Owner income$150k

Owner income$150kHow Much Does A Community Outreach Agency Owner Make At $344K Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k  Net margin-17% to 25%

Net margin-17% to 25% Revenue for target pay$601k

Revenue for target pay$601k Business difficultyHard

Business difficultyHard

You’re weighing owner pay against payroll, client work, and cash reserves This five-year model shows $150,000 in modeled owner salary, Year 1 revenue of $344,000, Year 1 EBITDA of -$58,000, and breakeven in Month 9 It excludes tax advice, guaranteed distributions, debt service, and personal benefit planning

Owner income$150kNet margin-17% to 25%Revenue for target pay$601kBusiness difficultyHardWant to test your owner pay number?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, staffing costs, overhead, reserves, and your pay goal.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

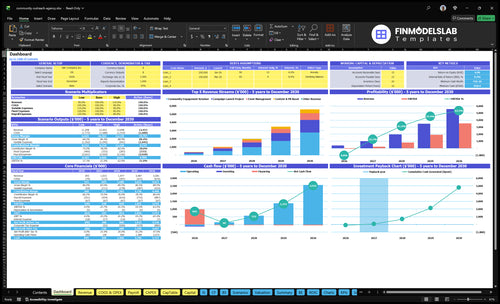

How does the Community Outreach Agency model show owner income?

The screenshot maps owner income from dashboard to cash flow, with Year 1 revenue of $344,000, Year 2 revenue of $922,000, and EBITDA from -$58,000 to $230,000; open the Community Outreach Agency Financial Model Template.

Owner-income model highlights

- Owner take-home output

- Revenue, margin, cash flow

- Month 9 breakeven

How much revenue does a community outreach agency need to pay the owner?

If the Community Outreach Agency wants to pay the owner and cover Year 1 costs, it needs about $427,000 in revenue. Here’s the quick math: $299,100 of fixed payroll, overhead, and marketing divided by a 70% contribution margin gets you there, while the modeled Year 1 revenue of $344,000 still leaves about -$58,000 EBITDA.

Year 1 breakeven

- $217,500 modeled payroll

- $66,600 fixed overhead

- $15,000 marketing budget

- $427,000 revenue needed

What the model says

- 70% contribution margin after delivery costs

- $344,000 researched Year 1 revenue

- -$58,000 EBITDA gap

- Targets are planning assumptions, not promises

Can a community outreach agency owner make a living?

Yes, a Community Outreach Agency owner can make a living, but owner salary must be treated separately from profit distributions; for this model, the CEO / Lead Strategist salary assumption is $150,000. The pressure point is cash timing: Year 1 EBITDA is -$58,000, breakeven arrives in Month 9, and What Is The Most Effective Strategy To Measure Community Outreach Agency's Impact? helps tie client results to retention and pricing.

Pay Reality

- Plan salary at $150,000

- Fund Year 1 EBITDA gap: -$58,000

- Reach breakeven by Month 9

- Convert clients early to protect cash

Profit Rules

- Separate salary from distributions

- Use Year 2 EBITDA: $230,000

- Hold reserves for taxes and hiring

- Reinvest before taking extra cash

What is a typical community outreach agency profit margin?

A typical Community Outreach Agency can show a 70% delivery margin in Year 1, improving to 82% by Year 5, but EBITDA can swing from -168% in Year 1 to about 250% in Year 2 as fixed overhead gets spread across more revenue. If you’re also sizing launch costs, see What Is The Estimated Cost To Open And Launch Your Community Outreach Agency? because direct delivery costs and fixed overhead move differently.

Delivery margin shift

- 70% in Year 1

- Rises to 82% by Year 5

- Materials, logistics, software, travel fall

- Higher revenue lifts margin percentage

Profit gets distorted

- -168% EBITDA in Year 1

- About 250% by Year 2

- Overhead and staffing spread out

- Owner take-home can still stay tight

Which drivers move owner income most?

1

70%Contract mix

A 70% retainer mix steadies monthly cash and lowers churn risk, so owner income is less exposed to one-off projects.

2

$120-$140/hrScope control

Staying in the $120-$140 hourly band while holding scope tight protects margin, and creep is the main leak.

3

70%Delivery margin

Keeping delivery margin near 70% leaves more revenue after direct labor, which is where owner profit is won or lost.

4

$1.5KClient pipeline

At a $1.5K CAC, retention has to stay strong so each new client covers sales cost across more months.

5

$150KOwner utilization

The $150K owner salary only pays off with strong billable load, because nonbillable time drops net income fast.

6

$830KOverhead reserve

An $830K cash floor and $66.6K of fixed overhead mean slow collections can drain profit before the model breaks even.

Community Outreach Agency Core Six Income Drivers

Contract Mix And Revenue Quality

Retainer-Led Revenue Quality

This income driver is the mix between retainers and one-off work. In this model, a 40-hour retainer at $120 per hour equals $4,800 per client period before delivery costs, so steady retainers support payroll and owner pay better than event-heavy revenue.

Campaign launches and event management can still be profitable, but they can also swing cash flow. The Year 1 mix leans on 70% community engagement retainer work, with 60% campaign launch projects, 20% event management, and 15% content and PR boost work, so revenue quality matters more than headline revenue.

Track Mix, Not Just Sales

Measure active retainer hours, project start dates, and how much time gets eaten by scope changes. If a project turns into extra meetings, unpaid revisions, or delayed delivery, margin drops fast even when revenue looks strong.

- Track billable hours by contract type.

- Price scope changes before work starts.

- Match staffing to campaign timing.

- Forecast cash by renewal and launch dates.

One clean rule helps: protect the recurring base first. Retainers make income easier to forecast, while project work should only take on if staffing, timing, and handoffs are tight enough to keep owner pay from getting squeezed.

1

Pricing And Scope Control

Pricing and Scope Control

This driver is the price you charge for planning time, field coordination, meetings, reporting, stakeholder management, and scope changes. For Year 1, the rate card is $120/hour for retainers, $130/hour for campaign launch, $140/hour for event management, and $135/hour for content and PR boost.

Here’s the quick math: underpricing one 40-hour retainer by $10/hour cuts $400 from that client period before costs. Scope creep pushes paid work into non-billable time, so weak pricing hits gross margin first and owner pay soon after.

Protect the Billable Hour

Track three inputs: billable hours, non-billable hours, and scope changes. If a proposal does not name meetings, revisions, travel, reporting, and approval steps, the margin leaks fast. Strong scopes protect cash flow because every unpaid change lowers the money left for payroll, overhead, and the owner’s draw.

- Set a rate by service type.

- Cap revisions and meeting rounds.

- Charge for added scope changes.

- Review hours against the proposal.

2

Delivery Labor And Campaign Margin

Delivery Labor And Campaign Margin

This driver is the gap between client fees and direct delivery costs. Year 1 assumes 12% for campaign materials, 8% for third-party event logistics, 7% for software and tools, and 3% for travel and entertainment, so direct cost totals 30% and leaves a 70% contribution margin before payroll and overhead.

That margin funds field outreach labor, subcontractors, event support, and reporting time. On $100 of client fees, only $70 is left before salaries, rent, and owner pay, so any overrun in labor or logistics cuts take-home income fast.

Protect Direct Margin

Track each campaign by fee, direct cost, and labor hours. The key input set is client fee, materials, logistics, tools, travel, and subcontractor spend. If actual direct cost moves above 30%, the owner’s draw shrinks because less cash is left for payroll and overhead.

- Price field work by budgeted hours.

- Lock subcontractor caps upfront.

- Bill scope changes immediately.

- Review margin by client weekly.

Keep reporting and event support inside the contract budget. If extra visits or revisions keep piling up without a fee change, the job still looks busy but the profit leaks out of the owner’s pocket.

3

Owner Utilization And Founder Role

Owner Utilization Shift

Billable owner hours can lift early revenue, but they cap growth when every client needs the founder. In this model, the CEO / Lead Strategist salary stays at $150,000 across all five years, so the real gain comes from moving delivery to account managers and specialists while the owner focuses on sales, quality control, and senior strategy.

Here’s the quick math: if the founder keeps filling staffing gaps for free, payroll still rises but margins do not. That hurts cash flow and can trigger burnout, missed sales follow-up, and weaker owner pay. One line matters most: founder time should buy revenue, not replace payroll.

Track Founder Time, Not Just Revenue

Measure owner hours in three buckets: selling, delivery, and rework. If delivery stays high after the team grows, the founder is acting like a free employee, not a manager. Track billable hours, close rate on follow-up, and the share of work handled by staff versus the owner. That shows whether the business can support the $150,000 salary and still pay profit.

Use a simple rule: shift the founder away from meetings that can be delegated and toward work that protects margin. Keep the owner on sales, quality control, and senior client strategy. If the owner’s billable load stays high while payroll grows, profit per client falls and take-home income gets squeezed.

- Track billable vs. non-billable hours

- Limit free staffing gaps

- Delegate routine client meetings

- Review margin by account monthly

4

Client Acquisition And Retention

Client Renewal And Replacement

Client acquisition and retention covers new wins, renewals, and replacements when outreach campaigns end. With $15,000 in Year 1 marketing and $1,500 CAC (customer acquisition cost), the model supports about 10 clients ($15,000 ÷ $1,500). If clients do not renew, revenue falls fast, and owner pay gets squeezed because payroll stays fixed.

No renewal, no paycheck. Year 2 marketing rises to $25,000 with $1,400 CAC, which implies about 18 clients ($25,000 ÷ $1,400). That only helps if the pipeline stays full; gaps create idle staff, lower utilization, and weaker cash flow, so the business can look active while take-home income slips.

Track Renewals Before You Chase New Leads

Measure contract end dates, renewal rate, and how many clients move into repeat retainers. Also track referral volume and closeout report delivery, because clear handoffs help the next sale and cut replacement cost.

- Map every campaign end date.

- Ask for renewal before closeout.

- Document results for referrals.

5

Overhead, Reserves, And Reinvestment

Overhead, Reserves, and Owner Pay

For a community outreach agency, fixed overhead is the cost of staying ready to deliver. Here it totals $66,600 per year, or $5,550 per month, from $3,500 rent, $400 utilities, $250 supplies, $30 0 insurance, $750 accounting and legal, $150 hosting, and $200 communications.

That spend lowers immediate owner income, but it protects service quality and cash stability. Profit after overhead is not always take-home pay, because cash must also cover reserves, hiring, taxes, startup costs, and reinvestment. With a $830,000 minimum cash need in Month 2, early profit should be treated as working capital, not owner draw.

Track Cash Before You Take Draws

Measure monthly fixed overhead, cash runway, and reserve balance before setting owner pay. Here’s the quick math: annual overhead of $66,600 equals $5,550 a month, so every month of weak collections hits the owner fast. If collections slip, the draw has to slow first.

- $5,550 monthly fixed overhead

- $830,000 Month 2 cash need

- Reserve for taxes and payroll

- Delay draws until cash is stable

Track the inputs that change this driver: rent, payroll timing, tax set-asides, and reinvestment needs. If reserves are thin, keep profit in the business until cash can absorb a slow client renewal or a hiring step without forcing a personal pay cut.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income swings with client conversion, staffing, and cash control. The low case stays cash tight, while the base and high cases track the model's Month 9 breakeven and later-year scale.

| Scenario | Low CaseCash tight | Base CaseBreakeven path | High CaseScale case |

|---|---|---|---|

| Launch model | Slower client conversion and a heavy owner salary create a cash-tight start. | Modeled revenue reaches $344,000 in Year 1, then $922,000 in Year 2 as breakeven lands in Month 9. | Later-year scale pushes revenue toward $1.832 million in Year 3 with $820,000 EBITDA. |

| Typical setup | The business stays founder-led, with softer retainers, fewer projects, and the $150,000 owner salary pressuring cash. | A balanced mix of retainer, project, event, and PR work supports Year 1 revenue of $344,000 and Year 2 EBITDA of $230,000. | Stronger retention, fuller staffing, and tighter cash control let the agency scale while Year 3 EBITDA reaches $820,000. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Near-zero take-homeCash tight | Year 2 positive take-homeBreakeven path | Scale-case upsideScale case |

| Best fit | Use this to test the early cash squeeze if sales close slowly and the founder still carries most of the delivery load. | Use this as the main planning case for budgeting, hiring, and owner pay once the model reaches breakeven. | Use this to test upside if client retention holds, staffing stays efficient, and cash control keeps pace with growth. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Community Outreach Agency Porter's Five Forces Analysis

- Community Outreach Agency BCG Matrix

- Community Outreach Agency Business Model Canvas

- 7 Critical KPIs to Track for Your Community Outreach Agency

- Community Outreach Agency Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Community Outreach Agency Profitability

- Analyzing the Monthly Running Costs for a Community Outreach Agency

- Community Outreach Agency Startup Costs: $535K CAPEX To $830K Cash

- Community Outreach Agency Financial Model Template in Excel

- How To Open A Community Outreach Agency In 4 To 10 Weeks

- How to Write a Community Outreach Agency Business Plan

- Community Outreach Agency Marketing Mix

- Community Outreach Agency Marketing Plan

- Community Outreach Agency Business Proposal

- Community Outreach Agency PESTEL Analysis

- Community Outreach Agency Pitch Deck Example Editable PPTX

- Community Outreach Agency Business SWOT Analysis

- Community Outreach Agency Value Proposition Canvas

Frequently Asked Questions

The researched model includes a $150,000 CEO / Lead Strategist salary from launch That does not mean the business fully funds it in Year 1, because EBITDA is -$58,000 on about $344,000 revenue Early owner pay may rely on startup cash until Month 9 breakeven and stronger Year 2 EBITDA of $230,000