Owner income$923k

Owner income$923kHow Much Can a Directed Energy Deposition Owner Make? $199M Year 1?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$923k  Net margin30.1%

Net margin30.1% Revenue for target pay$579k

Revenue for target pay$579k Business difficultyHard

Business difficultyHard

Key Takeaways

- Billable utilization drives the biggest income swing.

- Higher-spec jobs raise revenue and protect margins.

- Pricing must cover setup, inspection, and scarce capacity.

- Fixed overhead and reserves cut owner take-home fast.

Owner income$923kNet margin30.1%Revenue for target pay$579kBusiness difficultyHardWant to test your DED owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

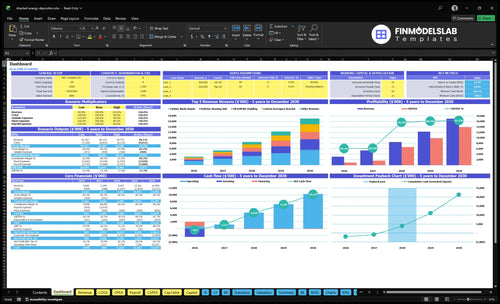

Want to see owner income in the Directed Energy Deposition Manufacturing model?

This dashboard shows revenue, gross margin, fixed overhead, operating profit, reserves, and owner take-home in the Directed Energy Deposition Manufacturing Financial Model Template; open it for the $307M Year 1 to $1.7B Year 5 bridge, with $462k fixed overhead and a $199M-$1.326B pre-tax profit pool.

Owner-income model highlights

- Owner take-home sensitivity

- Revenue bridge and margin

- Scenario tabs, inputs, charts

What costs reduce directed energy deposition gross margin?

If you’re pricing Directed Energy Deposition Manufacturing, the biggest margin hits are feedstock, shielding gas, machinist labor, inspection, tooling, energy, software, logistics, commissions, scrap, rework, and post-processing; the startup-cost view is here: How Much To Start Directed Energy Deposition Manufacturing Business?. Unit direct costs run from $500 for oil drill bit cladding to $1,850 for marine propeller hubs. In Year 1, commissions and logistics take 55% of revenue, and rework hurts twice because it uses capacity without clean revenue.

Direct cost drivers

- Powder: $210 to $850

- Shielding gas: $45 to $150

- Machinist labor: $140 to $450

- Inspection: $80 to $300

Margin pressure points

- Commissions and logistics: 55% of revenue

- Scrap cuts sellable output

- Rework uses capacity twice

- Post-processing adds extra labor

How does the owner role change DED shop income?

If the founder runs selling, quoting, programming, quality, and job control, a Directed Energy Deposition Manufacturing shop can show higher early take-home because owner labor replaces hired staff. But that is not the same as scalable profit: the model already includes per-unit machinist labor of $140 to $450 and inspection of $80 to $300, while a hired general manager cost is not included. Add specialists when you need more sales capacity, throughput, and quality control, even if owner cash dips first.

Early owner cash

- Founder sells the work.

- Founder writes quotes.

- Founder programs jobs.

- Founder checks quality.

Scale and control

- No general manager cost shown.

- Specialists lift throughput.

- Quality control protects margin.

- Owner cash can drop first.

How much revenue does a DED shop need to pay the owner?

If you’re paying the owner from Directed Energy Deposition Manufacturing cash flow, use this formula: (target owner pay + $462k fixed overhead + debt service + reserve allowance) ÷ gross margin. At the stated 79.8% Year 1 gross margin, fixed-overhead break-even is about $579k before debt and reserves, and each extra $1 of owner pay needs about $1.25 of revenue before those items. Keep owner compensation separate from guaranteed salary, because customer deposits, inspection delays, and reinvestment needs can slow distributions.

Revenue math

- $462k fixed overhead sits below owner pay

- 79.8% gross margin drives the split

- $579k covers overhead only

- Debt service raises the needed revenue

Owner pay planning

- Set pay after cash coverage

- Use reserves for delays and rework

- Don't confuse pay with guaranteed salary

- Reinvest before taking distributions

Want to see the six DED income drivers?

1

$923K-$13.9MBillable Utilization

More billable machine time turns the fixed plant into EBITDA, and the model grows from $923K in Year 1 to $13.9M in Year 5.

2

$2.8K-$24.0KJob Mix

Higher-value repair and defense jobs lift average contract size, with marine hubs at $22K-$24K and brackets near $3.8K-$4.2K.

3

79.8%-80.7%Pricing Discipline

Keeping realized prices inside the 79.8%-80.7% gross margin band protects take-home when some part prices fall over time.

4

$618-$2.8KDirect Cost Control

Powder, gas, machinist labor, inspection, and tooling are the main per-part costs, so every cut drops straight to margin.

5

6-14 FTESkilled Throughput

More engineers and quality staff raise throughput, but bottlenecks in handoffs or QA can cap the whole line.

6

$606KOverhead Reserves

The fixed load is about $606K a year, and reserves plus debt service come out before the owner sees cash.

Directed Energy Deposition Manufacturing Core Six Income Drivers

Billable machine utilization

Billable Machine Utilization

With $462k of annual fixed overhead, billable utilization is the main profit lever because every accepted repair or build spreads that cost across more revenue. In this business, utilization should mean customer-approved production and repair hours, not open machine availability.

Here’s the quick math: at 79.8% Year 1 gross margin, each $1 of revenue adds about $0.80 before fixed overhead, debt, and reserves. That helps owner pay only if setup time, rework, and inspection holds stay tight; otherwise true utilization drops fast.

Measure Accepted Hours, Not Uptime

Track billable deposition hours and accepted-output rate every month. No machine-hour source data is provided, so the model should ask for both inputs before forecasting income. If the shop is busy but work fails inspection or waits on customer approval, the machine looks loaded while cash conversion stays weak.

- Billable hours accepted by customers

- Rework hours and inspection holds

- Setup time per job

A small lift in accepted hours can matter more than a small price change because fixed overhead is already known. Better scheduling, fewer changeovers, and cleaner first-pass quality protect revenue quality and keep gross profit closer to the modeled 79.8%.

1

Job mix and contract value

Repeat Repair Mix

Owner income improves when the job mix shifts from one-off work to repeat, qualified repair and build contracts. Using the stated prices, 120 turbine blade repairs at $12,500 plus 15 marine propeller hubs at $22,000 implies $1.83M of Year 1 revenue. That mix matters because setup, inspection, and rework costs sit inside each job before profit reaches the owner.

At Year 5 volume, 400 turbine repairs and 85 marine hubs would imply $6.87M at the same prices. These are qualification-driven jobs, so documentation, inspection, and quality systems come before dependable revenue. If approvals slip, cash comes later, and owner pay gets pushed out.

Track Contract Quality

Track jobs by type, price per job, repeat rate, and first-pass acceptance rate. The key inputs here are qualified repair count, build count, and average contract value. One clean measure is revenue per approved job, because it shows whether the mix is moving toward higher-value work or staying stuck in low-margin one-offs.

Price the whole job, not just deposition time. Include programming, inspection, post-processing, and hold time in the quote. Repeat work lowers selling cost and smooths cash flow, but only if the quality file is complete enough to clear audits and avoid rework.

2

Pricing discipline

Pricing discipline

Directed Energy Deposition (DED) pricing has to cover setup, programming, deposition time, material, shielding gas, inspection, post-processing, risk, and scarce machine capacity. If a quote misses any one of those, one repair can burn technician time and inspection cost while the machine sits tied up. In this model, Year 1 prices run from $2,800 for oil drill bit cladding to $22,000 for marine propeller hubs.

Year 5 modeled pricing rises to $3,000 to $24,000. That matters because underquoting a complex repair cuts gross profit and can turn a busy shop into a cash squeeze. Better quoting protects the modeled 798% to 807% gross margin and keeps owner pay from getting squeezed by rework and inspection holds.

Quote every job from real cost

Build each quote from the actual cost stack: labor, gas, powder or wire, inspection, post-processing, and machine time. Track billable deposition hours, accepted-output rate, and rework rate, because those inputs decide whether a price turns into cash. If a job needs extra setup or repeat inspection, raise the quote before release.

Watch these inputs:

- Setup and programming hours

- Deposition and inspection time

- Material and shielding gas use

- Post-processing and rework

- Scarce machine capacity

Use that data to set a floor price for each part family. If one quote is too low, it ties up a machine slot that could have carried higher-priced work and it delays cash collection.

3

Direct cost control

Direct cost control

If powder, wire, shielding gas, labor, inspection, tooling wear, energy, waste, and software stay tied to each accepted job, owner take-home holds up. The unit direct-cost benchmarks here are $945 for turbine blade repair, $700 for aerospace brackets, $500 for oil drill bit cladding, $1,850 for marine propeller hubs, and $815 for defense housing units.

The risk is simple: scrap, rework, failed inspection, excess powder waste, and post-processing overruns eat gross profit before fixed overhead is even paid. Direct cost per accepted part is the number that tells you whether the owner can keep more cash or just stay busy.

Measure cost per accepted part

Use accepted output as the base, not machine time alone. Here’s the quick math: total direct spend on material, labor, inspection, energy, waste, and software divided by accepted units. That shows the real cost of one good part and where margin leaks out.

- Track scrap and rework rate

- Track failed inspection cost

- Track powder waste per job

- Track post-processing overruns

If one part family keeps running above its benchmark, tighten process control, stop quoting too low, or drop the worst jobs. Better control helps keep gross profit near $245M in Year 1 and protects the owner’s draw.

4

Skilled labor throughput

Skilled labor throughput

Skilled labor throughput is the speed and quality of programming, machine operation, inspection coordination, quoting, and customer engineering that turns jobs into accepted, billable output. In this model, machinist labor runs $140 to $450 per unit and inspection runs $80 to $300 per unit, so labor alone can swing unit cost by $220 to $750 before materials and overhead. One skilled bottleneck can delay accepted revenue and cash collection.

Owner labor can lift early cash flow because you keep more of the work in-house, but it can also hide the real cost of production. Hiring skilled staff may reduce take-home at first, yet it can raise throughput, quality, and sales capacity. The key question is whether the owner is buying speed or just postponing the true labor bill.

Track labor by role and unit

Measure labor hours per accepted unit, not just open shop hours. Track programming time, machine time, inspection time, quote turnaround, rework, and customer engineering touch time by job. If a part sits in inspection or needs repeated setup, the real cost per unit climbs fast and owner pay gets squeezed even when revenue looks busy.

Use staffing to remove the choke point that slows accepted output. A shop that relies on the owner for quoting, programming, and inspection can l ook lean, but it usually caps volume and delays cash. If hired labor improves acceptance rate and cuts holds, the lower near-term draw can still win on profit and collection speed.

5

Fixed overhead and equipment reserves

Fixed overhead and equipment reserves

Fixed overhead comes out before owner pay. The disclosed line items are $22k monthly lease, $45k insurance and liability, and $12k service contracts, which totals $79k/month or $948k/year. The talking points also cite $385k/month and $462k/year, so the model should reconcile that gap before setting take-home pay or debt capacity.

Reserves matter too: calibration, software, maintenance, financing, and reinvestment should be funded before distributions. If those costs are skipped, cash looks strong early but gets hit later by service calls, rework, or machine downtime. One line to remember: lean overhead lowers break-even revenue, but underfunded reserves turn into a cash shock.

Track overhead before you set owner pay

Build owner draw from cash after fixed costs and reserves, not from gross revenue. Track monthly lease, insurance, service contracts, calibration, software, and planned reinvestment, then compare them to billable deposition hours and accepted jobs. The key inputs are fixed overhead, reserve funding, and accepted output.

- Reconcile the overhead figure each month.

- Ring-fence reserve cash before draws.

- Test break-even with actual billables.

For a shop like this, one missed inspection or machine repair can wipe out a month of owner pay if reserves are thin. Keep a separate equipment reserve so the next calibration, software renewal, or service event does not hit operating cash.

6

Compare lean, base, and high DED owner-income scenarios

Owner income scenario table

Owner income moves with utilization, job mix, and staffing because this service carries heavy fixed overhead. The three cases show how the profit pool changes from launch to fuller scale.

| Scenario | Low CaseLow use, thin mix | Base CaseSteady mix, steady use | High CaseHigh use, hard scale |

|---|---|---|---|

| Launch model | This is the lower earnings path if the shop ramps slowly and capacity stays partly unused. | This is the modeled middle path with steady volume and a more balanced job mix. | This is the stronger path if utilization stays high and complex jobs fill the schedule. |

| Typical setup | Year 1 runs at $3.066M revenue and $923k EBITDA, with light throughput across repair and build work. | Year 3 reaches $8.447M revenue and $6.594M EBITDA, with the 3% sales commission load in place and logistics still adjustable. | Year 5 reaches $16.996M revenue and $13.879M EBITDA as throughput climbs across all five job lines. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $923kLaunch year pool | $6.6MModeled core pool | $13.9MUpside scale pool |

| Best fit | Best for launch planning and stress-testing a slow sales ramp. | Best for the core operating plan and lender or investor cases. | Best for upside testing when capacity, staffing, and reserves all work in sync. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Directed Energy Deposition Manufacturing Porter's Five Forces Analysis

- Directed Energy Deposition Manufacturing BCG Matrix

- Directed Energy Deposition Manufacturing Business Model Canvas

- What Are The 5 KPIs For Directed Energy Deposition Manufacturing Business?

- Directed Energy Deposition Manufacturing Business Plan Template in Pre-Written Word

- How Increase Profitability Of Directed Energy Deposition Manufacturing?

- What Are Directed Energy Deposition Manufacturing Operating Costs?

- Directed Energy Deposition Startup Costs For A $307M Year 1 Plan

- Directed Energy Deposition Financial Model Template in Excel

- How To Open A Directed Energy Deposition Business In 6–12 Months

- How To Write A Business Plan For Directed Energy Deposition Manufacturing?

- Directed Energy Deposition Manufacturing Marketing Mix

- Directed Energy Deposition Manufacturing Marketing Plan

- Directed Energy Deposition Manufacturing Business Proposal

- Directed Energy Deposition Manufacturing PESTEL Analysis

- Directed Energy Deposition Manufacturing Pitch Deck Example Editable PPTX

- Directed Energy Deposition Manufacturing Business SWOT Analysis

- Directed Energy Deposition Manufacturing Value Proposition Canvas

Frequently Asked Questions

The researched Year 1 case shows a $199M pre-tax operating profit pool on $307M revenue and 798% gross margin That is before debt service, taxes, reserves, and reinvestment, so it is not guaranteed owner salary By Year 5, modeled revenue reaches $1700M and the pre-tax operating profit pool reaches $1326M