Owner income$283k to $1.91M

Owner income$283k to $1.91MHow Much Does a Craft Beer Bar Owner Make? $283k Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$283k to $1.91M  Net margin26% to 58%

Net margin26% to 58% Revenue for target pay$1.10M

Revenue for target pay$1.10M Business difficultyHard

Business difficultyHard

You’re looking at owner take-home, not bartender wages or brewery production economics This five-year craft beer bar model shows $1096M Year 1 revenue, $283k Year 1 EBITDA, and breakeven in Month 3, before taxes, debt service, reinvestment, and personal owner choices

Owner income$283k to $1.91MNet margin26% to 58%Revenue for target pay$1.10MBusiness difficultyHardWant to test your craft beer bar owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will move with sales, margins, payroll, taxes, debt, and reserve policy.

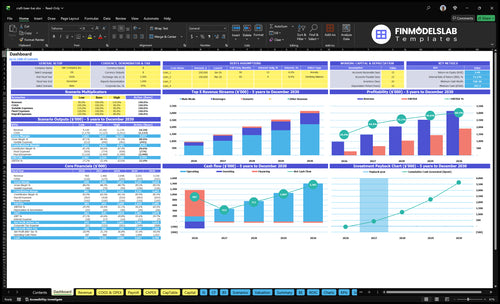

Want the Craft Beer Bar financial model view?

Open the Craft Beer Bar Financial Model Template to see revenue, EBITDA, cash, break-even, and payback, plus assumptions for covers, AOV, sales mix, COGS, payroll, fixed costs, and capex.

Owner-income model highlights

- Owner pay tied to EBITDA

- Reserve and debt-service view

- Year 1 to 5 scenarios

How do craft beer bar margins affect owner take-home?

Owner take-home gets squeezed or helped by COGS, because every 1 point of margin moves straight into EBITDA unless price or volume offsets it. For setup context, see What Is The Estimated Cost To Open Your Craft Beer Bar?; the model puts food and beverage ingredients at 100% in Year 1, easing to 90% by Year 5, and packaging and supplies at 20% falling to 15%. Mix shifts from 25% beverage and 70% meals to 29% beverage and 66% meals, so the bar’s take-home depends on mix, waste, and pricing discipline.

Margin levers

- Track draft beer COGS by keg

- Separate package mix from draft

- Watch waste and comps weekly

- Model happy hour pricing

Cost items to isolate

- Specialty keg costs by SKU

- Food and beverage ingredients

- Packaging and supplies inflation

- Volume offsets for margin loss

How does the owner role change craft beer bar income?

If the owner works the floor, the Craft Beer Bar can look stronger on cash flow because the owner can replace paid management or shifts. Here’s the quick math: a Restaurant Manager is already modeled at $65,000 per year, and total payroll runs $314,000 in Year 1 before rising to $487,000 by Year 5 as staffing scales.

Working-owner impact

- Owner labor can cut payroll cash outlay.

- Paid management makes costs clearer.

- Absentee ownership still needs oversight.

- Service quality drives margin every day.

What protects profit

- Controls keep inventory tight.

- Scheduling prevents extra labor.

- Shrinkage can shrink distributions.

- Repairs can erode owner payouts.

What is a realistic craft beer bar owner salary?

A realistic Craft Beer Bar owner salary starts with EBITDA, not revenue: the model shows $283k Year 1 EBITDA on $1.096M revenue, so salary must come after reserves, debt, reinvestment, and taxes. Use What Is The Most Important Metric To Measure The Success Of Craft Beer Bar? to keep salary tied to operating performance, not wishful top-line sales.

Salary Range Logic

- Start with $283k EBITDA

- Hold cash for slow months

- Pay debt before distributions

- Separate salary from profit

Owner Pay Risks

- Year 5 EBITDA: $1.905M

- Year 5 revenue: $3.288M

- Unpaid shifts hide labor gaps

- Taxes reduce real take-home

Want the six drivers behind craft beer bar income?

1

$1.10M-$3.29MRevenue Volume

More covers and higher check sizes lift sales from Year 1 to Year 5, and that sets the ceiling on owner take-home.

2

$314K-$487KLabor Efficiency

Payroll climbs fast as staffing grows, so tighter scheduling and faster turns protect profit.

3

88.0%-89.5%Beverage Margin

Keeping drink and ingredient costs low leaves more cash after each sale, so small mix shifts matter.

4

$12.9K/moFixed Costs

Rent, utilities, and overhead set a steady drag, and sales have to clear that base before owner pay rises.

5

100-450/dayEvents Traffic

Events and repeat visits fill slower days, which smooths traffic and supports a faster path to profit.

6

$767KCash Buffer

Minimum cash drops to $767K in Month 2, so cash reserves and debt service can decide whether you reach Month 3 breakeven.

Craft Beer Bar Core Six Income Drivers

Revenue Volume

Revenue Volume

Revenue volume sets the ceiling on owner pay. In year 1, 965 weekly covers at $21,080 a week annualize to about $1.096M ($21,080 × 52). By year 5, 2,235 weekly covers and $63,240 a week annualize to about $3.288M. More covers, a higher check, and more open days all push the top line.

Saturday drives the shape of the week. Year 1 Saturday volume is 200 covers at $25, or $5,000 in daily sales. Here’s the catch: if demand is still light, payroll can get built for a full room that has not arrived yet, and owner profit gets squeezed before the bar has enough traffic to support it.

Track Covers and Check

Watch covers by day, average check, seat turnover (how often each seat sells again), open days, and event lift. Those five inputs tell you whether revenue is coming from real traffic or just longer hours. If covers rise but check size slips, the bar can look busy and still miss the cash needed for owner draw.

- Covers by day

- Average check

- Seat turnover

- Open days

- Event lift

Use a weekly forecast tied to booked covers and event dates. If trivia, tastings, or brewery nights add traffic, measure the extra covers and sales, not just the buzz. That keeps labor and hours matched to demand, which protects margin and leaves more room for the owner to pay themselves.

1

Beverage Gross Margin

Beverage Gross Margin

Beverage gross margin is the cash left after beer cost, supplies, waste, and comps. In this model, COGS and supplies equal 120% of revenue in Year 1 and 105% in Year 5, so drink sales must be tightly managed before they can fund payroll, rent, or owner pay. Beverage mix also rises from 25% to 29%, so small shifts in pour cost hit cash fast.

Here’s the quick math: stronger specialty rotations can lift check size, but they can also raise keg cost and spoilage risk. What this estimate hides is processing and marketing, so the cash available for take-home pay is tighter than gross drink sales alone suggest.

Track Pour Cost, Not Just Sales

Measure draft COGS, keg yield, pour cost, package beer margin, waste, comps, and supplier pricing every week. Tie each rotation to a check-size lift and compare it with added keg cost and spoilage risk, or you can grow revenue while shrinking cash.

- Log actual ounces poured.

- Count comped and spilled drinks.

- Review supplier prices monthly.

2

Labor And Scheduling

Labor And Scheduling

Labor is the biggest controllable cost after product. In this model, Year 1 payroll is $314k against $1.096M revenue, and Year 5 payroll is $487k against $3.288M revenue. That means staffing can squeeze owner pay fast if labor stays fixed while sales lag, especially on slow weekdays.

The labor plan includes manager, head chef, line cooks, kitchen assistants, customer service lead, and dishwasher. Owner shifts can cut cash payroll, but unpaid labor should be tracked separately so margins are real. One clean rule: don’t staff Tuesday like Saturday.

Staff to the daypart

Track labor as a percent of sales by day, not just by month. Use covers, average check, and open hours to build each shift, then compare midweek and weekend staffing. Here’s the quick math: if payroll is held near 29% of Year 1 revenue and 15% of Year 5 revenue, more cash stays available for rent, inventory, and owner draw.

- Match staffing to covers.

- Separate owner hours.

- Watch weekday labor spikes.

- Cut overlap on slow shifts.

- Review schedule vs. sales weekly.

What this estimate hides: if slow midweek shifts carry weekend-level staffing, labor burns cash before the bar can scale. That risk shows up first in lower operating profit, then in weaker owner distributions.

3

Occupancy And Fixed Costs

Occupancy And Fixed Costs

$129k per month in fixed costs means the bar has a high revenue floor before the owner sees real take-home pay. Rent is $75k per month, or $90k per year, and the rest sits in utilities, software, insurance, repairs, cleaning, accounting and legal, and waste management.

That load is 141% of Year 1 revenue and still 47% of Year 5 revenue, so lease size matters as much as sales growth. Here’s the quick math: if traffic starts slow, fixed costs keep running while owner pay gets squeezed. The main risk is signing a lease that needs high traffic from day one.

Track Rent Before You Sign

Measure the full fixed-cost stack, not just base rent. Track rent, utilities, software, insurance, repairs, cleaning, accounting and legal, and waste management as one monthly number, then compare it to actual covers, average check, and weekly sales. If revenue misses plan, owner pay is the first thing that gets crowded out.

Use the lease to stress-test slow months and weak midweek traffic. A $75k monthly rent commitment only works if the store can keep enough gross profit after product, labor, and payment fees to cover the $129k fixed bill. If not, negotiate smaller space, lower base rent, or a later rent step-up.

4

Events And Repeat Customers

Event Nights Drive Midweek Covers

Events like tap takeovers, trivia, tastings, mug clubs, live music, and brewery partnerships matter because they move Monday through Thursday traffic. Year 1 midweek volume is 435 covers a week at an $18 average check, or $7,830 weekly. Weekend volume is 530 covers at $25, or $13,250.

Here’s the quick math: total weekly sales are $21,080, which annualizes to about $1.096 million. Every 10 extra midweek covers add $180 a week, or $9,360 a year, before labor and promo costs. The risk is paying for events that do not lift covers or repeat visits.

Track Cover Lift, Not Just Attendance

Measure each event against the same weekday baseline. Track added covers, average check, repeat visits, and any change in labor needed to run the night. If the event fills seats but check size drops, the lift may not reach owner pay or cover the extra staffing.

- Compare event night vs baseline.

- Watch check size by day.

- Track repeat visits within 30 days.

- Stop events without cover growth.

Use the first month to test what brings people back, then keep the formats that add steady weekday traffic. The best events improve gross margin only when the extra covers beat promo spend, pour cost, and labor.

5

Cash Reserves And Debt Service

Cash Reserves Before Owner Draws

A craft beer bar’s owner can only pay themselves from cash left after rent, payroll, inventory, and debt service. This model shows a $767k minimum cash need in Month 2, plus $263k capex, with Month 3 breakeven and 15 months to payback, so early profit does not equal safe draw.

Here’s the quick math: EBITDA rises from $283k in Year 1 to $1,905M in Year 5, but cash still has to cover loan payment s, repairs, inventory rebuilds, seasonal slowdowns, and reserves. If the balance dips below the target, owner distributions should stop first.

Track Cash Cover and Debt Dates

Measure cash on hand, monthly debt service, and the cash runway in weeks. Build a 13-week forecast that includes beer and food reorders, payroll timing, capex, and tax payments. If the bar needs to rebuild stock after a busy weekend, that cash must stay inside the business, not go to the owner.

Set a reserve floor before any draw. Use the floor to test three items: slow-season sales, one repair event, and one missed weekend target. If any one of those pushes cash below the floor, the owner pay rate is too high for the current trading level.

6

Compare lean, base, and strong craft beer bar owner income cases

Owner income scenarios

Owner income moves with traffic, pricing, and labor load. The low case assumes the owner covers shifts; the high case assumes denser demand and repeat visits.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower-income path, with the owner still working shifts. | This is the modeled mid-case path, with steadier earnings as the bar scales. | This is the stronger-income path, with the best payoff from dense demand. |

| Typical setup | Year 1 model: $1.096M revenue, 88.0% gross margin, $314k payroll, $1.548M fixed costs, and $283k EBITDA; Month 3 breakeven keeps pressure on daily cover counts. | Year 3 model: $2.138M revenue, 88.7% gross margin, $426k payroll, and $1.046M EBITDA, with stronger manager controls needed as volume rises. | Year 5 model: $3.288M revenue, 89.5% gross margin, $487k payroll, and $1.905M EBITDA, supported by repeat traffic and fuller capacity. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $283kLow income | $1.046MScale case | $1.905MUpside case |

| Best fit | Use this to stress test a slower launch with high operating effort and tight margin control. | Use this as the core planning case for a bar that is gaining traction but still needs tight day-to-day control. | Use this to test the upside if the bar wins regular traffic and runs with tight labor discipline. |

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. They are before taxes, debt service, reserves, and reinvestment.

Related Products

- Craft Beer Bar Porter's Five Forces Analysis

- Craft Beer Bar BCG Matrix

- Craft Beer Bar Business Model Canvas

- 7 Critical KPIs to Scale Your Craft Beer Bar

- Craft Beer Bar Business Plan Template in Pre-Written Word

- 7 Concrete Strategies to Increase Craft Beer Bar Profitability

- How to Run a Craft Beer Bar: Essential Monthly Operating Costs

- Craft Beer Bar Startup Costs: $263K CAPEX And $767K Cash Need

- Craft Beer Bar Financial Model Template in Excel

- How To Open A Craft Beer Bar In 6 To 12 Months With Launch Steps

- How to Write a Craft Beer Bar Business Plan in 7 Steps

- Craft Beer Bar Marketing Mix

- Craft Beer Bar Marketing Plan

- Craft Beer Bar Business Proposal

- Craft Beer Bar PESTEL Analysis

- Craft Beer Bar Pitch Deck Example Editable PPTX

- Craft Beer Bar Business SWOT Analysis

- Craft Beer Bar Value Proposition Canvas

Frequently Asked Questions

The modeled owner-income pool starts with EBITDA, not revenue In this case, Year 1 revenue is $1096M and EBITDA is $283k By Year 5, revenue reaches $3288M and EBITDA reaches $1905M Actual take-home is the portion left after taxes, debt service, reserves, reinvestment, and any owner salary choices