Owner income$90k

Owner income$90kHow Much Diverse Children's Books Owners Can Make With $304M Sales

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$90k  Net margin83%–86%

Net margin83%–86% Revenue for target pay$1.27M

Revenue for target pay$1.27M Business difficultyHard

Business difficultyHard

Key Takeaways

- Catalog growth only pays when titles move fast.

- Sales mix matters more than title count.

- Margin gains matter most after fixed costs.

- Cash stays trapped until costs and reserves clear.

Owner income$90kNet margin83%–86%Revenue for target pay$1.27MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, operating costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to stress-test the model for Diverse Children's Books?

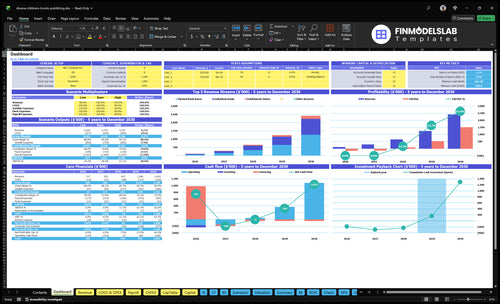

Open the dashboard in Diverse Children's Books Financial Model Template to check income outputs, assumptions, and scenario tabs for title catalog, sales mix, unit economics, repeat buyers, CAC, marketing spend, payroll, fixed costs, cash reserves, and owner take-home.

Owner-income model highlights

- Owner income scenarios included

- Revenue from $1,272k to $304M

- EBITDA from -$1,257k to $214M

- Month 27 breakeven

- Month 48 payback

What changes when scaling a diverse children’s books business?

When Diverse Children's Books scales, the founder shifts from author-operator to publisher-manager. Payroll rises from $150k in Year 1 to $298k in Year 5, and marketing rises from $50k to $140k; the institutional sales mix also grows from 10% to 25%. That can lift EBITDA (earnings before interest, taxes, depreciation, and amortization), but it also means more cash tied up, more workload, more inventory risk, and bigger reserves before owner take-home improves.

Role changes

- Founder manages catalog growth

- School outreach becomes a sales engine

- Library orders add volume

- Contractors and fulfillment need oversight

Money changes

- Payroll grows to $298k

- Marketing grows to $140k

- Institutional sales reach 25%

- Reserves matter before owner take-home

How much revenue is needed for children’s book publisher owner pay?

For Diverse Children's Books, owner pay depends on margin and overhead, not revenue alone. The model shows $1.272M in revenue and about $1.049M in gross profit, but $2.306M in marketing, fixed costs, and payroll can still leave EBITDA at about -$1.257M by Year 3. At $7.833M in revenue, the model’s stated 841% margin produces about $2.542M EBITDA after $4.046M of operating load, so owner pay is still cash-based and reserves plus inventory come first.

What drives pay

- $1.272M revenue, $1.049M gross profit

- $2.306M operating load can erase pay

- EBITDA can still be -$1.257M

- Revenue alone does not fund owner pay

Cash rule for the owner

- $7.833M revenue lifts EBITDA to $2.542M

- That still follows $4.046M in load

- Pay after reserves and inventory needs

- Cash-based pay is safer than profit-based pay

How do children’s book profit margins affect take-home?

For Diverse Children's Books, take-home improves when direct-cost margin widens: as wholesale book cost falls from 100% to 80%, packaging from 15% to 11%, transaction fees from 25% to 21%, and fulfillment from 35% to 31%, margin moves from 825% to 857%. Here’s the quick math: each 1 point of margin is worth about $13k at Year 1 revenue and $304k at Year 5 revenue, so print choices, direct checkout, wholesale discounts, paid ads, and creative contractors all change cash available for owner draws. If you want the startup-cost side first, see How Much Does It Cost To Open, Start, Launch Your Diverse Children's Books Business?

Margin drivers

- Wholesale drops from 100% to 80%

- Packaging drops from 15% to 11%

- Transaction fees drop from 25% to 21%

- Fulfillment drops from 35% to 31%

Take-home impact

- 1 margin point equals about $13k Year 1

- 1 margin point equals about $304k Year 5

- Direct checkout can improve cash flow

- Paid ads and contractors hit owner draws

Want the six drivers that move owner income?

1

$1.27M-$3.04MCatalog Size

More titles widen the buyer base and lift revenue fastest, so this is the biggest owner-cash lever.

2

0.5-0.9/moSales Velocity

Repeat buyers moving from 20% to 40% and 0.5 to 0.9 orders a month raise sales without paying for every order again.

3

10%-25%Channel Mix

Growing institutional orders to 25% shifts volume toward steadier demand and can smooth cash flow.

4

82.5%-85.7%Unit Margin

Low book, packaging, fee, and shipping costs keep most of each sale, so more revenue turns into profit.

5

$20->$14Marketing Efficiency

CAC falling from $20 to $14 means each new customer costs less, which improves payback and take-home cash.

6

$2.31M-$4.69MOverhead Control

Keeping fixed operating load in range is what gets the model to Month 27 breakeven and protects owner cash after reserves.

Diverse Children's Books Core Six Income Drivers

Catalog Size And Backlist Strength

Catalog Size

A bigger catalog only helps if each title keeps selling. Backlist means older titles that still move, and that’s where classroom relevance, cross-sells, and themed bundles can raise owner income. The real driver is sales per title, not title count alone. If repeat buyers rise from 20% to 40%, the same catalog can produce steadier recurring revenue.

The cash risk is upfront spend on inventory, licensing, editing, illustration, sensitivity reading, and launch work. If titles move slowly, cash gets tied up in stock while founder pay stays fixed at $90k. That means title-level break-even matters more than adding more books.

Track Sales Per Title

Measure each title as its own mini business. A title helps income only when it earns back its launch cost and keeps bringing buyers into repeat orders, classroom buys, and bundles.

- Rank titles by sales per title.

- Track repeat buyers monthly.

- Cut slow movers fast.

- Bundle books that already sell together.

Use the catalog to build recurring demand, not just more SKUs. If repeat buyers do not move toward 40%, more inventory can lower cash and delay owner draws.

1

Sales Velocity By Channel

Sales Velocity By Channel

This driver is the pace of orders across parents, educators, schools, libraries, bookstores, events, and direct online sales. It affects owner income because more units only help if they turn into cash fast enough to cover marketing, fulfillment, and fixed costs before profit is drawn out.

The model moves from 4,000 orders in Year 1 to 64,000 orders in Year 5. The institutional mix rises from 10% to 25%, which can steady volume but may slow cash collection and squeeze margin. The big risk is mistaking broad interest for repeatable conversion; the strongest lift shows up when CAC falls from $20 to $14.

Measure Channel Speed, Not Just Demand

Track orders by channel, CAC by channel, and days from order to cash. That tells you whether volume is actually usable profit or just busy work. If institutional orders grow, separate them from direct sales so you can see the cash lag and the margin hit clearly.

- Count orders weekly by channel

- Split direct and institutional CAC

- Watch cash timing on school orders

- Test repeat buying before scaling ads

Here’s the quick math: a 30% CAC drop, from $20 to $14, makes each order easier to turn into contribution profit. That matters most when volume is real, not just seasonal. If channel mix shifts toward schools and libraries, keep enough cash reserved to cover slower payment cycles.

2

Unit Economics And Gross Margin

Gross Margin by Channel

For children’s books, gross margin is what’s left after book cost, fulfillment, platform fees, and wholesale discounts. The model shows direct-cost margin moving from 82.5% to 85.7%, so a small mix shift can change cash available for payroll and owner pay.

Here’s the quick math: at $304M Year 5 revenue, a 1-point margin move is about $304k before overhead. Direct bundles can lift average order value, but wholesale and distributor sales usually bring less cash per sale and slower money in. What this hides: cash timing matters as much as margin.

Improve Margin Mix

Measure margin by format, order type, and channel. Track direct checkout, bundle rate, wholesale discount, and shipping cost on every order so you can see which path funds owner income.

- Separate direct and wholesale margin.

- Price bundles against postage.

- Watch platform fees monthly.

- Forecast cash, not just revenue.

If direct bundles raise order value without lifting fulfillment cost too much, cash for reinvestment and draw improves faster. If wholesale share rises, expect lower cash per sale and tighter working capital before payroll.

3

Marketing Efficiency And CAC

Marketing Efficiency and CAC

Marketing only lifts owner income when paid spend turns into profitable orders and repeat buyers. Here, annual marketing rises from $50k to $140k, while CAC improves from $20 to $14 because new customers rise from 2,500 to 10,000. That’s better efficiency, but it still only works if the orders cover fulfillment and overhead fast enough.

The real risk is spending ahead of contribution profit and burning cash before repeat sales show up. Email lists, reviews, educator outreach, partnerships, and author visits matter because they can lower paid dependence and improve payback speed. If CAC slips, owner draws get squeezed even if top-line sales look strong.

Track CAC by channel, not just total spend

Measure CAC as marketing spend divided by new customers, then split it by channel. Here’s the quick math: $50k / 2,500 = $20 and $140k / 10,000 = $14. That’s the benchmark to beat. If one channel brings cheap customers but weak repeat buying, it may still hurt take-home income.

- Track new customers by channel.

- Track repeat purchase rate.

- Track payback period by cohort.

- Track revenue from email and referrals.

Use reviews, educator outreach, partnerships, and author visits to pull more demand from low-cost channels. The goal is simple: keep CAC falling while repeat orders rise, so paid spend supports cash flow instead of draining it.

4

Production And Creative Cost Recovery

Title-Level Cost Recovery

For a children’s book business, production and creative spend only helps owner income when each title earns back its upfront cost. That cost can include illustration, editing, design, sensitivity reading, licensing, ISBNs, inventory, website content, and launch assets. With $68k in startup cash items already planned, the owner’s take-home cash stays pressured until those dollars are recovered from book sales.

Here’s the key issue: if creative spend is treated like a sunk cost, the business can look “busy” while distributions stay blocked. The owner should track title-level break-even and not confuse revenue with cash that is safe to withdraw. If founder pay is set at $90k, recovery timing matters even more because early profit has to clear both title costs and overhead before cash can be drawn.

Track Payback by Title

Measure each book separately: total creative cost, unit gross margin, units sold, and cash recovered. Split the upfront spend into the biggest buckets so you can see what must be earned back first, like $25k inventory, $15k website development, and $5k marketing content. That keeps the owner from over-ordering titles that won’t pay back fast enough.

Use a simple rule: do not expand launches until the current title has covered its own cash outlay. Watch sell-through, reorder timing, and gross profit by title, then compare that to the recovery schedule. One clear metric: cash recovered ÷ total title cost. When that ratio lags, owner distributions should wait.

5

Overhead, Reserves, And Reinvestment Discipline

Overhead, reserves, and draw discipline

High gross margin does not mean free cash. With $306k/year in fixed costs, payroll rising from $150k to $298k, and marketing rising from $50k to $140k, operating profit gets consumed fast, so owner pay has to wait for cash, not just paper profit.

Here’s the quick math: the model shows a $520k minimum cash requirement and Month 48 payback. That means reserves, inventory, taxes, debt service, and new-title reinvestment come before extra draws. Operating profit is not the same as cash you can safely take home.

Protect cash before owner draws

Track three numbers every month: cash on hand, reserve target, and planned reinvestment. If cash drops below the $520k floor, pause draws and protect working capital first. That keeps the business able to buy inventory, fund taxes, and pay debt without forcing a rushed sale or a credit crunch.

- Set a fixed owner draw policy.

- Review reserves before each payout.

- Budget new titles separately.

- Keep tax cash out of profit.

6

Compare low, base, and mature owner-income scenarios

Owner income scenarios

Owner income shifts as the model moves from Year 1 cash burn to Year 3 profit and Year 5 scale. Marketing, repeat orders, and staffing decide when draws start.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the Year 1 cash-burn case, where the founder stays on the modeled $90,000 salary and takes no extra draw. | This is the Year 3 modeled case, where the business turns EBITDA-positive and the founder can start looking at small draws. | This is the Year 5 scale case, where stronger cash flow can support larger owner distributions before taxes and reinvestment. |

| Typical setup | Year 1 uses $50,000 marketing, 20% repeat customers, 1.20 units per order, and a lean staff build while EBITDA stays negative. | Year 3 assumes $100,000 marketing, 30% repeat customers, 1.30 units per order, and $86,000 EBITDA with a fuller team in place. | Year 5 assumes $140,000 marketing, 40% repeat customers, 1.40 units per order, and $1.513 million EBITDA with a fully built team. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $90k salary onlyLow Case | Salary plus modest drawBase Case | Salary plus distributionsHigh Case |

| Best fit | Use this if you want the downside cash plan and need to see how long the founder can wait for distributions. | Use this as the core plan if you want the first realistic window for owner distributions. | Use this to test upside and how much cash the founder can pull after reserves and reinvestment. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Diverse Children's Books Porter's Five Forces Analysis

- Diverse Children's Books BCG Matrix

- Diverse Children's Books Business Model Canvas

- 7 Essential KPIs to Scale Diverse Children's Books

- Diverse Children’s Books Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Diverse Children's Books Profitability

- How to Manage Monthly Running Costs for Diverse Children's Books

- Diverse Children’s Books Startup Costs: Plan For $520K

- Diverse Children's Books Financial Model Template in Excel

- How to Start a Diverse Children’s Book Business in 3–9 Months

- How to Write a Business Plan for Diverse Children's Books

- Diverse Children's Books Marketing Mix

- Diverse Children's Books Marketing Plan

- Diverse Children's Books Business Proposal

- Diverse Children's Books PESTEL Analysis

- Diverse Children's Books Pitch Deck Example Editable PPTX

- Diverse Children's Books Business SWOT Analysis

- Diverse Children's Books Value Proposition Canvas

Frequently Asked Questions

The model includes $90,000 in annual founder pay, but extra take-home depends on cash flow Year 1 revenue is about $127,200 with about -$125,700 EBITDA, so distributions are not supported early By Year 5, revenue reaches about $304 million and EBITDA reaches about $214 million before taxes, reserves, debt, and reinvestment