Owner income$250K

Owner income$250KHow Much Does a Condo Development Owner Make With $250K Operator Pay

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$250K  Net marginN/A

Net marginN/A Revenue for target payN/A

Revenue for target payN/A Business difficultyHard

Business difficultyHard

Key Takeaways

- Pricing drives sellout value and every concession matters.

- Land timing and density can make or break returns.

- A 1% hard-cost overrun can erase $27.5M.

- Closings, not reservations, unlock owner cash and profit.

Owner income$250KNet marginN/ARevenue for target payN/ABusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, debt, reserves, taxes, and ownership terms. It is not guaranteed salary, tax advice, or owner distribution advice.

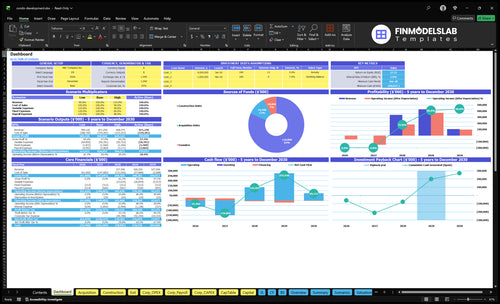

How do you check owner income in a Condo Development pro forma?

This screenshot from the Condo Development Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions—open the model.

Owner-income model highlights

- Owner take-home dashboard

- Unit mix and pricing

- EBITDA, cash curve, IRR

- Acquisition and build timing

- Hard costs and capex

- Payroll and fixed expenses

- $735M land cost

- $2,750M construction cost

- -$2,408M minimum cash

- $4,390M cumulative EBITDA

How do construction and financing costs impact condo development profit margin?

For Condo Development, profit margin gets hit first by hard-cost overruns and interest carry; the model’s $2,750M construction budget means a 1% overrun is $275M before financing ripple, and slow closings can worsen the -$2,408M minimum cash point. For build-cost context, see How Much Does It Cost To Open, Start, Launch Your Condo Development Business? Sales and brokerage commissions also fall from 60% to 40% by model year, while soft costs drop from 25% to 15%.

Cost pressure

- 1% overrun adds $275M

- Hard costs hit margin first

- Interest carry rises with delays

- Closings stretch cash needs

Margin drivers

- Commissions fall from 60% to 40%

- Soft costs fall from 25% to 15%

- Slow sales extend carry

- Cash strain can deepen losses

How does project scale change small condo development owner income?

For Condo Development, bigger project scale can raise owner income, but it also ties up far more cash and pushes distributions out. With 6 owned projects, $735M of land, and $2.75B of construction, about $3.485B is in play before payback. The owner may earn $250K/year for development leadership, but the real upside shows up late, and here payback hits at Month 44.

Income upside

- More units can lift total profit.

- $250K/year covers leadership work.

- 6 projects spread income across deals.

- Scale can widen the upside if sold well.

Income drag

- $3.485B ties up a lot of capital.

- Needs lenders, investors, and brokers.

- Needs project and construction managers.

- Month 44 payback delays cash recovery.

Is condo development profitable?

Yes, Condo Development can be profitable in the base model, but only after a heavy cash trough; see What Is The Current Market Reception To Condo Development? before treating profit as owner cash. The model shows $43.90M cumulative EBITDA, 27.12% ROE, 0.03% IRR, breakeven in Month 31, and payback in Month 44.

Profit signals

- Cumulative EBITDA: $43.90M

- ROE: 27.12%

- Breakeven: Month 31

- Payback: Month 44

Cash risk

- Year 1 EBITDA: -$6.18M

- Year 2 EBITDA: -$14.87M

- IRR is thin at 0.03%

- One delay can push distributions out

Want to see what changes owner income fastest?

1

HighSale Price

Higher unit prices flow through after the 5.5%-8.5% project cost load, so this sets the biggest swing in owner distributions.

2

$275MBuild Cost

The construction budget is the largest cash use, and overruns hit equity value fast.

3

$73.5MLand Basis

The land base has to be recovered before take-home cash starts to build.

4

M31-M44Closing Timing

Sales start in Month 31 and payback lands in Month 44, so faster closings bring cash back sooner.

5

5.5%-8.5%Soft Carry

Broker commissions and soft costs take a fixed slice of revenue, and every point saved stays in equity.

6

27.12%Owner Share

The equity split decides how much of the project gain turns into take-home cash for owners.

Condo Development Core Six Income Drivers

Unit Sale Pricing And Sellout Value

Unit Sale Pricing

Unit sale pricing drives owner income because gross sellout value is the pool that pays costs, reserves, investors, and owner distributions. It is average unit price × unit count, adjusted for concessions, unit mix, and closing volume. The source data does not include sale price or units, so profit per unit stays blank until those inputs are entered.

- Inputs: price, units, concessions, mix, closings

- Watch: net sellout, not list price

Protect Net Price

Here’s the quick math: each price change flows through after commissions of 60% to 40% and soft costs of 25% to 15%. So a small cut in unit price can hit profit fast, while a better unit mix can lift cash without adding much cost. Slow closing volume still delays cash and owner draws.

- Track: net proceeds per closed unit

- Test: concessions before price cuts

- Control: closing pace by month

1

Land Basis And Entitlements

Land Basis and Entitlements

Land basis and entitlements decide how much profit is left before construction starts. The model carries $735M of owned land across 6 projects, or about $122.5M per project on average. Higher allowable unit count and density spread that cost; weak approvals or slow timing push closings and owner take-home cash further out.

Entitlements are the public approvals that let the project build the planned units. Track acquisition price, approval timing, carrying period, and entitlement cost, because every delay adds cash drag before sales begin. There is no rental cost buffer here, so the site must work against realistic sellout and duration assumptions.

Buy for Density and Timing

Buy the site on the unit count you can actually permit, not the one you hope for. Test the land price against realistic sellout speed and approval months, because a deal that only works at peak density leaves owner income exposed if zoning stalls or the market softens.

Track land cost per approved unit, approval months, and project carry on every case. If higher density lowers the land burden, great; if delays stretch the carrying period, treat that as a margin hit and rework the model before committing capital.

2

Hard Construction Cost Control

Hard Cost Control

Hard construction cost control is where condo profit gets protected or lost. Hard costs include labor, materials, general contractor pricing, change orders, parking, finishes, and building systems. With a $2,750M budget over 15 to 20 months, a 1% overrun equals $27.5M in lost margin before financing. That comes straight out of owner distributions.

Track Cost Drift Fast

Watch committed cost, forecast-to-complete, and approved change orders every week. Lock scope early, compare trade bids to budget, and force quick sign-off on late changes, since they cost the most near completion. The key inputs are labor, materials, GC pricing, parking, finishes, and building systems. If change orders pile up late, owner pay drops even if sales stay strong.

3

Soft Costs And Financing Carry

Soft Costs And Carry

Professional fees, insurance, legal, marketing, loan fees, and interest all hit profit before the owner sees cash. In this model, variable soft costs run 25% in Year 1, then 23%, 20%, 18%, and 15% by Year 5, while fixed overhead is $26K/month and payroll rises from $445K to $735K. Higher leverage, longer timelines, and slower draws cut take-home income.

Here’s the quick math: every extra point of soft cost or interest lowers net project profit, so delays can turn paper margin into carry expense. To estimate owner income, you need loan size, rate, draw schedule, closing timing, and total soft-cost budget; without those inputs, distributions and profit stay incomplete.

Track Carry Before It Eats Distributions

Measure soft costs as a percent of hard cost and track them monthly, not just at closing. If Year 1 soft costs stay near 25%, then a miss on legal, insurance, or marketing can hit cash flow fast because $26K/month of overhead keeps running even when units are not closing.

- Track fees by vendor and phase.

- Match loan draws to spend timing.

- Model interest through final close.

- Update payroll against project pace.

What this estimate hides: lender rules and the draw schedule can raise carry even when the build stays on plan, so keep a monthly forecast and refresh it when timing slips.

4

Sales Absorption And Closing Timing

Sales Absorption Timing

A signed unit is not cash. Owner income starts when buyers close and the lender clears releases, so absorption is the pace from contract to closing, not just interest in the project. In this model, sale starts run from Month 31 through Month 54, with breakeven in Month 31 and payback in Month 44.

Here’s the quick math: faster closings pull cash forward, cut interest carry, and shorten the wait to owner distributions. Slow sellout can stretch the -$2,408M cash trough. The main risk is counting presales as revenue before closing, which overstates take-home income and timing.

Track Closings, Not Hype

Measure presales, reservations, cancellations, closing pace, concessions, and inventory aging every month. If aged units build up, cash stays locked, interest carry rises, and owner pay slips later even if headline demand looks strong.

Use lender release rules in the forecast, not just signed contracts. Test monthly closings against the Month 31 to Month 54 sales window, and flag any slip that could push payback past Month 44. One delayed closing can matter more than several new reservations.

- Track contract-to-close days.

- Watch concession dollars per unit.

- Age inventory by unit and stack.

5

Capital Stack And Owner Profit Share

Capital Stack And Owner Pay

If the project looks profitable, your take-home can still be thin. The capital stack decides who gets paid first: debt service, reserves, investor prefs, taxes, then the owner. A model can show 2712% ROE, but if cash lands late, 003% IRR means little money is available when you need to pay yourself.

This driver includes debt, owner equity, outside equity, preferred returns, guarantees, developer fees, reserves, and the promote split. EBITDA is not take-home pay. Owner income depends on the waterfall, the order cash gets paid. If the waterfall favors investors or holds back cash for reserves, the owner draw drops even when the project clears the profit target.

Track The Waterfall Before You Split Profit

Model monthly cash after debt service, reserve top-ups, and investor preferred returns, then test what is left for the owner. Put hard caps on fees and guarantees, because those claims can move cash out of the owner lane before profit is shared. Here’s the quick math: if cash is trapped in reserves or unpaid prefs, owner pay waits.

- Debt balance and interest rate

- Preferred return and promote split

- Developer fee and guarantee terms

- Reserve balance and refill rules

- Tax timing and reinvestment needs

If the deal needs reinvestment to finish the next phase, treat that as cash locked up, not spendable profit. The clean test is simple: after debt service, reserves, and investor claims, what cash still reaches the owner? If the answer is thin, the capital stack is too heavy for the project’s cash flow.

6

Compare low, base, and high condo development owner income scenarios

Owner income scenarios

Owner income swings hard here because cash is tied up early in land and construction, then comes back as units close. Delayed sales, higher build costs, and financing carry can cut distributions.

| Scenario | Low CaseLow | Base CaseBase | High CaseHigh |

|---|---|---|---|

| Launch model | This is the weaker earnings path, where income stays tight until sales catch up. | This is the modeled path with steady project delivery and planned owner compensation. | This is the stronger earnings path, where pricing and closings beat the base case. |

| Typical setup | Sales close later, build costs run hotter, and cash stays trapped longer, so owner income leans toward salary with thin upside. | Six owned projects, $73.5M land, $275M construction, and a $250k owner salary point to Month 31 breakeven, Month 44 payback, and 2712% ROE. | Faster closings, better pricing, and tighter build costs lift distributions above the base case while the owner keeps the same core salary. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $250k salary, limited distributionsLow | $250k salary, modeled distributionsBase | $250k salary, stronger distributionsHigh |

| Best fit | Use this to stress delayed sales, cash strain, and lower owner draws. | Use this as the core plan for funding, hiring, and cash timing. | Use this to test upside from faster absorption and tighter cost control. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Condo Development Porter's Five Forces Analysis

- Condo Development BCG Matrix

- Condo Development Business Model Canvas

- 7 Critical Financial KPIs for Condo Development

- Condo Development Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Condo Development Profit Margins

- How Much Does It Cost To Run Condo Development Each Month?

- Condo Development Startup Costs: $2408M Cash Need Before Sales

- Pre-Built Condo Development Financial Model Template in Excel

- How To Open A Condo Development Company In 18 To 36+ Months

- How to Write a Condo Development Business Plan: 7 Steps

- Condo Development Marketing Mix

- Condo Development Marketing Plan

- Condo Development Business Proposal

- Condo Development PESTEL Analysis

- Condo Development Pitch Deck Example Editable PPTX

- Condo Development Business SWOT Analysis

- Condo Development Value Proposition Canvas

Frequently Asked Questions

In this model, the clearest owner pay is the $250,000 annual CEO / Head of Development salary Larger take-home depends on distributions after closings, debt, reserves, taxes, reinvestment, and investor payouts EBITDA totals about $4390M over five years, but that is not the same as cash the owner can withdraw