Owner income$277k–$4.08M

Owner income$277k–$4.08MHow Much Conflict Resolution Consulting Owners Make: $150K+ Plan

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$277k–$4.08M  Net margin24%–70%

Net margin24%–70% Revenue for target pay$44k/mo–$468k/mo

Revenue for target pay$44k/mo–$468k/mo Business difficultyHard

Business difficultyHard

You’re building a US conflict resolution consulting business where owner income comes from paid client work, service mix, and cost control This model plans a $150,000 founder salary, first-year revenue of about $532,000, and EBITDA of $127,000 before taxes, reserves, debt, or distributions

Owner income$277k–$4.08MNet margin24%–70%Revenue for target pay$44k/mo–$468k/moBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on demand, staffing, taxes, reserves, and distributions, and it is not guaranteed salary, tax advice, or owner distribution advice.

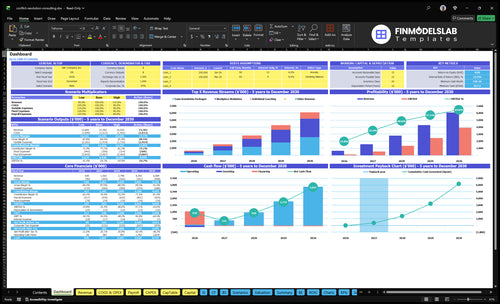

How do you check owner income in the Conflict Resolution Consulting model?

This screenshot shows assumptions, revenue, margin, costs, reserves, and owner take-home; open the Conflict Resolution Consulting Financial Model Template to review it.

Owner-income model highlights

- Owner pay is explicit

- Revenue spans $532k to $562M

- EBITDA spans $127k to $3.932B

- Breakeven hits by Month 6

- Payback lands in 15 months

How much revenue does a conflict resolution consultant need to pay themselves?

For Conflict Resolution Consulting, the Year 1 revenue target is about $532,000 if you want to cover a $150,000 founder salary, $187,500 in payroll, and $73,800 of fixed overhead. Here’s the quick math: $127,000 EBITDA plus payroll and overhead totals $388,300, and at a 73% contribution margin, that implies about $531,918 in collected revenue. The cash plan matters too: minimum cash need reaches $818,000 in Month 2, so collected revenue matters more than booked revenue.

Year 1 revenue target

- $150,000 founder salary

- $187,500 Year 1 payroll

- $73,800 fixed overhead

- About $532,000 revenue needed

Cash and margin pressure

- 73% contribution after variable costs

- 27% variable cost drag

- $818,000 minimum cash need

- Collected revenue beats booked revenue

How much does a conflict resolution consulting business owner make?

A Conflict Resolution Consulting owner can make $150,000 in founder salary in Year 1, with $127,000 EBITDA left in the model before taxes and reinvestment; for the main success signal behind that income, see What Is The Main Indicator That Shows The Success Of Conflict Resolution Consulting?. By stage, the model moves from solo income to boutique profit to scaled practice economics, but EBITDA is not automatic take-home pay.

Owner Pay By Stage

- Solo launch: $150,000 founder salary

- Year 1 EBITDA: $127,000

- Stable boutique revenue: $1.359 million

- Year 2 EBITDA: $552,000

What Owners Keep

- Scaled Year 5 revenue: $5.62 million

- Scaled Year 5 EBITDA: $3.932 million

- Pay comes after taxes

- Reserve for debt, hiring, and growth

Can a conflict resolution consulting business scale beyond the owner?

Yes—Conflict Resolution Consulting can scale beyond the owner, but the founder’s job shifts from billable expert to manager of quality, people, and process. In the model, payroll grows from $187,500 in Year 1 to $715,000 in Year 5, while direct consultant fees fall from 12% to 8% of revenue. So the business can grow, but more revenue can also mean less control and more review time.

Owner-led model

- Founder sells most billable hours

- Revenue ties to realized rate

- Capacity stays capped fast

- Quality control stays simple

Scaled model

- Add senior mediators and juniors

- Use ops, marketing, and admin

- Payroll rises to $715,000

- Founder spends more time reviewing

Want the six income drivers?

1

$720-$6.8KService Mix

Mixing in team packages moves the average ticket from about $720 to $6.8K and lifts owner take-home before taxes fastest.

2

4-19hBillable Hours

More billable hours per engagement spread fixed costs and raise owner take-home before taxes.

3

$180-$360Realized Rate

Higher hourly rates turn the same booked work into more revenue and more owner take-home before taxes.

4

$800-$1KAcquisition Cost

Lower CAC keeps more of the marketing budget working for booked cases, so more profit reaches the owner.

5

86%-91%Gross Margin

Lower consultant and platform fees leave more of each dollar for owner take-home before taxes.

6

$818KRunway

The model needs $818K minimum cash in Month 2, so reserve discipline can protect owner take-home during the ramp.

Conflict Resolution Consulting Core Six Income Drivers

Pricing And Realized Rate

Pricing And Realized Rate

Pricing is the fastest income lever here because higher rates raise revenue without the same cost increase. Year 1 rates are $250/hour for workplace mediation, $180/hour for individual coaching, and $300/hour for team packages; Year 1 engagement values are $2,000, $720, and $4,500.

By Year 5, rates rise to $290, $200, and $360—about 16%, 11%, and 20% higher. The catch is realized rate: intake calls, prep, documentation, travel, and follow-up all dilute take-home income if they are not priced in or tightly capped.

Raise the Realized Rate

Measure realized rate as collected revenue divided by total time, not just billed hours. Track booked hours, unpaid admin, travel, and collections by service line so you can see which jobs pay less than they look. One clean rule: if a service needs more hidden time, its sticker price must cover it.

- Billable hours by service

- Unpaid intake and follow-up time

- Prep, documentation, and travel

- Collected revenue per engagement

- Rate by service line

Raise income by charging for prep-heavy work, setting minimum engagement fees, and keeping no-show or late-change policies tight. If hourly work keeps hiding admin time, owner pay falls even when bookings stay steady. The goal is simple: move more of each engagement into paid time and less into off-the-clock labor.

1

Billable Utilization

Billable Utilization

Billable utilization is the share of working time that turns into paid client hours. In this consulting model, workplace mediation uses 8 to 12 hours per engagement, coaching stays at 4 hours, and team packages use 15 to 19 hours. The catch is that sales, scheduling, prep, notes, and follow-up are still work, so owner income drops fast if those hours are treated as billable.

Here’s the quick math: one lost team package can remove $4,500 in Year 1 revenue and $6,840 in Year 5 revenue. So the real driver is not just how busy the calendar looks, but how much of that time is paid work versus admin. Paid workload is what funds take-home pay.

Track billable time by engagement type

Measure billable hours and non-billable hours separately for mediation, coaching, and team work. Use one log for intake calls, prep, notes, travel, and follow-up, then compare that total to hours actually invoiced. If utilization slips, revenue may look full while owner pay weakens because unpaid labor is quietly rising.

Track two numbers each month: hours sold and hours delivered. Then check whether a 4-hour coaching job or a 19-hour team package is creating enough revenue after admin time. If the mix includes more complex team work, price and schedule it with extra buffer so the owner is not absorbing hidden labor for free.

2

Service Mix

Service Mix

When the mix shifts toward workplace mediation and team packages, revenue per closed case rises because Year 1 values are $2,000 and $4,500 and Year 5 values are $3,480 and $6,840. Coaching stays lower at $720 to $800, so fewer high-ticket matters can support owner pay.

The catch is delivery load. Higher-value work usually needs more prep, stakeholder calls, documentation, and follow-up, so realized margin can fall if pricing only covers live time. Track mix by service, case count, and nonbillable hours, or the profit on paper will be stronger than the cash in the bank.

Track Mix by Case Type

Model the mix across coaching, workplace mediation, and team packages, then test how each one changes monthly revenue and labor time. One lost team package cuts $4,500 in Year 1 or $6,840 in Year 5, so small mix shifts can move owner income fast.

Use a simple forecast: case count × engagement value, then add expected prep and follow-up hours so you see margin, not just sales. If demand emphasis moves from 40% to 60% mediation and from 20% to 40% team packages, staffing and scheduling need to keep up or delivery delays will hit cash flow.

3

Client Acquisition

Referral-Led Client Acquisition

Referrals and marketing drive how steady this consulting revenue is. The main sources are attorneys, human resources leaders, executives, employee relations teams, and professional networks. At a $50,000 Year 1 marketing budget and $1,000 CAC, that implies about 50 new clients; at $180,000 and $800 CAC, about 225. Lower CAC helps owner income because more revenue comes in for each dollar spent.

The catch is cash timing. Booked engagements do not pay payroll, so longer sales cycles can raise reserve needs and delay owner distributions. One slow quarter can look fine on bookings but still leave the bank account short.

Track close speed, not just leads

Measure each source by lead-to-close time, CAC, and booked-to-cash lag. If attorney referrals close faster than executive outreach, shift spend there first. The goal is not just more inquiries; it is more collected cash that can cover payroll and owner draws.

- Split results by referral source.

- Compare $1,000 and $800 CAC.

- Watch reserve needs before hiring.

- Test which source books fastest.

If sales cycles stretch, hold more cash and delay distributions until booked work turns into collected revenue. That discipline protects payroll and keeps growth from becoming a cash squeeze.

4

Delivery Leverage

Staff-Led Capacity

Delivery leverage means the founder is no longer the only delivery engine. As the team scales to two senior mediators and two junior mediators by Year 5, more billable work can get done without adding founder hours. That can lift revenue, but payroll rises to $110,000 per senior mediator and $80,000 per junior mediator.

The key math is simple: more staffed hours help owner income only if billings grow faster than labor cost. The model assumes direct consultant fees decline from 12% to 8%, so margin should improve if utilization stays tight. What this hides: low contractor use, quality misses, and extra owner oversight can erase the gain fast.

Track Capacity, Not Headcount

Measure billable hours per mediator, not just payroll count. Use founder pay of $150,000, operations manager pay of $75,000, marketing specialist pay of $65,000, and admin assistant pay of $45,000 to test whether support staff free up enough delivery time. If a new hire does not raise billed work or cut founder time, owner take-home drops.

Build a forecast for each role: senior mediator, junior mediator, and support staff. Then watch utilization, client trust, and handoff quality on every case. One line to remember: unused capacity is expensive capacity. If contractor utilization is inconsistent, payroll lands before cash does, and the owner may need to hold back draws.

5

Overhead And Reserves

Overhead and reserves

Owner pay comes after fixed bills and cash reserves. With $6,150 in monthly overhead, the business must clear rent, software, legal and accounting, insurance, web, utilities, and supplies before any draw. If profit is strong but cash is tight, take-home still stays low.

Here’s the quick math: $3,500 rent plus $800 software plus $700 legal and accounting leaves little room for delays. The $818,000 minimum cash need in Month 2 shows why reserves matter; they protect payroll and cover slow collections, not owner income.

Protect cash before owner pay

Track monthly overhead, reserve balance, and days sales outstanding, which is how long clients take to pay. If receivables stretch, cash gets trapped even when revenue looks fine. Keep a separate reserve account sized to payroll and fixed costs, then pay yourself only after that floor is covered.

Use a simple rule: fund the $6,150 monthly overhead first, then set aside cash for payroll timing and the $115,000 startup capex already committed. If collections slip, cut owner distributions before touching reserves. That keeps the firm stable and avoids paying yourself with borrowed cash.

6

Compare lean, base, and scaled owner-income scenarios

Owner income scenarios

Income moves fast here because owner pay depends on whether the practice stays founder-led or adds mediators and support staff. The model shifts from a lean launch to a multi-person practice, so profit and owner draw diverge quickly.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the conservative path, where founder pay and early EBITDA stay close to Year 1 results. | This is the modeled middle path, where Year 2 scale supports a larger team and stronger owner income. | This is the upside path, where Year 5 scale supports the highest modeled owner income. |

| Typical setup | Year 1 stays founder-led, with 8 mediation hours, 4 coaching hours, and 15 package hours, 86% gross margin, and breakeven by Month 6. | Year 2 adds a senior mediator and marketing specialist, lifts billable hours, and holds gross margin near 87% with EBITDA at $552,000. | Year 5 runs with a larger delivery team, 91% gross margin, and EBITDA of $3,932,000 as staffing expands to support more volume. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $127k - $150kLow Case | $552kBase Case | $3.9MHigh Case |

| Best fit | Use this to stress-test a slower launch and a mostly solo operating model. | Use this as the working plan for a growing boutique practice with managed complexity. | Use this to test a high-capacity practice with more management load and more moving parts. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Conflict Resolution Consulting Porter's Five Forces Analysis

- Conflict Resolution Consulting BCG Matrix

- Conflict Resolution Consulting Business Model Canvas

- 7 Core KPIs for Conflict Resolution Consulting Success

- Conflict Resolution Consulting Business Plan Template in Pre-Written Word

- 7 Data-Driven Strategies to Increase Conflict Resolution Consulting Profitability

- How Much Does It Cost To Run Conflict Resolution Consulting Monthly?

- Conflict Resolution Consulting Startup Costs: $115K CAPEX, $818K Cash

- Conflict Resolution Consulting Financial Model Template in Excel

- How To Start A Conflict Resolution Consulting Business In 4 To 10 Weeks

- How to Write a Conflict Resolution Consulting Business Plan

- Conflict Resolution Consulting Marketing Mix

- Conflict Resolution Consulting Marketing Plan

- Conflict Resolution Consulting Business Proposal

- Conflict Resolution Consulting PESTEL Analysis

- Conflict Resolution Consulting Pitch Deck Example Editable PPTX

- Conflict Resolution Consulting Business SWOT Analysis

- Conflict Resolution Consulting Value Proposition Canvas

Frequently Asked Questions

In this model, the owner has a planned $150,000 founder salary The business also produces $127,000 of Year 1 EBITDA and $3932 million by Year 5, but that is not the same as take-home pay Taxes, reserves, reinvestment, debt service, and distribution policy come after EBITDA