Owner income$240k+

Owner income$240k+How Much Diaphragm Wall Construction Owners Make On $421M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$240k+  Net margin69.4%-81.2%

Net margin69.4%-81.2% Revenue for target pay$42.1M-$119.5M

Revenue for target pay$42.1M-$119.5M Business difficultyHard

Business difficultyHard

A diaphragm wall contractor owner can model a $240,000 annual salary line plus possible pre-tax distributions, but that distribution is not automatic In the first year, completed revenue is $421M, gross profit is about $336M, and gross margin is about 798% under the researched assumptions After 55% referral and bonding fees, $590,400 in fixed overhead, and the $240,000 CEO salary line, the model leaves about $304M before taxes, debt service, retainage, and extra reinvestment By the fifth year, revenue reaches $1195M and gross margin is about 817%, but cash discipline still decides owner take-home

Owner income$240k+Net margin69.4%-81.2%Revenue for target pay$42.1M-$119.5MBusiness difficultyHardWant to test your own owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from monthly revenue, gross margin, labor, overhead, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to customize the Diaphragm Wall Construction forecast?

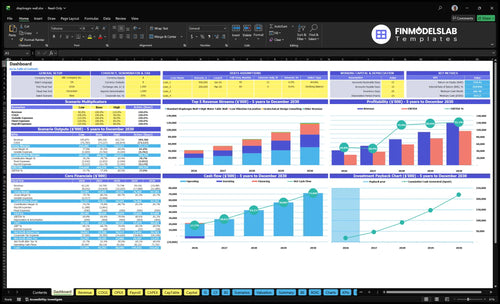

This dashboard in the Diaphragm Wall Construction Financial Model Template shows revenue, costs, cash flow, and owner take-home—open it.

Owner-income model highlights

- $421M Year 1 revenue

- $1,195M Year 5 revenue

- 798% to 817% margin

- Concrete to consulting inputs

- Salary, reserves, distributions

Should a diaphragm wall contractor own or rent equipment?

For Diaphragm Wall Construction, the right call is owning only when backlog and utilization stay high, not because ownership feels better; see What Are Diaphragm Wall Construction Operating Costs? for the cost stack. The model already includes a $15,000 monthly heavy equipment yard lease and a 20% maintenance reserve, so ownership has to earn its keep after maintenance, mobilization, transport, and debt service.

Own when busy

- Protects schedule control

- Works when crews stay busy

- Covers fixed yard lease

- Needs debt service test

Rent when gaps hit

- Reduces cash risk in idle gaps

- Avoids maintenance downtime

- Lowers transport burden

- Pause distributions until tested

How much revenue does a diaphragm wall contractor need to pay the owner?

Diaphragm Wall Construction needs about $1.12M in annual revenue to cover a $240,000 owner salary plus $590,400 fixed overhead, assuming a 74.3% contribution margin; for setup details, see How To Write A Business Plan For Diaphragm Wall Construction?. Keep salary and distributions separate because profit can’t be paid out until taxes, debt service, retainage, and reinvestment are covered.

Owner pay math

- Owner salary target: $240,000

- Fixed overhead: $590,400

- Required contribution: $830,400

- Break-even revenue: $830,400 / 74.3% = $1.12M

Cash reality

- Year 1 model revenue: $4.21M

- Referral and bonding fees: 5.5%

- Distributions depend on collections

- Retainage can delay owner cash

How does retainage affect diaphragm wall contractor owner income?

In Diaphragm Wall Construction, retainage can make accounting profit look high while owner cash stays stuck. Year 1 profit capacity can reach $304M before taxes, debt service, retainage, and extra reinvestment, but retainage delays cash even after revenue is booked. Bonding also pulls cash, with 25% Year 1 fees and 15% Year 5 fees, and delayed pours, site access issues, disputed change orders, and GC payment timing can cut distributions even when gross margin is near 80%.

Cash timing

- Book profit before cash arrives

- Holdback delays owner distributions

- Bond fees consume early cash

- Project timing drives pay timing

What cuts cash

- Delayed concrete pours slow billing

- Site access issues push cash back

- Change orders can stay disputed

- General contractor timing stretches receipts

Want the six drivers that move owner income?

1

$42.1M-$119.5MBacklog Flow

Booked work lifts revenue from $42.1M in Year 1 to $119.5M in Year 5, and any gap leaves the $590.4K fixed base underfed.

2

2.5%-1.5%Bid Mix

Bonding fees step down from 2.5% to 1.5%, so better project selection keeps more of each contract in owner take-home.

3

45K-100KField Output

Standard wall output rises from 45,000 units to 100,000, and faster crew cycles spread payroll and yard costs across more billings.

4

19%-21%Cost Control

Direct cost stays near 19%-21% of sales, so small swings in concrete, steel, slurry, or labor flow straight into EBITDA.

5

$4.0MEquipment Uptime

The $4.0M equipment stack only pays off when uptime is high; idle plant turns capex into drag and trims cash.

6

$872KCash Discipline

Minimum cash lands at $872K in Month 1, so tight billing and collections protect liquidity when mobilization costs hit.

Diaphragm Wall Construction Core Six Income Drivers

Backlog And Project Utilization

Backlog And Crew Utilization

Backlog is the signed work ready to feed the field, and utilization is how fully crews, cranes, slurry systems, testing teams, and supervisors stay on paid jobs. Year 1 volume is 80,000 wall square feet, growing to 195,000 by Year 5, so better utilization means more revenue days and a stronger shot at owner pay.

Here’s the quick math: $590,400 of fixed overhead plus a $15,000 monthly yard lease equals $770,400 a year before variable field costs. That is about $9.63 per square foot at 80,000 square feet, but only $3.95 at 195,000. Idle gaps hurt twice because revenue stops while support costs keep running.

Track Square Feet, Not Just Starts

Measure backlog square feet by start date, plus crew days, crane days, slurry plant days, and testing-team days. The key check is simple: profitable wall square feet completed divided by available field capacity. If the queue thins out, fixed overhead and the yard lease stay in place, and owner distributions shrink fast.

Keep a 90-day lookahead and a weekly dispatch plan. Flag gaps early, resequence work to keep the plant moving, and do not fill the calendar with jobs that cannot cover their share of $590,400 overhead and the $15,000 monthly yard lease.

- Track backlog by square feet.

- Match work to available crews.

- Watch idle crane and slurry days.

- Recheck the next 90 days weekly.

- Price only jobs that cover fixed burden.

1

Bid Pricing And Contract Mix

Bid Pricing And Contract Mix

Better contracts beat raw volume. Year 1 pricing is $450 per standard wall square foot, $620 for high water table work, and $580 for low vibration work. Consulting adds $55,000 per project and testing adds $28,000 per project, so the contract mix can lift revenue fast without adding the same amount of field hours.

The catch is margin. Markup has to cover direct unit costs, revenue-based COGS, 30% referral commissions, bonding fees, and risk. Hard-bid work with poor ground assumptions can wipe out owner distributions faster than negotiated work with clear change-order rules, especially when site conditions force extra labor, equipment days, or rework.

Price For Risk And Change Orders

Track price by job type, not just total revenue. Split bids into standard wall, high water table, low vibration, consulting, and testing. Then compare price per square foot, direct unit cost, referral commission, and bonding burden on each job. If a contract needs heavy assumption risk, the price must cover it up front or the owner pays for it later.

Use a simple test before every bid: project revenue minus direct cost minus 30% referral fee minus bonding and risk reserve. Protect the margin with written change-order rules, soil-condition clauses, and clear exclusions. Consulting at $55,000 and testing at $28,000 can improve cash flow, but only if they are priced and billed as separate scope.

- Track margin by contract type.

- Separate add-ons from base scope.

- Document ground-risk assumptions.

2

Field Productivity And Ground Conditions

Field Productivity And Ground Conditions

When ground gets harder, margin gets thinner. Wall depth, panel thickness, cage complexity, obstructions, slurry control, and concrete placement speed drive labor hours, equipment days, and schedule risk, so owner take-home falls if production slows.

Year 1 direct unit cost runs $66 per standard wall square foot, $95 in high water table work, and $74 in low vibration work. That cost base rises when crews move slower, while fixed overhead and site supervision keep running, so each delayed panel squeezes gross margin and cash available for owner pay.

Track Output By Ground Condition

Measure productivity by panel type, not just total square feet. The key inputs are square feet completed, labor hours, equipment days, and condition class for each job segment. Here’s the quick math: if slower ground adds hours and days, the same fixed overhead gets spread across fewer productive units.

Watch these fields on every project:

- Square feet per shift

- Hours per panel

- Slurry loss and cleanup

- Concrete placement rate

- Obstruction delay time

One clean rule: if production slips, reset the job-cost forecast fast so margin loss does not hit owner draw late.

3

Direct Cost Control

Direct Cost Control

Direct cost control hits owner income fast because this work is priced per wall square foot. On standard work, the model assumes $66 per square foot: $25 concrete, $18 rebar, $6 bentonite slurry, $5 fuel, and $12 direct operator labor. If the contract price is fixed, every dollar saved here lifts gross margin and leaves more cash for overhead and owner pay.

High water table jobs are the risk point. The adders are $35 waterproof additive, $22 epoxy-coated rebar, $12 polymer slurry agents, $8 extra fuel burn, and $18 specialized crew labor, or $95 more per square foot before rework, disposal, and testing. That means small waste or slurry losses can cut profit fast, even when revenue looks strong.

Track Cost Per Square Foot

Measure direct cost by wall type and job: standard, high water table, and low vibration. Compare actuals to the model’s $66 standard base and $161 high water table total. One clean rule helps: if the cost is tied to one wall, it belongs in direct cost, not overhead.

Log material tickets, fuel, labor hours, testing, waste disposal, and slurry handling by panel. Then price change orders for rework and disposal before they hit cash. If a job starts drifting above budget, cut it early by tightening crew mix, material ordering, and slurry recovery.

4

Equipment Cost And Utilization

Equipment Cost And Utilization

Equipment here is both capacity and overhead. The model carries a $15,000 per month heavy equipment yard lease, or $180,000 per year, plus a maintenance reserve tied to revenue. Crane, grab, hydromill, slurry plant, pump, transport, mobilization, and repair choices all change depreciation, rentals, debt service, and downtime, so they directly affect how much cash reaches the owner. p>

When backlog is steady, owning more gear can lift margin because each job spreads fixed equipment cost over more wall footage. When utilization drops, the same fleet drags profit fast because revenue pauses but the yard lease and support costs keep running. One idle month can wipe out a lot of take-home pay in a project-based business like this.

Track Idle Days, Not Just Revenue

Measure utilization by equipment days on job, idle days, and rental versus owned hours. Also track maintenance spend against revenue, because the reserve should rise with more work and drop when volume slows. That tells you whether the fleet is earning enough to cover the $15,000 monthly lease and still support owner draws.

- Track crane, grab, and hydromill days

- Log downtime by cause

- Separate owned from rented gear

- Watch mobilization and transport losses

- Match reserve to monthly revenue

If backlog is uneven, rent more often and keep cash flexible. If work is booked and repeatable, owning core gear can raise gross margin, but only if utilization stays high enough to cover depreciation, repairs, and the yard lease without squeezing owner pay.

5

Working Capital, Bonding, And Retainage

Cash Holdbacks and Bonding

For a diaphragm wall contractor, profit can look good on paper and still miss the owner’s bank account. Bonding fees are 25% of revenue in Year 1, about $1.053M, then fall to 15% in Year 5, about $1.792M. Add 30% referral commissions, and cash left for draws gets tight fast.

The key inputs are project revenue, bonding %, retainage %, change-order collectability, mobilization timing, and customer pay terms. Retainage is cash held back by the client, so model it as an editable holdback, not free profit. Unpaid change orders and slow billing can block owner distributions even when the income statement looks strong.

Track the Cash Gap

Build a cash forecast by job, not just a P&L. Track billed revenue, unbilled change orders, mobilization advances, retainage, and days to collect. One clean rule: if cash in is slower than payroll, equipment, and bond demands, profit stays locked in working capital.

Use these inputs each month: revenue by project, bond fee %, referral commissions, retainage %, approved change orders, and collection dates. Then stress-test owner pay against a 10- to 15-day slip in billing or payment; that is where strong margins get stranded.

- Bill approved change orders fast.

- Negotiate retainage and mobilization.

- Match bond limits to backlog.

- Track cash by project weekly.

6

Compare low, base, and high diaphragm wall owner-income cases

Owner income scenarios

Owner income shifts with project mix, volume, and how fast crews, equipment, bonding, and overhead scale. This model moves from Year 1 ramp-up to Year 5 mature utilization.

| Scenario | Low CaseEarly ramp-up | Base CaseScaled backlog | High CaseMature utilization |

|---|---|---|---|

| Launch model | Lower earnings path built on Year 1 volume and the smallest operating footprint. | Modeled mid-case built on Year 3 volume and a more established field team. | Stronger earnings path built on Year 5 volume and mature utilization. |

| Typical setup | Year 1 revenue is $42.1M, EBITDA is $29.4M, and the model carries $590.4k of fixed overhead plus a $240k CEO salary. | Year 3 revenue is $73.7M, EBITDA is $59.0M, and the bonding rate stays editable because only Year 1 and Year 5 rates are provided. | Year 5 revenue is $119.5M, EBITDA is $97.0M, and bonding fees fall to 4.5% with a fuller operating team. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $29.4MYear 1 EBITDA | $59.0MYear 3 EBITDA | $97.0MYear 5 EBITDA |

| Best fit | Use this to stress-test the opening year and the first big equipment and staffing ramp. | Use this for a scaled backlog with more design, testing, and field teams. | Use this when the backlog stays full and the fleet, crews, and support teams run near capacity. |

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Diaphragm Wall Construction Porter's Five Forces Analysis

- Diaphragm Wall Construction BCG Matrix

- Diaphragm Wall Construction Business Model Canvas

- What Are The 5 KPIs For Diaphragm Wall Construction Business?

- Diaphragm Wall Construction Business Plan Template in Pre-Written Word

- How Increase Diaphragm Wall Construction Profits?

- What Are Diaphragm Wall Construction Operating Costs?

- Diaphragm Wall Construction Startup Costs: $185M+ CAPEX Plan

- Diaphragm Wall Construction Financial Model Template in Excel

- How To Start A Diaphragm Wall Contractor In 6 To 12+ Months

- How To Write A Business Plan For Diaphragm Wall Construction?

- Diaphragm Wall Construction Marketing Mix

- Diaphragm Wall Construction Marketing Plan

- Diaphragm Wall Construction Business Proposal

- Diaphragm Wall Construction PESTEL Analysis

- Diaphragm Wall Construction Pitch Deck Example Editable PPTX

- Diaphragm Wall Construction Business SWOT Analysis

- Diaphragm Wall Construction Value Proposition Canvas

Frequently Asked Questions

The researched model includes a $240,000 CEO/owner salary line Beyond that, distributions depend on cash left after $421M in Year 1 revenue, $85M in direct costs, 55% referral and bonding fees, and $590,400 in fixed overhead Taxes, debt service, retainage, and reinvestment are excluded