Time to Open9-18 monthsLaunch runway

Time to Open9-18 monthsLaunch runwayHow to Start a Digital Banking Platform in 9 to 18+ Months

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Time to Open9-18 monthsLaunch runway  Launch Sequence7 stagesCompliance first

Launch Sequence7 stagesCompliance first Key BottleneckApproval gateState rules

Key BottleneckApproval gateState rules First Revenue StepPilot onboardRails activated

First Revenue StepPilot onboardRails activated

You’re opening a regulated financial product, not just launching an app, so the launch plan must start with the operating model, sponsor bank or licensing path, compliance controls, and core technology This guide covers the 9 to 18+ month launch path, with Year 1 to Year 5 model checks such as $30 million in Year 1 deposits and $11 million in Year 1 loans Use it to pressure-test readiness before beta, not as a substitute for legal or regulatory advice

Time to Open9-18 monthsLaunch runwayLaunch Sequence7 stagesCompliance firstKey BottleneckApproval gateState rulesFirst Revenue StepPilot onboardRails activatedLaunch timeline

This is a short web summary of the launch plan; the XLSX export contains the task-level Gantt Chart.

Launch scheduleMonth 1Month 2Month 3Month 4Month 5Month 6Month 7Month 8Month 9Month 10Month 11Month 12

Legal / Compliance

- Entity setup

- License review

- Policy draft

- KYC AML rules

Sponsor Bank

- Model shortlist

- Due diligence

- Commercial terms

- Approval review

Product Build

- Core ledger

- Account opening

- Admin tools

- Reporting build

Ledger / Payments

- ACH setup

- Card issuing

- Payment rails

- Reconciliation

Security / Risk

- Threat review

- Pen test

- Fraud tests

- Evidence pack

Staffing / Launch

- Key hires

- Support scripts

- Beta cohort

- Launch approval

- Public rollout

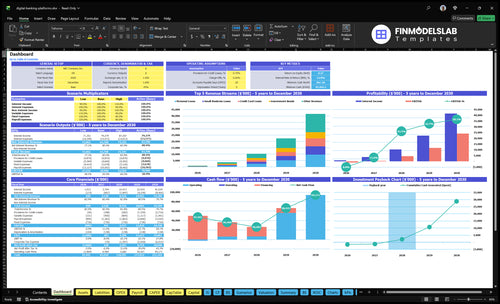

Why test launch numbers before go-live?

Before go-live, the screenshot in the Digital Banking Platform Financial Model Template shows revenue, costs, cash needs, assumptions, and break-even logic—open the model.

Financial model highlights

- Launch month dashboard

- Year 1 loans: $11M

- Year 1 deposits: $30M

- Year 5 loans: $470M

- Year 5 liabilities: $108B

- Credit losses separate

Do you need a bank charter to start a digital banking platform?

No, you don’t always need a bank charter to start a Digital Banking Platform; you can pursue a charter, partner with a sponsor bank, or use banking-as-a-service infrastructure, as explained in What Is The Primary Goal Of Your Digital Banking Platform?. For Year 1 plans of $30 million in deposits and $11 million in loans, the chosen path must match the compliance load before customer onboarding; this is feasibility guidance, not legal advice.

Path Choices

- Use a sponsor bank first

- Pursue a charter for control

- Use banking-as-a-service rails

- Match path to scale

Key Tradeoffs

- Expect model and risk review

- Prepare KYC/AML controls

- Validate disclosures and marketing

- Plan for fraud and payments

What launch risks can stop a digital banking platform from going live?

Weak compliance controls, untested fraud monitoring, and unclear sponsor-bank responsibilities can stop a Digital Banking Platform from going live. The risk gets real fast if Year 1 plans depend on $30 million in deposits or $11 million in loans that are not yet approved. Public launch should wait until operational errors, dispute handling, and fraud review can work at expected volume.

Launch blockers

- Weak compliance can halt approval.

- Failed KYC breaks account opening.

- Fraud monitoring must be tested first.

- Unclear duties delay launch decisions.

Go-live check

- Sign operating roles before launch.

- Test payment rails and escalation paths.

- Show security evidence and beta metrics.

- Validate the finance model against volume.

How do digital banking platforms get first customers?

First customers for a Digital Banking Platform usually come from a narrow niche, then a waitlist, employer or community partnerships, embedded finance channels, referrals, and a controlled beta. If you're sizing launch spend, see How Much Does It Cost To Launch Your Digital Banking Platform Business? because early traction only matters when it turns into funded, compliant accounts. In year 1, the bar is real money: about $30 million in deposits and $11 million in loans, not vanity downloads.

Best first channels

- Start with one narrow user niche

- Use waitlists to test demand

- Partner with employers and communities

- Push referrals and controlled beta access

What to track

- Signups and identity pass rate

- Funded accounts and card activation

- First transaction and support tickets

- Fraud alerts, churn, and fee use

Keep marketing claims tied to sponsor-bank approvals and customer disclosures, or you create trust and compliance risk. The first revenue comes when users fund accounts, use cards, pay subscriptions, generate platform fees, or qualify for approved lending products.

Confirm whether the platform is ready to go live

Launch readiness checklist

Use this go-live approval checklist to confirm the digital banking platform is ready before opening.

Bank path

- Sponsor bank agreement signedCritical

No signed bank path means no lawful deposit or payment launch.

- Licensing route approvedCritical

You need one clear licensing path before customer onboarding starts.

- Legal entity formedHigh

The entity must exist before contracts, accounts, and controls go live.

- Product scope clearedHigh

Uncleared products can block approvals and break the launch plan.

Compliance

- KYC/AML program approvedCritical

Know Your Customer and anti-money-laundering controls must be live first.

- Sanctions screening liveCritical

Screening must catch blocked names before account opening and payments.

- Customer disclosures approvedHigh

Customers need clear terms, fees, and limits before they fund accounts.

- Complaint handling definedHigh

A clear complaint path lowers regulatory risk and support confusion.

Platform

- Core ledger reconcilesCritical

The ledger is the source of truth, so balances must match.

- Account opening testedCritical

Customers need a working open, fund, and use flow at launch.

- ACH payments pass testsHigh

Payment failures at launch create support spikes and lost trust.

- Debit card issuing readyMedium

If cards are part of launch, the issuing path must be fully wired.

Security

- Fraud rules tunedCritical

Weak fraud rules can drain cash fast through fake accounts and transfers.

- Vendor contracts signedHigh

Vendor duties must be clear before any launch dependency goes live.

- Access controls lockedHigh

Role limits protect customer data and reduce internal error risk.

- Incident response testedCritical

A tested response plan is key when payments, data, or fraud issues hit.

People

- Compliance owner assignedCritical

One clear owner keeps compliance tasks from slipping at launch.

- Support coverage staffedHigh

Unstaffed support drives long waits and early churn.

- Dispute workflow rehearsedHigh

Chargebacks and account disputes need a fast, consistent path.

- Admin tools trainedMedium

Staff must know how to fix issues without breaking controls.

Economics

- Runway covers Month 12Critical

The model shows minimum cash in Month 12, so runway must cover it.

- Year 1 deposits hit $30MHigh

The launch case should support the Year 1 deposit anchor, not a softer guess.

- Year 1 loans hit $11MHigh

Revenue should not depend on loan volume that needs unapproved products.

- Breakeven path approvedCritical

Breakeven is Month 17, so the first revenue path must support that timing.

Want the six launch drivers that matter most?

1Regulatory Path

9-18+ moSponsor-bank approval can delay go-live 9-18+ months, and scale should wait until responsibilities are signed off.

2Platform Stack

Day-1 stackA tested ledger, payments, cards, and reporting stack keeps launch clean and cuts day-one breakage.

3KYC/AML

Fraud gateVerified identity, screening, and fraud queues protect onboarding and reduce sponsor-bank pushback.

4Data Security

SOC 2Encryption, access controls, and incident response lower breach risk and help partner approval.

5Customer Onboarding

Y1 $30M depA tight funnel turns verified users into funded accounts and first transactions, not just app installs.

6Ops Readiness

Month 1Staffing support, disputes, and fraud review early prevents backlog when the first accounts go live.

Regulatory and sponsor-bank path

Sponsor-Bank Readiness

No one should start customer onboarding until the charter, sponsor-bank, or banking-as-a-service path is clear and signed. This is the gate that decides who holds customer funds, who owns compliance, and who approves disclosures, payment flows, monitoring, and reporting.

Here’s the quick risk: if partner review comes back with scope cuts or rejection, launch slips fast. The safe move is to delay higher-risk products, like lending, until deposit accounts, KYC, and card flows pass review and the team has audit evidence ready.

Prelaunch Approval Checklist

Build the launch plan around the partner’s approval steps, not the app date. The core inputs are legal entity setup, policy drafts, partner-bank diligence, vendor review, product approval, and evidence for audit and monitoring.

One clean rule: if the responsibilities are not signed, the launch is not ready. That discipline lowers day-one surprises and supports a safer path toward $30 million in Year 1 deposits.

- Confirm compliance ownership first

- Document funds and disclosure flows

- Test KYC, cards, and reporting

- Hold lending until review passes

1

Platform architecture and integrations

Core Platform and Integrations

Your opening risk is not the app design; it’s whether the bank can move money, track balances, and report cleanly on day one. A digital bank must have a tested core ledger, account setup flow, payment rail links, debit card issuing, reconciliation, customer app, back-office console, and data exports before launch. If any one of those breaks, you can still “launch” on paper, but you can’t operate safely.

Here’s the quick read: keep scope tight at launch. For example, launching deposits first and pushing mortgages to Year 2 avoids building systems for a product with $0 assumed revenue in Years 1 and 2. That reduces setup load, cuts support friction, and lowers the chance of a delayed payment-rail approval or broken reconciliation causing an opening slip.

Test the money flow before public launch

Before opening, verify the full chain: account creation, ledger posting, payment movement, card issuance, and reconciliation. Test the sponsor-bank requirements, vendor contracts, security controls, and compliance reporting fields together, not one by one. If the ledger and reconciliation do not match in test, the business will spend launch week fixing balances instead of serving customers.

Assign one owner for each dependency and require signed-off outputs: tested ledger, approved payment rails, working debit cards, admin access, and data exports. One clean one-liner: if the back office can’t explain every balance movement, the launch is too early. Keep the first release limited to products the system can fully support, and hold back anything that adds complexity without near-term revenue.

- Test reconciliation before funding users.

- Confirm payment-rail approval early.

- Freeze scope on day-one products.

- Document vendor and sponsor-bank duties.

2

KYC/AML and fraud controls

KYC, AML, and fraud controls

KYC means proving a user is who they claim to be, and AML means spotting suspicious money movement. For a digital bank, this is a launch gate, not a back-office extra: without identity checks, sanctions screening, and a fraud queue, you cannot safely open to customers on day one.

The launch risk is simple. Weak onboarding creates failed sign-ups, fraud losses, and sponsor-bank concern. Readiness depends on tested identity pass rates, manual review staffing, transaction monitoring, escalation paths, adverse action handling, and audit logs that show who reviewed what and when.

Test the controls before open

Start with the full onboarding path: ID capture, sanctions screen, fraud rule hit, review queue, and final approve or deny. Then confirm support can handle locked accounts, suspicious activity escalations, and customer notices without slowing new account opening.

Document each control and assign an owner. If the fraud queue or manual review work is not staffed for beta, hold launch or limit access to a small test group until the queue, logs, and escalation process work cleanly.

- Verify identity and sanctions flow

- Staff manual review before beta

- Test fraud rules and alerts

- Track audit logs daily

- Confirm escalation and reporting

3

Security and data protection

Security Clearance

A digital bank can’t open safely until encryption, access controls, and least-privilege permissions are in place. If customer login data, payment credentials, or admin access are weak, trust breaks fast and launch timing slips before day one.

The launch gate is evidence, not promises: vendor risk files, a privacy policy, an incident response plan, penetration testing, and audit-ready proof of secure data handling. Where applicable, Gramm-Leach-Bliley Act obligations and SOC 2 readiness can shape partner approval and block public launch if testing or documentation is incomplete.

Lock Access Before Launch

Review admin access and production data permissions before any public release. One clean rule: if the team can’t show who can touch customer data, the launch is not ready.

- Confirm encryption in transit and at rest.

- Restrict admin rights to named users.

- Document vendor controls and review dates.

- Test incident response before live traffic.

- Keep pen test evidence on file.

- Map GLBA duties where they apply.

- Prepare SOC 2 evidence if required.

Failed security testing or missing vendor evidence can delay onboarding, payment access, and partner sign-off. That pushes cash needs out, slows first revenue, and leaves support teams exposed to avoidable incidents on opening day.

4

Customer onboarding and go-to-market

Verified Users First

For a digital bank, opening on time is not about app installs. It’s about getting verified, funded, active users so the first revenue can start through interchange, subscriptions, platform fees, or approved lending. If the onboarding flow is weak, you can be “open” on paper but still have no usable customers on day one.

This driver includes the onboarding funnel, KYC pass rates, funding steps, card activation, and first transaction tracking. A controlled segment launch is the safer move because drop-off often hits during identity checks or account funding. If sponsor-bank claims are not approved, or support and fraud monitoring are thin, launch timing slips and early cash flow stays soft.

Sequence the Funnel Before Broad Launch

Before opening, confirm the waitlist, approved messaging, referral loop, and any employer or community partnership that will feed the first wave of users. Then test each step: identity verification, funded-account metric, card activation metric, and first-transaction metric. Don’t count installs as readiness. One clean one-liner: if users cannot fund and use accounts, you are not live.

Assign clear owners for KYC review, support coverage, and fraud monitoring before launch day. Document the sponsor-bank-approved claims and the exact handoff when a user fails verification or funding. The main risk is drop-off, so watch where users stall and fix that step first. If onboarding is slow or confusing, first revenue gets pushed out even when the product is technically available.

- Verify sponsor-bank-approved claims first

- Track funded, active, transacting users

- Test identity and funding steps

- Staff support before public access

- Monitor fraud queues from day one

5

Operating model and support readiness

Support readiness

If customers hit locked accounts, failed transfers, disputes, or fraud alerts on day one, support becomes part of the launch path. This is not back-office fluff. The operating model must be ready in the first operating month with staffed compliance operations, customer support, dispute handling, fraud review, and clear escalation ownership.

The launch risk is backlog. If beta tickets sit open, unresolved disputes and slow fraud review can force a narrower rollout or delay broader access. Readiness depends on policies, service-level targets that define response and close times, admin tooling, sponsor-bank escalation paths, and reporting that shows where cases are stuck.

Staff the queue early

Before opening broader access, add review staff and test the full case flow: onboarding issue, account lock, transfer failure, dispute, fraud alert, vendor handoff, and final close. Keep each case with one named owner so nothing drifts between support, compliance, and fraud teams.

- Document who owns each case type.

- Test sponsor-bank escalation paths.

- Track open cases by aging.

- Review reports before launch day.

The quick check is simple: can the team answer, route, and close issues without building a queue? If not, stay in beta until the staff, tools, and reporting can keep pace with customer demand.

6

Related Products

- Digital Banking Platform Porter's Five Forces Analysis

- Digital Banking Platform BCG Matrix

- Digital Banking Platform Business Model Canvas

- 7 Critical KPIs to Measure for a Digital Banking Platform

- Digital Banking Platform Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Digital Banking Platform Profitability

- Analyzing the Running Costs for a Digital Banking Platform

- Digital Banking Platform Startup Costs: $151M First-Year Runway

- Digital Banking Platform Financial Model Template in Excel

- How Much Can A Digital Banking Platform Owner Make? $05M Pre-Reserve

- How to Write a Digital Banking Platform Business Plan in 7 Steps

- Digital Banking Platform Marketing Mix

- Digital Banking Platform Marketing Plan

- Digital Banking Platform Business Proposal

- Digital Banking Platform PESTEL Analysis

- Digital Banking Platform Pitch Deck Example Editable PPTX

- Digital Banking Platform Business SWOT Analysis

- Digital Banking Platform Value Proposition Canvas

Frequently Asked Questions

Start with the operating model, not the app screen Choose a charter, sponsor-bank, or banking-as-a-service path, then build KYC/AML, fraud monitoring, core ledger, payments, and customer support around that path A practical plan assumes 9 to 18+ months and validates Year 1 targets such as $30 million in deposits and $11 million in loans