Community Bank Startup Costs: $587K Monthly Fixed Overhead Plan

How much does it cost to start a community bank depends less on furniture and more on regulatory readiness, systems, staffing, and balance-sheet capital As researched planning assumptions, this model carries $587K per month in fixed operating costs and $530K in visible first-year payroll, with $345M in Year 1 loans Spendable startup costs should be tracked separately from working capital and required capitalization, because regulatory capital is a funding need, not an operating expense The model also assumes $41M in Year 1 funding liabilities and $14M in other interest-earning assets

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates the capitalized startup assets needed to open a community bank, not ongoing operating cash.

Important limits This calculator includes capitalized startup assets only. It excludes regulatory capital, pre-opening payroll, legal fees, marketing, deposits, inventory, debt service, working capital, and operating runway. Recurring monthly costs such as $18,000 for facilities, $12,000 for core banking, and $85,000 for cybersecurity are separate from CAPEX.

What does the Community Bank model show through Year 5?

This tab shows CAPEX/startup costs by timing, amount, and depreciation/amortization; open the Community Bank Financial Model Template to check assumptions.

Model screenshot highlights

- Launch cash need

- Staffing ramp, $530K payroll

- $345M loans, $14M assets

- $41M liabilities, $587K overhead

How should you build a community bank startup funding plan?

Build the Community Bank funding plan by phase, not as one big raise: tie spending to the organizer stage, application stage, systems implementation, branch readiness, staffing ramp, opening month, and the early operating period. Use the Year 1 base case of $345M in loans, $41M in funding liabilities, and $14M in other interest-earning assets to pace capital needs; the visible monthly fixed cost is $587K plus $530K payroll, or about $1.117M a month. Keep deposits and borrowings separate from regulatory capital, and use financial modeling next to test timing after approval, not as a substitute for it.

Phase funding

- Fund filings and advisor work first.

- Delay branch spend until approvals.

- Match hires to launch timing.

- Open only after systems pass tests.

Model guardrails

- Model $345M loans and $14M assets.

- Track $41M liabilities separately.

- Carry $1.117M monthly fixed cost.

- Use payroll at $530K visibly.

What are the biggest costs to start a community bank?

Community Bank startup costs are dominated by regulation, tech, and people, not the lobby. The listed fixed costs alone total about $174K per month or $2.09M a year before payroll, and a $530K Year 1 staffing load plus $345M in lending growth pushes up underwriting, loan ops, monitoring, and reporting.

Big fixed costs

- $85K/month cybersecurity and IT

- $55K/month compliance systems

- $12K/month core banking system

- $18K/month branch rent and facilities

People and control load

- $4K/month professional services

- $530K Year 1 staffing load

- $345M lending growth needs more staff

- Underwriting and reporting scale fast

What hidden costs of starting a community bank get missed?

The biggest misses are the costs before doors open and the costs that keep burning after launch, and they’re easy to confuse with assets or balance-sheet capital. That’s where How Much Does The Owner Of Community Bank Typically Make? starts to matter, because the owner’s take only shows up after you fund all the hidden startup drag.

$6K insurance, $55K compliance, $4K professional services, and $12K office supplies are recurring items that can get missed fast. Add 45% Year 1 marketing and promotions and 35% card processing fees, and the first-year cash need jumps a lot.

Pre-open costs

- Organizer expenses

- Charter support and legal counsel

- Feasibility studies and accounting

- Compliance readiness and vendor due diligence

Launch burn

- Bonding and insurance

- Policies, training, and payroll

- Operating runway and cash reserve

- Separate assets from expenses

Calculate Fuding Needs

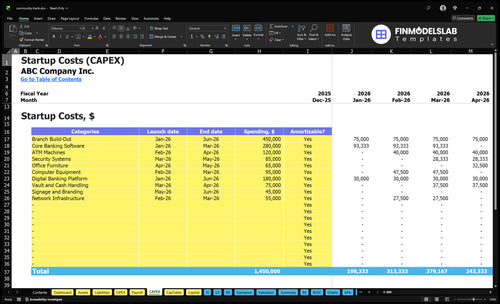

Startup cost summary

Shows the main startup asset costs and the non-CAPEX cash reserve needed to open and run the bank through early growth.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Branch Build-Out | $450,000 | Branch construction, finishes, and fit-out scope | Yes |

| Core Banking Software | $280,000 | Core system setup and launch configuration | Yes |

| Digital Banking Platform | $180,000 | Online and mobile banking build-out | Yes |

| ATM Machines | $120,000 | ATM hardware purchase and installation | Yes |

| Security Systems | $85,000 | Vault, alarm, and access-control hardware | Yes |

| Operating Reserve | $41,153,000 | Month 12 minimum cash need for payroll, overhead, and loan growth | No |

Community Bank Core Five Startup Costs

Regulatory Setup and Professional Advisory Startup Expense

Regulatory Prep Spend

Regulatory setup is mostly prep work, not a one-time buy. Model $55K/month for regulatory compliance and $4K/month for professional services to cover charter support, deposit insurance support, legal counsel, accounting, feasibility studies, policies, governance documents, board materials, and filing packages.

What Drives the Quote

Quote size depends on charter type, state or federal path, organizer group size, application complexity, and expected review rounds. Here’s the quick math: multiply the monthly advisory run-rate by the prep months, then add document-heavy work like board materials, governance drafts, and regulatory exhibits.

- Charter path changes scope.

- More rounds mean more hours.

- Complex filings raise review time.

How To Keep It Tight

Reduce waste by locking the application plan early, using clean drafts, and keeping the organizer group small and responsive. Don’t overbuy legal time for work that compliance staff can finish. The main mistake is treating prep spend like approval inventory; it’s a burn item that can stretch fast if revisions pile up.

- Freeze scope before drafting.

- Reuse policy templates carefully.

- Limit last-minute edits.

Quote Questions

Ask for a quote after you define charter type, state or federal path, organizer count, filing depth, and likely review rounds. Those inputs decide whether the budget stays near the base prep run-rate or climbs with extra legal, accounting, and compliance hours. Keep it tied to months of work, not approval probability.

Core Banking Technology and Cybersecurity Startup Expense

Core Stack

This startup cost covers core processing, online and mobile banking, payment connections, data security, identity tools, reporting, BSA/AML tools, testing, data conversion, and integrations. Keep one-time implementation separate from recurring fees. The model uses $12K/month for the core system and $85K/month for cybersecurity and IT.

Price It

Price the setup work from account volume, the number of interfaces, and managed service scope. Ask vendors to split implementation, testing, conversion, and training so the quote is usable. Here’s the quick math: one-time setup plus 12 months of recurring fees gives a cleaner first-year budget.

- Account volume changes setup load

- Interfaces drive testing time

- Managed scope lifts monthly fees

Card Fees

Card processing fees are a variable cost, not a core software cost. In the model, they run at 35% in Year 1 and step down to 25% by Year 5 as volume and mix improve. Track interchange, processor charges, and fraud controls from day one.

Keep It Lean

Cut spend by standardizing reports, limiting custom interfaces, and using default workflows where they still meet policy. Don’t skimp on BSA/AML, identity checks, or testing; weak controls get expensive later. The biggest quote swing comes from account count, interfaces, and managed service scope.

Branch Buildout, Equipment, and Security Startup Expense

Buildout Scope

Branch startup spend usually covers lease deposits, tenant improvements, teller stations, vault or cash handling space, ATM setup, signage, furniture, cameras, alarms, access control, workstations, network gear, and secure storage. Treat most of it as CAPEX or leasehold improvements, not operating expense. Size it by square footage, branch count, and cash handling needs.

Cost Inputs

Start with landlord allowance, then add vendor quotes for each unit: deposit, buildout, furniture, security, and IT. Recurring facility references are $18K/month branch rent and facilities, $35K/month utilities and maintenance, and $12K/month office supplies. These are operating costs, while buildout stays on the startup budget.

- Price by square feet.

- Separate cash and IT quotes.

- Use landlord credits first.

Keep It Clean

Do not mix branch buildout with regulatory capital. A safer budget trims scope through landlord-funded finishes, shared secure storage, and right-sized cash handling. Get quotes on square footage and branch count, then compare to allowance. One-liner: if the landlord pays more, your cash need drops fast.

- Push for tenant improvement allowance.

- Reuse fixtures where safe.

- Right-size ATM and vault scope.

Quote Inputs

Ask for pricing by square footage, branch count, cash handling model, and landlord allowance. A small branch with light cash activity needs less vault, security, and ATM scope than a full-service site. That keeps the estimate tied to the actual opening plan, not a generic bank template.

Staffing Readiness and Pre-Opening Payroll Startup Expense

Pre-Open Payroll

Pre-opening payroll covers hiring and training before doors open, so it is separate from post-launch operating payroll. For this bank, visible Year 1 salaries total $530K: $95K branch manager, 2 loan officers at $72K each, 3 tellers at $38K each, $85K compliance officer, and $92K IT manager.

What It Covers

Build the estimate from headcount × salary, then add recruiting fees, training, payroll taxes, and benefits before opening. Here’s the quick math: the named roles already total $530K, and that does not yet include pre-launch overhead. One clean rule: separate launch payroll from the steady-state Year 1 run rate.

- Count only pre-open months.

- Add taxes and benefits.

- Keep launch payroll separate.

Ramp Control

Staffing should scale with loan volume, not vanity hiring. The model rises from 2 FTE loan officers in Year 1 to 6 FTE in Year 5, and tellers from 3 FTE to 7 FTE. To keep cash burn in check, phase hires close to opening dates and delay nonessential back-office add-ons until workload proves out.

Readiness Check

Executive leadership, compliance, and IT need to be in place early because delays here push the whole launch. The practical test is simple: if recruiting takes longer than planned or training runs past the open date, pre-opening payroll grows fast, so hire to the launch schedule and not the wish list.

Insurance, Marketing, and Launch Readiness Startup Expense

Launch Spend

Count insurance, bonding, opening marketing, community outreach, signage, vendor onboarding, policies, supplies, training, and opening-day prep as pre-opening expense, not capital. For this bank, model $6K/month insurance premiums, $12K/month office supplies, and marketing and promotions at 45% in Year 1, easing to 25% by Year 5.

Cost Inputs

Estimate this from quote counts, months of coverage, and the opening date. Insurance and bonding need term quotes; supplies need units × unit price; launch marketing needs a Year 1 spend plan. Keep this spend tied to deposit gathering, borrower pipeline, and local trust, but do not let it crowd out technology, compliance, or capitalization.

Keep It Tight

Use opening marketing for local proof, not broad reach. Focus on community events, branch signa ge, and referral push that can be tracked by account opens and loan leads. One clean rule: spend enough to open strong, then step down fast if the pipeline does not move.

Board Check

Before launch, separate these costs from regulatory prep and branch buildout. The right question is simple: will this expense help gather deposits, win borrowers, and build local trust in the first months? If not, trim it, because launch spend should support the opening plan without overstating the bank’s technology, compliance, or capital needs.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Branch size, tech depth, compliance support, and staffing change the cash need fast. Base anchors to $587K monthly fixed overhead, $530K visible Year 1 payroll, $345M Year 1 loans, and $41M funding liabilities.

| Scenario | Lean LaunchCapital light | Base LaunchModel anchored | Full LaunchBroader scope |

|---|---|---|---|

| Launch model | Start with one branch, a narrower product set, and lighter staffing depth where allowed. | Run the modeled base case with standard branch coverage, full lending mix, and planned Year 1 staffing. | Expand branch reach, lending depth, operations support, and compliance coverage from the start. |

| Typical setup | Use core banking software, a small branch footprint, basic digital banking, and lean compliance support. | Use one branch, digital banking, in-house compliance, and the staffing plan reflected in Year 1. | Add deeper loan coverage, more operations staff, stronger controls, and broader market reach. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | Lower seven figuresTight scope | High seven figuresCore build | Low eight figuresExpanded build |

| Best fit | Fits a founder who wants a local start and can keep the launch market narrow. | Fits an operator ready to serve local residents and small businesses at the modeled base scale. | Fits a team with enough capital and execution depth to pursue broader market coverage from day one. |

Planning note: These scenario ranges are researched planning assumptions, not exact vendor quotes or regulatory capital offers.

Related Products

- Community Bank Porter's Five Forces Analysis

- Community Bank BCG Matrix

- Community Bank Business Model Canvas

- 7 Critical KPIs to Guide Community Bank Profitability

- Community Bank Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Community Bank Profitability

- How Much Does It Cost To Operate A Community Bank Monthly?

- Community Bank Financial Model Template in Excel

- How Much Community Bank Owners Can Make From $485M In Earning Assets

- Start a Community Bank: 18–36 Month US Launch Path

- How to Write a Community Bank Business Plan (7 Steps)

- Community Bank Marketing Mix

- Community Bank Marketing Plan

- Community Bank Business Proposal

- Community Bank PESTEL Analysis

- Community Bank Pitch Deck Example Editable PPTX

- Community Bank Business SWOT Analysis

- Community Bank Value Proposition Canvas

Frequently Asked Questions

No, regulatory capital is a funding requirement, not a normal operating expense Your budget should still show it beside CAPEX, pre-opening costs, and working capital because it drives total money raised In this model, operating costs include $587K monthly fixed overhead, $530K visible Year 1 payroll, and $345M in Year 1 planned loans