Owner income$145k

Owner income$145kHow Much Construction Cost Estimating Owners Make: $145k Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145k  Net margin32%–62%

Net margin32%–62% Revenue for target pay$235k-$460k

Revenue for target pay$235k-$460k Business difficultyHard

Business difficultyHard

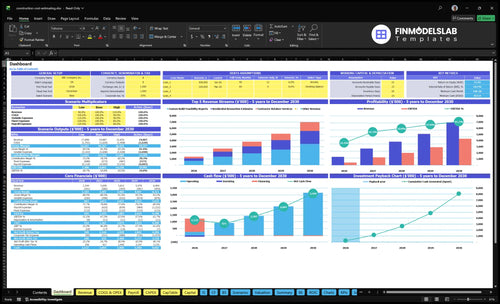

A construction cost estimating service owner can model $145k in annual owner salary, plus possible profit distributions if the business has cash left after reserves, taxes, debt, and reinvestment In the researched assumptions, revenue grows from $1344M in the first year to $6964M in year five EBITDA, which means earnings before interest, taxes, depreciation, and amortization, rises from $424k to $4298M, or about 32% to 62% of revenue If all EBITDA were distributable, pre-tax owner economic benefit would be $569k in the first year and $4443M in year five, but that is a planning case, not a guaranteed paycheck

Owner income$145kNet margin32%–62%Revenue for target pay$235k-$460kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full income forecast?

This dashboard shows revenue, margin, costs, reserves, and owner take-home assumptions in the Construction Cost Estimating Service Financial Model Template; open it.

Owner-income model highlights

- Month 5 breakeven

- $812k first-year cash need

- Revenue and EBITDA scenarios

Can a solo construction estimator make six figures?

Yes—a solo Construction Cost Estimating Service can make six figures in the planning case; the model already carries a $145,000 CEO and Principal Estimator salary, which is $45,000 over a $100,000 target. If you're mapping the setup, How To Launch Construction Cost Estimating Service Business? should be read with one hard caveat: capacity, not demand, becomes the bottleneck when each residential estimate takes 6 hours, each custom feasibility report takes 15 hours, and each contractor retainer takes 20 hours.

What supports six figures

- $145,000 planned owner salary

- 45% above a $100,000 income target

- Fee-for-service revenue model

- Residential and light commercial demand

What can break it

- 6 hours per residential estimate

- 15 hours per feasibility report

- 20 hours per contractor retainer

- Admin, revisions, sales calls, follow-up

What profit margin can a construction cost estimating service earn?

The Construction Cost Estimating Service can move from about 32% EBITDA margin in year one to about 62% by year five if variable delivery costs fall from 25% of revenue to about 17%. For the KPI view, see What Are The 5 KPI Metrics For Construction Cost Estimating Service? The gap comes from cheaper cost data, hosting, referral commissions, and payment fees, but rework, scope creep, underpriced complex jobs, and idle estimator payroll can wipe it out.

Margin gains

- 32% EBITDA in year one

- 62% EBITDA by year five

- Variable costs drop to about 17%

- Cost data and fees take less revenue

Margin risks

- Rework cuts profit fast

- Scope creep adds unpaid hours

- Complex jobs get underpriced

- Idle estimator payroll hurts margin

Should a construction estimating business owner hire estimators?

Yes—but only if the business can keep the extra bench busy. For Construction Cost Estimating Service, hiring can lift capacity from 1 senior and 1 junior to 5 senior and 3 junior roles, but payroll rises from $3675k in year one to $940k in year five, so lead flow, pricing, and review standards have to stay tight. Owner-led work keeps control; agency-style growth adds complexity.

When hiring helps

- Raises estimate volume

- Spreads senior review load

- Supports more active bids

- Helps if utilization stays high

What hiring adds

- Payroll grows to $940k

- Review time eats capacity

- Quality control gets harder

- Sales pressure rises fast

What drives owner take-home most?

1

$750-$2.7KAverage Fee

Moving more work into custom-build and retainer pricing lifts revenue per estimate and pushes owner take-home up fastest.

2

8.5-12hEstimate Volume

More billable hours per active customer, plus lower CAC, makes each marketing dollar buy more revenue.

3

6-20hLabor Efficiency

Simple renovation estimates take 6 hours, while retainer work takes 20, so faster handling protects margin.

4

45%-35%Project Mix

Shifting residential work down from 45% to 35% and replacing it with custom builds and retainers improves revenue density.

5

10%-30%Repeat Contractors

Growing contractor retainers from 10% to 30% smooths cash flow and keeps work coming back.

6

$9.6K/moOverhead Discipline

Keeping fixed overhead near $9.55K a month protects break-even, because cost creep hits take-home fast.

Construction Cost Estimating Service Core Six Income Drivers

Average Fee Per Estimate

Average Fee Per Estimate

Average fee per estimate is the first revenue lever here. If the mix is $750 for residential renovation estimates, $2,250 for custom build feasibility reports, and $2,200 for contractor retainer work, then pricing decides cash coming in before cost control does. By year five, those rise to $900, $2,625, and $2,700, so a higher fee can lift owner pay without adding more jobs.

Here’s the quick math: a 20% jump on renovation pricing, about 17% on feasibility work, and about 23% on retainer work only helps if scope stays tight. Use clear scope, complexity tiers, revision limits, and turnaround terms. If the fee is too low for the time spent, revenue looks busy but profit and draw stay thin.

Raise the fee without hurting fit

Track fee by project type, not just total sales. Separate renovation estimates, feasibility reports, and retainer work, then compare price to hours, revisions, and turnaround days. If the same scope keeps growing, the fee is too low. If higher pricing cuts close rate, the market or client fit may not support it yet.

One clean rule: price the work, not the hope. Document what is included, what costs extra, and how many revisions are covered. That protects revenue quality and keeps owner income tied to value delivered, not to unpaid scope creep.

- Track fee by project type

- Limit revisions in writing

- Set turnaround terms up front

- Test price against close rate

- Watch hours per estimate

1

Completed Estimate Volume

Completed Estimate Volume

Completed estimates turn pricing into revenue, but the ceiling is set by review time. A residential renovation estimate takes 6 hours, a custom feasibility report takes 15, and a contractor retainer takes 20, so more demand only helps if owner hours and QA can keep up. Missed deadlines hit repeat work, which cuts future revenue and owner pay.

Cap Volume by Review Time

Track completed jobs by type, average fee, and owner review hours. Here’s the quick math: revenue equals completed estimates × average fee, so volume matters only when turnaround stays tight and quality holds. Active customer work can run from 85 to 120 billable hours per month, so use that range to cap the forecast and protect cash flow.

- Count jobs by estimate type.

- Measure owner review hours.

- Watch missed-deadline repeat rates.

If the mix shifts toward 20-hour retainers, the same team completes fewer jobs, so forecast by capacity first and demand second.

2

Estimator Labor Efficiency

Estimator Labor Efficiency

Estimator labor efficiency is how many billed estimates the team can finish for each hour spent on scoping, takeoff, review, and rework. The model shows payroll at $3,675k and later $940k as the team scales, so wasted labor hits gross margin and owner pay fast. If scoping is loose, revenue can look strong while cash stays tight.

The owner still pays for labor even when it is not on payroll, because time spent fixing estimates cuts sales calls, client review, and delivery capacity. Track hours estimated vs. actual, rework rate, subcontractor cost per bid, and review time. Poor scoping turns high revenue into low cash, and that lowers the draw the owner can safely take.

Control the Hours Behind Each Bid

Use a simple job sheet on every estimate: scope, revision limit, turnaround time, and reviewer. Compare planned hours with actual hours on each job, and tag any estimate that needs repeat work. That tells you where margin is leaking before it shows up in owner income.

- Log hours by task.

- Split rework from first-pass work.

- Track subcontractor cost per bid.

- Measure review time each week.

If actual hours keep running above estimate, raise price, narrow scope, or cut low-value work before payroll and overhead outrun cash.

3

Project Complexity Mix

Project Complexity Mix

Your income changes when the mix shifts toward simpler or more complex jobs. In year one, residential renovation estimates are 45% of listed mix, then fall to 35% by year five. Custom feasibility reports rise from 25% to 35%, and contractor retainer services rise from 10% to 30%. That mix lifts fee per job, but it also changes delivery time, rework risk, and owner cash flow.

Here’s the quick math: 6 hours for a renovation estimate, 15 for a feasibility report, and 20 for a retainer job means complex work can crowd out volume even when pricing is better. Simple jobs close faster; complex jobs carry higher fees. Retainers smooth monthly revenue, but only if the fee covers the extra review time and revision load.

Price by complexity, not by habit

Track mix by project type, hours, and gross margin per job. A service that looks busy can still pay poorly if a 35% share of feasibility reports absorbs too much review time or if renovation work stays at 45% without enough fee lift. The key inputs are project count, fee, delivery hours, revision limits, and close time.

Set a floor price for each scope tier and test whether the fee covers labor plus rework. If retainers rise to 30%, watch whether they improve cash flow or just add low-margin support work. No niche is best unless the price covers the effort to deliver it. Measure owner time per job, then cut work that ties up capacity without lifting take-home income.

4

Repeat Contractor Relationships

Repeat Contractor Work

Repeat clients cut sales drag and smooth monthly workload. In this model, contractor retainer services grow from 10% of listed mix to 30%, while CAC, or customer acquisition cost, falls from $225 to $175 even as marketing spend rises from $45k to $110k. That only helps if retained work still covers delivery time and keeps gross profit strong.

Here’s the quick math: more repeat orders mean fewer one-off quotes, less proposal churn, and steadier cash flow. Track lead source, close rate, repeat order rate, and revenue per client. If repeat demand slips, higher marketing spend can raise volume but still lower owner take-home pay.

Track Retention, Not Just Leads

Measure each contractor by source, first-job close rate, and how fast they reorder. Then compare CAC to repeat revenue per client. Lower CAC means little if retained work is thin or priced too low. One clean rule: marketing should buy profitable retained work, not just more estimates.

Build the forecast around repeat mix, not wishful demand. If retainer work stays near 30% of listed mix, monthly workload is steadier and sales time falls. If it stays near 10%, expect more hunt time, more volatility, and less room for owner pay after marketing and delivery costs.

- Track lead source by client type.

- Track repeat order rate monthly.

- Track revenue per contractor client.

- Compare CAC to retained gross profit.

5

Fixed Overhead Discipline

Fixed Overhead Discipline

Fixed overhead sets the break-even floor, so it directly limits owner pay. Here, fixed expenses total $955k per month, including insurance, office, accounting, IT support, software licenses, and telecom. Annual fixed overhead is $1,146k before payroll and marketing, and software licenses alone run $22k per month.

The key is to keep overhead out of direct delivery costs. If you mix them, gross margin looks better than it is, and pricing decisions get sloppy. Remote work can lower office cost, but only if turnaround, accuracy, and client service hold up. If service quality slips, repeat contractor work and owner income fall fast.

Control the Burn Rate

Track overhead by line item each month: insurance, office, accounting, IT support, software, telecom, and payroll. The simple test is whether monthly contribution after direct delivery costs can clear $955k before owner draw. If not, pricing, volume, or staffing is off.

- Separate fixed and direct costs.

- Watch software at $22k/month.

- Test remote work on quality.

- Protect turnaround and revision speed.

Build a forecast that flags overhead creep early. One-liner: if fixed cost rises faster than estimate volume, owner income gets squeezed even when revenue grows. Use monthly variance reviews, and stop any spend that does not support more completed estimates or better client retention.

6

Compare low, base, and high owner income planning cases

Owner income scenarios

Owner income rises as utilization, staffing, and margin improve. Better cash control can keep more profit available, but it does not guarantee distributions.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower-earnings path based on Year 1 operating results. | This is the modeled mid-case built around Year 3 results. | This is the stronger-earnings path based on Year 5 scale. |

| Typical setup | Year 1 reaches $1.344M revenue, $424k EBITDA, a 32% margin, and a $145k owner salary, for about $569k pre-tax economic benefit before reserves. | Year 3 reaches $3.812M revenue, $1.983M EBITDA, a 52% margin, and about $2.128M pre-tax economic benefit before reserves. | Year 5 reaches $6.964M revenue, $4.298M EBITDA, a 62% margin, and about $4.443M pre-tax economic benefit before reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $569kLow Case | $2.128MBase Case | $4.443MHigh Case |

| Best fit | Use this to stress-test a slower launch, tighter hiring, and conservative cash use. | Use this as the main planning case for a steady Year 3 operating run rate. | Use this to test upside with strong utilization, disciplined hiring, and tight cash control. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Construction Cost Estimating Service Porter's Five Forces Analysis

- Construction Cost Estimating Service BCG Matrix

- Construction Cost Estimating Service Business Model Canvas

- What Are The 5 KPI Metrics For Construction Cost Estimating Service?

- Construction Cost Estimating Business Plan Template in Pre-Written Word

- How Increase Profitability Construction Cost Estimating Service?

- What Are Operating Costs For Construction Cost Estimating Service?

- Construction Cost Estimating Service Startup Costs: $107K–$812K

- Construction Cost Estimating Service Financial Model Template in Excel

- How To Start A Construction Cost Estimating Service In 4-8 Weeks

- How To Write A Business Plan For Construction Cost Estimating Service?

- Construction Cost Estimating Service Marketing Mix

- Construction Cost Estimating Service Marketing Plan

- Construction Cost Estimating Service Business Proposal

- Construction Cost Estimating Service PESTEL Analysis

- Construction Cost Estimating Service Pitch Deck Example Editable PPTX

- Construction Cost Estimating Service Business SWOT Analysis

- Construction Cost Estimating Service Value Proposition Canvas

Frequently Asked Questions

In the researched model, the owner role is paid $145k per year Business profit is separate: EBITDA is $424k in the first year and $4298M in year five If profit is distributed, owner economic benefit can be higher, but taxes, reserves, debt, and reinvestment can reduce actual cash taken home