Owner incomeUp to $1.575M

Owner incomeUp to $1.575MHow Much Dance School Owners Make: $1575M Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeUp to $1.575M  Net margin42.3%

Net margin42.3% Revenue for target pay$3.72M

Revenue for target pay$3.72M Business difficultyMedium

Business difficultyMedium

You’re not comparing teacher wages you’re planning how tuition turns into owner pay In this five-year model, EBITDA runs from $1575M in Year 1 to $36221M in Year 5 before taxes, debt payments, reserves, and owner-specific distributions Scope includes tuition, recital and workshop income, payroll, rent, marketing, software, insurance, cash reserves, and reinvestment

Owner incomeUp to $1.575MNet margin42.3%Revenue for target pay$3.72MBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to pressure-test the full Dance School model?

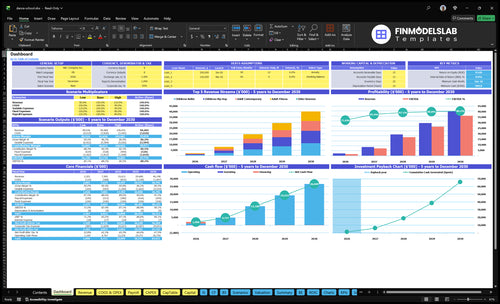

This screenshot shows revenue, EBITDA, cash, breakeven, and owner-pay outputs, plus the assumption tabs. Open the Dance School Financial Model Template.

Model highlights

- EBITDA from $1,575M to $36,221M

- Minimum cash: $910k

- Month 1 breakeven shown

- Year 1 to Year 5 ramps

- Enrollment, occupancy, tuition

- Payroll, costs, capex tests

What dance school operating costs most affect profit margin?

For a Dance School, profit margin gets hit hardest by payroll, rent, and empty class seats; for setup context, see How Much Does It Cost To Open A Dance School? The fixed overhead is $8,800 per month, led by $6,000 in studio rent, so low enrollment hurts fast. Payroll climbs from $212,500 in Year 1 to $350,000 in Year 5, while variable cost rates improve from 125% to 85%, but owner take-home still weakens when under-filled classes carry full instructor and facility cost.

Big margin drivers

- Payroll is the biggest swing cost.

- $6,000 rent anchors fixed overhead.

- Instructor bonuses raise labor cost fast.

- Music licensing adds fixed pressure too.

What squeezes profit

- Processing fees cut gross margin on each payment.

- Under-enrolled classes still carry full cost.

- 125% to 85% variable costs improve slowly.

- Year 5 payroll reaches $350,000.

Can a dance school owner make a living from one location?

Yes, a Dance School owner can make a living from one location in this model, but only if enrollment, occupancy, payroll, and rent stay on plan; track What Is The Most Important Metric To Measure The Success Of Your Dance School? because class utilization drives the answer.

Model says yes

- Year 1 EBITDA: $1575M

- Breakeven starts in Month 1

- Minimum cash need: $910k

- Before taxes, debt, reserves, distributions

Watch the levers

- Payroll is $212,500 in Year 1

- Fixed overhead is $8,800/month

- Class utilization must stay on plan

- Owner role changes take-home pay

How does the owner role change dance school income?

For a Dance School, owner-led teaching can make early income look stronger because you skip instructor payroll, but it also ties up the owner’s time and slows growth. A hired-instructor model costs more, yet it supports more classes across children’s ballet, children’s hip-hop, adult fitness, and adult contemporary. In this plan, staffing rises from 2 dance instructor FTEs in Year 1 to 5 in Year 5, so the tradeoff is take-home pay now versus enrollment growth, scheduling control, and retention.

Owner-led income

- Higher early take-home by skipping payroll

- Owner time becomes the limit

- Less room for more classes

- Works best at small scale

Hired staff growth

- Costs more upfront than owner teaching

- Supports more class types and schedules

- Staffing grows from 2 to 5 FTEs

- Helps retention with steadier coverage

What drives owner income most?

1

40%-85%Class Fill

Moving from 40% to 85% occupancy lifts revenue from the same studio hours, so more of each tuition dollar reaches owner income.

2

280-640Enrollment Volume

Total active students rise from about 280 to 640, which spreads rent and staff cost across more paid seats.

3

$120-$170Tuition Price

Monthly tuition climbs from $120 to $170, and even small price gains lift take-home across every enrolled student.

4

$213K-$350KInstructor Payroll

Staff payroll rises from about $213K to $350K a year, so wage control is key to keeping EBITDA strong.

5

$8.8K/moFacility Cost

Fixed overhead runs about $8.8K a month, and trimming it improves margin without needing more students.

6

$1.5K-$6KAdd-on Revenue

Recital tickets and workshops add $1.5K to $6K, which is clean upside after the core classes are full.

Dance School Core Six Income Drivers

Enrollment Volume

Enrollment Volume

Enrollment volume is the number of active paying students in class. It matters because each filled spot helps spread fixed rent, software, insurance, and admin costs across more accounts. In the model, total places grow from 280 in Year 1 to 640 in Year 5, while occupancy rises from 40% to 85%. That lifts paying spots from about 112 to 544.

Here’s the quick math: more paying students means more recurring tuition, but empty seats still use instructor time and studio space. So retention matters as much as new signups. If occupancy slips, owner pay gets squeezed fast because fixed costs do not fall with attendance. One clean line: filled seats drive cash flow.

Track fill, churn, and class seats

Measure enrollment by filled spots ÷ total places, then watch retention by cohort and class type. A studio can grow revenue only if new signups stay long enough to cover fixed overhead and support profit draw. Use monthly occupancy targets, waitlists, and re-enrollment rates to spot weak classes early. If one time slot stays underfilled, it is a margin leak, not just a sales issue.

- Track occupancy by class and month.

- Watch churn before each billing cycle.

- Cut empty slots or merge weak classes.

Use the Year 5 target as the planning anchor: 544 filled spots at 85% occupancy. That level gives the owner more stable tuition cash, better coverage of fixed costs, and a stronger base to pay instructors without eroding take-home income.

1

Tuition Pricing

Tuition Pricing

Average revenue per student comes from monthly tuition, class mix, registration fees, private lessons, and premium programs. The disclosed tuition range is $120-$150 in Year 1 and $140-$170 in Year 5. Children’s programs move from $140 to $160, and adult contemporary from $150 to $170.

Higher tuition improves owner income only if retention and perceived quality hold. A $10 monthly increase adds $10 × active students × 12 in annual revenue before churn, but weak retention can erase the gain fast because instructor payroll and studio time are already committed.

Price by class mix

Track tuition per program, not just one blended average. Watch registration fees, private lesson attach rate, and premium program share, because those raise revenue per student without adding many fixed costs.

- Separate kids, adult, and premium pricing.

- Test raises after fill-rate checks.

- Watch churn after every price change.

- Protect quality before pushing higher fees.

2

Class Capacity Utilization

Class Capacity Utilization

Class capacity utilization is the share of seats and billable days you actually sell. For a dance school, the same rent and instructor time earn more when occupancy moves from 40% in Year 1 to 85% in Year 5, and billable days rise from 20 to 22 per month. That is about 2.1x more filled seats from the same room.

Under-filled classes hurt margin because the instructor and studio are already committed. The key inputs are total seats, filled seats, class cap, billable days, and no-shows. If a class runs too empty, each student carries more fixed cost; if it runs too full, safety, attention, and retention can slip.

Fill Seats Without Breaking the Class

Track utilization by class, time slot, and age group. Use filled seats ÷ available seats as the core metric. Compare that to monthly tuition, because more fill at the same price lifts recurring revenue and owner draw faster than adding more weak classes.

- Watch fill rate weekly.

- Cut or merge weak classes.

- Keep caps below safety limits.

- Use waitlists before adding rooms.

3

Instructor Payroll

Instructor Payroll

Instructor payroll is the biggest staffing lever in a dance school. Year 1 staffing includes 1 studio manager, 1 lead instructor, 2 dance instructor FTEs, and 0.5 administrative assistant FTE; annual payroll starts at $212,500 and rises to $350,000 as instructor staffing reaches 5 FTEs. That is a $137,500 increase, or about 64.7%, so labor growth can outrun tuition if class fill does not keep pace.

Owner-taught classes can lift early take-home because they replace paid instructor hours. But if quality drops, retention and referrals can slip, and then payroll rises while recurring tuition stays soft. One weak hire can cut margin faster than the wage line suggests.

Control Instructor Hours

Track payroll by class, not just by month. Use instructor FTE, paid hours per class, retention, and occupancy by program to see where labor earns its keep. If a class stays thin, merge sections, shift the owner into early classes, or keep that slot closed until demand covers the wage.

Only add instructor FTEs when enrollment and repeat bookings justify the step-up. Build a monthly forecast that ties class count, fill rate, and payroll to cash flow and owner draw. Also document pay rates, prep time, and coverage rules so staffing stays tied to margin, not habit.

4

Facility Cost

Studio Overhead

Facility cost is the fixed-cost gatekeeper. This studio carries $8,800 a month in fixed overhead: $6,000 rent, $900 utilities, $350 insurance, $500 cleaning, plus software, supplies, website, and property tax. That is $105,600 a year before instructor payroll or owner pay. If enrollment does not fill the room schedule, fixed rent eats margin fast.

The $94,000 buildout for renovation, sound, lighting, mirrors, barres, furniture, security, marketing materials, and HVAC matters because it sets the cost of opening at full quality. Here’s the quick math: facility cost only works when occupancy climbs from 40% toward 85% across 280 to 640 places; otherwise the same space supports too few tuition dollars.

Match Rent to Seats

Measure monthly fixed cost per filled seat, not just total rent. Use capacity, occupancy, and billable days to see whether the schedule covers the $8,800 base. If classes stay half-full, the space still costs the same, so owner pay gets squeezed even when revenue grows. One clean rule: add space only after the current room is nearly full.

- Track occupancy by class.

- Watch fixed cost per filled seat.

- Delay expansion until seats fill.

- Test whether rent supports tuition.

If occupancy rises and the room stays safe and usable, the s ame rent produces more recurring tuition. If it doesn’t, trim space commitments before adding more overhead. Facility cost should follow enrollment capacity, not lead it.

5

Add-On Revenue

Add-On Revenue

Add-ons matter when they carry real margin. In the model, recital tickets and workshops rise from $1,500 to $6,000 per month, or $18,000 to $72,000 a year. That is a $54,000 annual swing in cash and owner profit before extra costs. Seasonal sales help, but they do not replace tuition if fixed payroll keeps running.

Count only profit, not pass-throughs. Costume or venue charges can look like revenue, but if the studio pays those costs out again, the margin is thin or zero. Here’s the quick math: add-ons improve take-home only when gross margin stays high after labor, ticketing, handling, and event costs.

Track True Margin

Track add-on sales by line: tickets, workshops, camps, intensives, private lessons, merchandise, costume handling, and competition programs. Split pass-through costs from true profit, and review margin by event before you price the next one. A $6,000 month can still underperform if the studio gives away cash on venue, staff, or costume costs.

Use a simple test: if an add-on cannot help cover fixed costs like rent and payroll, it should not drive planning. Seasonal spikes can fund cash flow, but owner pay stays safer when add-ons are forecasted separately from recurring tuition and booked only when capacity and staffing are already covered.

6

Compare low, base, and high owner-income cases from the model

Owner income scenarios

Owner income rises with occupancy, tuition, billable days, and staffing efficiency. The low, base, and high cases show how a Dance School moves from launch pressure to scaled earnings.

| Scenario | Low CaseDownside path | Base CaseCore plan | High CaseUpside path |

|---|---|---|---|

| Launch model | This is the lower-earnings path, with launch-year demand still thin and costs heavy. | This is the modeled middle path, with steadier enrollment and a more stable cost base. | This is the stronger-earnings path, where scale and fuller classes push profit harder. |

| Typical setup | Year 1 runs at 280 program places, 40% occupancy, 20 billable days, $120-$150 tuition, 125% variable cost rate, and $212,500 payroll. | Year 3 reaches 520 program places, 75% occupancy, 21 billable days, $130-$160 tuition, 104% variable cost rate, and $310,000 payroll. | Year 5 reaches 640 program places, 85% occupancy, 22 billable days, $140-$170 tuition, 85% variable cost rate, and $350,000 payroll. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $1.6MLaunch-year floor | $16.9MMid-case plan | $36.2MUpside case |

| Best fit | Use this to stress-test Month 1 cash needs, thin enrollment, and heavy launch costs before owner draws. | Best for the core operating plan and lender review, before owner take-home is reduced by reserves, taxes, debt, and reinvestment. | Use this to test what happens if classes stay full and fixed studio costs are spread over more students. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. Owner take-home comes after reserves, taxes, debt, and reinvestment.

Related Products

- Dance School Porter's Five Forces Analysis

- Dance School BCG Matrix

- Dance School Business Model Canvas

- 7 Essential KPIs to Track for Dance School Performance

- Dance School Business Plan Template in Pre-Written Word

- Increase Dance School Profitability: 7 Strategies for Margin Growth

- How to Run a Dance School: Essential Monthly Operating Costs

- Dance School Startup Costs: $94K CAPEX Plus $910K Cash Plan

- Dance School Financial Model Template in Excel

- How To Open A Dance School In 8–16 Weeks With First Classes

- How to Write a Dance School Business Plan in 7 Actionable Steps

- Dance School Marketing Mix

- Dance School Marketing Plan

- Dance School Business Proposal

- Dance School PESTEL Analysis

- Dance School Pitch Deck Example Editable PPTX

- Dance School Business SWOT Analysis

- Dance School Value Proposition Canvas

Frequently Asked Questions

In this researched model, first-year owner-pay capacity is tied to $1575M of EBITDA, not a guaranteed salary That figure is before taxes, debt payments, reserves, and distributions The same year includes 40% occupancy, 20 billable days per month, $120-$150 tuition, $212,500 payroll, and $8,800 monthly fixed overhead