Owner income$3.1M

Owner income$3.1MDense Phase Pneumatic Conveying Owner Income: $39M Base Case

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$3.1M  Net margin49%

Net margin49% Revenue for target pay$6.4M

Revenue for target pay$6.4M Business difficultyMedium

Business difficultyMedium

A pneumatic conveying business owner can make meaningful money, but it’s not a fixed salary or guaranteed distribution Using the researched assumptions, the first-year model shows $637 million in revenue, a 704% gross margin, and about $392 million in pre-tax operating profit before debt, taxes, and additional reinvestment By the mature-year scenario, revenue reaches $2803 million and operating profit reaches about $2070 million What this estimate hides is cash timing, retainage, warranty work, and how much the owner keeps inside the company

Owner income$3.1MNet margin49%Revenue for target pay$6.4MBusiness difficultyMediumWant to test your owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Not guaranteed salary, tax advice, lender advice, or owner distribution advice.

How does the model show owner income?

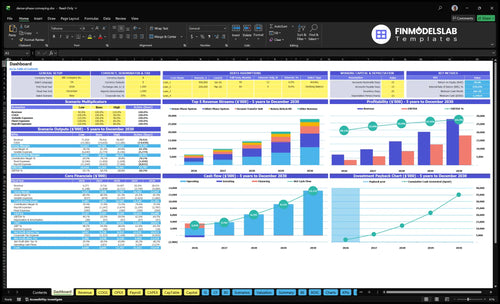

This dashboard in the Dense Phase Pneumatic Conveying Systems Financial Model Template shows revenue, margin, costs, reserves, and take-home assumptions. Open it.

Owner-income model highlights

- Owner income: take-home output

- $637M revenue: unit build

- $956k reserve: scenario logic

How much revenue can a dense phase conveying company make?

A dense phase conveying company can scale from about $637M in year 1 to $972M, $1.446B, $2.034B, and $2.803B in the mature year. That is revenue, not profit or owner income; the real swing factor is whether quoting quality and execution control turn bids into cash. Dense phase systems run from $345k to $3.883M each, while dilute systems run from $185k to $2.082M.

Revenue scale

- $637M in year 1 revenue

- $972M in year 2 revenue

- $1.446B in year 3 revenue

- $2.803B mature-year revenue

Revenue drivers

- Dense phase units: $345k-$3.883M each

- Dilute systems: $185k-$2.082M each

- Unit volume rises from 102 to 373

- Cash depends on quoting and execution

What are typical margins for pneumatic conveying installation?

Typical margins in this model run very high on paper: 704% in year one and 759% in the mature year, with $469k unit COGS per dense phase system plus revenue-based COGS, external engineering, and install labor shaping the spread. If you also want the build-cost side, see How Much To Start Dense Phase Pneumatic Conveying Systems?

Cost drivers

- $469k unit COGS

- 60% revenue-based COGS

- Engineering drops 40% to 20%

- Install labor drops 60% to 40%

Margin risks

- Delays push cash out

- Controls scope can expand fast

- Freight eats the spread

- Commissioning rework hurts profit

How much revenue does a pneumatic conveying business need to pay the owner?

For How Do I Start Dense Phase Pneumatic Conveying Systems Business?, owner pay should come from profit, not top-line sales; under the provided first-year mix, $637M revenue produces $449M gross profit and $392M operating profit after fixed overhead and General Manager payroll.

Quick Math

- Start with $637M annual revenue

- Subtract $86.595M unit COGS

- Gross profit lands at $449M

- Operating profit reaches $392M

Owner Pay Rule

- Add required cash reserves first

- Cover debt service before distributions

- Set aside taxes before owner draws

- Fund reinvestment before extra pay

What drives owner income the most?

1

$345KProject Mix

A $345K dense phase ticket drives most of the gross profit, so mix shifts toward bigger installs lift owner income fast.

2

70.4%Margin Control

At 70.4% gross margin on the dense phase system, every point of cost slippage hits take-home hard.

3

$6.37MSales Pipeline

Year 1 revenue of $6.37M only turns into cash if bids keep closing and projects keep moving.

4

$390KCapacity Build

The $390K fixed overhead, plus the $175K general manager seat, means idle engineering or install time burns cash fast.

5

45-150Parts Revenue

Rotary airlock kits rise from 45 to 150 units, and dust modules from 15 to 60, which adds steadier add-on revenue.

6

15%Warranty Reserve

A 15% reserve protects cash from claims and rework, but too much tied-up working capital slows growth.

Dense Phase Pneumatic Conveying Systems Core Six Income Drivers

Project Size And Mix

Project Size and Mix

If you sell larger engineered systems and more dense-phase jobs, revenue per project rises fast. In the model, dense-phase units are priced at $345k each, and the first-year mix shows 6 units tied to $207M, while dilute systems show 12 units tied to $222M. The real driver is not just unit count; it’s which system type, how much controls integration is included, and who the customer is.

That mix can lift owner income, but bigger jobs also trap cash longer. Larger projects usually mean higher deposits, more freight exposure, and more money tied up before commissioning. If a project slips, the owner feels it in slower cash conversion, higher working capital needs, and delayed profit draw. One clean rule: bigger revenue only helps if margin and billing pace keep up.

Raise Revenue per Project

Track average project value, dense-phase share, controls adders, deposit timing, and days from order to commissioning. The inputs that matter most are system type, number of lines, customer segment, and how much engineering and installation are bundled into the job.

- Price multi-line work separately.

- Bill deposits before fabrication starts.

- Watch freight and commissioning timing.

- Favor higher-value industrial customers.

Here’s the quick math: when a job moves from a simple dilute package to a larger engineered build, revenue per contract rises, but so does execution risk. If cash is stuck in materials, freight, and field work for too long, owner pay gets squeezed even when sales look strong. Measure project mix by gross invoice value, not just unit count.

1

Gross Margin Control

Gross Margin Control

Gross margin is what’s left after direct project costs, before overhead and owner distributions. The model shows 704% first-year gross margin after $86,595k unit COGS, 60% revenue-based COGS, and 100% variable engineering plus installation costs, so small estimating misses can hit owner pay fast.

For dense phase jobs, the cost stack is real: $12k high-pressure blowers, $185k custom pressure vessel, $64k controls, $42k valves, and $58k oversized freight. One missed change order or rework loop can wipe out the spread that funds overhead and the owner’s draw.

Track Job Margin Before You Book It

Quote every job from the same cost base: materials, engineering hours, install labor, freight, and rework. Here’s the quick math: project gross margin = price minus direct project costs. If custom controls or oversized freight are in scope, price them before the contract starts, not after install.

- Track margin by job, not just month

- Log change orders before work starts

- Compare quoted and actual engineering hours

- Flag freight overruns on each order

The owner’s income depends on what’s left after those direct costs. If estimating errors, rework, or missed change orders show up, the project may still look busy, but take-home pay drops because gross profit shrinks before overhead is covered.

2

Sales Pipeline Quality

Sales Pipeline Quality

This driver is the share of bids that are a real fit for the plant, the budget, and the delivery team. The model assumes $637M in first-year revenue and $2,803M in the mature year, but that only works if the pipeline turns into projects the team can actually win and build at modeled margin. Poor-fit bids burn scarce engineering time and travel, site inspection, and proposal time, which cuts utilization and owner pay.

Track quote quality, win rate, customer fit, and whether each project clears modeled margin. If a bid wins on price but needs extra redesign, rework, or concessions, the business may book revenue and still lose cash flow. Clean pipeline discipline protects gross margin, keeps staff on billable work, and makes annual profit more predictable.

Tighten bid filters

Before sending a proposal, score each lead for engineering complexity, site access, budget fit, and delivery risk. If the project cannot clear margin without discounting or extra labor, stop bidding. One clean rule: only bid work you can price, build, and commission without stretching the team.

- Count leads, bids, and wins.

- Track proposal hours per win.

- Measure margin by project.

- Log site-visit and travel cost.

- Reject weak-fit, low-margin deals.

That keeps scarce engineering time on jobs that can close and deliver. Stronger pipeline quality usually means fewer wasted bids, better pricing power, steadier cash timing, and more profit left for owner draw.

3

Engineering And Installation Capacity

Engineering and install capacity

Capacity is the ceiling on how many projects turn into billed revenue and owner profit. The model grows from 102 total units in year one to 373 units in the mature year, so throughput, not demand alone, sets income. Outside engineering starts at 40% of revenue and contract installation labor at 60%, then both fall as the team gets faster and more efficient.

Track crew load and handoff speed

Measure units sold, engineering hours per unit, install crew utilization, and project slip days. Here’s the key tradeoff: hiring or subcontracting can raise throughput, but payroll and coordination costs can hit cash before the job bills. If projects slip, owner distributions drop even when backlog looks healthy, so keep the schedule tight and the handoff from design to field clean.

4

Service And Parts Revenue

Service and Parts Revenue

Aftermarket work can lift owner income between installs, but only if each job covers technician time, travel, and inventory cost. In this model, service is an add-on stream tied to vacuum transfer units, rotary airlock kits, and dust collection modules. It is not recurring revenue unless a signed maintenance contract exists, so treat audits, troubleshooting, replacement parts, and controls upgrades as one-off sales.

Here’s the quick math: if a service call is priced below labor, truck roll, and parts mark-up, it cuts gross margin and cash. If it is priced above those costs, it helps smooth income between larger projects and supports owner draw. The key inputs are number of calls, average ticket, parts mix, and contract status.

Price Every Aftermarket Visit

Track each service line separately: system audits, replacement components, controls upgrades, troubleshooting visits, and maintenance contracts. That keeps revenue quality clear and stops one-off work from being mistaken for recurring income. Use signed contracts for any repeat billing, and price each job so gross profit stays positive after labor, travel, and stocked parts.

Watch service gross margin, average response cost, and repeat work rate. The model already shows aftermarket items alongside core systems, so the win is better mix, not more volume at any price. If a job needs extra site visits or fast parts shipping, raise the price or the work can eat the cash that should pay the owner.

- Separate billable service from warranty work.

- Quote travel and parts up front.

- Use contracts only when signed.

5

Warranty And Working Capital Reserves

Warranty and Working Capital Reserves

Owner pay here depends on cash timing, not just accounting profit. The model holds a 15% warranty reserve, and the first-year figure is stated as $956k on $637M of revenue. That reserve covers commissioning rework, slow collections, retainage, and other cash gaps that can leave a profitable project business short on spendable cash.

Working capital is the cash tied up between billing and collection. Deposits, progress billing, supplier payments, and final customer cash all move on different clocks, so owner distributions can lag reported earnings. A reserve is normal cash discipline, not a sign the business is failing.

Track cash, not just profit

Use one simple rule: if cash comes in after cash goes out, the owner draw waits. Track deposit date, milestone billings, supplier due dates, retainage, and final collection on every project so you can see where cash gets trapped. One clean line: profit does not pay the owner if cash is still on the job.

- Track reserve by job

- Separate retainage from profit

- Review aged receivables weekly

- Hold cash for rework

- Bill milestones faster

If collections slip or commissioning takes extra rework, raise the reserve before taking distributions. Tighten progress billing, ask for larger deposits, and keep supplier terms aligned to customer cash timing. That protects owner income without starving the project team of cash.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with project count, system mix, and how fast engineering and installation payroll scale against fixed overhead.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the first-year downside case, where launch volume stays light and owner income tracks early operating profit. | This is the normal operating case, with steady project flow and owner income tied to the modeled middle path. | This is the stronger earnings path, where mature-year volume and margin expansion push owner income higher. |

| Typical setup | Year 1 runs at about $6.371M revenue, 102 total units, and 70.4% gross margin, with $565k fixed overhead plus General Manager payroll. | Mid-model output reaches about $14.457M revenue, 204 total units, and 73.3% gross margin, with a larger sales and delivery team. | Mature-year output reaches about $28.031M revenue, 373 total units, and 75.9% gross margin, with a much larger field and engineering bench. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $3.92MLow Case | $10.03MBase Case | $20.70MHigh Case |

| Best fit | Use this if you want a cautious launch view and a stress test for early cash use. | Use this as the core planning case for a typical sales ramp and steady hiring. | Use this to test upside if mature demand and staffing expansion both hold. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Dense Phase Pneumatic Conveying Systems Porter's Five Forces Analysis

- Dense Phase Pneumatic Conveying Systems BCG Matrix

- Dense Phase Pneumatic Conveying Systems Business Model Canvas

- What Are The Five KPIs For Dense Phase Pneumatic Conveying Systems Business?

- Dense Phase Pneumatic Conveying Systems Business Plan Template in Pre-Written Word

- How Increase Dense Phase Pneumatic Conveying Systems Profits?

- What Do Dense Phase Pneumatic Conveying Systems Cost To Run?

- Dense Phase Pneumatic Conveying Startup Costs: $130k+ CAPEX

- Dense Phase Pneumatic Conveying Systems Financial Model Template in Excel

- Start a Dense Phase Conveying Business in 3–6 Months

- How To Write A Business Plan For Dense Phase Pneumatic Conveying Systems?

- Dense Phase Pneumatic Conveying Systems Marketing Mix

- Dense Phase Pneumatic Conveying Systems Marketing Plan

- Dense Phase Pneumatic Conveying Systems Business Proposal

- Dense Phase Pneumatic Conveying Systems PESTEL Analysis

- Dense Phase Pneumatic Conveying Systems Pitch Deck Example Editable PPTX

- Dense Phase Pneumatic Conveying Systems Business SWOT Analysis

- Dense Phase Pneumatic Conveying Systems Value Proposition Canvas

Frequently Asked Questions

The model shows up to about $392 million of first-year pre-tax operating profit before debt, taxes, and extra reinvestment That comes from $637 million in revenue and a 704% gross margin Actual owner pay depends on cash reserves, collections, warranty claims, and whether the owner leaves cash inside the company