Owner income$175k+

Owner income$175k+How Much Can A Cost Segregation Study Service Owner Make? $175k+

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$175k+  Net margin-1% to 39%

Net margin-1% to 39% Revenue for target pay$1.04M

Revenue for target pay$1.04M Business difficultyHard

Business difficultyHard

In the researched model, the owner role carries a $175,000 Principal Tax Strategist salary, but distributions depend on profit, cash, taxes, debt, and reserves Revenue grows from $1044 million in Year 1 to $5386 million in Year 5, while EBITDA moves from -$12,000 to $2121 million The business breaks even in Month 7 and pays back in 20 months Treat owner take-home as salary plus only the profit the firm can safely distribute after keeping enough cash in the business

Owner income$175k+Net margin-1% to 39%Revenue for target pay$1.04MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the owner-income math behind the model?

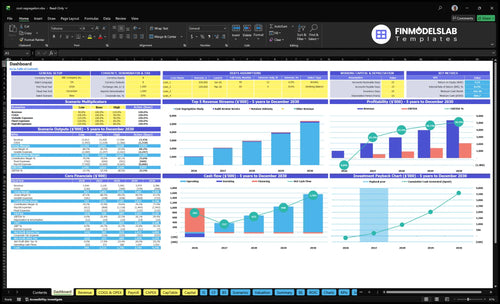

This screenshot shows dashboard outputs, revenue, margin, costs, reserves, and owner take-home assumptions as a planning bridge; open the Cost Segregation Study Service Financial Model Template.

Owner-income model highlights

- Owner pay; cash need

- Revenue: $1,044M to $5,386M

- EBITDA: -$12k to $2,121M

- Month 7 break-even, 20-month payback

- Low/base/high cases tested

How much can a cost segregation consultant make?

A Cost Segregation Study Service consultant’s income depends on capacity, role, and team model; What Are The 5 KPI Metrics For Cost Segregation Study Service Business? helps separate billings from owner cash. In the provided small-team model, payroll is $530k, owner salary is $175k, and EBITDA is -$12k, so revenue doesn’t equal spendable income.

Income Drivers

- Separate billings from owner take-home

- Solo income is capped by study capacity

- Review quality limits safe volume

- Owner role changes cash outcome

Scale Case

- Year 1 payroll: $530k

- Owner salary: $175k

- Year 1 EBITDA: -$12k

- Year 5 model: $5.386M revenue, $2.121M EBITDA

What is the cost segregation consulting profit margin?

If you're pricing a Cost Segregation Study Service, use EBITDA margin as the planning proxy: the model is -11% in Year 1, then 254% in Year 2, 322% in Year 3, 361% in Year 4, and 394% in Year 5. For the cost lines behind that, see What Are Operating Costs For Cost Segregation Study Service? Audit support and quality review cut into take-home, but they protect delivery quality.

Margin drivers

- Site travel drops from 85% to 65%.

- Database subscriptions fall from 40% to 20%.

- Referral commissions stay at 100%.

- Tax research moves from 30% to 10%.

Scale effects

- Fixed overhead stays at $132k a year.

- Payroll rises from $530k to $1495M.

- Audit support lowers take-home margin.

- Quality review protects delivery quality.

How many cost segregation studies per month are needed?

If your studies are being sold and collected at the modeled fee, the Cost Segregation Study Service needs about 9 completed and collected studies per month in Year 1, rising to 18 in Year 2, 24 in Year 3, 32 in Year 4, and 40 in Year 5. Here’s the quick math: the average fee is modeled at $7,875 in Year 1 from 35 hours × $225, and $8,370 in Year 5 from 31 hours × $270. Collection rate should be editable, because uncollected work cuts the monthly study count fast.

Year 1 volume

- 9 studies per month

- $7,875 average fee

- 35 hours per study

- $225 hourly value

Year 5 volume

- 40 studies per month

- $8,370 average fee

- 31 hours per study

- $270 hourly value

Pricing drivers

- Larger properties can support higher fees

- Engineering review takes more time

- Site work adds labor hours

- Audit support must be ready

Volume drivers

- Revenue mix sets monthly count

- Completed studies must be collected

- Editable collection rate matters

- Target owner pay ties to cash received

Want the six drivers that move owner take-home?

1

9-40/moStudy Volume

More completed studies drives most revenue, so moving from 9 to 40 a month changes owner income fast.

2

$7.9K-$8.4KStudy Fee

A small lift in modeled fee per study compounds across every close and lifts margin.

3

100%Referral Mix

If the pipeline leans on referral partners, commission drag cuts take-home on every win.

4

$530K-$1.50MLabor Scale

Payroll growth from about $530K to $1.50M means utilization has to stay tight or EBITDA slips.

5

12 hrsReview Load

Audit review work adds 12 hours, so heavier quality checks can choke throughput and raise labor cost.

6

$667KCash Floor

A $132K fixed overhead base and a $667K minimum cash need limit owner draws until collections stabilize.

Cost Segregation Study Service Core Six Income Drivers

Completed study volume

Completed study volume

Completed study volume is the main revenue engine here. At 9 studies per month in Year 1 and 40 per month in Year 5, annual collected revenue scales fast: about $850,500 in Year 1 (108 × $7,875) and $4,017,600 in Year 5 (480 × $8,370), assuming the studies are completed and billed as planned.

The catch is capacity. Volume only improves owner income if senior engineers, junior estimators, coordinators, and review time can keep turnaround clean. If sales outpace delivery, you get rework, slower cash collection, and weaker profit. More volume helps only when quality and timing hold.

Manage throughput, not just sales

Track completed studies per month, average turnaround time, and review hours per file. Those are the inputs that show whether volume is real or just backlog. If the team is near capacity, add staff or cap new work before report quality slips, because low-quality work can delay payment and hurt owner draw.

Use a simple rule: only sell what the team can finish cleanly. Measure studies completed ÷ studies sold, then compare that to labor load and review time. If volume rises but rework also rises, margin falls and cash gets tighter even when top-line revenue looks stronger.

- Track completed studies monthly.

- Watch turnaround time closely.

- Limit work at capacity.

- Protect review time and quality.

1

Average study fee

Average study fee

The fee per study is the main revenue lever because every closed project is billed once. The model shows $7,875 in Year 1 from 35 hours × $225 and $8,370 in Year 5 from 31 hours × $270. That is only a 6.3% fee lift, so profit improves most when price rises faster than production time.

Inputs are property size, documentation needs, site review time, and report complexity. The owner’s take-home income rises when the fee covers analyst hours, review time, and overhead on each study. If a large or messy property gets priced like a simple one, revenue looks fine but cash flow and profit fall after rework and extra review.

Price by complexity, not guesswork

Track fee per study, hours per study, and fee per hour on every job. If 31-hour projects still command $8,370, the implied rate is $270/hour; if hours drift back toward 35 without a higher fee, margin slips. Use clear pricing tiers for property size, missing records, and site visits.

Test add-ons for messy files and complex assets, then review them monthly against realized hours. The goal is simple: raise price faster than production time. That keeps more gross profit in the business and leaves more room for owner pay after labor and fixed costs.

2

Referral partners and lead generation

Referral Lead Cost

This driver is about what it costs to turn a referral or click into a paying study. The model shows marketing spend rising from $45k in Year 1 to $140k in Year 5, while CAC drops from $1,800 to $1,600. If acquisition cost rises faster than fee growth, owner pay gets squeezed even when bookings increase.

The big risk is partner economics: referral partner commissions are modeled at 100% of revenue each year. That means cheap leads are not enough if they do not close and collect. For this service, lead quality matters more than lead count, because weak-fit property owners can burn cash and still leave little profit for the owner.

Track CPA and Close Rate

Measure lead source, CPA (cost per acquisition), close rate, collect rate, and fee by partner. Use marketing spend, referral commissions, study fee, and source mix to estimate income. Real estate investor referrals and other high-fit partners can lift conversion, but only if the deal closes and the invoice gets paid.

- Marketing spend by source

- Referral commission per deal

- Cost per acquired client

- Close rate by partner

- Collect rate after invoicing

Set a hard floor for each channel. If a source brings low-cost leads but they do not close, the cash return is weak and owner distributions stay smaller. Keep the channels that produce paid studies at a margin that can cover payroll, overhead, and the owner’s draw.

3

Production labor efficiency

Production labor efficiency

This driver is about how many billable hours it takes to finish one study, and how much of payroll turns into client work. When labor is tight, fewer hours per study means more capacity from the same team, faster cash collection, and better EBITDA (earnings before interest, taxes, depreciation, and amortization) because payroll is the biggest scaling cost.

The model shows payroll rising from $530k in Year 1 to $1.495M in Year 5, while study effort improves from 35 to 31 hours per study and hourly pricing moves from $225 to $270. The risk is cutting review too far and weakening audit support, which can create rework and hurt the owner’s take-home pay.

Track hours, not just output

Measure utilization (paid time spent on billable work), hours per study, and rework by analyst, engineer, and reviewer. The goal is simple: keep turnaround tight without weakening documentation. If a faster process creates even a small audit gap, you can lose time, margin, and collections later.

Use a clean review gate, then test where hours can drop safely. Track these inputs:

- Hours per study

- Rework rate by reviewer

- Utilization by role

- Audit-support touchpoints

4

Fixed overhead and professional costs

Fixed overhead and professional costs

The business starts each month with $11k of fixed costs before any study revenue comes in, or $132k a year. That bucket includes the lease, liability insurance, cloud CRM and ERP maintenance, legal and compliance, utilities, and admin supplies, so owner pay only starts after collected fees clear that base.

The cash drag is bigger when you include $1.435M of capex for laptops, measurement gear, furniture, software build, infrastructure, web work, and security. If volume is still thin, that spend ties up cash early and leaves less room for distributions, even when the work pipeline looks active.

Keep fixed spend tied to booked work

Track monthly fixed burn, cash collected, and the number of studies needed to cover $11k. Split costs into fixed and variable lines, then watch lease, software, legal, and admin spend separately so you can see what really moves owner income.

Only lock in new overhead when it clearly shortens turnaround, improves audit support, or lifts close rates. If a cost does not help more studies close or collect faster, it mostly delays profit draw and makes the business carry enterprise cost before recurring volume supports it.

- Track fixed burn every month.

- Separate fixed from variable spend.

- Tie new costs to booked studies.

5

Reserves and owner payout policy

Cash Reserves and Owner Pay

Pre-tax profit is not owner pay. This model needs a $667k minimum cash balance in Month 6, breaks even in Month 7, and reaches payback in 20 months, so the owner can plan around a $175k salary but should only take extra distributions when cash still covers payroll timing, marketing tests, audit support, tax payments, and growth hires.

Inputs are ending cash, monthly payroll, tax accruals, marketing spend, and hiring plans. If reserves stay tight, near-term take-home drops; if they stay funded, the firm can keep scaling without forcing debt or a rushed owner draw. Cash discipline is the income driver here.

Set the reserve floor first

Track cash against the $667k floor every month and treat $175k as salary, not profit share. Hold distributions until the reserve covers at least one payroll cycle, planned marketing tests, tax payments, and the next hire. That keeps owner pay lower now, but it protects the cash needed to scale.

- Watch ending cash monthly.

- Tag payroll and tax dates.

- Approve draws after reserve.

- Stress test Month 6 cash.

6

Low, base, and high owner income scenario objective

Owner income scenarios

Owner income changes fast because study volume, billing rate, and payroll move together. Year 1 is near break-even, while Year 3 and Year 5 can support a bigger draw.

| Scenario | Low CaseDownside case | Base CasePlanning case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lower owner-income path with Year 1 volume and near-break-even economics. | This is the modeled middle path with Year 3 volume, positive EBITDA, and a scaled team. | This is the stronger owner-income path with Year 5 volume, high EBITDA, and a larger delivery bench. |

| Typical setup | About 9 studies a month, $1.044M revenue, and -$12k EBITDA keep cash tight while payroll and marketing stay heavy. | About 24 studies a month, $2.945M revenue, and $947k EBITDA support salary plus a real profit draw. | About 40 studies a month, $5.386M revenue, and $2.121M EBITDA support salary plus a larger distribution pool. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $175k salary onlySalary only | $175k plus profit drawProfit draw | $175k plus larger drawUpside draw |

| Best fit | Use this to stress-test cash discipline and what happens if growth is slow. | Use this as the main operating plan if sales and delivery stay on track. | Use this to test upside if hiring, referrals, and throughput all land well. |

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; actual owner take-home depends on salary, reserves, taxes, and debt.

Related Products

- Cost Segregation Study Service Porter's Five Forces Analysis

- Cost Segregation Study Service BCG Matrix

- Cost Segregation Study Service Business Model Canvas

- What Are The 5 KPI Metrics For Cost Segregation Study Service Business?

- Cost Segregation Study Service Business Plan Template in Pre-Written Word

- How Increase Profits For Cost Segregation Study Service?

- What Are Operating Costs For Cost Segregation Study Service?

- Cost Segregation Study Service Startup Costs: Plan for $8105k

- Cost Segregation Study Financial Model Template in Excel

- How to Start a Cost Segregation Study Service in 6 to 12 Weeks

- How To Start Cost Segregation Study Service?

- Cost Segregation Study Service Marketing Mix

- Cost Segregation Study Service Marketing Plan

- Cost Segregation Study Service Business Proposal

- Cost Segregation Study Service PESTEL Analysis

- Cost Segregation Study Service Pitch Deck Example Editable PPTX

- Cost Segregation Study Service Business SWOT Analysis

- Cost Segregation Study Service Value Proposition Canvas

Frequently Asked Questions

The researched model includes a $175,000 owner-level Principal Tax Strategist salary EBITDA is -$12,000 in Year 1, then rises to $534,000 in Year 2 and $2121 million in Year 5 Real take-home depends on reserves, taxes, debt, and whether profit is distributed or reinvested