Digital Banking Startup Costs: Plan Year 1 Before $28M In Loans

This digital banking startup budget separates CAPEX for the app, core ledger, cloud, cybersecurity, and integrations from pre-opening legal, compliance, payroll, and launch expenses It also sizes working capital against model costs such as $55,500 per month in fixed overhead and at least $950,000 in first-year listed payroll Total funding need is not the same as startup cost because regulatory capital, sponsor-bank reserves, customer deposits, and loan funding tied to a $28 million Year 1 loan portfolio are separate caveats

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a digital banking launch, before launch-month operating costs.

Scope limits Excludes payroll runway, working capital, debt service, regulatory capital, reserves, customer deposits, inventory, and marketing. Ongoing cloud hosting of $15,000 per month and cybersecurity subscriptions of $7,000 per month after launch are operating costs, not CAPEX.

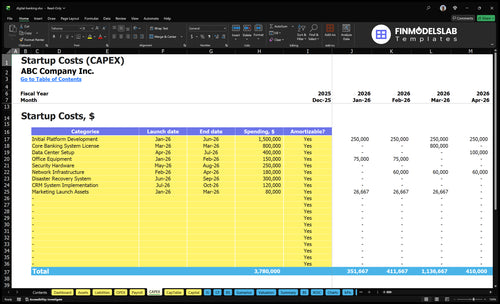

What does the CAPEX tab show?

This screenshot shows the Digital Banking Financial Model Template CAPEX tab, where startup costs, launch timing, depreciation, and amortization sit; review assumptions.

Key screenshot highlights

- Startup costs and timing

- Working capital and cash need

- Payroll and fixed expenses

- $55.5k fixed monthly

- $950k first-year payroll

- $666k overhead; 47% variable

- $28m loans; $535m liabilities

- $35m interest-earning assets

How should founders build a digital bank funding plan?

Founders should fund Digital Banking in phases, not all at once: cover CAPEX, pre-opening spend, launch-month cash, and a 12-month runway tied to milestones like regulatory readiness, app build, sponsor bank setup, KYC/AML testing, card or ACH launch, customer support, and acquisition tests. Here’s the quick math: with a 47% variable expense load, runway means the months of fixed costs and payroll covered before deposits and revenue scale. Keep the balance sheet map tied to $28 million Year 1 loans, $35 million other interest-earning assets, $535 million liabilities, and a $16 million first-year operating base before CAPEX.

Fund by milestone

- Fund regulatory readiness first

- Then app build and sponsor bank

- Then KYC and AML testing

- Then card or ACH launch

Test the model

- Separate CAPEX from opex

- Show pre-opening cash needs

- Show launch-month cash burn

- Show 12-month runway coverage

What hidden costs of starting a digital bank should founders budget for?

If you're budgeting for Digital Banking, the hidden costs sit in compliance, security, and partner setup, not just the app build; see How Much Does The Owner Of A Digital Banking Business Typically Make? for the revenue side. Plan for $3,000 a month in insurance, $6,000 in professional services, $10,000 in legal and compliance fees, and $7,000 in cybersecurity subscriptions. Add 47% variable expenses from interchange fees paid and BaaS provider fees, plus cash for customer support, fraud response, and chargebacks.

$535 million in Year 1 liabilities and $40 million in customer deposits are funding and balance sheet items, not app launch costs, and every extra month of onboarding burns fixed overhead and payroll.

Setup costs

- Budget due diligence and audits

- Pay for sponsor bank onboarding

- Cover privacy and consumer reviews

- Test cybersecurity before launch

Runway costs

- Set aside extra cash runway

- Hold insurance and legal reserves

- Expect fraud and chargeback exposure

- Protect payroll during onboarding delays

What is the biggest digital banking startup cost?

Digital Banking startup cost is usually driven first by pre-launch payroll, not the app. In Year 1, payroll alone is at least $950,000, and the listed fixed spend adds up fast: $666,000 overhead plus $40,000 a month for legal/compliance, cloud, software licenses, and cybersecurity, or about $2.1 million total before growth spend. A tougher charter can raise regulatory and capital needs, and the biggest swing item is whether you build core banking and integrations in-house or buy them as SaaS instead of booking them as CAPEX.

Year 1 cost stack

- $950,000 payroll minimum

- $666,000 fixed overhead

- $120,000 legal and compliance

- $276,000 cloud, licenses, cybersecurity

What pushes it higher

- More lending products add risk scope

- More payment links raise integration cost

- More compliance tools raise fees

- Build or buy changes cash timing

Calculate Fuding Needs

Startup cost summary

This table separates digital banking startup assets from excluded cash needs, using low, base, and high planning scenarios.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Initial Platform Development | $1,500,000 | Core app build and launch-ready tech stack | Yes |

| Core Banking System License | $800,000 | Licensed core banking system setup and integration | Yes |

| Data Center Setup | $400,000 | Hosting and infrastructure setup for launch | Yes |

| Security Hardware | $250,000 | Physical security and infrastructure controls | Yes |

| Network Infrastructure | $180,000 | Connectivity and vendor integration backbone | Yes |

| Regulatory Capital and Liquidity Reserve | $50,111,000 | Regulatory capital, sponsor bank reserves, and loan funding | No |

Digital Banking Core Five Startup Costs

Regulatory, Legal, And Compliance Setup Startup Expense

Setup scope

Budget for legal structuring, regulatory strategy, sponsor-bank diligence, BSA/AML policies, consumer protection, privacy, vendor risk, compliance program design, and board materials. This work starts before revenue and keeps running through launch, so it belongs in pre-opening spend. It does not include regulatory capital, sponsor-bank reserves, or approval conditions.

Budget math

Here’s the quick math: $10,000 per month in legal and compliance fees plus a $120,000 annual Compliance Officer equals $240,000 for 12 months, before any other spend. Split this from ordinary setup items so the cash plan shows both operating burn and any separate reserve asks.

Keep it lean

Use one governance pack, reused policy templates, and a single vendor review path to cut rework. Don’t trim AML, privacy, complaints, or sponsor-bank reviews; weak controls only push costs into delays. While the work is active, this base case burns about $20,000 a month.

Approval risk

This budget prepares you for review, but it does not promise a bank charter, sponsor-bank approval, or product approval. Keep regulatory capital, sponsor-bank reserves, and approval conditions in a separate line item so no one treats them like routine startup costs.

Banking Platform, App, And Core Technology Startup Expense

What It Covers

This cost covers the banking product engine: mobile app, web app, account opening, core ledger, customer profiles, loan workflows, deposits, statements, cloud architecture, APIs, security, QA, and product management. For startup budgeting, split capitalized build work from launch run rate. The monthly operating floor here is $30,000 in cloud, software, and cybersecurity subscriptions, before salaries.

Build Or Buy

If you build core software, app code, ledger logic, and workflow design can sit in CAPEX. If you buy more modules, cost shifts into implementation fees and monthly SaaS. With a $180,000 CTO, $160,000 Head of Product, and $150,000 Lead Engineer, senior tech payroll is about $490,000 a year, or $40.8k a month.

Launch Run Rate

Launch operating cost starts with $15,000 cloud hosting, $8,000 software licenses, and $7,000 cybersecurity subscriptions, so the base SaaS stack is $30,000 per month. Add technical payroll, and the core technology team is about $70.8k a month. That’s the cash burn to watch before product revenue arrives.

Cash Control

Budget this as three buckets: capitalized development, recurring subscriptions, and support. Scope creep in account opening, loan workflows, or reporting can push costs from one-time build into ongoing fees. The cleanest savings come from choosing what to build first and what to buy until launch is stable.

Banking Infrastructure, Vendor Integration, And Payment Rails Startup Expense

Rails and checks

KYC, KYB, AML screening, fraud monitoring, ACH, debit card issuing, processor setup, sponsor bank work, statements, notifications, data reporting, and reconciliation are the core setup pieces here. Pricing usually tracks volume, risk, product scope, integration complexity, and compliance review depth, so the budget needs quotes by module, not one lump sum.

Estimate drivers

Here’s the quick math: model 35% interchange fees paid plus 12% BaaS provider fees, or 47% variable cost on related transaction volume. At Year 1 scale, the integrations support $28 million of loans, $40 million of customer deposits, and $535 million of total liabilities, so usage-based fees can move fast.

- Price by product and rail.

- Get volume-based quotes.

- Model compliance review time.

Cut waste safely

Keep setup work in pre-opening CAPEX only when it is capitalized, and book per-transaction fees as operating expense. The cleanest savings come from limiting scope at launch, using one processor path where possible, and avoiding extra vendor layers that add duplicate checks, reports, and reconciliation work.

- Start with required rails only.

- Skip duplicate vendor tools.

- Track fees by transaction type.

Budget rule

Use separate lines for integration setup, compliance review, and live transaction costs. A practical budget keeps launch build costs in startup expense or CAPEX, then treats ongoing screening, processor, ACH, card, and BaaS charges as operating spend tied to volume, risk profile, and how many products go live first.

Pre-Launch Team, Payroll, And Professional Services Startup Expense

Team Cost

This pre-launch team covers founders, chief executive, technology, product, marketing, engineering, compliance, risk, operations, and customer support setup. The listed salaries total $950,000 a year: CEO $200,000, CTO $180,000, Head of Product $160,000, Head of Marketing $140,000, Lead Engineer $150,000, and Compliance Officer $120,000. That is the core payroll base before any extra hires.

Advisor Spend

Outside counsel, auditors, and specialist advisors should sit outside payroll runway. At $6,000 a month, they add $72,000 a year and start before revenue, while legal and compliance work also runs through launch. Use this bucket for structuring, sponsor-bank diligence, Bank Secrecy Act and anti-money laundering (BSA/AML), privacy, vendor risk, and board materials; it is not regulatory capital or reserve funding.

Burn Rate

Here’s the quick math: $950,000 of annual payroll is about $79,167 a month. Add $55,500 of fixed overhead and each pre-launch month burns about $134,667 before capital spending (CAPEX). So a one-month delay needs another $134.7k of runway, and a two-month slip needs roughly $269k.

Hiring Pace

Keep hiring staged until the product and compliance gates are live. Use the listed leadership and compliance roles first, then add risk, operations, and customer support only when launch timing is real. One rule: fixed overhead keeps burning even if approvals slip, so track monthly burn weekly and push non-core work to advisors.

- Delay non-core hires.

- Use advisors for spikes.

- Review burn weekly.

Launch Readiness, Insurance, Customer Operations, And Go-To-Market Startup Expense

Launch Spend

Marketing and customer acquisition sit in pre-opening or early operating expense, not CAPEX. For a digital bank aiming at $40 million of Year 1 deposits and a $28 million loan portfolio, spend has to cover brand launch, acquisition tests, communications, and operating readiness before revenue is stable.

Readiness Budget

Here’s the quick math: $3,000 insurance + $6,000 professional services + $7,000 cybersecurity subscriptions + $5,000 office rent = $21,000 per month before payroll. Add the $140,000 Head of Marketing salary and this launch bucket runs about $32,667 a month.

Keep It Tight

Use small channel tests, simple support scripts, and one owner for escalations so launch spend stays tied to response time and conversion. Buy only the tools that cut handling time or reduce risk. That keeps customer support tools, call center setup, and incident response from becoming fixed costs with no payoff.

Ops Risk

Cyber insurance and errors and omissions coverage protect the launch, but weak support or fraud response still hurts fast. If account issues take too long to fix, churn rises; if fraud steps are slow, losses rise. That risk matters when the plan is built to support $40 million in deposits and a $28 million loan book.

Compare 3 Startup Cost Scenarios

Scenario Table

Digital banking costs swing with scope. A partner-bank MVP keeps setup light, while a full build pushes up compliance, integrations, payroll, and launch spend.

| Scenario | Lean LaunchPartner-bank MVP | Base LaunchModel baseline | Full LaunchHighest complexity |

|---|---|---|---|

| Launch model | Uses a sponsor-bank or partner-bank model with a narrow product set and a small in-house team. | Builds the modeled digital bank with core lending, deposits, and a full operating team. | Adds broader lending, more channels, and a heavier operating model across compliance, product, and support. |

| Typical setup | Starts with deposits, one or two loan types, and only the integrations needed to launch. | Uses the modeled capex stack, monthly overhead, and first-year payroll reflected in the forecast. | Expands the tech stack, vendor links, and go-to-market program beyond the base plan. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $750,000 - $2,000,000Lowest funding need | $4,000,000 - $6,000,000Plan for burn | $7,000,000 - $12,000,000Highest funding need |

| Best fit | Best for teams that want a narrow launch, one partner bank, and the lowest upfront cash draw. | Best for founders who want the modeled launch path and can fund the full first-year operating stack. | Best for well-funded teams that need broader product scope and can absorb slower compliance and build cycles. |

Planning note: Scenario ranges are researched planning assumptions, not exact quotes.

Related Products

- Digital Banking Porter's Five Forces Analysis

- Digital Banking BCG Matrix

- Digital Banking Business Model Canvas

- 7 Critical KPIs to Track for Digital Banking Success

- Digital Banking Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Digital Banking Profitability Now

- Calculating the Monthly Running Costs for a Digital Banking Startup

- Digital Banking Financial Model Template in Excel

- How Much Digital Banking Owners Can Make From $33M Net Interest Spread

- How To Start A Digital Bank In The US In 9 To 24+ Months

- How to Write a Digital Banking Business Plan in 7 Actionable Steps

- Digital Banking Marketing Mix

- Digital Banking Marketing Plan

- Digital Banking Business Proposal

- Digital Banking PESTEL Analysis

- Digital Banking Pitch Deck Example Editable PPTX

- Digital Banking Business SWOT Analysis

- Digital Banking Value Proposition Canvas

Frequently Asked Questions

It depends on charter strategy, sponsor-bank setup, technology scope, and launch scale In the researched model, fixed overhead is $55,500 per month, or $666,000 in the first year Listed first-year payroll adds at least $950,000, so the operating base is at least $1616 million before CAPEX, one-time setup, marketing, reserves, and regulatory capital