Owner income$115k

Owner income$115kDaylight Harvesting Business Owner Income: $115K Pay, Month 16 Breakeven

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$115k  Net margin-48% to 32%

Net margin-48% to 32% Revenue for target pay$359k

Revenue for target pay$359k Business difficultyHard

Business difficultyHard

Key Takeaways

- Booked projects drive revenue only when crews can deliver.

- Bigger scopes raise revenue but also labor and cash risk.

- Margin improves when hardware, freight, and trips stay controlled.

- Maintenance steadies cash, but installation still pays the bills.

Owner income$115kNet margin-48% to 32%Revenue for target pay$359kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

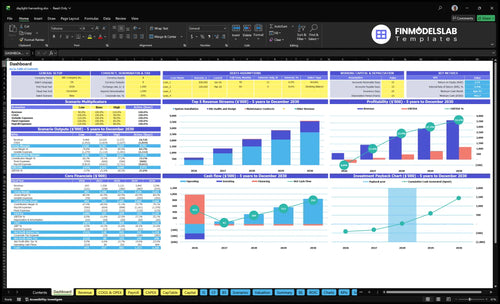

How do you check owner income in the Daylight Harvesting System Installation model?

This screenshot in the Daylight Harvesting System Installation Financial Model Template shows revenue, EBITDA, breakeven month, minimum cash, payback, and owner pay assumptions. Open the model.

Owner-income model highlights

- Owner pay scenarios

- Revenue growth and margin

- Payroll scale and cash low

Can a daylight harvesting installation business owner make more by hiring crews?

Yes, Daylight Harvesting System Installation can make more by hiring crews, but only if backlog, margin, cash flow, and quality control can carry the payroll. In the model, field techs grow from 2 FTE at $130k total salary in Year 1 to 6 FTE at $390k in Year 5, while project managers rise from 1 FTE at $75k to 3 FTE at $225k; revenue climbs from $603k to $3.596M and EBITDA improves from -$290k to $1.155M. The catch is cash strain: breakeven lands at Month 16 and minimum cash need is $443k, so hiring too early just turns owner income into payroll risk.

When hiring helps

- 2 to 6 field tech FTEs

- 1 to 3 project managers

- Revenue scales to $3.596M

- EBITDA reaches $1.155M

What can break it

- Breakeven comes at Month 16

- Minimum cash need is $443k

- Early hiring raises payroll risk

- Quality control must keep pace

How much revenue does a daylight harvesting business need to pay the owner?

Daylight Harvesting System Installation needs about $905k in revenue to cover a $115k owner role if you treat it as general manager payroll. Year 1 payroll, fixed overhead, and marketing total about $642k—$485k payroll, $133k fixed overhead, and $24k marketing—so $603k of Year 1 revenue still needs outside cash; Year 2 at $1.358M clears breakeven and supports about $157k EBITDA (earnings before interest, taxes, depreciation, and amortization) before taxes and reserves.

Year 1 gap

- $603k revenue in Year 1

- $642k total pay, overhead, marketing

- $905k rough breakeven revenue

- Outside cash is still needed

Year 2 payoff

- $1.358M Year 2 revenue

- Clears breakeven in the model

- Supports about $157k EBITDA

- Leaves room for taxes and reserves

How much does a daylight harvesting installation business owner make?

A Daylight Harvesting System Installation business owner makes a planned $115,000 owner-manager salary in Year 1 in the researched model, but no extra profit-supported distribution because EBITDA is -$290,000. For startup planning details, see How To Launch Daylight Harvesting System Installation Business?.

Owner pay

- $115,000 planned Year 1 salary

- $0 profit-supported Year 1 distribution

- -$290,000 Year 1 EBITDA

- Sales role can replace paid labor

Profit path

- Revenue: $603,000 in Year 1

- Revenue: $1.358 million in Year 2

- Revenue: $3.596 million in Year 5

- EBITDA reaches $1.155 million in Year 5

Want the six levers that move owner income?

1

$603K-$3.6MProject Volume

More signed jobs drive the jump from $603K in Year 1 to $3.6M in Year 5, and that scale is what gets the model to Month 16 breakeven with $443K minimum cash.

2

71%-76%Gross Margin

Gross margin moves from about 71% to 76%, which is the cleanest path from -$290K EBITDA to $1.155M by Year 5.

3

$95-$170/hrContract Value

Shifting more work toward higher-rate design and maintenance hours lifts revenue per project without needing the same jump in field headcount.

4

80-100hLabor Efficiency

Keeping installation and commissioning hours tight protects the spread between billed work and payroll as project load rises.

5

$1.2K-$1.0KChannel Mix

Lower CAC, from $1,200 to $1,000, matters because better-fit channels bring in more profitable project types and save cash before payback.

6

15%-55%Maintenance Revenue

Recurring maintenance grows from 15% to 55% of the mix and stabilizes cash, but it stays secondary unless you build it on purpose.

Daylight Harvesting System Installation Core Six Income Drivers

Project Volume And Qualified Demand

Qualified Project Volume

More completed daylight harvesting installs raise owner income only when crews, commissioning capacity, and cash flow can keep pace. Here’s the quick math: marketing rises from $24k to $60k, CAC improves from $1,200 to $1,000, and acquired customers move from 20 in Year 1 to 60 in Year 5. That supports revenue growth, but only if gross margin holds and Month 16 breakeven is real.

What this estimate hides is the pipeline trap: leads don’t pay bills. Owner draw improves only after booked site audits, signed installation scopes, and paid maintenance work convert demand into finished jobs. If the team can’t install, calibrate, and collect fast enough, extra demand just adds backlog and working-capital strain.

Track Booked Work, Not Leads

Measure site audits booked, scope-to-install close rate, and days to cash collection each month. Tie the marketing budget to booked audits, not raw inquiries, so the funnel stays real. If audit volume rises but signed scopes do not, cut spend or tighten qualification before labor and freight costs expand.

Also track crew load and commissioning hours against planned installs. The goal is simple: more completed projects with no margin leak. If gross margin stays intact, higher project volume should lift owner pay after breakeven; if not, the extra revenue will be swallowed by overtime, callbacks, and delayed payment.

1

Average Contract Value And Scope Mix

Average Contract Value And Scope Mix

When a job adds more zones, sensors, controllers, design, programming, and building-controls integration, average contract value rises and the owner earns more per site. Here’s the quick math: installation billing moves from $7,600 in Year 1, based on 80 hours × $95/hour, to $11,500 in Year 5, based on 100 hours × $115/hour. That is a 51% lift in install revenue before overhead.

Scope mix also changes cash flow. Site audit billing rises from $1,800 to $2,040 per audit, and maintenance from $480 to $560 per visit. Bigger jobs can improve gross profit, but they also bring change orders, slower collections, and more working capital tied up before the owner can pay themselves.

Track Scope Before You Price It

Measure revenue per project, hours per job, and change-order rate on every install. If the scope gets larger, price the extra design, programming, and integration work up front. A clean scope sheet should name the zones, sensors, controllers, and controls handoff, so the estimate matches the labor actually used.

- Track billed hours versus planned hours.

- Separate audit, install, and maintenance rates.

- Preprice building-controls integration work.

- Invoice deposits on larger projects.

- Watch days sales outstanding closely.

The owner does best when bigger contracts lift margin without stretching cash. If unbilled labor or slow pay pushes collections past 30 to 45 days, take-home income gets squeezed even when revenue looks strong. Quote the full scope, document exclusions, and bill change work fast.

2

Gross Margin Across Equipment And Labor

Equipment And Labor Margin

This driver is the gap between what a daylight harvesting job bills and what sensors, controllers, wiring, lifts, subcontracted electrical work, freight, and sales travel really cost. The source model shows direct and variable cost load easing from 290% of revenue in Year 1 to 242% in Year 5, with contribution margin moving from 710% to 758%. That gap is what funds owner pay after overhead.

What this estimate hides is fixed cost pressure. Fixed overhead is separate and includes $111k monthly rent, software, insurance, fleet, utilities, and admin. So if takeoffs miss hardware, subcontractor hours, or unpaid commissioning trips, gross margin falls first and owner draw follows. One unpaid site revisit can wipe out the profit on a small job.

Tighten Job Costing

Track every job by line item: quoted vs. actual hardware, lift time, freight, travel, and subcontracted electrical labor. Use the takeoff to set the markup, then compare it to the closeout sheet before you book revenue. Here’s the quick math: if freight or commissioning travel slips through, the owner eats it, not the customer.

Improve margin by controlling the leakage points: poor takeoffs, weak hardware markup, unmanaged subcontractor hours, missed freight, and unpaid commissioning trips. Use one checklist per project, and require billing for every return trip. That protects gross profit, smooths cash flow, and leaves more room for owner pay after fixed overhead.

- Match quote to takeoff.

- Recover freight and travel.

- Cap subcontract labor hours.

- Bill commissioning visits.

3

Labor Productivity And Commissioning Accuracy

Labor Productivity and Commissioning Accuracy

Labor productivity drives owner pay because installation work is billed by the hour, and commissioning—the final test-and-calibrate step—is where rework shows up. Year 1 uses 80 installation hours per job at $95/hour for $7,600 of billed labor; Year 5 rises to 100 hours at $115/hour, or $11,500. Every unbilled trip, bad zone layout, or sensor error cuts EBITDA before the owner can take a draw.

Track Hours, Rework, and Callback Cost

Price to the real labor load, not the clean install estimate. Keep a job log for site audit hours at 12, installation hours, and maintenance hours at 4, then separate paid work from unpaid troubleshooting. If 10 hours on a Year 5 job go unpaid, that is $1,150 of lost billings at $115/hour. Watch for bad site assessment, wrong zoning, sensor placement errors, calibration delays, programming issues, and warranty callbacks.

4

Sales Channel And Project Type

Project Type And Sales Channel Mix

Sales channel and project type decide whether a daylight harvesting job is profitable or just busy. Direct facility owner retrofits usually pay better and close faster, while general contractor, energy-service-company, utility rebate, and new construction work can add volume but squeeze margin and delay cash.

The key inputs are lead cost, CAC, commissions, travel, payment terms, and project mix. With sales commissions and travel at 50% of revenue each year and CAC improving from $1,200 to $1,000, channel choice only helps owner income if collections stay quick; long terms can deepen the $443k cash low point.

Track Cash, Not Just Wins

Measure each channel by gross margin, days to cash, and CAC, not just signed revenue. If a project type needs more coordination, rebate paperwork, or subcontracted bidding, it should earn a higher price or a smaller share of the funnel.

- Track CAC by source.

- Track days from bid to cash.

- Price slower-paying work higher.

- Prefer direct owner retrofits.

- Limit rebate-heavy pipeline exposure.

Build the forecast by project type: expected price, commission, travel, and payment timing. If a channel stretches receivables, it ties up cash and can block owner pay even when booked work looks healthy. One slow-paying job can cost more than two fast ones.

5

Maintenance Revenue And Recalibration Work

Maintenance Revenue And Recalibration Work

If install work is lumpy, service keeps cash coming in. Each modeled maintenance visit is 4 hours, billed at $120/hour in Year 1 and $140/hour in Year 5, so gross billings run $480 to $560 per visit. The work can include sensor recalibration, troubleshooting, post-installation commissioning support, and controls audits.

The model assumes maintenance contracts attach to 150% of customers in Year 1 and 550% by Year 5, so recurring work can smooth owner pay between projects. Still, installation stays the main revenue engine unless the service base is built on purpose. What this hides: unpaid callbacks, travel, and lift time can turn good billing into thin profit.

Track Service Attach And Billable Hours

Track paid service hours, contract attach rate, and callback rate. That shows whether maintenance is real revenue or just free labor. Price extra trips separately, and define what counts as billable recalibration versus warranty support so gross margin and owner draw stay clean.

- Price 4-hour visits as fixed scopes.

- Quote audits with every install.

- Flag any unpaid repeat trip.

If paid hours rise but callbacks rise faster, the owner feels it fast in cash flow. The fix is tighter scope notes, faster scheduling, and clear handoff docs from install to service.

6

Compare lean, base, and mature owner income scenarios

Owner income scenarios

Owner income rises as installation volume, maintenance mix, and pricing improve, while payroll and direct costs stay controlled. The low case is cash-tight, the base case is profitable, and the high case scales recurring work.

| Scenario | Low CaseCash strain | Base CaseProfit build | High CaseScale upside |

|---|---|---|---|

| Launch model | This is the lean case, where owner pay is tight and depends on funded operating cash. | This is the modeled case, where owner income is supported by steady profit and more recurring work. | This is the stronger earnings path, where owner income benefits from larger scale and recurring contracts. |

| Typical setup | Year 1 lands at $603k revenue and -$290k EBITDA, with $24k marketing, $485k payroll, and a mix led by site audits and design. | Year 3 reaches $2.121M revenue and $478k EBITDA, with $48k marketing, $732.5k payroll, and a stronger installation and maintenance mix. | Year 5 reaches $3.596M revenue and $1.155M EBITDA, with $60k marketing, $1.06M payroll, and 55% maintenance contracts. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $115kFunding risk | $115k - $478kCore plan | $478k - $1.155MGrowth upside |

| Best fit | Use this to stress-test cash strain and owner-pay deferral. | Use this as the main operating case for planning and hiring. | Use this to test upside if the business wins more recurring service work. |

Planning note: These scenario ranges are researched planning assumptions from the model, not guaranteed earnings, salary promises, tax advice, or cash distributions.

Related Products

- Daylight Harvesting System Installation Porter's Five Forces Analysis

- Daylight Harvesting System Installation BCG Matrix

- Daylight Harvesting System Installation Business Model Canvas

- What 5 KPIs Should Daylight Harvesting System Installation Business Track?

- Daylight Harvesting System Installation Business Plan Template in Pre-Written Word

- How Increase Daylight Harvesting System Installation Profits?

- What Are Operating Costs For Daylight Harvesting System Installation?

- Daylight Harvesting Installation Startup Costs: $196k CAPEX Plus Cash

- Daylight Harvesting System Installation Financial Model Template in Excel

- Launch a Daylight Harvesting Installer in 60–120 Days

- How To Write A Business Plan For Daylight Harvesting System Installation?

- Daylight Harvesting System Installation Marketing Mix

- Daylight Harvesting System Installation Marketing Plan

- Daylight Harvesting System Installation Business Proposal

- Daylight Harvesting System Installation PESTEL Analysis

- Daylight Harvesting System Installation Pitch Deck Example Editable PPTX

- Daylight Harvesting System Installation Business SWOT Analysis

- Daylight Harvesting System Installation Value Proposition Canvas

Frequently Asked Questions

The researched model supports a $115k general manager salary, but Year 1 EBITDA is -$290k, so extra take-home is not profit-funded EBITDA turns positive at $157k in Year 2 and reaches $1155M in Year 5 before taxes, debt service, reserves, and reinvestment