Owner income$80k

Owner income$80kHow Much DIY Craft Kit Owners Can Make: $80K Salary, Month 34 Breakeven

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$80k  Net margin-76%

Net margin-76% Revenue for target pay$200k

Revenue for target pay$200k Business difficultyHard

Business difficultyHard

Key Takeaways

- Higher kit prices lift AOV, but can hurt conversion.

- Volume only works when margins stay positive.

- Materials, packaging, and fulfillment drop from 99% to 40%.

- Repeat customers cut CAC pressure as orders grow.

Owner income$80kNet margin-76%Revenue for target pay$200kBusiness difficultyHardWant to test your craft kit owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will move with sales volume, margin, payroll, taxes, and reserve policy.

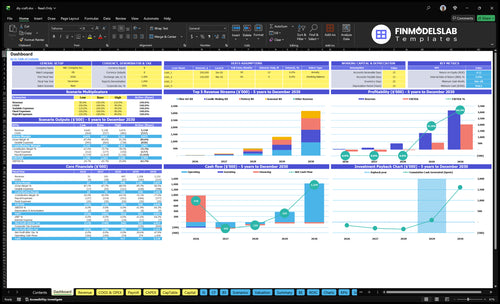

Want a cleaner view of the DIY Craft Kits forecast and owner income?

The dashboard in DIY Craft Kits Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions; open the model. Charts show EBITDA, cash, breakeven in Month 34, payback in Month 49, Year 1 EBITDA of -$152,000, and Year 4 EBITDA of $556,000.

Owner-income model highlights

- Owner income view

- EBITDA and cash charts

- Scenario tests for planning

- Not guaranteed results

What changes when scaling a DIY craft kit business?

Scaling DIY Craft Kits only works if margin stays intact. Marketing rises from $15,000 in Year 1 to $150,000 in Year 4, CAC improves from $35 to $28, repeat customers grow from 25% to 50%, and units per order move from 110 to 125.

Here’s the catch: payroll shifts from founder plus a half-time designer to added marketing, operations, and customer service roles, so higher revenue can still lower owner take-home if packing labor, returns, ad costs, or excess inventory climb faster than contribution profit. Simple rule: grow sales only when each order still leaves room after fulfillment and ads.

What scales

- Marketing jumps from $15,000 to $150,000

- CAC improves from $35 to $28

- Repeat buyers rise from 25% to 50%

- Units per order rise from 110 to 125

What can break

- Payroll adds more roles

- Packing labor can outrun revenue

- Returns cut contribution profit

- Excess inventory traps cash

Can you make a living selling DIY craft kits?

Yes, you can make a living with DIY Craft Kits, but not from operating profit right away. In the model, founder pay is $80,000/year from Month 1, yet EBITDA is negative in Years 1–3, so full-time income depends on funding, volume, and tighter systems. By Year 5, the model assumes CAC drops from $35 to $25 and repeat customers rise from 25% to 55%, so a part-time start may avoid payroll strain while scaled ecommerce needs fulfillment labor, inventory controls, and cash reserves.

What has to work

- $80,000 founder salary starts Month 1

- Years 1–3 stay EBITDA negative

- Volume must scale before pay feels safe

- Part-time can reduce payroll pressure

What improves the odds

- CAC drops from $35 to $25

- Repeat buyers rise from 25% to 55%

- Fulfillment labor becomes a real cost

- Cash reserves protect inventory buys

How many DIY craft kits do I need to sell to make money?

At Year 1 unit economics, DIY Craft Kits needs about 505 kits/month to cover overhead, or about 1,648 kits/month to cover overhead plus a $6,667/month founder salary. The core math behind What Is The Most Important Metric To Measure The Success Of Your DIY Craft Kits Business? is simple: $51.70 AOV minus 19.9% variable costs and $35 CAC leaves only about $6.42 per first order, so breakeven lands in Month 34 under the researched assumptions.

Unit Math

- Kit price: $47

- Units/order: 1.10

- AOV: $51.70

- Pre-CAC margin: 80.1%

Sales Targets

- CAC: $35/order

- Profit/order: $6.42

- Overhead: 505 kits/month

- Salary included: 1,648 kits/month

Want to see what drives craft kit owner income?

1

$52-$70Kit Pricing

Weighted AOV rises from about $51.70 in Year 1 to $70.14 in Year 5, so each order carries more gross profit before fixed costs.

2

1.10-1.30Order Size

Units per order climb from 1.10 to 1.30, so each checkout produces more revenue without a second acquisition cost.

3

25%-55%Repeat Rate

Repeat customers grow from 25.0% to 55.0% of new buyers, and that lifts lifetime order count without paying full CAC again.

4

$35-$25CAC

Customer acquisition cost falls from $35 to $25, so more of each marketing dollar turns into take-home profit.

5

13%-10%Materials

Raw materials and packaging drop from about 12.9% to 10.0% of revenue, which widens gross margin on every kit.

6

7%-4%Fulfillment

Shipping and fulfillment costs fall from 7.0% to 4.0%, so more gross profit survives the trip to the customer.

DIY Craft Kits Core Six Income Drivers

Kit Pricing And Average Order Value

Kit Pricing and AOV

For DIY craft kits, price per kit and units per order set revenue per customer. In the provided model, weighted kit price rises from about $47 in Year 1 to about $5,395 in Year 5, while units per order rise from 110 to 130, lifting AOV from about $5,170 to $7,014. That can grow profit fast if fulfillment and materials do not rise at the same pace.

The risk is simple: if price moves faster than perceived value, conversion can fall. Bundles, seasonal kits, and add-ons can raise revenue without the same fixed overhead increase, but only if customers still see the box as worth the price. One clean rule: raise AOV only when the offer still feels easy to buy and easy to gift.

Raise AOV Without Breaking Conversion

Track weighted kit price, units per order, AOV, and conversion rate by offer type. Then test bundles, seasonal drops, and add-ons one step at a time. Here’s the quick math: if AOV rises but conversion slips, revenue may stall even when headline pricing looks stronger. What this estimate hides is the full cost of customer hesitation, refunds, and slower sell-through.

Use a simple control list: price, bundle mix, add-on attach rate, and conversion by channel. Keep the first offer easy to understand, then stack higher-value options after trust is built. If pricing changes outpace product photos, reviews, or project outcomes, owner income can drop even with higher sticker prices because fewer orders close and cash comes in slower.

1

Unit Sales Volume

Unit Sales Volume

Unit sales volume is the number of kits sold. It only improves owner income when contribution margin stays positive, meaning there is money left after CAC, materials, packaging, fulfillment, fixed costs, and payroll. With a $15,000 Year 1 marketing budget and $35 CAC, that supports about 429 new customers before repeat orders.

The key inputs are orders, price, unit cost, and packing capacity. If the business buys too much stock or pays to ship unprofitable orders, more volume can drain cash instead of paying the owner. One clean rule: grow units only when each box still helps cover overhead and take-home pay.

Track Profit Per Order First

Measure profit per order as sale price minus CAC, materials, packaging, fulfillment, and payment fees. If that number is negative, more volume just scales the loss. Use weekly demand forecasts so inventory, labor, and shipping match actual orders, not hope.

Watch three controls: inventory turns, packing capacity, and repeat orders. If packing falls behind, cash gets trapped in stock and rush shipping. If repeat buyers rise, the same acquisition spend supports more revenue, but only if the next kits are already in stock and ready to ship.

- Forecast units every week.

- Stop ads on weak-margin orders.

- Match stock to pack capacity.

- Track repeat orders monthly.

2

Material And Packaging Costs

Material And Packaging Costs

Each kit’s bill of materials (BOM) and box cost set gross margin. If raw materials stay near 99% of revenue in Year 1, there is almost no room left for shipping, labor, or owner pay; by Year 5, that drops to 80%, which gives the business more cash to keep.

This driver uses units sold, supplier price, pack-out parts, and defect rate. Packaging matters too: moving from 30% to 20% improves margin, but weak inserts or missing parts can trigger refunds, reships, and bad reviews, which hit profit and cash fast.

Protect Margin Per Kit

Track cost per kit, packaging cost per order, and the share of orders with missing or damaged parts. Batch buys, standardize parts, and renegotiate supplier terms so the 80% material target and 20% packaging target hold as volume grows. One bad box can erase the profit from several clean orders.

Build a simple QC check before shipping: count parts, test inserts, and inspect box strength. If defect rate rises, forecast more refunds and reships, because those hidden costs cut take-home income even when sales look healthy.

3

Customer Acquisition Cost

Customer Acquisition Cost

Customer acquisition cost (CAC) is what you spend to win one new buyer, so it sets how much of the first order is left after marketing. Here, marketing spend rises from $15,000 in Year 1 to $225,000 in Year 5, while CAC improves from $35 to $25. That implies about 429 new customers at Year 1 spend and 9,000 at Year 5 spend, before repeat orders.

For craft kits, revenue growth alone is not enough if CAC eats the first-order margin (profit left after the first box ships) before repeat purchases arrive. Paid social, visual search, marketplace promotions, influencer campaigns, and email capture all change profit per order, cash timing, and owner pay. If CAC stays above first-order margin, growth can look strong but still दब pressure on cash flow.

Control CAC by channel

Track CAC by channel, campaign, and cohort. Use CAC = marketing spend ÷ new customers, then compare it with first-order margin after materials, packaging, and fulfillment. If a channel brings buyers who do not repeat, it can still hurt cash flow even when sales rise.

- Measure CAC by source weekly.

- Track first-order margin per order.

- Test email capture against paid ads.

- Watch repeat orders before scaling spend.

The key question is simple: does one new customer earn back acquisition cost before the second order? If not, cut wasted spend, raise conversion, or shift budget to channels that bring repeat buyers. That protects operating cash and the owner’s draw.

4

Repeat Purchase Rate

Repeat Purchase Rate

Repeat purchase rate matters because it lowers reliance on paid acquisition. In this model, repeat customers rise from 25% of new customers in Year 1 to 55% in Year 5, while customer life stretches from 12 to 36 months. Average repeat orders per month climb from 0.25 to 0.45, so the same customer base can drive more revenue and steadier owner pay.

The hidden risk is cadence. If themed kits, seasonal drops, or subscriptions slow down, repeat buyers run out of reasons to come back. Then the business leans harder on new paid customers, which makes cash flow and profit swing more with ad costs and launch timing.

<

div class="tips-box">

Track Reorders By Signup Month

Measure reorders by signup month and watch repeat share, months retained, repeat orders per month, and average order value (AOV). More repeats mean fewer new paid customers are needed to hit the same revenue, which helps protect owner draw. Keep inventory and content cadence in step, or the repeat loop breaks.

- Track repeat rate monthly by signup month.

- Test themed series and seasonal drops.

- Forecast stock before each launch.

5

Fulfillment Efficiency And Owner Time

Fulfillment Efficiency And Owner Time

When fulfillment runs hot, the owner’s income gets squeezed fast. Here, fulfillment costs fall from 70% of revenue in Year 1 to 40% in Year 5, so every process gain protects gross margin. If packing is slow or messy, shipping and rework eat the cash that should pay the owner.

Don’t treat unpaid packing as free. If the owner is picking, packing, and shipping, that labor should be priced into the model, or take-home income looks better than it is. Ops payroll also starts later: a $45,000 role at 0.5 FTE (half-time) in Year 2 and 1.0 FTE (full-time) from Year 3 onward.

Price Packing Labor Before You Scale

Track order count, pack time per order, shipping cost, reship rate, and owner hours. That is the real input set for fulfillment margin. Batching work, using packing stations, shipping software, and clear pick lists cuts waste and helps the margin move toward the 40% Year 5 level.

- Charge for every packing hour.

- Measure cost per shipped order.

- Cut picks, touches, and rework.

- Staff before owner burnout hits.

If order volume grows before those controls are in place, cash flow gets tied up in labor and postage, and the owner’s draw gets pushed back even when sales are rising.

6

Compare lean, base, and growth craft kit owner income scenarios

Owner income scenarios

Owner income changes quickly here because early marketing, payroll, and studio costs outrun sales before the model reaches breakeven in Month 34 and payback in Month 49.

| Scenario | Low CaseDownside case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | The low case stays under pressure from weak volume and a slow repeat loop, so owner pay stays tight. | The base case pays the founder $80,000 and runs negative EBITDA of $152,000 in Year 1, $178,000 in Year 2, and $48,000 in Year 3 before turning positive in Year 4. | The high case assumes stronger kit mix, lower CAC, and more repeat orders, which lifts owner take-home after fixed costs. |

| Typical setup | Lower-priced kits, softer repeat buying, and fixed studio costs keep the business close to a salary-only outcome. | Studio rent, software, and payroll stay in place while the model works through Month 34 breakeven and needs about $417,000 of cash cushion by Month 36. | Higher-priced kits, better mix into Candle Making and Seasonal kits, and stronger repeat buying spread the same payroll over more gross profit. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Founder salary onlyIncome floor | Salary-supported break-evenCore plan | Salary plus upsideScale upside |

| Best fit | Use this to stress test cash flow if demand starts slower than planned. | Use this as the main planning case for budgeting owner pay and cash needs. | Use this to test what happens if demand and repeat buying run above the base plan. |

Planning note: These ranges are researched planning assumptions only, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- DIY Craft Kits Porter's Five Forces Analysis

- DIY Craft Kits BCG Matrix

- DIY Craft Kits Business Model Canvas

- Tracking 7 Key Financial Metrics for DIY Craft Kits

- DIY Craft Kits Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Profitability for DIY Craft Kits

- Analyzing the Running Costs to Operate a DIY Craft Kits Business

- DIY Craft Kits Startup Costs: $39K CAPEX To $417K Cash Need

- DIY Craft Kits Financial Model Template in Excel

- How To Open A DIY Craft Kits Business In 6 To 12 Weeks

- How to Write a DIY Craft Kits Business Plan: 7 Actionable Steps

- DIY Craft Kits Marketing Mix

- DIY Craft Kits Marketing Plan

- DIY Craft Kits Business Proposal

- DIY Craft Kits PESTEL Analysis

- DIY Craft Kits Pitch Deck Example Editable PPTX

- DIY Craft Kits Business SWOT Analysis

- DIY Craft Kits Value Proposition Canvas

Frequently Asked Questions

The researched model includes an $80,000 founder salary, but early profit does not support that on its own EBITDA is -$152,000 in Year 1, -$178,000 in Year 2, and -$48,000 in Year 3 The business reaches breakeven in Month 34, so early owner pay needs funding or reserves