Owner income$0

Owner income$0How Much Does A Country Club Owner Make With -$68M Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0  Net marginBelow 0%

Net marginBelow 0% Revenue for target pay$0

Revenue for target pay$0 Business difficultyHard

Business difficultyHard

Key Takeaways

- Recurring dues must cover fixed costs and payroll.

- Retention and waitlists protect pricing and cash flow.

- Ancillary spend only helps when it turns profitable.

- Labor and reserves decide what owners actually keep.

Owner income$0Net marginBelow 0%Revenue for target pay$0Business difficultyHardWant to test your own country club owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. The modeled club reaches breakeven in Month 28, but EBITDA stays negative through Year 5.

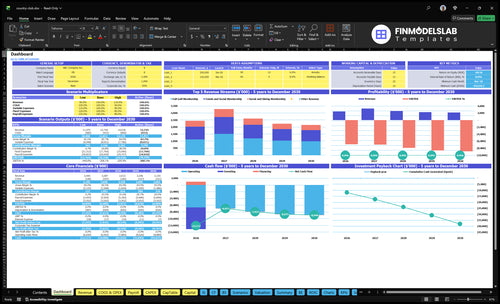

Can you check owner income in the Country Club model?

If you're checking whether the Country Club Financial Model Template supports the owner, open it to review dashboard, assumptions, revenue, payroll, fixed costs, capex, EBITDA, cash runway, breakeven, and owner take-home. Test dues from $400 to $1,700, membership mix from 250% to 400%, CAC from $4,000 to $5,500, marketing from $20M to $14M, and capex at $645M; the base case shows Month 28 breakeven, Month 60 cash of -$446M, and $0 owner income.

Owner-income model highlights

- $0 owner take-home

- EBITDA losses and runway

- Test dues and CAC

What country club operating costs hurt owner take-home most?

Payroll is the biggest hit to owner take-home, then the $150,000 lease or mortgage, with fixed costs adding up to $296,000 a month. Year 1 payroll is about $30M and climbs above $45M by Year 4, while EBITDA stays negative from -$68M to -$89M, so reserve planning comes before owner pay. If you’re sizing the startup, start with How Much Does It Cost To Open And Launch Your Country Club Business?

Main monthly drains

- $150,000 lease or mortgage

- $60,000 grounds contracts

- $45,000 utilities

- $25,000 insurance

Big cash pressure

- Year 1 payroll: $30M

- Year 4 payroll: above $45M

- Launch capex: $645M

- EBITDA: -$68M to -$89M

How many members does a country club need to be profitable?

A Country Club doesn’t have one profitable member count; dues, mix, churn, facility size, and amenity cost drive the answer. In this model, dues alone need about 5,476 members to cover $53.552M/year in facility, payroll, and marketing costs, so track What Is The Current Member Engagement Level At Country Club? before scaling spend.

Profit math

- $815 weighted monthly dues

- $9,780 annual dues per member

- $3.552M facility costs before labor

- $30M Year 1 payroll

Scale risk

- $20M Year 1 marketing

- $4,000 Year 1 CAC

- $5,500 Year 5 CAC

- Breakeven appears in Month 28

Do dining, events, golf, and tennis increase country club owner income?

Yes — but only when Country Club adds sales that leave contribution profit, meaning revenue after direct costs. Food and beverage COGS are 80% in Year 1 and 70% by Year 5, while pro shop and event supplies are 50% in Year 1 and 40% by Year 5, so dues are the base and dining, events, golf, and tennis help only if they’re priced above variable cost.

What raises income

- Recurring dues set the floor.

- Dining adds margin if waste stays low.

- Events help when priced above labor.

- Lessons and carts lift revenue per member.

What can wipe it out

- Staffing can absorb extra sales.

- Service gaps can hurt repeat spend.

- Inventory waste cuts contribution fast.

- Event labor can erase the upside.

Want the six country club income drivers?

1

$815/moMember Dues

Weighted Year 1 dues are about $815 per member a month, so more active members and a richer mix feed recurring income fast.

2

$296K/moFixed Overhead

The $296K monthly fixed base is the biggest drag on take-home, so every cut in lease, utilities, insurance, and software lifts EBITDA.

3

$3.0MLabor Load

Year 1 wages total about $3.0M, and the 40 FTE service and grounds base can creep up fast without tight scheduling.

4

$4K-$5.5KAcquisition Cost

CAC starts at $4K and climbs to $5.5K, so each new member gets harder to win unless retention stays strong.

5

11%-13%Ancillary Margin

Food, beverage, and event supplies run about 11%-13% of revenue, so tighter buying and pricing protect contribution on social spend.

6

$6.45MCapex Load

The $6.45M build and upgrade program ties up cash early, so payback depends on dues growth beating maintenance and reinvestment needs.

Country Club Core Six Income Drivers

Active member count and recurring dues

Recurring Dues

Dues are the income base because they repeat every month. With a Year 1 mix of $1,500 full golf, $750 tennis and social, and $400 social and dining, weighted monthly dues land at $815, rising to $988 in Year 5. That steady cash flow is what funds owner pay after fixed costs and payroll.

The risk is dues density, not just member count. If pricing or mix slips, $296,000 in monthly fixed costs and payroll can go uncovered fast. Here’s the quick math: $296,000 / $815 ≈ 363 member-equivalents just to cover fixed costs before payroll. Churn, discounts, family plans, and local pricing all move that number.

Protect Dues Density

Track active members by tier, net dues after discounts, churn, family share, and local comp pricing. Those five inputs tell you whether recurring revenue will cover the club’s fixed base and still leave room for profit. If net dues fall below $815 per member-equivalent, owner cash gets squeezed even when headcount looks fine.

- Count members by dues tier

- Measure discount leakage monthly

- Watch churn by segment

- Test family plan pricing

- Reset rates to local comps

Push mix toward higher-value tiers when capacity allows, and keep concessions tight. If Year 5 weighted dues reach $988, more of each new dollar can cover payroll, reserves, and owner take-home. If onboarding or pricing cuts drag the average down, the club can look busy and still run short on cash.

1

Initiation fees, retention, and waitlist strength

Initiation Fees and Waitlist Strength

Initiation fees can lift cash flow, but only if the club can keep the cash. If policy makes fees seasonal, restricted, deferred, or reinvested, they do not fully reach owner pay.

Retention matters because acquisition cost rises from $4,000 in Year 1 to $5,500 in Year 5. Strong waitlist depth supports pricing and reduces cash strain, while weak demand can force dues concessions or more marketing, with budget pressure moving from $20M in Year 1 to $14M by Year 5.

Track Paid Joins, Not Just Sign-Ups

Measure collected initiation fees, retention rate, and waitlist fill rate. Also track how much cash is restricted or deferred by policy, because that changes what the owner can actually draw.

- Count signed, paid, and deferred joins.

- Watch churn by member cohort.

- Test price against waitlist depth.

- Match marketing spend to openings.

Here’s the quick math: a stronger waitlist lets the club hold price and cut paid acquisition, while a weak one pushes up marketing and concessions. With acquisition cost already climbing from $4,000 to $5,500, every retained member protects cash that would otherwise be spent replacing them.

2

Ancillary spend from dining, events, golf, and tennis

Ancillary Spend Profit

Ancillary spend includes dining, banquets, guest events, carts, lessons, and pro shop sales. It lifts revenue per member, but profit depends on mix: food and beverage COGS start at 80%, and pro shop and event supplies start at 50%. So $10,000 of dining sales can leave about $2,000 before labor, while $10,000 of shop sales can leave about $5,000 before labor.

The owner’s take-home rises only when added sales use idle clubhouse and course time. The key inputs are member count, average check, event volume, guest counts, and labor tied to kitchen, carts, and service. Revenue is not profit.

Track Margin by Event

Measure each line separately: dining, banquets, guest events, lessons, carts, and shop sales. Track average check, food cost, labor hours, and sell-through so you can see which events create contribution profit after direct costs. If an event fills off-peak time but needs extra staff or inventory, the margin can disappear fast.

Price for the full load, not just the headline sale. Use member-friendly scheduling, cap menus where kitchen capacity is tight, and control inventory so sales do not turn into waste. The best ancillary dollar is the one that fits existing space and staff.

3

Facility utilization and amenity scheduling

Facility Utilization and Scheduling

When the club fills tee times, courts, dining rooms, and event spaces, the same $296,000 in monthly fixed facility costs before payroll gets spread across more member activity. That lifts margin and helps cash flow reach the owner faster. The key metric is booked capacity versus available hours, not just member count.

But this only works if the club protects exclusivity. Overcrowding can raise churn and force dues pressure. Planned downtime for turf, irrigation, court care, clubhouse repairs, and service reset is part of the income model, so idle hours should be managed, not ignored.

Track Capacity by Amenity

Measure utilization rate by tee sheet, court hour, dining seat, and event night. Then compare booked hours, no-show rate, and wait times against member complaints and churn. Here’s the quick test: if more bookings raise revenue but service slips, the owner’s take-home can fall.

Use off-peak scheduling for social events and seasonal amenities to turn slack periods into contribution profit. Keep a simple rule: fill the weak hours, not the peak hours. That protects pricing power, preserves member experience, and keeps fixed cost absorption high.

- Track booked vs. open hours daily.

- Limit peak-time overcrowding.

- Schedule downtime on low-demand slots.

- Review churn after busy weekends.

4

Labor efficiency and service model

Labor efficiency and service model

Payroll is the gatekeeper here. In Year 1, labor runs about $30M and climbs above $45M by Year 4, while service and grounds staff rise from 40 FTE to 65 FTE. The leadership layer alone includes a $250,000 General Manager, $130,000 Executive Chef, $120,000 Head Golf Professional, and $100,000 Director of Tennis. If service slips, retention and dues pricing can weaken fast.

Here’s the quick math: the payroll increase is about $15M, or 50%, while staff count rises 62.5% from 40 to 65. That means the owner only wins if added labor supports more member revenue, better retention, or higher pricing power. What this estimate hides is service quality risk: trimming too hard can save cash now but hurt renewals later.

Measure payroll against member service

Track payroll by department, overtime, and staffed service hours, then tie each to member demand. The key test is simple: does each added dollar of labor protect dues, improve retention, or lift spend? If not, it is likely dragging owner inc ome. Keep fixed leadership pay visible, because the four named roles already total $600,000 before hourly labor.

- Watch payroll by department monthly.

- Match staffing to peak tee times.

- Protect service during busy periods.

- Cut overtime before cutting coverage.

- Test staffing changes by member feedback.

Use a service-first staffing plan. Service and grounds labor should flex with traffic, but the club still needs enough coverage to keep the experience premium. If understaffing hurts member satisfaction, dues pricing gets harder to defend and churn risk rises. If staffing is too loose, payroll eats the cash that should reach the owner.

5

Maintenance reserves, capital improvements, and debt service

Reserves, Capex, and Debt Service

For this club, maintenance reserves are a pre-owner-pay deduction. The business also carries $645M in launch capex, including $25M for the clubhouse renovation and $12M for irrigation, plus $150,000 per month in fixed lease or mortgage cost. That is $1.8M a year before repairs, replacements, or owner draw.

Input the reserve schedule, the timing of each capital project, and the debt payment path. If reserves are too low, the club defers upkeep, then member churn rises, repairs get bigger, and pricing power weakens. One clean rule: fund the roof, turf, courts, kitchen, and systems before take-home pay.

Track Reserves Like a Fixed Bill

Build the reserve as a monthly line item, not a leftover. Watch capex per member, debt service coverage, and the share of dues that gets set aside before distributions. If monthly fixed payments stay at $150,000, reserve gaps hit cash fast, so owner income should rise only after the club funds needed upkeep.

- Track each asset’s replacement date.

- Separate repair and upgrade spend.

- Match reserves to member usage.

- Test pricing against upkeep needs.

6

Compare low, base, and high country club owner income scenarios

Owner income scenarios

Owner income stays under pressure because heavy capex, high fixed costs, and negative EBITDA hit before cash flow stabilizes. The gap between low, base, and high cases comes down to member growth, mix, and whether the club funds its fixed load first.

| Scenario | Low CaseDownside | Base CasePlan case | High CaseUpside |

|---|---|---|---|

| Launch model | Owner income stays negative because growth is slow and fixed costs keep running at full load. | Owner income follows the modeled path, but cash stays tight even as the club reaches Month 28 breakeven. | Owner income improves only if the club adds more members, improves dues mix, and keeps payroll tighter. |

| Typical setup | Member churn is higher, events stay weak, and the club carries the full lease, staffing, and maintenance burden before any owner draw. | The model uses the stated dues mix and prices, with EBITDA still negative in Years 1-5, about -$6.849M to -$8.890M, $6.45M of capex, and minimum cash at -$44.635M by Month 60. | A stronger golf-weighted member base, lower CAC, better ancillary spend, and tighter staffing schedules improve cash, but funding needs still matter before any meaningful draw. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No owner take-homeNo draw | No owner take-homeNo draw | Limited owner drawGrowth case |

| Best fit | Use this to stress-test a soft launch with weak retention and no room for owner distributions. | Use this for lender and board planning when the club hits breakeven on paper but still needs cash support. | Use this to test whether better volume and cost control can support a real owner draw later on. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Country Club Porter's Five Forces Analysis

- Country Club BCG Matrix

- Country Club Business Model Canvas

- 7 Critical KPIs to Track for Your Country Club

- Country Club Business Plan Template in Pre-Written Word

- Increase Country Club Profitability: 7 Strategies for Margin Improvement

- How Much Does It Cost to Run a Country Club Each Month?

- Country Club Startup Costs: $645M CAPEX Before Working Capital

- Country Club Financial Model Template in Excel

- Start A Country Club: 28-Month Breakeven Launch Guide

- How to Write a Country Club Business Plan: 7-Step Financial Guide

- Country Club Marketing Mix

- Country Club Marketing Plan

- Country Club Business Proposal

- Country Club PESTEL Analysis

- Country Club Pitch Deck Example Editable PPTX

- Country Club Business SWOT Analysis

- Country Club Value Proposition Canvas

Frequently Asked Questions

In this researched case, a guaranteed owner salary is not supported because EBITDA is negative every year The model shows -$68M EBITDA in Year 1 and -$89M in Year 5 Owner pay should be tested as pre-tax discretionary cash flow after payroll, fixed costs, reserves, capex, and debt or lease obligations