Owner income$415.1k

Owner income$415.1kHow Much Can a Cucumber Drink Owner Make on $11M Year 1 Sales

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$415.1k  Net margin78.4%

Net margin78.4% Revenue for target pay$92.8k/mo

Revenue for target pay$92.8k/mo Business difficultyMedium

Business difficultyMedium

Key Takeaways

- Sell-through drives revenue; empty shelves without reorder don't pay.

- Year 1 pricing and volume set gross sales.

- Channel deductions can erase contribution fast.

- Cash tied in inventory can block owner draws.

Owner income$415.1kNet margin78.4%Revenue for target pay$92.8k/moBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, payroll, overhead, marketing, debt service, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

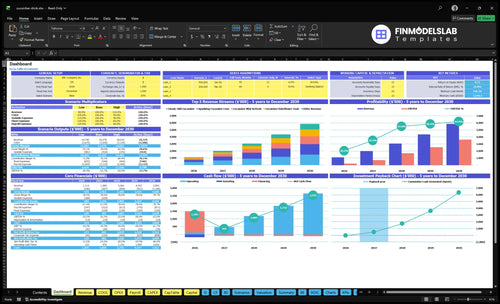

Want to check owner income in the model?

Screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Cucumber Beverage Company Financial Model Template—open the model. Charts show Year 1 revenue of $1114 million, Year 5 revenue of $58545 million, gross margin near 78%, $9,100 monthly overhead, and $110,000 founder salary.

Owner-income model highlights

- Dashboard to owner income

- SKU, COGS, cash flow

- Scenarios test pricing and volume

How many cases does a cucumber beverage company need to sell to pay the owner?

Cucumber Beverage Company needs about 166,239 units to cover fixed overhead, non-owner payroll, and a $110,000 founder salary; cases can’t be stated until units per case are defined. For the operating metrics behind this math, see What Are The 5 KPIs For Cucumber Beverage Company?.

Quick math

- 300,000 units in Year 1 model

- $1.114 million projected revenue

- $684,312 contribution after variable costs

- $2.28 contribution per unit

Owner pay test

- $109,200 fixed overhead

- $160,000 non-owner payroll

- $110,000 founder salary

- Cases = 166,239 ÷ units per case

What changes cucumber beverage company owner income the most?

For a Cucumber Beverage Company, owner income changes most when you grow sales volume without losing gross margin. Pricing, channel deductions like distributor cuts, demos, freight, and receivables, and marketing payback decide whether growth turns into cash or just more work. A lean owner-run launch keeps payroll low, but it can also cap sales execution, so the founder’s role has a direct hit on take-home pay.

Biggest income levers

- Sales volume drives top-line cash.

- Pricing lifts every unit sold.

- Gross margin keeps more per case.

- Channel costs can erase gains fast.

What shapes owner pay

- Owner-run launch saves payroll.

- Managers turn pay into payroll plus profit.

- Regional retail growth adds distributor costs.

- Broader distribution needs more inventory cash.

What profit margin does a cucumber beverage company need?

The margin target is not fixed; on the Year 1 numbers here, Cucumber Beverage Company needs about 51% gross margin just to cover variable costs, fixed overhead, and shown payroll before reserves. Here’s the quick math: $240,308 in COGS on $1.114 million sales is 78.4% gross margin, and for the KPI view see What Are The 5 KPIs For Cucumber Beverage Company?. With variable costs at 17% of revenue and fixed overhead plus payroll at $379,200, the cushion can shrink fast.

Margin math

- 78.4% Year 1 gross margin

- 17% variable cost load

- $379,200 fixed overhead plus payroll

- Floor is about 51% before reserves

Cost pressure points

- Cucumber base cost moves fast

- Glass or cans add packaging cost

- Co-packing and testing hit margin

- Cold storage, freight, and deductions bite

Want the six biggest income drivers?

1

300K-1.47MCase Volume

More cases sold lifts revenue from Year 1 to Year 5 and gives fixed overhead more room, so owner take-home can grow faster.

2

$3.50-$4.25Price Mix

A small lift in price or product mix drops straight into contribution, so pricing power matters right away.

3

75%-85%Gross Margin

Unit COGS of $0.55-$1.06 sets the gross margin, and a better mix leaves more cash after production.

4

17%-11.5%Channel Costs

Distributor, ad, and freight costs take a bigger bite early, so tighter trade terms protect operating profit.

5

8%-4.5%Ad Efficiency

Digital marketing starts heavy, so better conversion and repeat buys keep contribution from getting eaten up.

6

$1.14MCash Buffer

Minimum cash hits in Month 2, so reserves have to carry payroll and inventory before owner take-home turns on.

Cucumber Beverage Company Core Six Income Drivers

Case Volume And Sell-Through

Case Volume and Sell-Through

Real sell-through drives income, not just retail placement. If stores take cases but do not reorder, the business only ties up cash and builds fake distribution. Track units sold per month, cases sold per account, repeat orders, and stockout rate so revenue reflects what shoppers actually buy.

The forecast rises from 300,000 units in Year 1 to 1,470,000 units in Year 5. At about $228 contribution per added unit after Year 1 COGS and variable costs, each extra unit lifts profit before fixed costs, payroll, and reserves. More doors only help when they reorder.

Measure Reorders, Not Just Doors

Build a simple sell-through sheet by account: shipped cases, sold units, reorder timing, and out-of-stock days. If first orders do not turn into repeat orders, cut the weak account and shift product to faster stores.

- Track units sold each month.

- Track cases per account.

- Track repeat order rate.

- Track stockout days.

Here’s the quick math: more sold units raise gross profit, but only if inventory cash, waste, and distribution costs stay controlled. Owner pay improves when sell-through stays strong enough to fund reserves and a draw.

1

Pricing And Package Format

Pricing And Pack Mix

Pricing and package mix move owner pay before any cost cuts. Year 1 list prices range from $350 to $425 per unit, with a blended price near $371; Year 5 ranges from $370 to $445. A $0.10 price change on 300,000 units shifts gross sales by $30,000 before channel costs.

Bottles, cans, single-serve packs, multipacks, wholesale, and direct sales all change realized revenue. Higher pricing only works if velocity holds and channel deductions do not rise. The risk is premium packaging without enough repeat demand; that can lift invoice sales but leave cash for owner draws unchanged.

Track Net Price Per Unit

Track realized price per unit by channel, plus sell-through and repeat orders. Compare net revenue on bottles, cans, multipacks, wholesale, and direct sales, not just list price. If a small price step slows reorders, the extra gross sales can vanish fast.

Test price and pack changes in short runs, then watch velocity (sell-through rate), deduction rate, and cash collected. The best mix is the one that keeps units moving and protects margin. If premium packs need heavy discounting to clear, they reduce operating cash and owner income.

2

Gross Margin And Product Cost

Gross Margin And Product Cost

If drinks sell but COGS stays high, the owner feels it fast. Year 1 shows $240,308 of COGS on $1.114 million of sales, or about 21.6%; some products still run at 30% to 42% of revenue. That margin is the cash cushion that pays payroll, rent, and owner draw.

Unit cost comes from ingredient cost, bottle or can cost, co-packing fee, testing, waste, and batch size. Here, unit COGS ranges from $0.55 to $1.06, so premium packaging and small-batch runs can compress profit quickly. When gross margin slips, owner pay drops dollar for dollar after fixed costs.

Track COGS By SKU Weekly

Measure gross margin by SKU, not just by the full line. Tie each production run to actual yield, waste, and pack cost so you can see which bottle or can format is draining cash. If batch size gets too small, per-unit cost rises and the owner’s draw gets squeezed.

Use a simple run sheet to control this driver:

- Ingredient cost per batch

- Pack cost per unit

- Co-packing fee per unit

- Testing and waste loss rate

- Gross margin by SKU

If one premium flavor lands near the 42% cost mark, it needs a higher price or a tighter run size. Otherwise, the margin leak shows up in lower profit and less cash for the owner.

3

Distributor And Trade Costs

Distributor And Trade Costs

Channel costs turn gross sales into cash. In Year 1, 50% distributor commission and 40% freight leave only 10% of invoice sales before trade spend. That trade spend includes retailer allowances, promotional discounts, slotting, and chargebacks, and it must be tracked separately from list price. One clean rule: net revenue, not invoice sales, pays the owner.

By Year 5, commission falls to 40% and freight to 30%, so the deduction load eases to 70% before trade spend. On a Year 1 base of $1,114,000, each 1% equals $11,140 before taxes and reserves. That means small changes in deductions can move owner pay fast, even if unit volume looks strong.

Track Net Revenue Waterfall

Build the forecast from the bottom up: list price, less distributor commission, less freight, less trade spend, equals net revenue. Here’s the quick math: if a deduction grows by 1% of Year 1 revenue, the owner gives up $11,140 before overhead. If deductions are rising faster than sales, don’t chase more doors until you know the margin by account.

Track these inputs each month:

- Net revenue by SKU

- Distributor commission rate

- Freight per case

- Trade spend by account

- Chargebacks and allowances

What this hides: high placement can still hurt cash if slotting and promo discounts eat the contribution. The owner should approve new accounts only when the post-deduction margin still covers fixed costs and a realistic draw.

4

Marketing Efficiency And Repeat Purchase

Marketing Efficiency And Repeat Purchase

Marketing has to buy repeat sales, not just first looks. In Year 1, digital ads drive 80% of revenue, so demos, sampling, influencer content, retail merchandising, and ads must create trial and then reorder; otherwise the owner pays for attention that never turns into cash.

Here’s the quick math: cutting wasted Year 1 marketing by 1% of revenue frees $11,140, but only if sales velocity holds. The real test is whether store-level demand and repeat buying stay high enough to cover acquisition spend before fixed costs and owner draw.

Track Trial To Reorder

Measure cost per trial, repeat rate, revenue per store, and payback period by channel. A campaign is working only if it gets a second purchase fast enough to beat the reorder cycle; if not, it is just expensive awareness.

- Track trial by store and channel.

- Link ads to reorder rate.

- Cut spend with slow payback.

- Shift budget to high-repeat stores.

By Year 5, digital ads still drive 45% of revenue, so this is not just a launch issue. If repeat purchase proves out, marketing can scale profit and owner pay; if it does not, every extra dollar spent on sampling and merch andising drags cash flow.

5

Cash Flow And Inventory Reserves

Cash Flow And Inventory Reserves

Owner pay here depends on cash, not just profit. Year 1 shows $305,112 operating profit after shown costs, but inventory builds, production deposits, receivables, spoilage, and growth reserves can still block draws. Working capital means cash tied up in inventory and receivables. If retailer payments lag, the business can look profitable and still feel tight on cash.

Here’s the risk: scaling toward $58.545 million in Year 5 without funding working capital can keep owner income flat even as profit rises. Track months of inventory, production minimums, accounts receivable days, waste allowance, and the reserve balance. If any of those stretch, cash gets trapped before it reaches the owner.

Track Working Capital Weekly

Measure cash conversion, not just sales. Start with forecast units, then model inventory on hand, supplier deposit timing, and retailer collection days. A simple rule: if inventory grows faster than sell-through, owner draws should pause until the reserve rebuilds. That keeps the business from funding growth with unpaid stock.

- Track months of inventory.

- Track accounts receivable days.

- Set production minimums.

- Set waste allowance.

- Protect the reserve balance.

Use the reserve balance as a guardrail. If cash falls below the amount needed for the next production run plus expected receivables lag, distributions should wait. That choice protects owner income later, because running out of cash forces emergency financing or slower replenishment, both of which hit take-home pay.

6

Compare lean, base, and high-growth owner income scenarios

Owner income scenarios

Owner pay moves with volume and margin, but taxes, reserves, debt, and hiring can cut the founder's take-home fast.

| Scenario | Low CaseLaunch case | Base CaseGrowth case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the launch case with owner pay anchored to Year 1. | This is the modeled growth case with owner pay tied to Year 3 scale. | This is the stronger earnings path with owner pay tied to Year 5 scale. |

| Typical setup | Year 1 runs at 300,000 units and $1.114M revenue, with $229k EBITDA before taxes and reserves. | Year 3 reaches 795,000 units and $3.065M revenue, and variable-cost rates are still editable because Year 3 percentages are not fully provided. | Year 5 reaches 1.47M units and $5.855M revenue, with $3.629M EBITDA before taxes, reserves, and debt. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $110k - $229kLaunch pay | $701k - $1.69MModeled scale | $2.55M - $3.63MScale upside |

| Best fit | Founders stress-testing the first operating year and a tight cash stance. | Operators planning regional growth and a fuller sales setup. | Teams planning broader distribution and testing the upper end of owner take-home. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or cash distributions.

Related Products

- Cucumber Beverage Company Porter's Five Forces Analysis

- Cucumber Beverage Company BCG Matrix

- Cucumber Beverage Company Business Model Canvas

- What Are The 5 KPIs For Cucumber Beverage Company?

- Cucumber Beverage Company Business Plan Template in Pre-Written Word

- How Increase Cucumber Beverage Company Profits?

- What Are Cucumber Beverage Company Operating Costs?

- How Much It Costs To Start A Cucumber Beverage Company: $140K+ Plan

- Cucumber Beverage Company Financial Model Template in Excel

- How To Start A Cucumber Beverage Company In 4 To 9 Months

- How To Write A Business Plan For Cucumber Beverage Company?

- Cucumber Beverage Company Marketing Mix

- Cucumber Beverage Company Marketing Plan

- Cucumber Beverage Company Business Proposal

- Cucumber Beverage Company PESTEL Analysis

- Cucumber Beverage Company Pitch Deck Example Editable PPTX

- Cucumber Beverage Company Business SWOT Analysis

- Cucumber Beverage Company Value Proposition Canvas

Frequently Asked Questions

In the provided Year 1 model, the founder salary is $110,000, and operating profit after shown costs is $305,112 before taxes, debt, investor distributions, and reserves That creates a $415,112 pre-tax planning ceiling if all profit were distributed Real take-home may be lower when inventory, receivables, and growth cash are funded