Time to Open8-16 weeksLaunch runway

Time to Open8-16 weeksLaunch runwayHow To Open A Credit Risk Assessment Business In 8–16 Weeks

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Time to Open8-16 weeksLaunch runway  Launch Sequence6 stagesCompliance first

Launch Sequence6 stagesCompliance first Key BottleneckData accessLicense and data

Key BottleneckData accessLicense and data First Revenue StepPaid pilotPilot approval

First Revenue StepPaid pilotPilot approval

To start a credit risk assessment business, form the company, define a B2B lender niche, confirm US compliance exposure, secure data sources, document the scoring method, set up secure reporting, test with pilot clients, and then launch sales outreach The researched planning assumption is an 8–16 week launch window, mainly driven by data vendor approval, Fair Credit Reporting Act (FCRA) exposure if consumer credit data is used, and pilot validation Day-one readiness means you can explain how borrower default risk is evaluated, protect client data, and deliver reports lenders can use in underwriting First revenue should come from a paid pilot, portfolio review, underwriting support project, or recurring risk monitoring engagement

Time to Open8-16 weeksLaunch runwayLaunch Sequence6 stagesCompliance firstKey BottleneckData accessLicense and dataFirst Revenue StepPaid pilotPilot approvalLaunch timeline

This is a short web summary of the launch plan; the XLSX export carries the detailed Gantt chart.

Launch scheduleWeek 1Week 2Week 3Week 4Week 5Week 6Week 7Week 8Week 9Week 10Week 11Week 12

Legal / compliance

- Form entity

- Review data law

- Draft contracts

- Approve compliance

Data / vendors

- Shortlist sources

- Request quotes

- Sign data deals

- Map fields

- Load test feeds

Scoring model

- Define score rules

- Build scorecard

- Validate samples

- Calibrate thresholds

- Document method

Tech / security

- Set cloud stack

- Build portal

- Add access controls

- Set audit logs

- Test exports

Staffing / ops

- Hire analyst

- Train workflow

- Set QA checks

- Prep support

- Review cadence

Sales / pilot

- Pick niche

- Build lead list

- Start outreach

- Run pilot

- Gather feedback

- Close first deals

Why test launch timing before opening?

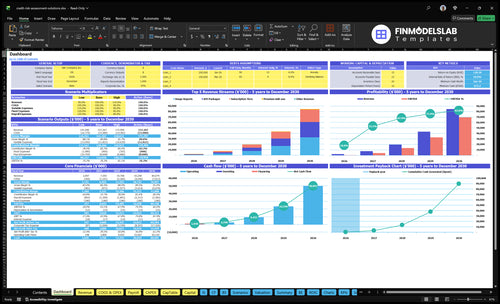

The screenshot shows revenue, costs, cash needs, assumptions, and break-even logic—open the Credit Risk Assessment Financial Model Template.

Financial model highlights

- Dashboard and model tabs

- Client ramp and tiers

- Usage, API, add-ons

- Validation, wages, fixed costs

- CEO, data, engineering, sales, CS

- $150k marketing, $1,500 CAC

- $15k fixed monthly

- 28% revenue-linked load

- About $817k base burn

- Runway and break-even path

Do you need a license to start a credit risk assessment business?

Credit Risk Assessment may not need a standalone license, but it may trigger the Fair Credit Reporting Act, 15 U.S.C. §1681, if it uses consumer credit data or supports lending decisions; see What Is The Most Important Indicator For Credit Risk Assessment Business Success? before vendor onboarding or pilots.

License trigger

- Check consumer data use first

- Confirm permissible purpose before reports

- Review client lending use cases

- Document FCRA position before sales

Compliance cost

- $100-$1,000 statutory damages per consumer

- Adverse-action support may be required

- Privacy and contracts need review

- Get legal review before pilots

What mistakes delay a credit risk assessment launch?

Credit Risk Assessment launches get delayed when teams sell before a compliance review, rely on weak data, or skip model documentation. The fast fix is a readiness check for permissible data use, vendor contracts, scoring logic, security controls, report QA, and buyer segment. Here’s the quick math: in Year 1, data licensing can be 12% of cost, cloud processing 5%, and validation 3%, so rework gets expensive fast.

Main launch delays

- Compliance review comes after sales

- Weak data sources slow trust

- Undocumented logic blocks approvals

- Poor security raises buyer risk

Go or no-go checks

- Verify permissible data use

- Lock vendor contracts first

- Document scoring logic clearly

- Test buyer segment fit early

How long does it take to launch credit risk assessment services?

Credit Risk Assessment usually takes 8–16 weeks to launch. The fastest path is a narrow B2B commercial-lending niche with client-provided portfolio data; the slower path adds consumer data, external vendor approvals, API delivery, and deeper security review. Here’s the quick rule: compliance first, then data intake, then model validation, then pilots, then broad sales.

Fastest launch path

- Pick one B2B lending niche

- Use client-provided portfolio data

- Validate scoring before pilots

- Start broad sales after pilots

Main launch delays

- Vendor contracts slow setup

- Consumer data adds review

- API delivery adds work

- Unclear scoring docs delay approval

Confirm what must be ready before opening

Launch readiness checklist

Use this go-live approval checklist before opening the credit risk assessment service.

Entity & permissions

- Entity setup completeCritical

You need a legal entity before contracts, banking, and onboarding.

- Permissible data use signedCritical

No borrower data should enter the model until use is allowed in writing.

- Client contract terms reviewedHigh

Terms should cover scope, limits, liability, and client data handling.

Data rights

- Data vendors approvedHigh

Use only sources with clear rights, coverage, and stable delivery.

- Input quality checks setCritical

Bad inputs produce bad scores, so checks must run before launch.

- Refresh schedule definedMedium

Model timing must match client use or risk scores go stale.

Model method

- Inputs and assumptions loggedCritical

Clients need a clear method for what drives each score and what it does not cover.

- Scoring logic documentedCritical

This keeps the model explainable when clients ask why a score changed.

- Risk tiers mappedHigh

Clear cutoffs turn scores into actions the client team can use.

- Review steps definedHigh

A fixed review path lowers errors before a score reaches a client.

Security & audit

- Access controls enabledCritical

Only approved staff should see borrower data and score outputs.

- Audit trail records liveCritical

Logs must show who changed data, rules, or reports.

- Secure reporting flow testedHigh

Clients need safe delivery of reports without exposing raw data.

Team & controls

- Roles assignedHigh

Each task needs one owner so analysis, QA, and client work do not slip.

- Training completedHigh

Staff should know privacy, model limits, and escalation steps before go-live.

- Go-live signoff completeCritical

Do not launch until compliance, data, and model method are all signed off.

Launch economics

- Pilot offer readyHigh

Start with one clear offer so early client feedback is comparable.

- Client intake and payment testedHigh

The first revenue step needs a working path from lead to invoice or payment.

- Sales channel confirmedHigh

Pick one path to reach clients and keep the first pipeline measurable.

- Unit economics testedCritical

Year 1 uses $150,000 marketing, $1,500 CAC, $15,000 fixed monthly costs, and 28% variable plus COGS load.

- Cash runway stress testedCritical

Minimum cash is $672,000 in Month 6, and breakeven is Month 6, so funding must cover the trough.

Which launch drivers matter most?

1Compliance Position

Launch gateWritten compliance approval prevents blocked pilots and cleaner lender onboarding.

2Data Access

12% revSigned data access cuts vendor lag and reduces report disputes.

3Scoring Methodology

QA modelA documented score with QA builds lender trust and speeds paid pilots.

4Secure Reporting Workflow

$3K/moSecure delivery lowers onboarding objections and protects borrower data during pilots.

5Lender Sales Pipeline

$150K / $1.5K CACA named buyer list turns marketing spend into first signed pilots.

6Operating Capacity

$650KYear 1 staffing load is about $650K, so pilot volume must stay disciplined.

Compliance Position

Compliance Position

Compliance is the first launch gate for this business. If the service touches consumer credit data, supports lending decisions, or even looks like it does, opening can stop until legal, privacy, and sales claims are lined up. If the firm is truly commercial-only analytics, the written boundary still has to be clear on day one.

Readiness means a written compliance position, approved data use, contract language, and report-use limits. Permissible purpose means the data use is allowed for the stated lending job. The main risk is shipping reports that clients use for credit decisions before review, which can delay onboarding and block first revenue.

Lock the use case before launch

Before opening, get legal review, privacy controls, permissible purpose checks, and sales-claim review done in sequence. That keeps the launch plan realistic and avoids rework after pilots start. One clear rule helps: if the report could affect lending, it needs compliance sign-off first.

Document what the report can and cannot be used for, then bake that into client contracts and sales scripts. Keep the boundary simple enough for onboarding teams to follow. If the team cannot explain the use case in one sentence, the launch is not ready.

- Confirm consumer vs. commercial data use

- Approve contract and report wording

- Test sales claims against compliance

- Set a written use boundary

1

Data Access

Data Access

This launch lives or dies on whether you have approved borrower, financial, payment, public-record, or portfolio data that fits the lender niche. No clean data feed, no day-one report. Year 1 data acquisition and licensing is modeled at 12% of revenue, so weak vendor terms or slow approvals can push cash needs up before the first pilot converts.

Readiness starts with signed vendor or client data access, a data dictionary, quality checks, and a permission trail. If the source data is messy, the first issue is not model quality, it’s report disputes, rework, and delayed launches. Faster pilots depend on data that is stable enough to trust and specific enough for the client’s credit use case.

Data access setup

Before opening, lock the data path end to end. Here’s the quick test: can you get the same fields every time, can you explain each field, and can you prove you had rights to use it? If any of those fail, opening date slips because onboarding, QA, and client review all slow down.

- Verify borrower and portfolio source rights.

- Document every field in a data dictionary.

- Run quality checks before first client delivery.

- Keep a permission trail for every source.

- Test one pilot niche before scale-up.

What this estimate hides: bad data can still pass a contract screen but fail in live use. That means more analyst time, slower cash collection, and more back-and-forth with clients. Clean access upfront is what keeps the first reports on schedule and cuts disputes after launch.

2

Scoring Methodology

Documented Scoring Model

If the score is not documented, lenders will slow the launch or refuse to use it. Day one depends on a repeatable borrower default risk model with clear inputs, scoring logic, risk tiers, assumptions, and analyst review so the team can defend each report during pilot use.

The main risk is a black-box score that cannot be explained inside a lender’s credit file or committee process. Build in validation and client-facing notes before pilots, with Year 1 model validation at 3% of revenue, so the first reports are usable without extra rework or credibility damage.

Lock the model before pilots

Before opening, verify the full scoring pack: inputs, scoring logic, risk tiers, assumptions, model validation, QA steps, and explainable outputs. That is the launch gate. If any of these are still moving, pilot timing slips and the sales team will struggle to promise a stable first delivery.

- Document model inputs and source rules.

- Define risk tiers before client demos.

- Write plain-English analyst notes.

- Test repeatability on sample borrowers.

- Approve the client explanation template.

What this setup protects: faster trust, fewer report disputes, and smoother paid pilot conversion. What it hides: if validation takes longer than planned, the team may need more review time and a later launch date, even if the software is ready.

3

Secure Reporting Workflow

Secure Reporting Workflow

This driver decides whether lenders will trust the platform enough to send borrower data on day one. The workflow needs role-based access, encrypted storage, a secure file exchange or portal, report templates, record retention, and an audit trail. If any step is missing, onboarding slows and sales teams face objections before the first pilot starts.

Here’s the quick math: base cloud infrastructure is modeled at $3,000 per month, plus usage-based cloud processing at 5% of Year 1 revenue. That cost only works if the workflow is stable from the start, because weak borrower data security is the main bottleneck and can delay launch-ready report delivery.

Lock Down Data Flow

Before opening, map exactly how borrower files enter, get processed, and leave the system. Test each control: access roles, encryption, file transfer, retention, and audit logs. The goal is simple: a lender should be able to upload data, get a report, and trace who touched it without any manual scramble.

- Confirm who can view raw files.

- Test encrypted storage and transfers.

- Load report templates before pilots.

- Set retention and deletion timing.

- Verify audit logs after each run.

4

Lender Sales Pipeline

Named Buyer List

For credit risk assessment, launch only works if the first buyers are specific. Small lenders, fintechs, loan brokers, private credit firms, and commercial finance teams are the best-fit groups. If positioning is broad, you may book meetings but still miss signed pilots, which pushes back opening, raises cash burn, delays first revenue, and leaves the team with no live feedback on day one.

Build the Pilot Funnel

Before launch, lock a named buyer list, one pilot offer, one sample report, one outreach message, and one follow-up workflow. Here’s the quick math: $150,000 in Year 1 marketing at $1,500 CAC implies about 100 customers if that cost holds. Tie niche choice to pilot pricing and report scope so sales can move from interest to a signed test.

- Use one buyer type first.

- Price the pilot before outreach.

- Match report scope to buyer needs.

- Track follow-up after every reply.

5

Operating Capacity

Day-One Operating Capacity

Operating capacity is the launch gate here. This business cannot open cleanly unless analysis, data handling, client communication, report QA, compliance oversight, engineering, sales, and account management are covered from day one. With Year 1 wages modeled at about $650,000 before benefits or taxes, the staffing plan has to match launch scope, or pilot work will outrun review capacity.

The readiness signal is a defined analyst workflow and turnaround time. If the team cannot review reports fast enough, clients will see delays, QA misses, and weaker trust. The real bottleneck is selling more pilot work than the team can examine well, because that turns growth into service failure instead of first revenue.

Staff to the Review Load

Before opening, map who owns each step and how long each step takes. The Year 1 plan assumes a CEO, Lead Data Scientist, Senior Software Engineer, Sales Manager, and 5 Customer Success Managers. That mix only works if handoffs are written down, QA is assigned, and client follow-up does not steal time from analysis.

Test the workflow on a small pilot set before launch. Confirm who checks data, who signs off on reports, who answers client questions, and what the turnaround time is. If volume rises before capacity is proven, the team will need more cash, more hires, or both, and opening-day service will slip.

6

Related Products

- Credit Risk Assessment Porter's Five Forces Analysis

- Credit Risk Assessment BCG Matrix

- Credit Risk Assessment Business Model Canvas

- 7 Essential Financial KPIs to Scale Credit Risk Assessment

- Credit Risk Assessment Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Credit Risk Assessment Profitability

- How Much Does It Cost To Run Credit Risk Assessment Monthly?

- Credit Risk Assessment Startup Costs: $80K+ CAPEX And $11M Runway

- Credit Risk Assessment Financial Model Template in Excel

- How Much Do Credit Risk Assessment Owners Make?

- How to Write a Credit Risk Assessment Business Plan: 7 Steps

- Credit Risk Assessment Marketing Mix

- Credit Risk Assessment Marketing Plan

- Credit Risk Assessment Business Proposal

- Credit Risk Assessment PESTEL Analysis

- Credit Risk Assessment Solutions Pitch Deck Example Editable PPTX

- Credit Risk Assessment Business SWOT Analysis

- Credit Risk Assessment Value Proposition Canvas

Frequently Asked Questions

Start with a narrow paid pilot before building a full platform Use lender-provided portfolio data, document your scoring method, and deliver secure reports manually This keeps the launch closer to the 8–16 week range while you test demand Track Year 1 assumptions like $1,500 CAC, $150,000 marketing spend, and 3% validation cost