Owner income$90k

Owner income$90kHow Much Disaster Cleanup Owners Make: $90K Salary Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$90k  Net margin74.5%–80.5%

Net margin74.5%–80.5% Revenue for target pay$121k

Revenue for target pay$121k Business difficultyHard

Business difficultyHard

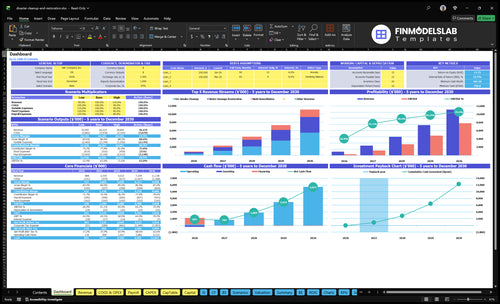

A disaster cleanup business owner can model $90,000 in annual owner-manager pay, with any extra take-home depending on cash left after payroll, equipment, reserves, financing, and reinvestment In the provided assumptions, the business reaches breakeven in Month 5, needs minimum cash of $747,000 in Month 6, and shows EBITDA of $239,000 in Year 1 EBITDA means earnings before interest, taxes, depreciation, and amortization, so it is not the same as owner cash By Year 5, modeled EBITDA reaches $784 million, but distributions still depend on collections timing, reserve policy, and growth spending

Owner income$90kNet margin74.5%–80.5%Revenue for target pay$121kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full forecast for Disaster Cleanup?

Tabs cover revenue, service mix, pricing, costs, cash flow, EBITDA, breakeven, payback, and owner pay. Open the Disaster Cleanup Financial Model Template.

Owner-income model highlights

- Year 1 EBITDA: $239,000

- Year 3 and 5: $268 million, $784 million

- Assumptions: $25k-$100k marketing; CAC $500-$350

- Salary, reserves, reinvestment, distributions

How much revenue does a disaster cleanup business need to pay the owner?

Disaster Cleanup needs about $514,000 in annual revenue to pay the owner $90,000, based on $165,000 non-owner payroll, $103,200 fixed overhead, and $25,000 marketing. Here’s the quick math: that is $383,200 in fixed load before project costs, so sales alone won’t tell you much. Early equipment spend is $223,000, so cash planning matters before you chase growth.

Revenue drivers

- $165,000 non-owner payroll

- $103,200 fixed overhead

- $25,000 marketing budget

- $90,000 owner pay target

Cash load

- $383,200 fixed load

- $514,000 revenue needed

- $223,000 early equipment spend

- Plan for reserves and debt

How does owner involvement affect disaster cleanup income?

For Disaster Cleanup, owner involvement helps protect early cash because the owner-operator can handle estimates, dispatch, customer calls, and project oversight. But that same setup can strain capacity during storm spikes, and collections delays plus emergency availability can make income lumpy even when EBITDA is positive. The model funds one owner-general manager at $90,000, while certified technicians scale from 2 in Year 1 to 6 in Year 5.

Cash control

- Owner handles estimates fast

- Owner answers customer calls

- Owner runs dispatch

- Owner keeps jobs moving

Workload risk

- Storm spikes raise workload

- $90,000 owner role is built in

- Techs grow from 2 to 6

- Cash can lag EBITDA

Can a disaster cleanup business owner make a good living?

Yes — a Disaster Cleanup owner can make a good living: the model supports a $90,000 owner-manager salary, but real take-home depends on scale, cash flow, and reinvestment. To keep that pay healthy, track job volume, collections, and customer outcomes with How Is Disaster Cleanup Tracking Its Overall Success And Customer Satisfaction?. EBITDA, meaning profit before financing and non-cash costs, is modeled at $239,000 in Year 1 and $784 million in Year 5, but it’s not guaranteed cash.

Owner Pay

- Supports $90,000 owner salary

- Covers dispatch and estimates

- Manages projects and collections

- Small crews earn mainly salary

Scale Upside

- $239,000 Year 1 EBITDA

- $784 million Year 5 EBITDA

- Add technicians and project managers

- Reinvest before taking extra cash

Want the six biggest income drivers?

1

$350-$500 CACEmergency Jobs

Lower CAC from $500 in Year 1 to $350 in Year 5 helps the same ad spend buy more qualified jobs and lifts owner take-home.

2

74.5%-80.5%Margin Control

Direct cost control lifts gross margin before salaried payroll from 74.5% to 80.5%, so more of each job stays in the business.

3

85-121 hrsCrew Capacity

Billable hours rise from 85 to 121, and tighter scheduling turns the same crew base into more revenue.

4

$95-$130/hrJob Mix

Shifting work toward higher-rate fire smoke cleanup and away from lower-rate jobs raises average revenue per hour.

5

$747KClaims Cash

Insurance billing and collections matter because the model needs $747K minimum cash, so slow pay cuts owner take-home.

6

$8.6K/moOverhead Reserve

Fixed overhead runs about $8.6K a month before the $90K owner pay, so reserve discipline protects cash.

Disaster Cleanup Core Six Income Drivers

Qualified Emergency Job Volume

Qualified Emergency Job Volume

More qualified emergency calls only raise owner income when the company can answer fast, estimate cleanly, staff the job, and collect cash on time. Here’s the quick math: marketing spend rises from $25,000 in Year 1 to $100,000 in Year 5, while CAC falls from $500 to $350, so paid demand scales from about 50 qualified calls to about 286 if conversion holds.

Turn Calls Into Profit, Not Noise

Track qualified calls, response time, estimate-to-close rate, crew hours, and gross margin together. If volume rises but crews, extractors, dryers, or project managers are booked, revenue leaks into overtime, delays, and bad jobs. The useful rule is simple: size marketing to crew capacity and equipment availability, not vanity lead counts.

- Measure calls by job type.

- Reject unprofitable rush work.

- Match spend to staffed capacity.

- Watch CAC against close rate.

1

Average Job Size And Service Mix

Average Job Size And Service Mix

Job size is the billable hours times the hourly rate, and the mix matters because water, fire, and mold work do not invoice the same way. In Year 1, the model shows water at 20 hours × $95 = $1,900, fire at 40 × $110 = $4,400, and mold at 25 × $100 = $2,500. A shift toward bigger fire jobs raises revenue per call, but it also slows cash if the work takes longer to finish and bill.

By Year 5, modeled invoices rise to $2,730 for water, $7,800 for fire, and $3,850 for mold. That helps owner income only if the crew stays on schedule and the job is scoped right. Bigger tickets can improve profit per job, but they also need tighter project management and more working capital to cover labor, materials, and delays.

Track Job Mix by Service

Measure average invoice by service line each month, then compare hours billed, hourly rate, and collected cash. If a service brings higher revenue but keeps jobs open longer or creates more rework, it can still hurt take-home pay. One clean rule: revenue growth is good only when cash moves fast enough to fund the next job.

- Track water, fire, and mold separately

- Watch invoice per billable hour

- Review aged receivables weekly

- Price bigger jobs for admin time

2

Gross Margin Control

Gross Margin Control

Gross margin is what’s left after direct job costs. In disaster cleanup, those costs include materials, overtime and specialist subcontractors, fuel and vehicle maintenance, and referral commissions. The model shows a 255% project cost load in Year 1, then 195% in Year 5, so owner income only improves if scope stays tight and rework stays low.

Here’s the risk: overtime, missed documentation, and redo work can wipe out the margin gain fast. If those costs drift, the business may still book sales but have less cash left for salaried payroll, overhead, debt service, and owner draw.

Hold Scope Tight

Track each job’s direct cost % against invoice value: 10% materials, 7% overtime and specialist subcontractors, 6% fuel and vehicle maintenance, and 25% referral commissions in Year 1. Use one job sheet for estimate, field notes, and invoice so misses show up before billing closes.

One clean rule helps: if a job needs extra labor, extra miles, or a rework visit, flag it before the margin is gone. Year 5 only helps if the team keeps documentation tight and stops scope creep from turning profitable work into break-even work.

- Watch direct cost % on every job

- Flag overtime before approval

- Match field notes to invoices

3

Crew Utilization And Capacity

Crew Utilization And Capacity

Crew utilization is how much of each technician and project manager’s time turns into billable restoration work. In this model, certified restoration technicians grow from 2 FTEs in Year 1 to 6 FTEs in Year 5, and project managers rise from 0.5 FTE to 2 FTEs. If demand outpaces crew time, overtime and owner work rise; if labor sits idle, payroll drains profit.

The owner’s income depends on matching emergency calls to crew slots fast enough to finish jobs, bill them, and collect cash. Here’s the quick math: more usable hours usually means more completed jobs and better gross margin, but only if scheduling stays tight. Understaffing boosts overtime and stress; overstaffing burns payroll during slow weeks. Both cut take-home pay.

Fill the Schedule, Not Just the Payroll

Track billable hours per FTE, overtime, and unfilled shifts by week. Use those inputs to decide when to add techs or project managers, and when to hold back. The goal is simple: keep enough emergency coverage to respond fast, but not so much payroll that slow weeks eat margin.

Measure the gap between available crew time and booked work. If response times slip, jobs get lost; if crews are idle, cash flow weakens. Better dispatch planning turns demand into completed, billable, profitable work, which is what funds owner pay after labor, overhead, and reserves.

4

Insurance Billing And Collections Timing

Insurance Cash Lag

Insurance work can look profitable before the money hits the bank. The hard part is the gap between documentation, approvals, and receivables, which can delay owner pay even when the job is already earned. In this model, breakeven is Month 5, but the minimum cash need is $747,000 in Month 6. Profit is not cash.

For the owner, that means distributions depend on collection speed, not just job margin. If follow-up slows or paperwork is incomplete, cash stays trapped in accounts receivable, so the business may show income on paper while still protecting payroll, reserves, and other obligations. EBITDA is not money you can draw until collections clear.

Track Cash, Not Just Invoices

Measure each claim from job close to cash collected, and break out delays by documentation, adjuster approval, and follow-up. If one step slips, owner pay slips with it. The useful question is simple: how much of the billed work is still unpaid, and for how long?

- Invoice date and cash date

- Approval date and missing docs

- Open receivables by age

- Cash reserve above $747,000

Set owner draws only after cash on hand stays above the $747,000 Month 6 minimum and after reserves cover payroll, fuel, materials, and other obligations. If collections lag, hold distributions even when the income statement looks strong.

5

Overhead, Equipment, And Reserve Discipline

Overhead, Equipment, And Reserve Discipline

Fixed overhead is $8,600 per month, or $103,200 per year, before payroll and marketing. That means the business must cover rent, admin, insurance, and other base costs before the owner sees real take-home. If project cash is tight, owner pay should wait until the overhead is covered and the reserve is funded.

The bigger drag is equipment. Early capex totals $223,000 for vehicles, extraction gear, dehumidifiers, air movers, safety stock, tools, containment gear, testing equipment, and office setup. One line item can’t starve the rest: if trucks or drying gear sit idle, billable jobs slow down and owner income falls fast.

Protect Cash Before Paying Yourself

Track three numbers every month: fixed overhead, equipment replacement spend, and cash reserve balance. Here’s the quick math: if monthly overhead is $8,600, the business must clear that first, then keep enough cash to repair or replace trucks and gear before any owner draw. Pay the owner, but don’t drain working cash.

- Watch repair bills and downtime.

- Set a reserve before drawing profit.

- Separate owner pay from reinvestment.

- Fund trucks, gear, and safety stock first.

What this estimate hides is timing risk. Disaster cleanup cash often lags the work, so a profitable month can still leave the bank short if equipment fails or a job needs fast rebuild spend. If reserve discipline slips, the owner ends up financing operations out of personal pay.

6

Compare lean, base, and high owner-income scenarios using the model assumptions

Owner income scenarios

Owner income moves with ramp, CAC, payroll, and cash needs. Year 1 is tight, Year 3 supports scale, and Year 5 is the strongest draw case after reserves and reinvestment.

| Scenario | Low CaseLean ramp | Base CaseModeled base | High CaseUpside scale |

|---|---|---|---|

| Launch model | This case assumes a Year 1 ramp with slower volume and tighter cash. | This case assumes Year 3 scale with steadier demand and better unit economics. | This case assumes Year 5 scale with stronger demand and the best owner income path. |

| Typical setup | It uses $25,000 of marketing, $500 CAC, a $90,000 owner salary, $239,000 EBITDA, Month 5 breakeven, and a $747,000 minimum cash need. | It uses $60,000 of marketing, $400 CAC, 775% gross margin before salaried payroll, and $2.68 million EBITDA with heavier payroll. | It uses $100,000 of marketing, $350 CAC, 805% gross margin before salaried payroll, and $7.84 million EBITDA with distributions after reserves, debt, taxes, and reinvestment. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $90,000 salary onlyLean take-home | Salary plus modest distributionsCore case | Salary plus larger distributionsUpside only |

| Best fit | Use this to stress test the launch year when cash is tight and distributions are limited. | Use this as the main planning case for an operating business with real job flow and growing staff. | Use this to test upside once the business is mature and can fund growth before paying out cash. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Disaster Cleanup Porter's Five Forces Analysis

- Disaster Cleanup BCG Matrix

- Disaster Cleanup Business Model Canvas

- 7 Essential KPIs for Disaster Cleanup Businesses

- Disaster Cleanup Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Disaster Cleanup Profitability

- How Much Does It Cost To Run A Disaster Cleanup Business Each Month?

- Disaster Cleanup Startup Costs: $747k First-Year Cash Plan

- Disaster Cleanup Financial Model Template in Excel

- How to Open a Disaster Cleanup Business in 8 to 16 Weeks

- How to Write a Disaster Cleanup Business Plan in 7 Steps

- Disaster Cleanup Marketing Mix

- Disaster Cleanup Marketing Plan

- Disaster Cleanup Business Proposal

- Disaster Cleanup PESTEL Analysis

- Disaster Cleanup Pitch Deck Example Editable PPTX

- Disaster Cleanup Business SWOT Analysis

- Disaster Cleanup Value Proposition Canvas

Frequently Asked Questions

The model includes $90,000 per year for the owner-general manager Extra owner income depends on collections, reserves, debt, capex, and reinvestment EBITDA is modeled at $239,000 in Year 1 and $784 million in Year 5, but EBITDA is not the same as distributable cash