Owner income$135k

Owner income$135kHow Much Corporate Retreat Planning Owners Make: $135k Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$135k  Net margin7.3%

Net margin7.3% Revenue for target pay$927k

Revenue for target pay$927k Business difficultyHard

Business difficultyHard

You’re pricing owner pay before the sales pipeline is proven, so the clean answer starts with revenue, margin, overhead, and cash This model shows $927k Year 1 revenue, $68k Year 1 EBITDA, a $135k CEO salary, 7 months to breakeven, and 16 months to payback These are planning assumptions, not tax advice, salary guarantees, or distribution promises

Owner income$135kNet margin7.3%Revenue for target pay$927kBusiness difficultyHardWant to test your retreat planning owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on demand, margin, payroll, taxes, debt, and reinvestment choices.

Want to check owner income in the Corporate Retreat Planning Service model?

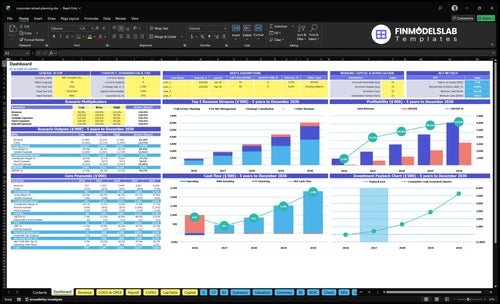

This screenshot shows how bookings turn into owner income, with revenue, EBITDA, breakeven month, payback month, cash need, and staffing assumptions in the Corporate Retreat Planning Service Financial Model Template. Open the model to see Year 1 through Year 5, from $927k revenue to $6.058M and $68k EBITDA to $3.188M.

Owner-income model highlights

- Bookings to owner income

- Revenue grows $927k to $6.058M

- EBITDA grows $68k to $3.188M

How much should a corporate retreat planning business owner pay themselves?

A Corporate Retreat Planning Service owner should pay themselves the modeled $135,000 per year CEO and Lead Strategist salary, then keep owner draws separate; see How Increase Corporate Retreat Planning Service Profits? for the profit levers behind that number. Year 1 EBITDA is only $68,000 after payroll, and the model shows a $766,000 minimum cash need in Month 6, so early distributions should stay conservative.

Owner Pay

- Set salary at $135,000 per year

- Treat salary as labor pay

- Separate draws from payroll

- Do not drain operating cash

Cash Guardrails

- Protect $766,000 Month 6 cash need

- Remember EBITDA is $68,000

- Hold distributions until cash stabilizes

- If selling retreats, salary is earned

Can a corporate retreat planning business scale beyond the owner?

Yes — a Corporate Retreat Planning Service can scale beyond the owner, but the owner’s income changes as they move from planner to sales lead or agency operator. Here’s the quick math: staffing grows from 1 senior planner, 1 sales role, 1 logistics coordinator, and 05 admin FTE in Year 1 to 4 planners, 3 sales FTE, 5 logistics FTE, and 1 admin FTE in Year 5, which protects delivery quality but pushes payroll from $379k to $1048M.

How the owner scales

- Move from planner to sales lead.

- Shift into agency operator work.

- Grow headcount with demand.

- Keep service quality consistent.

Main scale risks

- Seasonality can swing bookings.

- Client concentration raises exposure.

- Capacity bottlenecks slow delivery.

- Quality control gets harder fast.

What profit margin can a corporate retreat planning business make?

Corporate Retreat Planning Service can be a very high-margin business if you keep pass-through venue and hotel budgets out of profit. Here’s the quick math in the How Much To Start Corporate Retreat Planning Service Business? view: gross margin starts near 85% after 12% contracted facilitator fees and 3% software COGS, and Year 1 EBITDA margin is about 73% ($68k on $927k).

Year 5 EBITDA margin can reach about 526% ($3.188M on $6.058M) if operations stay lean. Net margin still depends on payroll, marketing, CAC, travel, referrals, insurance, and overhead.

Year 1 margin drivers

- 73% EBITDA margin

- $68k EBITDA on $927k

- 85% gross margin start

- 12% facilitator fees, 3% software COGS

Year 5 margin view

- 526% EBITDA margin

- $3.188M EBITDA on $6.058M

- Net margin varies by overhead

- Do not count pass-through budgets

Want the six drivers of retreat planning profit?

1

$927K-$6.1MRetreat Volume

More booked retreats drive the biggest take-home swing, since revenue scales from Year 1 to Year 5 across the model.

2

$7K-$11KNet Revenue

A higher average retreat ticket lifts each sale, so the same team can earn more without needing as many bookings.

3

85%Gross Margin

Year 1 gross margin starts at 85%, and keeping service costs tight leaves more cash after facilitator fees and software.

4

1-4 FTEPlanner Labor

Planner headcount is a hard capacity limit, and the senior planner grows from 1.0 to 4.0 FTE, which can squeeze profit if work stays manual.

5

$2.5K-$1.8KCAC Efficiency

CAC falls from $2.5K to $1.8K, so each new client costs less and marketing dollars go farther.

6

$112K/moOverhead Control

Fixed overhead runs at about $112K per month, and the $135K owner salary means lean cost control matters early.

Corporate Retreat Planning Service Core Six Income Drivers

Retreats booked per month

Bookings per month

Retreats booked per month drives income only when the team can deliver each event without misses. More qualified bookings raise revenue, but the real limit is capacity: Year 1 assumes 25 average billable hours per month, rising to 30 in Year 5. If bookings pile up in peak retreat months, labor and travel costs can outrun the extra revenue.

Here’s the quick math: booked retreats must flow into active customers, then into billed hours, then into margin. With $25k Year 1 CAC, weak close rates can eat cash fast. The owner’s take-home income improves only after capacity, payroll, and trip costs are covered. More bookings are good; uncontrolled bookings are not.

Track bookings against capacity

Measure booked retreats against active customers and available billable hours, not just lead count. Watch close rate, month-to-month seasonality, and the share of work landing in peak months. If 25 hours becomes 30 hours without service failures, owner pay can rise; if delivery slips, margin drops first.

Track CAC beside net service revenue, then set a hard booking cap before travel and labor overload the team. Use a simple test: if each new retreat does not cover its share of planner time, travel, and overhead, it is not adding cash. The goal is fewer bad-fit bookings and more profitable ones.

1

Average net revenue per retreat

Average Net Revenue per Retreat

Average net revenue per retreat rises when the team sells full planning, on-site management, and strategic consultation, not just event setup. In the model, service value is about $70k per active customer in Year 1 and $112k in Year 5, using higher rates and higher attach rates. That lifts owner income because more of each retreat becomes fee revenue instead of pass-through spend.

Keep managed event budgets separate from company revenue. Venue, hotel, food, and transport cash should not be counted as profit, or the margin will look better than it is. The real driver is pricing discipline: if scope expands without a rate lift, the owner needs more clients to grow pay. One well-priced retreat can do more than several low-scope jobs.

Raise Fee Revenue per Retreat

Track service revenue per active customer, not total event spend. Break each retreat into planning hours, on-site days, and consultation time, then price each piece clearly. The target should move from $70k in Year 1 toward $112k in Year 5 as attach rates rise. If scope creeps without a rate lift, owner income gets diluted fast.

- Billable hours per retreat

- Hourly rate by service type

- Attach rate for add-on work

- Pass-through budget kept separate

Use a simple rule: separate managed budgets from service fees in every proposal and invoice. That keeps gross margin clean and shows whether owner pay is rising because the work is better priced, not because the retreat got bigger. If planners add more on-site management, raise the fee or cap the scope.

2

Gross margin and vendor economics

Gross Margin Control

For a corporate retreat planner, this driver is the gap between client billings and vendor-heavy delivery costs. Year 1 gross margin is about 85% after 12% contracted facilitator fees and 3% software COGS. If a project runs $100,000, that leaves about $85,000 before travel and commission leakage, so every vendor choice flows straight to owner income.

Travel and site inspections add 6%, and referral and partner commissions add 4%. Venue, hotel, food, and transportation payments are pass-through costs, not profit. If markup rules are loose or disclosures are thin, EBITDA, or operating profit before financing and taxes, gets overstated and the owner can end up paying themselves on money that was never real margin.

Track Vendor Take Rate

Measure gross margin by project, not just by month. Track the fee, facilitator cost, software COGS, travel, site visits, and commissions on every retreat, then compare to the 85% target and the extra 10% tied to travel and referrals. One clean rule helps: separate pass-through spend from service revenue in the ledger.

- Client fee per retreat

- Facilitator fee percentage

- Software COGS percentage

- Travel and site inspection spend

- Referral and partner commissions

Test vendor markup and commission policies before scaling them. If markup lifts revenue, disclose it clearly in the client scope and invoice, and keep venue, hotel, food, and transportation reimbursements out of owner profit math. That protects cash flow, keeps margin real, and leaves more room for owner pay when volume rises.

3

Planner labor and delivery model

Planner Staffing and Delivery Capacity

Planner labor is the engine that protects service quality, but it also eats owner cash fast. Year 1 payroll is $379k, including $135k CEO salary, $85k senior planner, $75k sales role, $60k logistics coordinator, and $24k admin coverage. That spend can support more billable work, but if bookings lag, the owner’s take-home gets squeezed.

By Year 5, payroll reaches $1,048M as planners, sales, and logistics scale. Contractors can flex for peak retreat months, which helps protect delivery quality, but it adds labor risk and makes cash flow less stable. The key tradeoff is simple: more staffed capacity can lift revenue, but only if billable hours and close rates keep pace.

Track Capacity Before You Add Headcount

Measure staffed hours against booked retreats, average billable hours, and peak-month load. For this model, the important inputs are headcount mix, contractor hours, sales conversion, and on-site delivery time per event. One clean rule: do not add payroll unless projected billable hours can cover it with room for travel and admin time.

Use a simple check: if payroll rises faster than active clients, owner profit gets thinner. Track labor as a share of revenue, then test whether contractors can cover spikes before hiring full-time staff. That keeps delivery smooth and helps protect owner pay when retreat volume is uneven.

- Watch billable hours per planner.

- Separate contractor and employee costs.

- Stress-test peak retreat months.

- Link hires to booked demand.

4

Client acquisition efficiency

Client acquisition efficiency

For a corporate retreat planner, client acquisition efficiency is the gap between what you spend to win a client and the net planning revenue that client brings in. With marketing spend rising from $55k in Year 1 to $150k by Year 5, the key check is CAC falling from $25k to

Here’s the quick math: a lower CAC means more gross profit left after sales and marketing. But paid marketing only works if close rates and repeat bookings hold. Referrals, partnerships, repeat HR clients, and outbound sales all need to be measured against net planning revenue, not the total event budget the client pays vendors. One clean rule: don’t count pass-through spend as margin.

Track CAC against net planning revenue

Measure CAC by channel: paid, referral, partnership, repeat client, and outbound. Then compare each one to net planning revenue per retreat, not the full event budget. If CAC drops from $25k to $18k, that’s $7k more profit per win before delivery costs. If repeat HR clients lift average client value at the same time, owner draw improves faster.

Watch close rate, repeat rate, and payback period. If close rates slip or repeat bookings slow, higher marketing spend can burn cash fast even when lead flow looks strong. Keep a simple scorecard: spend, qualified leads, wins, CAC, and net revenue per client. The best channels are the ones that keep CAC below the profit you can keep after labor, travel, and vendor costs.

5

Fixed overhead and reserves

Fixed Overhead and Reserves

$112k per month in fixed overhead sits in front of payroll, so this business has to clear a big cash hurdle before the owner can draw much income. That overhead includes rent, insurance, CRM, legal, accounting, content production, telecom, and internet. On an annual basis, that is $1.344M before payroll, so weak booking months hit owner pay fast.

Reserves are not spare profit. The model needs $766k of minimum cash in Month 6, and early capex adds $117k. Here’s the quick math: if cash collections slip, the owner’s income gets squeezed even when projects look booked on paper. Cash runway matters more than revenue headlines.

Track Cash Burn, Not Just Bookings

Measure overhead by month and by category, then tie it to active client revenue. The key question is whether gross profit from retreats can cover $112k of fixed costs plus payroll before the reserve target is touched. If not, owner pay should stay limited until cash rebuilds.

- Track monthly overhead by line item.

- Hold reserve cash for Month 6.

- Time capex before peak delivery.

- Separate operating cash from profit.

Use a simple rule: reserves first, owner draws second. That protects delivery quality, keeps vendors paid, and prevents a strong sales month from hiding a weak cash position.

6

Compare low, base, and high corporate retreat planning income scenarios

Owner income scenarios

Owner income depends on booking volume, service mix, and staffing. Revenue can rise fast, but faster hiring, travel, and commissions can still cut take-home.

| Scenario | Low CaseLean take-home | Base CaseModeled take-home | High CaseScale upside |

|---|---|---|---|

| Launch model | This is the lower earnings path, with lean volume and little room for profit draws. | This is the modeled path, with income tracking the researched operating case. | This is the stronger earnings path, where scale lifts revenue but also raises the need for reserves. |

| Typical setup | A small mix of retreats, lower service depth, higher CAC, and limited distribution beyond the owner salary keep cash tight. | The plan reaches $927k Year 1 revenue and $68k EBITDA, with a $135k CEO salary, 7-month breakeven, and 16-month payback. | By Year 5, revenue reaches $6.058M and EBITDA $3.188M, but hiring, travel, and reserve needs can trim take-home if bookings do not keep pace. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlyThin margin | $135kModeled case | Salary plus profit upsideHigher upside |

| Best fit | Use this to test a slow start, weak referrals, and a long ramp to steady bookings. | Use this as the core planning case for an owner-operator who is building a repeatable sales and delivery rhythm. | Use this to test what happens when demand is strong and the owner expands delivery capacity without losing margin. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Corporate Retreat Planning Service Porter's Five Forces Analysis

- Corporate Retreat Planning Service BCG Matrix

- Corporate Retreat Planning Service Business Model Canvas

- What Are The 5 KPIs For Corporate Retreat Planning Service Business?

- Corporate Retreat Planning Service Business Plan Template in Pre-Written Word

- How Increase Corporate Retreat Planning Service Profits?

- What Are Operating Costs For Corporate Retreat Planning Service?

- Corporate Retreat Planning Startup Costs: $766K Cash Need

- Corporate Retreat Financial Model Template in Excel

- How To Start A Corporate Retreat Planning Service In 6–12 Weeks

- How To Write A Business Plan For Corporate Retreat Planning Service?

- Corporate Retreat Planning Service Marketing Mix

- Corporate Retreat Planning Service Marketing Plan

- Corporate Retreat Planning Service Business Proposal

- Corporate Retreat Planning Service PESTEL Analysis

- Corporate Retreat Planning Pitch Deck Example Editable PPTX

- Corporate Retreat Planning Service Business SWOT Analysis

- Corporate Retreat Planning Service Value Proposition Canvas

Frequently Asked Questions

The researched model includes a $135k CEO salary, $927k Year 1 revenue, and $68k Year 1 EBITDA By Year 5, it shows $6058M revenue and $3188M EBITDA That EBITDA is a profit pool before taxes and other items, not guaranteed owner take-home