Owner income$69k

Owner income$69kHow Much Does A Dessert Bar Owner Make? $83k Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$69k  Net margin7.7%

Net margin7.7% Revenue for target pay$898k

Revenue for target pay$898k Business difficultyHard

Business difficultyHard

You’re planning owner pay after payroll, rent, food costs, reserves, and startup cash, not just top-line sales In the first year, the researched assumptions show about $138M in revenue and $83k in EBITDA, meaning earnings before interest, taxes, depreciation, and amortization Actual dessert bar owner take-home pay depends on debt, taxes, reinvestment, and whether the owner is paid through payroll or distributions

Owner income$69kNet margin7.7%Revenue for target pay$898kBusiness difficultyHardWant to test your dessert bar owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay for a dessert bar.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

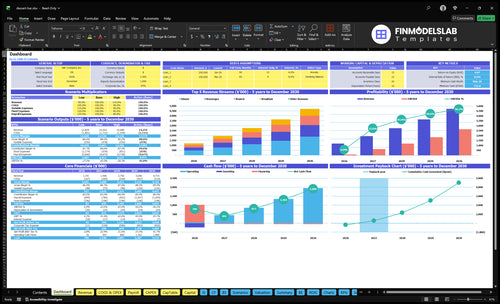

How do you check owner income in the Dessert Bar model?

Screenshot shows month-by-month revenue, margin, costs, reserves, and owner take-home assumptions. Open the Dessert Bar Financial Model Template.

Owner-income model highlights

- Owner cash flow output

- Month 4 breakeven

- Month 5 low point

- $723k minimum cash

- 18-month payback

- 667% ROE

- 009 percent IRR

- $83k Year 1 EBITDA

How much does a dessert bar owner take home after expenses?

A Dessert Bar owner can take home up to $83,000 in Year 1 EBITDA under this case, before taxes, debt service, cash reserves, and reinvestment; What Is The Most Important Measure Of Success For Dessert Bar? matters because take-home depends on covers, average order value, and cost control. Revenue is modeled at about $1.38 million from 405 weekly covers and a $50 to $75 AOV.

Owner Cash

- $83,000 EBITDA before owner cash choices

- Not the same as sales

- Taxes reduce actual take-home

- Debt and reserves reduce draws

Cost Drivers

- $605,000 payroll load

- $195,600 fixed overhead

- 25% marketing reduction target

- 15% operating supplies reduction target

How much revenue does a dessert bar need to pay the owner?

A Dessert Bar needs about $898k a month in revenue to support a $69k monthly owner draw, using a 82% contribution margin and about $667k of payroll plus fixed overhead. That treats owner pay as a target draw, not an automatic salary, and it leaves out debt, taxes, and reserves. The current Year 1 revenue assumption of about $1.148M a month is above that need, so the full-model EBITDA check still matters.

Target pay math

- $69k owner draw target

- 82% contribution margin

- $667k monthly payroll and fixed overhead

- $898k needed monthly revenue

Watch the gaps

- Exclude debt, taxes, reserves

- Current revenue assumption: $1.148M

- EBITDA stays the control check

- Owner pay should stay a target draw

What is a good profit margin for a dessert bar?

A good profit margin for a Dessert Bar is one that turns into owner cash after food, drink, and waste, not just a big percentage on paper. In the provided model, Year 1 gross margin after food and beverage costs is listed at 860%, and after operating supplies at 845%; How Much Does It Cost To Open A Dessert Bar Business? helps frame how much cash you need to support that margin. Here’s the real lever: premium desserts and beverages can lift average order value from $50 midweek and $75 on weekends in Year 1 to $70 and $100 by Year 5.

Margin drivers

- Year 1 food cost: 100%

- Year 5 food cost: 80%

- Year 1 beverage cost: 40%

- Year 5 beverage cost: 30%

Cash risks

- Spoilage cuts cash fast

- Portion creep raises food cost

- Chocolate, dairy, fruit waste hurts

- Packaging waste eats margin

Want the six dessert bar income drivers?

1

$50/$75Ticket Mix

Midweek tickets at $50 and weekend tickets at $75 set the ceiling on owner income, because each upsell lifts revenue with little extra labor.

2

405/wkWeekly Covers

Year 1 runs at 405 covers a week, so small gains in foot traffic and table turns flow straight into cash.

3

84.5%Margin Control

Food, beverage, and supplies leave about 84.5% after cost, so waste and portion control protect almost all of each sale.

4

$605KPayroll Load

Year 1 payroll totals $605K, so labor scheduling and the owner's role decide how much profit stays after service.

5

$10KFixed Overhead

$10K of monthly occupancy is the biggest fixed drag, so rent and location terms set the break-even line fast.

6

30%Add-On Sales

Beverages reach 30% of sales mix, and add-on drinks or pairings raise the average check without adding seats.

Dessert Bar Core Six Income Drivers

Average Ticket And Menu Mix

Average Ticket And Menu Mix

Average order value (AOV) is the fastest way to raise revenue without matching traffic growth. Year 1 assumes $50 midweek and $75 on weekends; by Year 5, that rises to $70 and $100. That kind of lift increases cash per cover, helps absorb fixed payroll and rent, and gives the owner more room for profit draw.

The mix matters too. Year 1 leans on 400 percent dinner and 250 percent beverages, then shifts to 340 percent dinner and 300 percent beverages by Year 5. Plated desserts, beverage pairings, tasting flights, brunch desserts, and add-ons can push ticket size up, but pricing too far above value or growing portions faster than price will cut margin.

Track Ticket, Not Just Traffic

Watch AOV by daypart and item mix by check. Here’s the quick math: if weekend checks stay at $75 to $100 and midweek checks move from $50 to $70, revenue improves without needing the same jump in covers. Track dessert attach rate, beverage attach rate, and add-on sales so you can see which items raise take-home profit, not just sales.

Test price in small steps and protect perceived value. Use menu engineering to keep high-margin desserts and drinks visible, then measure whether portions, garnish, or plate build justify the price. If guests start downgrading to lower-ticket items, AOV rises less than planned and the owner still carries the same fixed cost load.

1

Daily Orders And Foot Traffic

Daily Orders And Foot Traffic

Owner pay depends on cover volume (guest count), not just menu quality. At 405 weekly covers in Year 1, with 250 covers from Friday to Sunday and $75 AOV on weekends, the room has to fill enough seats to cover fixed payroll and occupancy before profit reaches the owner.

By Year 5, covers rise to 1,100 per week. That only works if seating capacity, hours, local demand, and conversion rate (walk-ins who sit down) can support it; slow Monday-to-Thursday traffic is the main risk because labor and rent still run.

Track Covers, Then Staff To Demand

Track covers by day, turn time, and no-show rate. Compare weekday covers to weekend demand so you know whether events, holidays, and dessert occasions are bringing in new guests, or just shifting them from one night to another.

Use weekly forecasts to match labor to traffic. If Friday through Sunday hold 250 covers, protect those shifts first, then trim slow midweek hours before payroll pressure cuts cash available for owner pay.

2

Food Cost, Packaging, And Waste Control

Food, Packaging, and Waste Control

For a dessert bar, this driver is the gap between what you buy and what you sell. Premium chocolate, dairy, fruit, sauces, garnishes, and takeaway packaging can support price, but spoilage or over-portioning turns margin into waste. In the disclosed model, Year 1 food costs are 100%, beverage costs are 40%, and operating supplies add 15%, for a combined ingredient and supply burden of 155% before it improves to 120% by Year 5.

The key inputs are portion size, batch size, prep sheets, par levels, end-of-day waste logs, and packaging use. Here’s the quick math: every wasted dessert cuts owner cash dollar for dollar, so the hit shows up first in gross margin and then in take-home pay. The main risk is overprepping for peak nights and throwing out high-cost items on slow midweek days.

Track Waste Before It Hits Cash

Measure waste by item and by day, then tie it to cover count and menu mix. Keep batch sizes small, set par levels as minimum stock levels, and use prep sheets so staff make only what sales can absorb. Pack only what you expect to sell, since takeaway containers add cost even when the dessert does not move.

- Log end-of-day waste daily.

- Match batches to demand.

- Review portions every week.

- Price packaging into menu items.

- Cut overprep on slow weekdays.

3

Labor Scheduling And Owner Role

Labor Scheduling And Owner Role

Payroll is the biggest visible cost here: $605k in Year 1, rising to $930k by Year 5. It includes $90k head chef, $60k sous chef, $120k kitchen staff, $75k manager, $140k servers, $90k bartenders, and $30k host, so any labor drift hits owner income fast.

If the owner replaces the paid manager, cash payroll can improve by that $75k line, but unpaid owner labor is still a real cost. The key is to separate owner salary, distributions, and unpaid work so the business does not look healthier than it is.

Track Hours by Role

Build the schedule from covers, daypart demand, and role hours. Track labor per cover, weekend versus midweek staffing, and manager hours replaced by the owner. If service suffers, labor savings can fade into lower sales, slower turns, and weaker take-home income.

Use a weekly dashboard that shows scheduled hours, actual hours, and labor cash. Keep owner time visible too, so you can judge whether the manager replacement is true savings or just hidden work.

4

Rent, Location, And Fixed Costs

Rent, Location, and Fixed Costs

Location can lift traffic, but fixed overhead sets the floor you must clear each month. Here, fixed costs total $163k per month or $1.956M per year, including $10k occupancy, $25k utilities, $500 software, $800 insurance, $12k accounting and legal, $300 admin supplies, and $1k maintenance. The owner’s take-home income depends on whether covers can fund this stack before food and labor.

The risk is signing for peak-weekend upside while midweek stays light. The model says occupancy alone is about 87% of Year 1 revenue, so slow Mondays or weak lunch periods can erase profit fast. One clean rule: good locations help revenue, but heavy fixed costs can still block owner pay.

Track Break-Even Monthly

Track monthly covers by daypart, rent as a share of revenue, and fixed-cost burn. Break-even is the point where profit is zero, so test the lease against weak midweek traffic, not just Friday and Saturday. If weekday covers do not carry enough of the $163k overhead, owner income gets squeezed even when weekends look busy.

Before signing or renewing, compare the site’s traffic pattern with seating capacity and hours. A strong corner only works if it fills enough seats outside peak nights. What this estimate hides: any extra labor, food waste, or remake cost makes the gap to owner pay wider.

5

Channel Mix And Add-On Revenue

Channel Mix That Keeps Cash

Channel mix me ans where sales come from: dinner, brunch, breakfast, beverages, catering, party trays, preorders, takeout, delivery, private events, late-night service, and seasonal specials. In Year 1, the mix is 400 percent dinner, 200 percent brunch, 150 percent breakfast, and 250 percent beverages; by Year 5, beverage mix rises to 300 percent. That only helps owner pay if each channel clears fees, labor, and waste.

Here’s the quick math: add-ons lift revenue without needing the same traffic growth, but delivery can add platform fees, packaging, remakes, and labor pressure. A channel that sells more but leaves less cash after variable costs hurts take-home income. Rank channels by cash after variable costs, not by sales alone, and keep the ones that fit staffing and prep flow.

Measure Cash Per Channel

Track each channel separately: orders, average ticket, fees, packaging, remake rate, and labor minutes. Then compare cash left after variable costs. If delivery or late-night service needs extra staffing, it may look busy but still lower profit. One clean rule: keep the channels that add cash, not just volume.

- Track orders by channel.

- Log fees and packaging.

- Count labor minutes per order.

- Test brunch and beverage add-ons.

- Drop channels with weak cash.

6

Compare low, base, and high dessert bar owner income scenarios

Owner income cases

Owner income moves with cover growth, weekend pricing, and payroll load. Year 1 is thin, Year 3 is the core case, and Year 5 shows the upside if traffic keeps building.

| Scenario | Low CaseDownside case | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lower earnings path built on Year 1 volume and the model's $83k EBITDA before taxes, debt, and reserves. | This is the modeled middle case built on Year 3 volume, with owner take-home still shaped by reserves, debt, and reinvestment. | This is the stronger earnings path built on Year 5 volume, but owner take-home still depends on reserves, debt, and reinvestment. |

| Typical setup | It assumes 405 weekly covers, $50 midweek AOV, $75 weekend AOV, 14.0% COGS, 4.0% variable expenses, $605k payroll, and $195.6k fixed overhead. | It assumes 725 weekly covers, $60 midweek AOV, $88 weekend AOV, 12.5% COGS, 3.5% variable expenses, and $752.5k payroll. | It assumes 1,100 weekly covers, $70 midweek AOV, $100 weekend AOV, 11.0% COGS, 3.0% variable expenses, and $900k payroll. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $83kEarly profit | $1.2MCore profit | $2.7MScale upside |

| Best fit | Use this to stress-test early traffic, pricing, and cash use before the model fully ramps. | Use this as the working plan for budgeting, hiring, and lender discussions. | Use this to test upside if traffic stays strong and cash stays disciplined. |

Planning note: These ranges are researched planning assumptions only. They are not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Dessert Bar Porter's Five Forces Analysis

- Dessert Bar BCG Matrix

- Dessert Bar Business Model Canvas

- 7 Key KPIs to Track and Grow Your Dessert Bar

- Dessert Bar Business Plan Template in Pre-Written Word

- 7 Data-Driven Strategies to Boost Dessert Bar Profitability

- How to Run a Dessert Bar: Essential Monthly Operating Costs

- How Much Does It Cost To Open A Dessert Bar? $723k Plan

- Dessert Bar Financial Model Template in Excel

- How To Open A Dessert Bar In 4 To 9 Months With A Launch Plan

- How to Write a Dessert Bar Business Plan in 7 Steps

- Dessert Bar Marketing Mix

- Dessert Bar Marketing Plan

- Dessert Bar Business Proposal

- Dessert Bar PESTEL Analysis

- Dessert Bar Pitch Deck Example Editable PPTX

- Dessert Bar Business SWOT Analysis

- Dessert Bar Value Proposition Canvas

Frequently Asked Questions

The researched case shows $83k in Year 1 EBITDA, or about $69k per month before taxes, debt, reserves, and reinvestment That is based on about $138M in first-year revenue, 405 weekly covers, and $50 to $75 average order values It is not a guaranteed owner salary