Owner income$100k

Owner income$100kHow Much Commercial Waterproofing Owners Make In A $100K Pay Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$100k  Net margin73%–79%

Net margin73%–79% Revenue for target pay$337k

Revenue for target pay$337k Business difficultyHard

Business difficultyHard

You’re looking at owner income, not gross sales This model estimates $100,000 in planned annual owner pay, but the researched first-year revenue assumption is only $36,750, so distributions are not supported without more sales, lower staffing, or outside cash

Owner income$100kNet margin73%–79%Revenue for target pay$337kBusiness difficultyHardWant to test your waterproofing owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

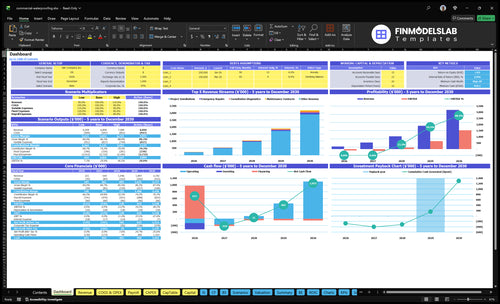

Want to see the Commercial Waterproofing forecast behind this?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Commercial Waterproofing Financial Model Template; open the model.

Owner-income model highlights

- Owner salary: $100k yearly

- Revenue ramps to $371,073

- Scenario tables show cash gaps

How do waterproofing job costs affect owner income?

In Commercial Waterproofing, job costs can cut owner take-home fast because Year 1 variable costs already eat 27% of revenue, and the startup-cost side is worth checking first in How Much Does It Cost To Open, Start, Launch Your Commercial Waterproofing Business?. That leaves 73% contribution before payroll, but the $100,000 owner salary still has to come from what’s left. True job gross margin only shows up when labor is tracked by project.

Core cost stack

- 12% materials

- 4% sealants and adhesives

- 7% sales commissions

- 4% project subcontractors

What protects income

- Track labor by project

- Count membrane and coating quantities

- Include mobilization and rentals

- Budget warranty callbacks

Is a commercial waterproofing business profitable?

Commercial Waterproofing can be profitable, but not at the shown Year 1 scale: $36,750 of revenue versus $246,000 of payroll, overhead, and marketing leaves about negative $219,000 after owner salary. The math only works if bigger jobs, better pricing, and tighter staffing lift billable hours. Here’s the quick split: installs drive most revenue at 40 hours and $120/hour, while maintenance runs at $90/hour and emergency repairs at $180/hour but only 10% of Year 1 mix.

Year 1 math

- $36,750 revenue in Year 1

- $246,000 in core costs

- About negative $219,000 after owner salary

- Not profit-positive at this level

What drives profit

- Install jobs use 40 hours at $120/hour

- Maintenance smooths utilization at $90/hour

- Emergency repairs price at $180/hour

- Mix, pricing, and staffing pace decide profit

Can a commercial waterproofing owner make more by hiring crews?

Yes, but not automatically. In Commercial Waterproofing, revenue rises from $36,750 in Year 1 to $371,073 in Year 5, while payroll grows from $165,000 to $640,000 and the owner still takes $100,000 a year. So hiring crews can lift capacity, but it only improves take-home if utilization, or billable crew time, and pricing cover the added overhead.

When crews help

- $371,073 revenue by Year 5.

- More crews mean more job capacity.

- Sales and estimating widen the pipeline.

- Maintenance contracts can smooth cash flow.

When crews hurt

- Payroll climbs to $640,000.

- Owner pay stays at $100,000.

- More staff delays profit.

- Owner-operated work can protect early cash.

Want the six main waterproofing income drivers?

1

70/20/10Project Mix

Install-heavy work stays near the $120/hour base, so more emergency and diagnostics jobs lift the average ticket and owner pay.

2

$120-$180/hrBid Pricing

Better bids win more of the $180 emergency work instead of discounting toward the $120 install rate.

3

40-50hCrew Utilization

More billable hours per crew member lift revenue before headcount rises, and low utilization quickly eats margin.

4

73%-79%Margin Control

Holding materials at 12% to 10% and sealants at 4% to 3% keeps contribution margin before payroll in the 73% to 79% range.

5

$5.5KOverhead Discipline

Fixed overhead is about $5,500 a month before the $100,000 owner salary, so leaks here delay payback.

6

$418KCash Buffer

Minimum cash lands at $418,000 in month 29, and retainage plus taxes are not quantified, so weak collections can still force outside funding.

Commercial Waterproofing Core Six Income Drivers

Project Mix And Average Job Size

Project Mix and Job Size

If your mix leans to 70% installation work, the revenue base is steadier, but take-home income still depends on job size and scope. At $120 per hour and 40 billable hours, one installation job brings about $4,800 before direct costs; with 27% direct costs in Year 1, that leaves about $3,504 before payroll.

Emergency repairs price higher at $180 per hour, but they run only 8 hours and make up 10% of mix. Maintenance work at $90 per hour for 4 hours keeps crews busy, but it can pull down average job value. Larger commercial projects help if bids protect margin and cut wasted mobilization.

Track Mix by Margin

Measure job type mix, billable hours, and the realized hourly rate on each project. Here’s the quick math: mix × hours × rate gives average job value, and then direct costs tell you what is left for payroll, overhead, and owner pay. That is the number that matters, not sales volume alone.

Push the work that uses crews well and avoids repeat setup, but don’t buy revenue with weak bids. If a larger commercial scope reduces mobilization waste, owner income can improve fast; if pricing misses labor, access, or warranty risk, the extra work just fills the calendar and squeezes cash.

1

Bid Pricing And Estimating Accuracy

Bid Pricing Accuracy

For commercial waterproofing, the bid must cover labor, materials, access, mobilization, subcontractors, and warranty risk. In Year 1, source prices are $120 per hour for installations, $90 for maintenance, $180 for emergency repairs, and $110 for diagnostics. A 40-hour installation priced 10% too low cuts about $480 of revenue before materials and crew payroll, so owner pay shrinks fast.

Here’s the quick math: if the quote misses scope, the job can still “win” and still lose money. With 27% direct percentage costs in Year 1 before payroll, the estimate has to protect margin, not just hit a low price. The main inputs are hours, service mix, site access, and warranty exposure. One clean rule: a better bid beats a cheaper bid only if it still leaves contribution.

Price From Scope, Not Hope

Track actual hours, material use, access delays, and rework on every job. Compare bid hours to real hours by service type: installation, maintenance, emergency repair, and diagnostics. If estimates are drifting by even 10%, that gap can wipe out the gross profit the owner expected to draw.

Use a bid checklist that forces pricing for setup, lifts, subcontractors, and warranty reserve. Keep a simple log of win rate versus margin, because a higher win rate only helps when the estimate holds profit. What this estimate hides is the cash hit from underquoted change orders and callbacks.

- Track bid hours vs. actual hours

- Separate access and mobilization costs

- Price warranty risk into every quote

- Review margin by service line

2

Crew Utilization And Field Productivity

Crew Utilization

When a waterproofing crew sits, payroll still runs. Year 1 carries $65,000 for one lead technician and $100,000 for owner project management, plus $5,500 in monthly fixed overhead. Utilization means the share of crew time that turns into billable work. Installation jobs use 40 billable hours; maintenance uses only 4 hours, so weak scheduling or weather can leave the owner with pay but not profit.

Protect Billable Days

Track billable hours per crew day, idle days by cause, and job mix. The quick math is simple: more billable days help cover the $66,000 annual overhead and keep owner pay funded. One lost day from weather, site access, inspections, sequencing, or delayed materials cuts contribution fast, so schedule maintenance work to fill gaps and keep the crew on paid jobs.

- Log idle time by cause.

- Review billable hours weekly.

- Use maintenance to fill gaps.

3

Direct Cost Control And Gross Margin

Direct Cost Control

Commercial waterproofing owner income rises when actual labor hours, material usage, sealants, equipment, subcontractors, and rework stay close to the estimate. In Year 1, direct and variable costs are 27% of revenue, leaving 73% contribution before payroll. By Year 5, those costs fall to 21%, lifting contribution to 79%. That spread is the money that supports payroll and, later, owner pay.

This is not net profit. Payroll, rent, insurance, marketing, and reserves still come after gross margin. Small misses in membrane quantities or warranty work can erase the cash left for owner distributions, even when the job looked profitable on paper.

Track Job Cost Drift

Measure estimate vs. actual on every job: labor hours, membrane quantities, sealants, subcontractor bills, equipment time, and rework. If direct costs run above 27% in Year 1, the owner loses margin before overhead is even covered. A job-cost sheet makes the leak visible fast.

Use the variance report before the next bid. Tighten takeoffs, price warranty risk, and flag any job with rising waste or callback labor. The goal is simple: keep enough contribution after direct costs to cover fixed overhead and still leave cash for the owner.

4

Overhead, Insurance, Equipment, And Management Costs

Overhead And Team Cost Control

Commercial waterproofing overhead can eat owner pay fast because $5,500 per month in fixed overhead, or $66,000 per year, comes off the top before profit shows up. That includes rent, insurance, licensing, utilities, accounting, software, vehicle maintenance, and supplies. If payroll grows from $165,000 in Year 1 to $640,000 in Year 5, the business must keep enough billable work in the field to cover both overhead and management labor.

The key inputs are billable jobs, staff count, and support cost per job. Startup capex of $125,000 for 2 vans and specialized equipment matters too, because it raises cash pressure before revenue stabilizes. One clean rule: add estimators, project managers, vehicles, and software only when revenue can cover them without shrinking owner distributions.

Watch Fixed Cost Per Billable Job

Track overhead as a share of revenue and as dollars per job. Here’s the quick math: if monthly fixed overhead is $5,500, each added billable job has to carry its share plus payroll and direct costs before the owner gets pa id. If staff growth lifts payroll faster than sales, gross margin can look fine while cash flow turns tight.

- Track overhead monthly.

- Delay hires until demand holds.

- Match vehicles to booked work.

- Review insurance and software annually.

What this estimate hides: slow months, idle crews, and extra vehicle upkeep. If revenue is uneven, keep a buffer so fixed costs do not force the owner to skip pay or borrow just to cover payroll and rent.

5

Cash Reserves, Retainage, And Reinvestment

Cash Reserve Discipline

Commercial waterproofing can look profitable on paper, but cash gets tied up fast. This model already shows $125,000 of visible early capex for vehicles and specialized equipment, plus marketing rising from $15,000 to $85,000 a year. Add slow-paying commercial clients, seasonal gaps, warranty callbacks, and equipment replacement, and owner pay becomes cash-after-reserve, not a simple profit draw.

What this hides is the timing gap. Retainage, taxes, and debt terms are not quantified, so distributions should wait until operating cash, reserves, and replacement needs are covered. One bad quarter can still fund the job but block the owner’s paycheck.

Track Cash Before You Pay Yourself

Measure collected cash, not just booked revenue. Track retainage held, average days to collect, monthly fixed overhead of $5,500, and planned marketing and equipment spend. If cash on hand cannot cover the next payroll, warranty work, and upcoming capex, distributions should pause.

- Forecast collections by job

- Separate reserve and profit

- Fund replacements monthly

6

Compare commercial waterproofing owner income scenarios

Owner income scenarios

Revenue can rise fast in commercial waterproofing, but payroll, marketing, and field labor can outrun margin. These cases show why owner income stays cash-constrained until utilization or staffing changes.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | Year 1 is a launch case with thin revenue and heavy overhead, so owner income stays negative. | Year 3 is the modeled middle path, but owner income is still negative under the current cost stack. | Year 5 is the scaled case, but the heavier team and overhead still keep owner income negative. |

| Typical setup | About $36,750 revenue, 73% contribution margin before payroll, a $246,000 payroll and marketing stack, and a modeled $100,000 owner salary. | About $129,939 revenue, 76% contribution margin, a $556,000 cost stack, and payroll that still absorbs most of the gross profit. | About $371,073 revenue, 79% contribution margin, a $791,000 cost stack, and a bigger staffing load across the field and office. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$219,000Low case | -$457,000Base case | -$498,000High case |

| Best fit | Use this to stress test a slow start and see how much cash the launch burns. | Use this as the working plan if you want the most realistic operating view. | Use this to test the upside path and the scale needed before costs stop outrunning margin. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Commercial Waterproofing Porter's Five Forces Analysis

- Commercial Waterproofing BCG Matrix

- Commercial Waterproofing Business Model Canvas

- 7 Essential KPIs to Scale Your Commercial Waterproofing Business

- Commercial Waterproofing Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Commercial Waterproofing Profitability

- How Much Does It Cost To Run Commercial Waterproofing Monthly?

- Commercial Waterproofing Startup Costs: $182k CAPEX to $418k Cash

- Commercial Waterproofing Financial Model Template in Excel

- How To Open A Commercial Waterproofing Business In 60 To 120 Days

- How to Write a Commercial Waterproofing Business Plan: 7 Steps

- Commercial Waterproofing Marketing Mix

- Commercial Waterproofing Marketing Plan

- Commercial Waterproofing Business Proposal

- Commercial Waterproofing PESTEL Analysis

- Commercial Waterproofing Pitch Deck Example Editable PPTX

- Commercial Waterproofing Business SWOT Analysis

- Commercial Waterproofing Value Proposition Canvas

Frequently Asked Questions

The researched model includes $100,000 in annual owner compensation That is planned pay, not guaranteed profit With Year 1 revenue at $36,750 and fixed costs, payroll, and marketing at $246,000, the company shows about a $219,000 operating deficit after that owner salary