash

- Occupancy drives billed rent

- Lease escalations raise revenue over time

- Parking and reimbursements add cash

- Free rent and downtime reduce receipts

Want to see what drives office building income?

1

$395K/moOccupancy

More occupied space pushes the $395K monthly rent run rate and is the fastest way to lift NOI and owner cash.

2

$/SFRent/SF

A better $/SF rate lifts gross rent without much extra cost, so more lease dollars fall through to EBITDA.

3

$43K/moOpex Control

Holding fixed costs near $43K a month and mature payroll near $540K keeps the spread between rent and cash from getting eaten up.

4

Month 26Financing Terms

Cheaper debt and cleaner draw timing matter because breakeven lands in Month 26, and weak terms drain cash before that.

5

60moRetention

Keeping tenants through lease rollover protects rent continuity and shortens the 60-month payback.

6

-$19.0MCapital Reserves

Reserves cover the cash trough near -$19.0M in Month 59 and keep owner take-home from stalling.

Commercial Office Building Core Six Income Drivers

Occupancy And Vacancy

Occupancy and Vacancy

Occupancy drives leased rentable square feet and collected rent, so a vacant suite cuts revenue first, then NOI, then owner take-home. With $395K in scheduled monthly rent, every 1% of rent lost is about $3,950 per month, which matters when EBITDA is thin.

Test stabilized occupancy against Month 26 breakeven and tenant rollover risk. The key is not just physical vacancy; it’s whether rent actually collects after lease-up delays, concessions, and nonpayment.

Track vacancy like cash

Build a monthly lease roll with vacancy loss, downtime, renewal timing, concessions, and collection rate. That shows where income falls before the bank balance does.

- Vacancy loss by suite

- Downtime between tenants

- Renewal timing risk

- Concessions and free rent

- Collection rate each month

Here’s the quick math: collected rent equals scheduled rent less vacancy loss, downtime, concessions, and missed collections. If a tenant leaves, the hit shows up in rent first, then NOI, then the owner’s draw.

1

Rent Per Square Foot

Rent per square foot

Rent per square foot is the main price meter for office income. It sets how much revenue the building can earn before expenses. For this model, do not stop at asking rent; use effective rent after free rent, concessions, and tenant improvement costs. Lease type matters too: a full-service gross lease leaves more costs with the owner, while a triple net lease shifts some costs to the tenant.

Here’s the quick math: rentable square feet × effective rent per square foot × occupied months. At the portfolio level, source rent fees total $395K monthly, with building-level assumptions from $25K to $90K per month. A small drop in realized rent per square foot hits NOI fast, and that flows straight into owner pay.

Track effective rent, not just asking rent

Track asking rent, effective rent, free-rent months, concessions, and tenant improvement allowances on every lease. That shows the real cash yield per square foot, not the sticker price. If you miss those costs, rent looks strong on paper but cash flow stays thin.

- Compare gross vs triple net deals.

- Measure rent by building and suite.

- Reprice renewals before rollover.

Use lease type to forecast owner income. Full-service gross leases usually mean more owner-paid operating costs, so the same rent rate can produce lower NOI. Triple net leases push some costs to tenants, which protects margin and leaves more cash for debt service and owner draws.

2

Operating Expense Control

Operating Expense Control

Operating expense control is what turns gross rental income into NOI (net operating income) before debt service. Include management fees, insurance, utilities, office rent, marketing, legal, accounting, and payroll. Keep debt payments, depreciation, income taxes, and capital reserves out of operating expenses, or you will overstate margin and owner cash.

Here’s the quick math: fixed overhead is $43K per month, or $516K per year. Add payroll of $3.025M in Year 1 or $540K in mature years, and weak expense control can leave Year 4 EBITDA (earnings before interest, taxes, depreciation, and amortization) thin even when rent is steady.

Track Expense Leakage

Measure each cost line monthly and by building. The owner should track fixed overhead, payroll, and expense per leased square foot, then compare actuals to budget. If a line moves without rent support, it goes straight into the owner’s draw gap.

- Management fees and payroll

- Insurance and utilities

- Office rent and marketing

- Legal and accounting spend

- Monthly NOI after expenses

Test staffing and vendor scope against rent collected, not scheduled rent. If control slips, a small overrun can wipe out cash because operating expenses hit NOI before debt service. Tight reporting matters most when annual payroll is $3.025M in Year 1 and still $540K in mature years.

3

Debt Service And Leverage

Debt Service And Leverage

Debt service sits after NOI (net operating income), so it’s the last step before owner take-home. Here’s the quick math: DSCR = NOI ÷ annual debt payments. If debt service rises because the loan amount, interest rate, or amortization changes, cash left for distributions drops fast even if rent looks strong.

Because loan payments are not provided, cash flow after mortgage must stay an input, not a guess. The model shows minimum cash reaching -$18,995M before any unsupported debt assumption, so leverage can turn positive property income into little or no owner draw. Refinancing risk matters too, because a reset can push annual debt service higher.

Track DSCR Before Distributions

Build the debt model with loan amount, interest rate, amortization, loan-to-value, maturity date, and DSCR. Keep NOI and annual debt payments in the same view so you can see when DSCR falls below 1.0x, which means NOI no longer fully covers debt service.

- Stress test refinance at higher rates.

- Model lower NOI and slower leasing.

- Track cash after mortgage monthly.

- Hold back owner draws until coverage holds.

If tenants roll or rent weakens, protect the mortgage cushion first. Use debt terms to forecast how much cash can actually reach the owner, not just how much income the building shows before financing costs.

4

Tenant Retention And Lease Rollover

Tenant Retention And Lease Rollover

Tenant retention is the share of expiring leases that renew instead of turning into vacancy. It keeps monthly rent steady and protects NOI, while weak retention adds downtime, brokerage fees, and tenant improvement allowances before the next tenant pays. The key inputs are renewal rate, lease expiry timing, tenant credit quality, and suite size.

Here’s the quick math: every move-out hits cash twice, first through lost rent and then through re-leasing costs. Staggered expirations and long-term tenants matter because they support the Month 26 breakeven path and reduce the risk that too much rent rolls at once.

Cut Rollover Losses Early

Track a lease-expiry schedule by month and test three cases: renew, re-lease fast, and re-lease slow. Model renewal rate, downtime, concessions, brokerage fees, and TI dollars for each case, then compare that to the rent you keep. If a tenant’s credit weakens, start renewal talks earlier so you are not pricing under pressure near expiration.

- Measure renewal rate by expiry month.

- Map expirations at least 12 months out.

- Price concessions before lease signing.

- Limit same-month lease clustering.

One missed renewal is not just lost rent; it is also cash spent on make-ready work before the next check clears. That is why retention lifts distributable incom e more reliably than chasing a higher asking rent with long vacancy and heavy buildout costs.

5

Capital Reserves

Capital Reserves

Capital reserves are cash held back for tenant improvements, leasing commissions, roof and HVAC work, and future vacancies. In this model, $58M of construction budgets and $280K of corporate capex sit ahead of owner payouts, so positive EBITDA does not mean full distributable income.

Here’s the quick math: Year 4 EBITDA is only $54K, and minimum cash reaches -$18,995M. If all excess cash goes to the owner, the building can miss repairs, lease-up needs, and liquidity support right when the next vacancy or capex cycle hits.

Hold a reserve floor

Set reserves from the cash plan, not from leftover profit. Track lease expirations, tenant improvement spend, leasing commissions, and roof/HVAC timing so you know how much cash must stay in the deal before any owner draw.

- Forecast capex by month.

- Stress-test vacancy timing.

- Keep a minimum cash floor.

- Delay draws when cash is thin.

Do not distribute all positive EBITDA when reserves are short. The owner’s take-home income is safer when cash is held for the next lease-up, repair, or downtime event instead of being paid out too early.

6

Compare low, base, and best-case office income scenarios

Owner income scenarios

Owner income swings with lease-up speed, staffing, and reserve use. Month 26 is the break-even point, but the mature case still only shows a small profit before debt and reserves.

| Scenario | LowRamp loss | BaseBreakeven watch | HighThin profit |

|---|---|---|---|

| Launch model | This is the slow-ramp case, where lease-up lags and owner income stays deeply negative. | This is the transition case, where the portfolio reaches Month 26 breakeven but earnings are still negative in Year 3. | This is the stronger case, where the asset base matures and owner income turns slightly positive before debt and reserves. |

| Typical setup | Year 1 EBITDA is about -$1.018M and Year 2 is about -$1.019M while the rent roll is still building. | Monthly scheduled rent reaches $395K, fixed monthly costs run $43K, and Year 3 EBITDA is still about -$480K as staffing scales. | Monthly scheduled rent stays around $395K, fixed monthly costs stay near $43K, and mature payroll reaches $540K while Year 4 EBITDA comes to about $54K. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$1.02MHigh loss | -$480KNear breakeven | $54KSmall profit |

| Best fit | Use this to stress-test cash needs if leasing runs behind plan. | Use this as the working case for lenders, investors, and cash planning. | Use this to test upside, but keep sensitivity on occupancy, payroll, and reserves. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Commercial Office Building Porter's Five Forces Analysis

- Commercial Office Building BCG Matrix

- Commercial Office Building Business Model Canvas

- 7 Critical KPIs for Commercial Office Building Performance

- Commercial Office Building Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Commercial Office Building Profitability

- How Much Does It Cost To Run A Commercial Office Building Monthly?

- Commercial Office Building Startup Costs: $261M Launch Budget

- Commercial Office Building Financial Model Template in Excel

- How To Open A Commercial Office Building In 6 To 18+ Months

- How to Write a Commercial Office Building Business Plan

- Commercial Office Building Marketing Mix

- Commercial Office Building Marketing Plan

- Commercial Office Building Business Proposal

- Commercial Office Building PESTEL Analysis

- Commercial Office Building Pitch Deck Example Editable PPTX

- Commercial Office Building Business SWOT Analysis

- Commercial Office Building Value Proposition Canvas

Frequently Asked Questions

In this model, reliable owner distributions are limited EBITDA is -$1018M in Year 1, -$1019M in Year 2, -$480K in Year 3, $54K in Year 4, and -$28K in Year 5 Debt service and reserves would reduce cash available to the owner further