Critical Illness Insurance Agency Startup Costs: $195K+ Launch Budget

You’re opening a regulated agency before commissions have time to catch up, so cash planning matters more than furniture choices This critical illness insurance agency launch budget covers disclosed CAPEX of $195,000+, first-year marketing of $135,000, fixed overhead of $14,600/month, and Year 1 payroll of $520,000 These are researched planning assumptions, not vendor quotes or guaranteed costs

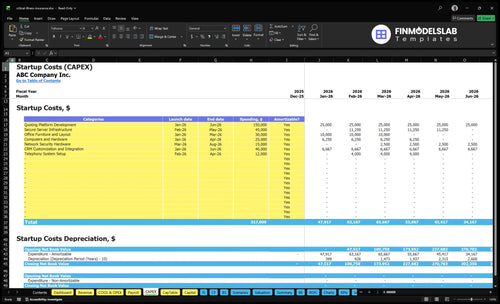

Insurance agency CAPEX calculator objective

Startup CAPEX Calculator

This estimates capitalized startup assets only for a critical illness insurance agency, not operating cash or payroll runway.

Scope limit This calculator covers capitalized startup assets only. It excludes licensing, payroll runway, SaaS subscriptions, marketing, commissions, working capital, deposits, debt service, and other operating costs.

Where do startup costs show up?

The screenshot shows the CAPEX tab in the Critical Illness Insurance Agency Financial Model Template, with startup costs, launch timing, depreciation, amortization, and working capital. Open it and adjust assumptions.

Key screenshot checks

- $150k platform build

- $45k secure servers

- $350/$1,500 CAC

How do I fund a critical illness insurance agency startup?

For a Critical Illness Insurance Agency, fund the launch as a cash plan, not a loan plan: disclosed startup needs already total about $1,025,200 from $195,000+ CAPEX, $520,000 payroll, $175,200 fixed overhead, and $135,000 marketing. Use the insurance agency financial model to test whether $350 buyer CAC and $1,500 carrier CAC still work once commissions hit, then keep debt light until commission timing is clear.

Funding plan

- Founder equity covers first cash need

- Partner capital reduces early strain

- Staged hiring protects runway

- Delay debt until commissions clear

Model checks

- Test buyer CAC at $350

- Test carrier CAC at $1,500

- Stress first-year runway before hiring

- Track break-even timing monthly

How much money do I need to start a critical illness insurance agency?

You should plan for at least $1,025,200 in disclosed Year 1 funding for a Critical Illness Insurance Agency, not just the $195,000+ CAPEX base; see What Are Operating Costs For Critical Illness Insurance Agency? for the fixed-cost view. Here’s the quick math: $195,000+ CAPEX + $520,000 payroll + $175,200 fixed overhead + $135,000 marketing, before office furniture/layout, state licensing, errors and omissions (E&O) insurance, deposits, variable policy costs, and cash reserve.

Budget floor

- $195,000+ disclosed CAPEX

- $520,000 Year 1 payroll

- $14,600/month fixed overhead

- $135,000 Year 1 marketing

Do not miss

- Office furniture and layout

- State licensing costs

- E&O insurance coverage

- Cash reserve for ramp-up

What are the biggest cost drivers for a critical illness insurance agency?

For a Critical Illness Insurance Agency, the biggest cost drivers are Year 1 payroll at $520,000, $195,000+ in CAPEX, and $135,000 in marketing. The fixed base also matters: $14,600/month overhead, $1,800/month professional liability, and compliance-heavy spend like $2,500/month cybersecurity and $2,000/month accounting/audit. Buyer CAC is $350 in Year 1, but seller/carrier CAC is $1,500, so partner acquisition costs much more.

Setup costs

- $520,000 Year 1 payroll

- $195,000+ CAPEX

- $135,000 marketing budget

- $6,500/month office lease

Acquisition and controls

- $350 buyer CAC

- $1,500 seller/carrier CAC

- $2,500/month cybersecurity

- $2,000/month accounting/audit

Insurance agency startup cost breakdown table objective

Startup Cost Summary

This table summarizes startup CAPEX and the separate non-CAPEX cash reserve for launching a critical illness insurance agency.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Quoting Platform Development | $150,000 | Build scope, security review, and implementation time | Yes |

| Secure Server Infrastructure | $45,000 | Hosting spec, security hardening, and setup | Yes |

| CRM Customization and Integration | $40,000 | Workflow complexity and system integrations | Yes |

| Office Furniture and Layout | $30,000 | Office buildout and workspace needs | Yes |

| Computers and Hardware | $25,000 | Workstation count and device spec | Yes |

| Operating Cash Reserve | $478,000 | Month 7 cash trough from Year 1 payroll, fixed overhead, and launch marketing | No |

Critical Illness Insurance Agency Core Five Startup Costs

Licensing And Compliance Startup Expense

State license setup

Licensing and compliance is a state-by-state cost, not a fixed number. One-time launch fees can include producer exam fees, pre-licensing education, background checks, and agency or entity registration where required. For health-related supplemental coverage, add state filing and training rules, then budget renewals and continuing education after launch.

What to budget

Build this cost from state fee schedules, the number of licensed producers, and each state’s renewal cycle. If you sell in more than one state, add multistate licensing, extra appointments, and more compliance tracking. The model should separate one-time pre-opening fees from the recurring load so launch cash does not mask Year 1 overhead.

- Count each licensed producer

- Track each state’s renewal date

- Price CE setup by jurisdiction

Keep it lean

Start in one state if you can, then add others only when sales justify the extra filings and renewals. Set one compliance calendar, buy pre-licensing and CE only once per needed license, and avoid paying for multistate setup before demand exists. The mistake is treating renewals as optional; they’re a recurring operating cost.

- Renew early, not late

- Centralize CE tracking

- Delay extra states until needed

Recurring compliance load

Use the model’s Year 1 licensing and compliance per policy assumption of 30% as the ongoing policy-level cost. That keeps renewals, continuing education, and state-specific upkeep inside unit economics. If you sell outside one state, layer each extra state’s license and renewal timing into the forecast before you scale.

E&O, Carrier Appointment, And Professional Setup Startup Expense

Fixed setup load

This startup line is mostly fixed overhead. At $1,800/month for professional liability insurance (E&O) and $2,000/month for accounting and audit services, Year 1 hits $45,600 before carrier work. Carrier appointments may have no direct fee, but paperwork, training, compliance checks, and system setup still burn cash and founder time.

What it covers

This budget covers legal and entity setup, contracting paperwork, compliance review, and commission administration readiness. To size it, use months of coverage, number of carriers, state count, and document volume. The appointment fee may be zero, but the setup work still belongs in startup cash, not in vague overhead.

- Count active carrier contracts.

- Track state filing needs.

- Price onboarding labor.

Keep it lean

Sequence the work: entity setup first, then compliance review, then carrier appointments, then commission admin. Don’t overbuy appointments before your sales process is ready. The biggest savings come from fewer rework loops, cleaner templates, and one accounting stack from day one.

- Use one contract checklist.

- Standardize onboarding steps.

- Review commission rules early.

Year 1 carrier mix

The Year 1 carrier mix is modeled at 600% national carriers, 300% regional mutuals, and 100% niche providers, so launch work will be broad and document-heavy. More carriers means more training, compliance checks, and commission admin rules. Fewer appointments cut setup time, but they also narrow product choice.

Technology Stack Startup Expense

CAPEX vs SaaS

For this startup, split capitalized assets from monthly software. The disclosed tech CAPEX is $150,000 for quoting platform development plus $45,000 for secure server infrastructure. That $195,000 sits up front, while cloud tools stay in operating spend. Keep data privacy, access controls, and audit trails in scope because medical and financial records are sensitive.

Monthly software load

The recurring tech stack is $4,300/month: $1,200 cloud CRM, $2,500 cybersecurity and data protection, and $600 telecommunications and internet. That totals $51,600/year before e-signature, secure document storage, website, and email if those are not bundled. Here’s the quick math: monthly tools are the burn you carry while policies are still ramping.

Core agency tools

Budget the stack around the workflow: CRM for lead tracking, quoting and enrollment tools, e-signature, secure document storage, phone system, website, and email. The estimate needs vendor quotes, user counts, storage needs, and contract length. If one platform bundles three functions, compare the full monthly fee against separate tools so you do not pay twice for the same process.

Security first

Do not skimp on controls to save a few hundred dollars. For an insurance agency, weak access control or poor audit trails can create real compliance pain, especially with diagnosis-related data. Use role-based access, encrypted storage, strong password rules, and documented logs from day one. The clean rule: if a vendor cannot show how it protects sensitive data, it is the wrong vendor.

Office And Physical Setup Startup Expense

Office Choice

Office choice changes cash burn fast. A disclosed lease of $6,500/month is $78,000/year, so a storefront can burn cash before commissions ramp. A home-based start lowers lease exposure, while a shared office sits in the middle. Don’t pay for retail frontage unless walk-in traffic clearly drives sales.

Build-Out Budget

Physical CAPEX should cover computers, monitors, phones, furniture, signage, layout, meeting space, and security devices. Office furniture and layout are listed as CAPEX, but the amount is not provided, so get a quote or user input before budgeting. Keep this separate from rent and monthly software.

Home Office Controls

A home-based launch can cut lease burn, but it still needs client privacy, secure document handling, and a professional meeting option. Use locked storage, separate work files, and a quiet space for calls and reviews. If those controls fail, the savings from skipping rent can get wiped out by trust and compliance problems.

Space Mix

A shared office can work if you need client meetings without a full lease, but it still adds fixed cost. A storefront only makes sense when the location itself brings sales. For a commission-driven agency, the cheapest safe setup is usually the one that protects documents, keeps meetings professional, and avoids locking in $6,500/month too early.

Client Acquisition And Launch Marketing Startup Expense

Launch Budget

Marketing is a working-capital expense, not CAPEX. For Year 1, the buyer budget is $120,000 and the seller/carrier budget is $15,000, so cash leaves before commission income arrives. One line: budget for lead flow first, then for closed policies.

Buyer Acquisition

Here’s the quick math: $120,000 at $350 CAC supports about 343 buyer policies ($120,000 ÷ $350). That budget covers the website, local SEO, compliant advertising, paid lead tests, referral partnerships, sales materials, review management, and launch campaigns. Use monthly spend and booked-call counts to keep the model honest.

- Track cost per booked call.

- Track cost per policy.

- Cut weak channels fast.

Lead Learning Cost

Paid leads that do not convert should sit in learning cost, not hidden revenue. That means you still count the spend, even when the lead quality is poor, because the miss tells you which message, audience, or zip code is off. The stated mix should be checked, since it reads 400% young families, 300% self employed, and 300% mortgage holders.

Carrier Acquisition

Year 1 seller/carrier acquisition marketing is $15,000 at $1,500 CAC, which funds about 10 seller or carrier relationships. Keep this spend tight: one clean pitch, compliant materials, and simple follow-up. If a channel cannot show booked meetings or signed relationships, it is a cost, not a growth asset.

Critical illness insurance agency cost scenarios table objective

Startup cost scenarios

Costs rise fast as you add office space, licensed staff, and compliance work. Lean keeps the team small; full launch pushes payroll and lease costs much higher.

| Scenario | Lean LaunchSolo-friendly | Base LaunchAgency-ready | Full LaunchGrowth build |

|---|---|---|---|

| Launch model | Home-based with one principal agent, outsourced admin help, and core systems. | Small office launch with a core team and a steady acquisition plan. | Leased office launch with a staffed sales, compliance, and support team. |

| Typical setup | Keep office spend low and fund licensing, professional liability insurance, CRM, secure storage, and compliant marketing. | Plan for disclosed CAPEX above $195,000, $14,600 monthly fixed overhead, and Year 1 marketing of $135,000. | Plan around $520,000 Year 1 payroll plus the $6,500 monthly office lease and a larger operating stack. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $150,000 - $250,000Lowest cash need | $450,000 - $600,000Core agency build | $750,000 - $1,000,000Highest cash need |

| Best fit | Best for a solo producer who wants to launch lean and stay compliant. | Best for a compliance-ready agency that wants a balanced launch. | Best for funded growth teams that need capacity from day one. |

Planning note: These ranges use researched planning assumptions, not exact quotes. User-entered state fees, deposits, and furniture/layout can move the total.

Related Products

- Critical Illness Insurance Agency Porter's Five Forces Analysis

- Critical Illness Insurance Agency BCG Matrix

- Critical Illness Insurance Agency Business Model Canvas

- What Are The 5 Core KPIs For Critical Illness Insurance Agency?

- Critical Illness Insurance Agency Business Plan Template in Pre-Written Word

- How Increase Profits For Critical Illness Insurance Agency?

- What Are Operating Costs For Critical Illness Insurance Agency?

- Critical Illness Insurance Agency Financial Model Template in Excel

- Critical Illness Insurance Agency Owner Income: $0–$222M

- How To Start A Critical Illness Insurance Agency In 8-16 Weeks

- How To Write A Business Plan For Critical Illness Insurance Agency?

- Critical Illness Insurance Agency Marketing Mix

- Critical Illness Insurance Agency Marketing Plan

- Critical Illness Insurance Agency Business Proposal

- Critical Illness Insurance Agency PESTEL Analysis

- Critical Illness Insurance Agency Pitch Deck Example Editable PPTX

- Critical Illness Insurance Agency Business SWOT Analysis

- Critical Illness Insurance Agency Value Proposition Canvas

Frequently Asked Questions

The disclosed startup base is $195,000+ of CAPEX for the quoting platform and secure server infrastructure A staffed first operating year adds $520,000 of payroll, $175,200 of fixed overhead, and $135,000 of marketing That totals about $103 million before state fees, deposits, office furniture/layout, variable policy costs, and cash cushion