Owner income$65k

Owner income$65kHow Much a Dog Trainer Owner Can Make: $65K Pay Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$65k  Net margin86%–90%

Net margin86%–90% Revenue for target pay$125k

Revenue for target pay$125k Business difficultyHard

Business difficultyHard

You’re not just asking what a trainer earns per hour you’re asking what the business owner can take home after costs In this five-year planning model, owner pay is modeled at $65,000 per year, with EBITDA, meaning earnings before interest, taxes, depreciation, and amortization, rising from $14,000 in Year 1 to $1124 million in Year 5 Actual dog trainer business income depends on pricing, client volume, service mix, capacity, local demand, reserves, and reinvestment

Owner income$65kNet margin86%–90%Revenue for target pay$125kBusiness difficultyHardWhat owner pay can your dog training numbers support?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Dog Trainer model?

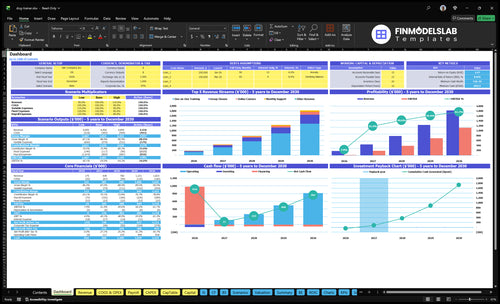

The Dog Trainer Financial Model Template shows revenue, EBITDA, breakeven, payback, and owner income—Year 1 EBITDA $14,000; Month 7 breakeven; 21-month payback.

Owner-income model highlights

- Assumptions and scenario tabs

- Revenue by service

- Payroll, capex, expenses

How much revenue does a dog trainer need to pay themselves?

If a Dog Trainer wants to pay themselves, use this formula: (owner pay + fixed overhead) ÷ 71%. With $65,000 owner pay and $23,400 fixed overhead, revenue needs are about $124,500; at $100,000 owner pay, it rises to about $173,800. That math assumes a 71% contribution margin after 14% direct costs, 12% marketing, and 3% payment processing, and it still leaves out taxes, reserves, debt, startup capex, and reinvestment.

Revenue math

- $65,000 pay needs $124,500 revenue

- $100,000 pay needs $173,800 revenue

- Use 71% contribution margin

- Subtract $23,400 fixed overhead first

Cash reality

- Taxes reduce take-home cash

- Reserves protect slow months

- Debt cuts distributable profit

- Startup capex needs cash too

What is a dog training business profit margin?

A Dog Trainer business can look very high margin if you stay in low-overhead services; see How Much Does It Cost To Open A Dog Trainer Business? for the cost stack behind the math. Using the figures provided, gross margin is 86% in Year 1 and 90% in Year 5 after materials, supplies, fuel, and maintenance, while contribution margin rises from 71% in Year 1 to 808% in Year 5 after marketing and payment processing.

Margin math

- 86% gross margin in Year 1

- 90% gross margin in Year 5

- 71% contribution margin in Year 1

- 808% contribution margin in Year 5

Revenue mix

- $340 for four private hours

- $11,250 for 25 group-class hours

- $60 online courses

- $5,250 support board-and-train; separate facility, care, insurance, staffing

How much can a solo dog trainer make?

A solo Dog Trainer can pay the owner about $65,000/year at $85/hour only if it reaches about $124,500 in annual revenue, or 122 billable hours/month; here’s the capacity math behind What Is The Most Important Indicator Of Success For Dog Trainer Business?. A $100,000 owner-pay target needs about $173,800 in annual revenue, or roughly 170 billable hours/month, before admin, travel, consults, marketing, and cancellations.

Pay math

- $85/hour private training price

- $1,950/month fixed costs

- 71% contribution after variable costs

- $124,500 revenue supports $65,000 pay

Capacity check

- 122 billable hours per month

- 122 ÷ 25 = 4.9 active customers

- About 59 customer-months/year

- $173,800 revenue supports $100,000 pay

Which six drivers move dog trainer owner income most?

1

$85/$45Pricing

Private sessions at $85 an hour and group classes at $45 an hour raise revenue per booked hour, so EBITDA, reserves, and owner take-home move up fast.

2

$85 CACClient Volume

An $85 CAC means each new client has to earn back its cost quickly, so fuller schedules spread fixed costs and improve cash.

3

45/35/15/10Service Mix

Shifting the mix across one-on-one, group, online, and support work changes margin quality, and better mix lifts EBITDA without needing more owner hours.

4

2.5-4.5hUtilization

As active customers move from 2.5 to 4.5 billable hours a month, the same calendar produces more revenue and better cash reserves.

5

$1.95KOverhead

About $1,950 in monthly fixed costs keeps break-even at Month 7, so small savings drop straight to profit and owner take-home.

6

$65KStaffing

The $65,000 owner salary, plus later hires, sets how fast capacity can grow and whether the business keeps its 21-month payback on track.

Dog Trainer Core Six Income Drivers

Pricing And Package Design

Package Pricing

Higher package value lifts revenue per client and makes cash less jumpy. Here’s the quick math: private training is $85/hour for 4 hours, or $340 per package; group classes are $45/hour for 25 hours, or $11,250 as modeled; online courses are $120 with 0.5 modeled billable hours; monthly support is $35/hour for 15 hours.

This driver depends on session count, trainer expertise, outcome promised, and local competition. If prices stay too low, owner pay gets squeezed before demand is the issue. With $1,950/month fixed overhead, every package has to leave room for direct labor, payment fees, and a profit draw.

Price for Outcome

Track price per client, hours delivered, and gross margin by offer. Tie the fee to a clear result, like basic obedience or behavior change, and write the scope down so extra sessions do not leak margin. One clean rule: if the package needs more time than planned, the price was too low.

- Compare fees to local competitors.

- Track actual hours per package.

- Separate one-on-one and group scope.

Use package design to push more clients into higher-value programs and recurring support. That raises monthly cash, smooths bookings, and protects take-home income when lead flow slows. The best price is the one that covers delivery, overhead, and owner pay without forcing constant volume.

1

Client Volume And Conversion

Client Conversion

Revenue here depends on inquiries, consult close rate, referrals, repeat packages, and active customers — not raw leads. With marketing at $12,000 in Year 1 and $36,000 in Year 5, CAC improves from $85 to $55, which implies about 141 customers in Year 1 and about 655 in Year 5 if conversion holds.

Here’s the quick math: $12,000 ÷ $85 = 141, and $36,000 ÷ $55 = 655. Take-home income rises only if those customers keep buying enough billable time. Average billable hours per active customer rise from 25 to 45 monthly, so the upside is real, but overbooking can crush service quality and cancel the gain.

Track Close Rate and Load

Measure inquiries per month, consult-to-sale close rate, referral share, repeat-package rate, and active customers. That tells you whether marketing is producing paying clients or just more calls. If close rate weakens, higher ad spend will raise CAC fast and squeeze owner pay before revenue catches up.

Keep booked hours below what delivery can handle. When active customers move from 25 to 45 billable hours a month, use the schedule as the guardrail: sell only what can be delivered, and watch consult capacity, travel time, and follow-up work. One clean rule: fill the calendar, not the backlog.

- Track inquiries to paid clients.

- Watch CAC by channel.

- Count repeat packages monthly.

- Cap bookings at real capacity.

2

Service Mix

Service Mix

Service mix is the split between private sessions, group classes, online courses, and monthly support. In this model, one-on-one training drops from 45% to 35%, group classes rise from 35% to 45%, online courses rise from 15% to 35%, and monthly support rises from 10% to 30%. Because these offers can overlap, the real driver is revenue per booked hour, not just customer count.

This mix changes cash flow and owner pay fast. Private work uses more trainer time, while online and support can scale with less delivery labor, so margin can improve if pricing holds. Board-and-train can lift revenue, but it brings separate care labor, facility cost, insurance, and liability work. One line: the best mix is the one that fills time without crushing margin.

Track Mix by Margin

Measure each service by price per hour, delivery time, cancel rate, and direct labor cost. Also track how many add-ons attach to each client, since overlap can hide weak pricing. If online courses and monthly support are growing, check whether they raise recurring revenue or just add admin. Use gross margin, the money left after direct delivery costs, and booked hours per trainer as the two main scorecards.

Test mix shifts in small steps. Move clients from private sessions into group or online only when fill rates stay high and support tickets stay manageable. If you add board-and-train, separate the unit economics: care labor, space, insurance, and liability should each be priced in. What gets measured here is simple: mix, margin, and owner draw.

3

Schedule Capacity And Utilization

Schedule Capacity

Owner income is capped by billable hours, not just inquiries. In Year 1, the model uses 25 hours per active customer per month, rising to 45 by Year 5. Private programs usually need 40 to 50 hours, group classes 25 to 35, and support 15 to 25, so travel, admin, consults, and cancellations can eat pay fast.

Here’s the quick math: more booked hours only help if they are paid and delivered. A full calendar with weak fill rates or high cancellations lowers cash collected per week, while low travel time and tight routing lift margin. Utilization is the share of available time that turns into billable work, and that ratio drives the owner’s draw.

Track Billable Hours

Measure booked hours, billable hours, cancellation rate, class fill rate, travel time, and admin time each week. Split them by private work, group classes, and support, since each uses a different hour range. If classes are underfilled or sessions slip, you lose revenue without lowering fixed time costs.

Set a floor for filled seats and reschedule rules before the calendar fills up. Keep the schedule lean enough to protect owner energy, because burned-out trainers miss follow-ups and let rebook rates fall. The best plan is not the busiest calendar; it is the one with the most paid hours per day.

4

Cost Structure And Reserves

Cost Structure and Reserves

Costs hit take-home before the owner sees any distributions. This model carries $1,950 a month in fixed overhead, or $23,400 a year, plus Year 1 var iable costs of 14% direct costs, 12% marketing, and 3% payment processing. That leaves less room for owner pay unless pricing and volume cover the full cost stack.

By Year 5, direct costs fall to 10% and marketing to 7%, but processing rises to 22% in the model. The cash point matters too: the core model flags $844,000 minimum cash in Month 2, so the funding plan needs enough runway for early losses, not just launch spend.

Track Burn Before Pay

Measure gross margin by service, then subtract overhead and cash outflow before you think about owner draw. Here’s the quick math: every package must cover 14% direct cost, 12% marketing, 3% processing, and $1,950 monthly fixed overhead in Year 1. If any offer fails that test, it is diluting profit, not funding pay.

Build reserves around the Month 2 cash trough, not the first sale. Track cash monthly, separate launch capex from operating cash, and stress test funding against the $844,000 minimum cash flag. If onboarding or client ramp is slower than planned, owner income drops fast because fixed costs keep running.

5

Staffing And Owner Role

Owner Pay vs Payroll

Owner-operator profit is not the same as manager-owner income. If the owner also trains, the model keeps that role at $65,000 a year. Once payroll adds an assistant trainer, marketing coordinator, administrative assistant, and senior trainer, the wage bill rises to $86,000 in Year 2, $135,600 in Year 3, $179,400 in Year 4, and $222,600 in Year 5.

That payroll growth only helps if each hire lifts billable hours, keeps cancellations low, and protects service quality. If staffing grows faster than pricing or utilization, owner take-home drops even when the calendar looks full. One clean rule: hire for capacity, not comfort.

Track Labor Before You Hire

Watch the numbers that decide whether staff pay creates more income or just more overhead: billable hours per trainer, class fill rate, no-show rate, and revenue per labor dollar. Define the role first, then tie the hire to a clear output like more sessions, more classes, or faster admin turnaround.

- Keep owner salary separate from profit.

- Model added hours before each hire.

- Document training standards for every role.

6

Compare lean, established, and scaled dog trainer owner-income scenarios

Scenario table

Owner income moves with service mix, billable hours, and payroll. Low stays solo, base adds support, and high scales into a fuller team with stronger EBITDA.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This lower case is a solo Year 1 path with about $144,000 revenue and $14,000 EBITDA, so owner pay stays tight. | This modeled Year 3 path uses about $711,000 revenue and $388,000 EBITDA, so owner pay is supported by scale. | This stronger Year 5 path reaches about $1,696,000 revenue and $1,124,000 EBITDA, so owner pay has more room. |

| Typical setup | One-on-one training carries most sales, gross margin is 86%, direct and variable costs run 29%, and fixed overhead is $23,400. | The mix shifts toward group classes and online courses, gross margin is 88%, and payroll reaches $135,600. | Group classes, online courses, and monthly support carry the mix, gross margin reaches 90%, and payroll rises to $222,600. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $65,000 floorLow Case | $65,000 plus profitBase Case | $65,000 plus surplusHigh Case |

| Best fit | Use this to stress-test a lean solo plan and thin demand. | Use this as the main planning case for a growing, balanced operation. | Use this to test upside if demand and staffing both scale well. |

Planning note: These scenario figures are researched planning assumptions only, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Dog Trainer Porter's Five Forces Analysis

- Dog Trainer BCG Matrix

- Dog Trainer Business Model Canvas

- 7 Financial KPIs to Track for Your Dog Trainer Business

- Dog Trainer Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Dog Trainer Profitability and Boost Margins

- How Much Does It Cost To Run A Dog Trainer Business Monthly?

- How Much It Costs To Start A Dog Training Business: $584k Plan

- Dog Trainer Financial Model Template in Excel

- How To Start A Dog Training Business In 4 To 10 Weeks

- How to Write a Dog Trainer Business Plan: 7 Actionable Steps

- Dog Trainer Marketing Mix

- Dog Trainer Marketing Plan

- Dog Trainer Business Proposal

- Dog Trainer PESTEL Analysis

- Dog Trainer Pitch Deck Example Editable PPTX

- Dog Trainer Business SWOT Analysis

- Dog Trainer Value Proposition Canvas

Frequently Asked Questions

In this model, the owner is paid a planned $65,000 salary each year, plus any safe distributions EBITDA is $14,000 in Year 1, $388,000 in Year 3, and $1124 million in Year 5 Those figures are before taxes, debt service, reserves, and reinvestment, so they are not guaranteed take-home cash