Owner income$85k

Owner income$85kHow Much Can A Drag Queen Story Hour Events Owner Make On $164K Revenue?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$85k  Net margin37%

Net margin37% Revenue for target pay$85k

Revenue for target pay$85k Business difficultyHard

Business difficultyHard

Key Takeaways

- Paid bookings drive EBITDA growth from losses to profits.

- Average fees matter only when they cover all costs.

- Performer staffing protects quality but compresses margins fast.

- Owner role and reserves set the income ceiling.

Owner income$85kNet margin37%Revenue for target pay$85kBusiness difficultyHardWant to test your owner pay scenario?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

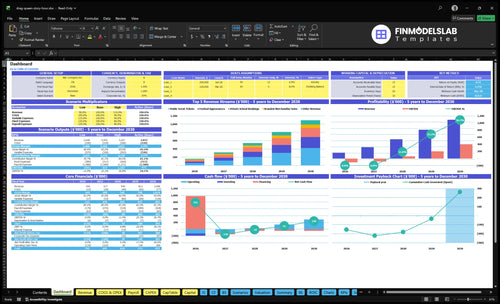

How does owner income look in the Drag Queen Story Hour Events model?

The Drag Queen Story Hour Events Financial Model Template dashboard shows assumptions, booking and ticket revenue, merch/book sales, concessions, costs, reserves, and owner take-home. Revenue rises from $164,000 to $1.096 million, EBITDA from -$110,000 to $402,000; breakeven lands in Month 26 and payback in Month 54. Open the model.

Owner-income model highlights

- Owner take-home forecast

- Breakeven in Month 26

- Payback in Month 54

How much can a Drag Queen Story Hour Events owner make per year?

A Drag Queen Story Hour Events owner can model $85,000 per year before tax as owner-operator pay, but there is no single universal salary; see How To Launch Drag Queen Story Hour? for launch context. Revenue scales from $164,000 in Year 1 to $1.096 million in Year 5, while EBITDA turns positive after Year 2.

Owner Pay

- Model salary: $85,000 before tax

- Year 1 revenue: $164,000

- Year 2 revenue: $317,000

- Year 3 revenue: $545,000

Profit Timing

- EBITDA: negative in Years 1–2

- Year 3 EBITDA: $60,000

- Year 4 EBITDA: $205,000

- Year 5 EBITDA: $402,000

Can a Drag Queen Story Hour Events business scale?

Yes—Drag Queen Story Hour Events can scale, but only if the owner stops doing every task and turns events into a repeatable system. An owner-as-performer protects margin but caps capacity; an owner-as-producer can book more dates, but adds performer and coordinator costs. In the model, scale reaches 12,000 tickets, 180 school bookings, and 60 festival appearances in Year 5, with breakeven in Month 26 and payback in Month 54.

Owner model

- Performer-led: higher margin, lower volume

- Producer-led: more bookings, more overhead

- 1 coordinator grows to 2

- Admin grows from 0 to 2 FTE

Scale drivers

- Partnerships unlock more bookings

- Routing cuts travel waste

- Availability limits event count

- Cost control decides payback timing

What should a Drag Queen Story Hour Events business charge?

Drag Queen Story Hour Events should price for the full event cost, not just the reading. A workable Year 1 guide is $25 public tickets, $850 school bookings, and $2,500 festival appearances; by Year 5, that moves to $35, $1,200, and $4,500. If the owner wants $85,000 pay, that means about $8,800 a month in revenue before overhead, so the early-year break-even need is higher.

Year 1 pricing

- $25 public tickets

- $850 school bookings

- $2,500 festival appearances

- Cover performer, prep, travel

Year 5 pricing

- $35 public tickets

- $1,200 school bookings

- $4,500 festival appearances

- Also fund insurance and reserves

Want to see the six owner-income drivers?

1

$164K-$1.1MPaid Bookings

More public, school, and festival bookings drive the jump from Year 1 revenue of $164,000 to Year 5 revenue of $1.096 million.

2

$25-$4.5KFee Growth

Ticket, school, and festival pricing all rise across the model, so a better fee mix lifts revenue without adding the same amount of labor.

3

18%-20%Performer Costs

Performer fees and payment charges keep direct costs near one-fifth of sales, so margin depends on keeping each booking efficient.

4

$85KOwner Salary

The $85,000 executive director salary is the founder's main draw, so the owner's role and staffing mix decide how much cash stays in the business.

5

$63.4KOverhead Buffer

Fixed overhead is $63,360 a year, and cash bottoms in Month 36, so reserve discipline protects take-home during uneven growth.

6

Off-modelGrant Funding

The source has no grant revenue line, so any grants or sponsorships should be modeled separately as upside, not base case.

Drag Queen Story Hour Events Core Six Income Drivers

Paid Booking Volume

Paid Booking Volume

More paid bookings are the main income swing here. Volume rises from 2,400 public tickets, 48 school bookings, and 12 festival appearances in Year 1 to 12,000 tickets, 180 school bookings, and 60 festival appearances in Year 5, and that’s the path from -$110,000 EBITDA to $402,000 EBITDA.

This only helps if staffing and admin keep pace. Inquiries do not equal paid contracts, so the real metric is booked-and-delivered events, not lead count. Institutional bookings also rise from 5 per month to 20 per month, which means sales follow-through and scheduling capacity can cap owner pay.

Track booked events, not leads

Build the forecast from paid tickets, school bookings, and festival appearances, then test whether the team can actually deliver them. If bookings grow but admin lags, cash comes in late, service quality slips, and repeat business weakens. That is how volume misses turn into lower EBITDA and smaller owner draws.

- Count paid contracts by channel.

- Track booked vs. delivered events.

- Watch institutional bookings per month.

- Match staff hours to event load.

1

Average Event Fee

Average Event Fee

This driver is the average money earned per event type. At $25 per public ticket, $850 per school booking, and $2,500 per festival appearance, the fee mix matters because each format has different cost pressure. If the fee does not cover prep, talent, travel, coordination, insurance, and risk planning, owner income gets squeezed even when events are busy.

Year 5 pricing rises to $35, $1,200, and $4,500. Festivals usually carry more revenue per appearance, while public events need enough ticket density to pay for the same effort. This is a planning variable, not a universal rate, so the real test is whether each booking still leaves enough gross margin to pay the owner after direct costs.

Price for Margin, Not Just Fill

Track average fee by format: public, school, and festival. Compare each one against the direct costs tied to that event, then watch which mix actually funds owner pay. A higher fee only helps if it survives staffing, travel, insurance, and admin time.

If school or festival work takes more setup, bake that into the quote. That keeps cash flow cleaner and avoids busy months that still leave little for the owner.

2

Performer Staffing Cost

Performer Staffing Cost

This driver covers performer pay, host coverage, and setup help. In this model, performer fees use 80% of revenue in Years 1 and 2, 85% in Years 3 and 4, and 90% in Year 5. That leaves very little room for owner pay unless pricing and volume are strong.

Owner income changes fast here: if the owner performs, they may keep more margin but hit a capacity wall; if they hire multiple performers or coordinators, delivery gets safer but the model shows a direct cost stack of 195% in Year 1 and 185% in Year 5. Fair pay protects quality, but understaffing can hurt repeat bookings.

Control Pay Before It Controls Profit

Track revenue per event, performer fee %, coordinator hours, and repeat booking rate. Then test whether flat pay, rev share, or a hybrid keeps labor inside the modeled band without lowering show quality. Here’s the quick math: on $1,000 of event revenue, an 80% performer fee leaves $200 before other direct costs.

Document who performs, who hosts, and who handles setup for each event. If the owner does all three jobs, income can rise short term, but capacity is the limit. If multiple hosts are needed, build that cost into the price first, because every extra paid role cuts the owner’s take-home cash.

- Track pay by event type.

- Price setup labor separately.

- Watch repeat bookings monthly.

3

Grants And Sponsorships

Grants and Sponsorships

For family-friendly story events, grants, sponsorships, and institutional partnerships can smooth cash flow and help fund free public shows. The forecast here assumes $0 in grant or sponsorship revenue unless you add it, so all modeled income comes from tickets, school bookings, festival appearances, merchandise, book sales, and concessions.

The key split is unrestricted support, restricted program funding, and earned revenue. Restricted dollars can pay for the program, but they may not be usable for owner pay, so they do not always improve take-home income the same way a paid booking does.

Track Support by Type

Build the forecast with three lines: unrestricted cash, restricted program money, and earned revenue. That keeps you from counting grant dollars twice or treating funded event costs as profit. Here’s the quick check: if a sponsor covers a free event, it helps margin and attendance, but only unrestricted support can flow cleanly into owner income.

Measure how much support offsets event costs versus overhead. Track cash received, use limits, and timing. If a pledge arrives after the event, it won’t help near-term payroll. If sponsorships replace ticket income, make sure they still cover performer fees, prep time, travel, and admin so margin does not get thinner.

4

Operating Overhead And Reserves

Operating Overhead and Reserves

Overhead and reserves are the cash drag that keeps the show running. Fixed overhead is $5,280/month or $63,360/year, with disclosed lines for $1,500 security, $2,000 marketing, $650 insurance, and $280 booking software, plus other admin not itemized here. That spend lowers near-term take-home, but it protects against cancellations, venue rules, and slow seasons.

Here’s the key point: reserve cash is not distributable owner income. The model shows minimum cash of $624,000 at Month 36 and payback at Month 54, so owner pay should come after overhead coverage and cash floors are met. If cash runs tight, draws should wait; if it runs above reserve, the extra can support salary or profit draws.

Protect the Cash Floor

Track overhead against earned revenue, not just against the bill stack. Use the $5,280/month baseline, then stress-test cancellations, venue deposits, and slow months. The $68,500 launch capex and the $624,000 cash floor mean this is a cash-preservation job, not just a profit story. Cut nonessential spend before owner draws if bookings soften.

- Review the monthly cash floor.

- Separate reserve cash from pay.

- Test slow-season cash burn.

- Hold draws after overhead.

Measure whether each fixed line buys protection or demand. Security, marketing, insurance, and booking software should either help fill the calendar or reduce event risk. If they do neither, review them fast. A reserve only helps if it stay s intact when a venue changes terms or a month comes in light.

5

Owner Role And Production Model

Owner Role Sets the Income Ceiling

The owner’s income depends on the role they fill. In this model, the owner salary is set at $85,000 as an Executive Director role, but owner-as-performer can keep part of the performer-fee economics only if event volume stays limited. Here’s the quick math: more hands-on work can lift take-home per event, but it also caps bookings, so total income may stall before the business does.

Owner-as-producer has the highest ceiling because the model can reach 240 institutional bookings by Year 5, but that only works with coordinators, admin support, marketing, and repeatable processes. If the owner tries to sell, perform, schedule, and manage community relationships alone, burnout risk rises fast, and missed bookings usually hit profit before revenue.

Track Role Mix, Not Just Bookings

Measure the owner’s time by role: performer, producer, booker, or team manager. Track bookings per month, owner hours per event, and labor cost per booking. If the owner is still doing sales, performance, and logistics, use that as a warning sign that the income ceiling is being set by capacity, not demand.

- Count paid bookings by channel.

- Separate performer and admin hours.

- Test when staff support pays back.

- Protect time for repeatable sales.

For planning, compare owner pay to the $85,000 salary model and test whether a producer-led setup can lift volume without pushing the owner into every event. If one role is overloaded, cash flow may look fine for a month or two, but repeat bookings and owner take-home usually weaken next.

6

Compare lean, base, and high owner-income outcomes

Owner income scenarios

Owner pay stays at $85,000, but EBITDA swings from -$110,000 in year 1 to $402,000 by year 5 as ticket volume, private bookings, and festival work scale.

| Scenario | Low CaseEarly funding need | Base CaseBreakeven reached | High CaseScaled production caveat |

|---|---|---|---|

| Launch model | This is the early loss case and it needs outside cash because year 1 EBITDA is -$110,000. | This is the breakeven case because year 3 EBITDA turns positive at $60,000. | This is the scale case, but it only works if the event calendar and staffing hold up through year 5. |

| Typical setup | Year 1 runs 2,400 public tickets, 48 private bookings, and 12 festivals at $25, $850, and $2,500, with $164,000 revenue, 80.5% gross margin, $63,360 fixed overhead, and $165,000 wages. | Year 3 reaches 6,800 public tickets, 110 private bookings, and 36 festivals at $30, $1,000, and $3,500, with $545,000 revenue, 81.0% gross margin, and $259,500 wages. | Year 5 reaches 12,000 public tickets, 180 private bookings, and 60 festivals at $35, $1,200, and $4,500, with $1.096 million revenue, 81.5% gross margin, $329,000 wages, and $402,000 EBITDA. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary only; no cushionCash burn | Salary only; breakevenAt breakeven | Salary only; profit roomScale upside |

| Best fit | Use this if you want to test how much outside cash the launch year needs. | Use this as the core budget case for hiring, pricing, and seasonality. | Use this to test what a larger calendar can support before adding more staff. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Drag Queen Story Hour Events Porter's Five Forces Analysis

- Drag Queen Story Hour Events BCG Matrix

- Drag Queen Story Hour Events Business Model Canvas

- What Five KPIs Should Drag Queen Story Hour Events Business Track?

- Drag Queen Story Hour Business Plan Template in Pre-Written Word

- How Increase Drag Queen Story Hour Events Profitability?

- What Are Drag Queen Story Hour Operating Costs?

- Drag Queen Story Hour Startup Costs: $685K CAPEX To $624K Cash Need

- Drag Queen Story Hour Events Financial Model Template in Excel

- How to Start Drag Storytime Events in 6 to 12 Weeks

- How To Write A Business Plan For Drag Queen Story Hour Events?

- Drag Queen Story Hour Events Marketing Mix

- Drag Queen Story Hour Events Marketing Plan

- Drag Queen Story Hour Events Business Proposal

- Drag Queen Story Hour Events PESTEL Analysis

- Drag Queen Story Hour Events Pitch Deck Example Editable PPTX

- Drag Queen Story Hour Events Business SWOT Analysis

- Drag Queen Story Hour Events Value Proposition Canvas

Frequently Asked Questions

The researched model budgets $85,000 per year before tax for the owner-operator role That is salary, not guaranteed profit distribution EBITDA is -$110,000 in Year 1, turns positive by Year 3 at $60,000, and reaches $402,000 in Year 5 if volume and pricing hit plan