Owner income$67K

Owner income$67KHow Much Custom Embroidery Owners Make: $80K Pay Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$67K  Net margin67%

Net margin67% Revenue for target pay$1.2M

Revenue for target pay$1.2M Business difficultyHard

Business difficultyHard

You’re trying to turn stitched polos, caps, hoodies, totes, and jackets into real owner income, not just busy production days This five-year model shows $197M in Year 1 revenue, 870% gross margin, and $80K modeled owner pay, before taxes, debt payments, personal benefits, or guaranteed distributions

Owner income$67KNet margin67%Revenue for target pay$1.2MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

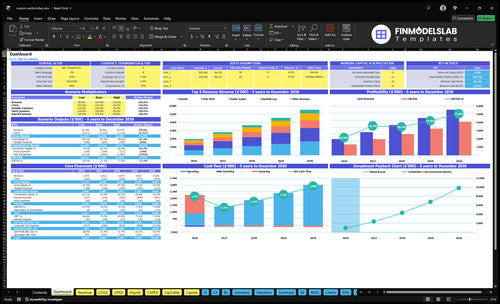

Can you check owner income in the embroidery financial model?

Dashboard shows revenue, margin, costs, reserves, and owner pay assumptions in the Custom Embroidery Service Financial Model Template—open it.

Owner-income model highlights

- Owner pay: $80K

- Year 1 revenue: $197M

- Year 3 revenue: $367M

- Gross margin: near 87%

- Scenarios: built in

Can a custom embroidery business replace a full-time income?

Yes, a Custom Embroidery Service can replace a full-time income under this model, because owner-operator pay is already set at $80,000 per year in Year 1. The key test is whether volume, pricing, and machine capacity hold; track that through What Is The Most Critical Metric To Measure The Success Of Custom Embroidery Service? before treating the income as safe.

Model Says Yes

- $80K owner pay included

- 15,500 units sold in Year 1

- $197M modeled Year 1 sales

- $135M pre-tax operating profit

Watch The Gaps

- Protect repeat business

- Keep machine uptime high

- Hold disciplined pricing

- Match capacity to orders

How much revenue does an embroidery business need to pay the owner?

If you want to pay the owner, a Custom Embroidery Service needs enough sales to cover fixed overhead, non-owner payroll, and the target owner pay first. Using the provided Year 1 numbers, the sales target is about $313K per year, or $26K per month, before reserves. That is a sales target, not net income.

Quick math

- $498K fixed overhead

- $125K non-owner payroll

- $80K owner pay

- Sales target: $313K yearly

What this means

- Cover costs before owner profit

- Monthly target is $26K

- Reserve cash comes after this

- Track sales, not just margin

Should an embroidery business owner do the stitching or hire staff?

If cash is tight, the owner should do the stitching at first; it avoids a labor bill and can protect take-home. But the model is built for hiring too: it budgets an $80K owner-operator and a $55K lead machine operator in Year 1, with lead capacity rising from 10 FTE to 15 FTE in Year 3 and 20 FTE in Year 4. That matters because output is forecast to grow from 15,500 to 34,100 units, and one person stitching will cap both sales time and turnaround.

Owner stitches first

- Saves labor in the short run

- Helps cash stay in the business

- Limits sales calls and follow-up

- Slows turnaround when orders stack up

Hire for growth

- Uses the $55K lead role in Year 1

- Supports more output per day

- Scales capacity from 10 FTE to 20 FTE

- Fits the jump from 15,500 to 34,100 units

What drives embroidery owner income?

1

15.5KOrder Volume

More units sold spread the $498K fixed overhead across more revenue, so owner take-home rises fastest with volume.

2

$127Avg Order Value

Mixing in higher-price items like hoodies and jackets lifts revenue per order without needing the same jump in unit count.

3

88.6%Gross Margin

The unit spread after direct costs is about 88.6%, and every point you keep adds straight to profit.

4

2 MachinesMachine Utilization

Keeping both machines busy matters because the same fixed shop costs only shrink when the line stays full.

5

$205KLabor Efficiency

Year 1 payroll is $205K including owner pay, so faster stitching and less rework protect take-home.

6

HighRepeat Accounts

Repeat commercial orders are a planning assumption, but they steady demand and cut selling time.

Custom Embroidery Service Core Six Income Drivers

Order Volume

Order Volume

Order volume is the number of finished units sold and shipped. In this model, Year 1 is 15,500 units, or about 1,292 per month, and Year 3 rises to 27,900 units. That volume only turns into owner income if jobs are priced right and produced cleanly; otherwise rework, rush work, and missed deadlines eat the margin.

Here’s the quick math: more units spread fixed costs like rent, software, insurance, and payroll across more sales. But weak volume leaves machines idle while those costs keep running, so profit and owner draw shrink fast. Volume without clean execution is busy work, not income.

Track clean units, not just orders

Measure shipped units, rework rate, rush orders, and labor hours per unit. The key inputs are order count, average order size, turnaround time, and available machine hours. If order flow rises but rework also rises, the extra volume can still cut take-home pay.

- Track units per month vs. 1,292 baseline.

- Watch rework and rush jobs weekly.

- Match staffing to 27,900-unit growth.

- Protect margins before taking more orders.

1

Average Order Value

Average Order Value

When average order value (AOV) rises, setup time gets spread across more items, so owner income usually improves faster than unit count alone. In this model, the mix matters: denim jackets sell at $300, hoodies at $200, and totes at $60. At 15,500 units in Year 1, a jacket-heavy mix should throw off more cash than a tote-heavy mix.

Here’s the quick math: $300 ÷ $60 = 5 totes. So one jacket order can carry the same revenue as five tote orders, before labor and stitch costs. Large school, team, event, and business orders can lift profit, but only if blank cost, digitizing, hooping, and rework stay controlled. A big order with weak pricing can still cut owner pay.

Track Ticket by Order Type

Track AOV by customer type and product mix, not just total sales. Watch blanks, labor hours, stitch complexity, and rush work on each order. If a larger order needs extra setup but the price doesn’t move, margin falls fast. The goal is to make bigger orders pay for their own labor and still leave room for the owner draw.

Set minimums and add-ons for digitizing, complex logos, and rush turnaround. Price school, team, and business jobs so the setup fee and production time are covered before volume grows. If smaller items like totes dominate the mix, revenue can look active while cash stays thin. Better AOV means fewer low-margin jobs and a cleaner path to take-home income.

2

Gross Margin And Pricing

Pricing Discipline

Gross margin here is the spread after unit cost, garment markup, and the disclosed 15% production overhead. The model shows Year 1 gross margin at 870%, so pricing has to cover setup fees, digitizing charges, stitch-count pricing, and minimums before owner pay. On $197M revenue, a 1-point margin miss is about $1.97M of pre-tax profit.

Protect Margin First

Price by order type and complexity, not just by piece count. Track gross margin by SKU, logo stitch count, rush work, and rework, then test higher minimums on small jobs that use the same setup time as larger ones. A busy-looking logo that is underpriced can still drain cash and push owner draw down.

3

Machine Utilization

Usable Machine Hours

Machine utilization is the share of paid labor time that turns into sellable embroidery, not idle time, thread swaps, hooping delays, or rework. In this model, output grows from 15,500 units in Year 1 to 34,100 units by Year 4, so every lost machine hour cuts revenue, slows cash flow, and pushes owner pay down even when payroll and rent stay fixed.

What this estimate hides: utilization drops when designs need extra hooping, thread changes, rework, or maintenance. More heads and better workflow help only if order flow stays steady. If the shop has paid labor hours but no profitable repeat work, machines look busy on paper and still fail to cover overhead.

Track Run Time, Not Just Orders

Measure usable machine hours, orders per run hour, and rework rate. Here’s the quick math: if labor is paid but the machine is stopped for setup or fixes, unit output falls and gross margin gets thinner. Track how many hours each design type needs, then price complex logos, stitch-heavy jobs, and rush work so they earn more than simple repeat runs.

Test workflow by order type: repeat logo apparel, uniforms, and team orders should fill gaps first because they need less setup and protect margin. Document maintenance downtime, hoop changes, and thread swaps weekly. If paid labor hours rise without a matching jump in finished units, owner income is leaking into idle time.

4

Labor Efficiency

Labor Efficiency

Labor efficiency is the gap between paid hours and finished units. In embroidery, that includes setup, hooping, trimming, quality checks, packaging, customer messages, and design review. Year 1 payroll is $205K, including $80K of owner pay, so every slow order or rework hit flows straight into profit and the owner’s take-home.

Unit labor is already embedded in product cost, from $100 per tote to $300 per denim jacket. If unpaid owner labor is not counted, profit can look stronger than it is. Here’s the quick test: track labor hours per finished unit, then compare that to price and job mix before you hire, discount, or promise faster turnaround.

Track Hours per Finished Unit

Measure labor by job type, not just by payroll. Split hours into setup, stitching support, rework, and customer admin, then divide by finished units. If one product line needs far more touches than the sale price supports, it is pressuring margin and cash flow even when sales look busy.

- Track hours per finished unit

- Log rework and rush orders

- Price complex jobs higher

- Count owner hours in cost

- Hire only after demand proves out

What this estimate hides is the labor drag from small orders and design changes. If labor hours rise faster than unit volume, owner pay gets squeezed first. Use the labor log to set minimums, adjust pricing, and decide when a new hire will actually improve margin instead of just adding payroll.

5

Repeat Commercial Accounts

Repeat Commercial Accounts

Repeat logo apparel, uniforms, school, team, and local business orders make revenue steadier because they spread setup time, sales effort, and digitizing work across more units. The model grows from 15,500 units in Year 1 to 27,900 units in Year 3, so recurring work helps keep gross margin and owner pay from swinging with one-off jobs.

The risk is concentration. One delayed school or business account can leave machine time idle while payroll, software, and rent still run. Repeat work only helps if reorder timing is predictable, artwork is approved once, and minimum quantities keep small jobs from becoming low-margin rush work.

Control Reorders and Turnaround

Track repeat-order rate, average reorder size, and the share of monthly units from recurring buyers. If repeat work fills more of the 1,292 monthly units, it is easier to cover $205K in Year 1 payroll, including $80K owner pay, without rush labor cutting into take-home.

Set reorder terms, artwork standards, turnaround windows, and minimum quantities before the first order ships. That keeps repeat jobs fast to place and easy to price, so they support profit instead of creating chaos when a big account needs a rush.

6

Compare lean, base, and high embroidery income scenarios

Owner income scenarios

Owner income changes with volume, payroll, and overhead as the shop moves from launch to scale. These cases show how the model shifts from lean to upside.

| Scenario | Lean CaseLean case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | Lean case uses the first-year launch model with lower owner take-home. | Base case uses the year-three operating model with steadier scale and pay. | High case uses the year-four scale-up model with the strongest owner payout path. |

| Typical setup | Year 1 assumes $197M revenue, 15,500 units, 870% gross margin, $498K fixed overhead, $205K payroll, and $80K modeled owner pay. | Year 3 assumes $367M revenue, 27,900 units, 872% gross margin, $328K payroll, and $265M pre-tax operating profit. | Year 4 assumes $455M revenue, 34,100 units, 874% gross margin, and $3,555K payroll with $336M pre-tax operating profit. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $80K modeled payLean income | $265M profit caseBase income | $336M upside caseHigh income |

| Best fit | Use this to stress-test launch cash flow and owner pay in the first operating year. | Use this as the mid-case for a more stable shop with repeat demand and fuller staffing. | Use this to test upside if volume scales faster and the shop runs near capacity. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Custom Embroidery Service Porter's Five Forces Analysis

- Custom Embroidery Service BCG Matrix

- Custom Embroidery Service Business Model Canvas

- 7 Essential Production and Sales KPIs for Custom Embroidery Service

- Custom Embroidery Service Business Plan Template in Pre-Written Word

- How to Increase Custom Embroidery Service Profitability with 7 Key Strategies

- How To Calculate Monthly Running Costs for a Custom Embroidery Service

- Custom Embroidery Service Startup Costs: $25K Machine Budget

- Custom Embroidery Financial Model Template in Excel

- How to Open a Custom Embroidery Business in 4–10 Weeks

- How to Write a Custom Embroidery Service Business Plan

- Custom Embroidery Service Marketing Mix

- Custom Embroidery Service Marketing Plan

- Custom Embroidery Service Business Proposal

- Custom Embroidery Service PESTEL Analysis

- Custom Embroidery Service Pitch Deck Example Editable PPTX

- Custom Embroidery Service Business SWOT Analysis

- Custom Embroidery Service Value Proposition Canvas

Frequently Asked Questions

Under the researched Year 1 model, the business makes $197M in revenue and about $135M in pre-tax operating profit after listed costs, including $80K modeled owner pay Gross margin is 870% after unit costs and production overhead Taxes, debt, reserves, and distributions are not included