Owner income$6,667 mo

Owner income$6,667 moHow Much Can a Dropshipping Business Owner Make? $80k to $95M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$6,667 mo  Net margin81% - 85%

Net margin81% - 85% Revenue for target pay$94k - $99k

Revenue for target pay$94k - $99k Business difficultyHard

Business difficultyHard

Key Takeaways

- Margin drives profit on every single order.

- Lower CAC helps, but scale can still break.

- Higher AOV and repeat buys lift revenue.

- Refunds and overhead can erase early gains.

Owner income$6,667 moNet margin81% - 85%Revenue for target pay$94k - $99kBusiness difficultyHardWant to test your dropshipping take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, taxes, debt, and reinvestment choices.

Want to see the full income model?

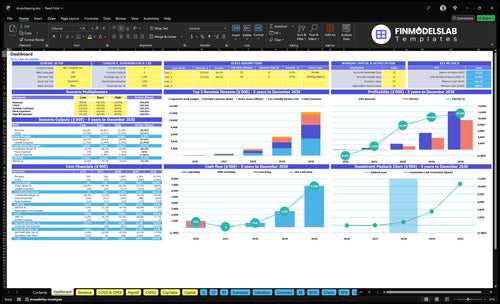

Yes—the dashboard shows revenue, EBITDA, owner pay, cash need, break-even, and payback; open the Dropshipping Business Financial Model Template.

Owner-income model highlights

- Owner pay from dashboard

- EBITDA from -$107k to $9.525m

- Month 15 break-even

- Month 27 payback

- $808k minimum cash need

- Year 1 loss, Year 2 recovery, Year 5 scale

- Assumptions map marketing to capex

What is a good profit margin for dropshipping?

For a Dropshipping Business, a good margin starts with gross margin—revenue after product cost and supplier shipping—and then you watch net profit, what’s left after ads, fees, payroll, tools, refunds, reserves, and reinvestment; see How Much Does It Cost To Open, Start, And Launch Your Dropshipping Business? for the startup cost side. Here’s the quick math: gross margin after product and shipping is 85% in Year 1 and 88% in Year 5, while contribution before ads and refunds is 81% in Year 1 and 85% in Year 5. High sales can still leave low owner income if CAC, returns, support, and payroll absorb the spread.

Margin levels

- Gross margin = revenue after product and shipping.

- 85% gross margin in Year 1.

- 88% gross margin in Year 5.

- 81% contribution in Year 1 before ads and refunds.

Why profit can shrink

- Net profit comes after ads and fees.

- CAC can eat the margin fast.

- Returns and support add real cost.

- Payroll and tools cut owner income.

How much does a dropshipping business owner make per month?

A Dropshipping Business owner’s monthly take-home before tax is not guaranteed: the plan shows a $6,667 monthly founder salary from $80,000/year, but Year 1 EBITDA, or operating profit before interest, taxes, depreciation, and amortization, is about -$8,900/month, so pay depends on startup funding. For the metric that decides whether that pay is sustainable, see What Is The Most Critical Indicator For The Success Of Your Dropshipping Business?.

Monthly owner pay

- Planned salary: $6,667/month

- Annual salary base: $80,000/year

- Year 1 EBITDA: -$8,900/month

- Funding covers early owner pay

Upside by scale

- Year 2 EBITDA: $7,500/month

- Figure is after founder salary

- Year 5 EBITDA: $793,750/month

- Compare small, base, scaled stores

Is dropshipping passive income?

No—a Dropshipping Business is not passive income if you want stable profit. The owner still has to test products, check suppliers, build ad creative and landing pages, and handle support, refunds, payment disputes, and margin review. Outsourcing can reduce the workload, but it adds payroll; support staffing can rise from 0.5 FTE to 2.5 FTE, marketing from 0.5 FTE to 2.0 FTE, so salary replacement is more realistic after Month 15 break-even and Month 27 payback.

Owner work stays active

- Test products often

- Check supplier quality

- Build ad creatives

- Fix landing pages

Costs rise with scale

- Handle customer support

- Process refunds fast

- Manage payment disputes

- Review margins every week

Want the six dropshipping income drivers?

1

81%-85%Contribution Margin

Pre-ad contribution sits near 81% in Year 1 and rises to 85% by Year 5, so small shifts in product cost or fees move owner profit fast.

2

$133K-$465KLabor Load

Payroll grows from about $133K in Year 1 to $465K in Year 5, so headcount can absorb the upside if sales do not scale faster.

3

$25-$17 CACPaid Traffic

CAC falls from $25 to $17, so each marketing dollar buys more customers and leaves more cash for the owner.

4

15%-45%Repeat Buyers

Repeat customers rise from 15% to 45%, which spreads acquisition cost over more orders and lifts lifetime value.

5

$85-$136Order Value

Higher average order value puts more gross profit behind each sale, which helps fixed costs get covered with fewer orders.

6

$1,059/moFixed Overhead

The fixed software stack is $1,059 a month before payroll, so lean overhead matters until volume ramps.

Dropshipping Business Core Six Income Drivers

Contribution margin

Contribution margin

Every order has to cover supplier cost, shipping, payment fees, platform fees, ads, support, and owner pay. Here’s the quick math: Year 1 inputs of 12% wholesale cost, 3% supplier shipping, 25% transaction fees, and 15% payment fees leave 81% before ads and refunds. By Year 5, that improves to 85%, so the business keeps more cash from each sale.

Protect margin per order

Track margin by order, not just revenue. Use order count, average order value, supplier cost, shipping, fees, and refunds to see what the owner can actually take home. Watch for supplier price changes, shipping subsidies, packaging charges, and weak markup. If those creep up, the 81% to 85% cushion shrinks fast and owner pay gets squeezed.

1

Paid acquisition efficiency

Paid acquisition efficiency

Paid acquisition efficiency decides whether more ad spend turns into owner profit or just more sales. In this model, CAC improves from $25 in Year 1 to $17 in Year 5, while annual marketing spend rises from $25,000 to $350,000. If CAC climbs faster than first-order profit, revenue grows but cash for owner pay gets tighter.

The key inputs are ad spend, CAC, AOV, conversion, and contribution margin. Using the provided benchmark, first-order revenue-to-CAC improves from about 34x at $85 AOV to about 80x at $136 AOV. The risk is simple: a profitable CAC in one niche or channel may not scale the same way in another.

Track CAC against first-order profit

Measure CAC by channel, not as one blended number. Split out ad spend, orders, refunds, and net contribution so you can see which traffic actually funds the business. If a channel needs $25 to win a customer but the first order cannot cover shipping, fees, and support, it is not helping owner income.

- Track CAC by source weekly.

- Test bundles to lift AOV.

- Watch refunds by product.

- Stop spend when payback slips.

Set a CAC ceiling from contribution margin, not from revenue alone. Higher AOV can support more ad spend, but only if conversion holds and returns stay low. If a channel scales but gets weaker orders or slower delivery, the extra sales can still cut profit and delay owner draws.

2

Conversion rate and average order value

Conversion Rate and Average Order Value

If traffic doesn’t turn into orders, it doesn’t pay the bills. The real driver is orders × AOV × contribution margin. Here, AOV rises from about $85 in Year 1 to $136 in Year 5 as price mix improves and units per order grow from 11 to 15 bundles. That can lift revenue without the same ad spend, but only if margin stays positive after supplier cost, shipping, fees, and refunds.

Raise Order Value Before Buying More Traffic

Track conversion rate, AOV, units per order, and contribution margin per order every week. Bundle offers, upsells, clearer product pages, and better product-market fit should raise order value, but count only gains that improve cash after ads and support. If AOV rises while refund costs or ad costs rise faster, owner pay gets squeezed.

- Watch bundle attach rate.

- Test checkout upsells.

- Compare margin by product mix.

- Drop low-converting products.

3

Retention and repeat purchases

Repeat Purchases

Repeat purchases matter because each reorder depends less on paid ads. In this model, repeat customers rise from 15% of new customers in Year 1 to 45% in Year 5, repeat customer lifetime grows from 6 to 14 months, and repeat orders per month rise from 03 to 07. That lifts cash flow and gives the owner more profit to draw.

The risk is weak reorder behavior. If the product is a one-time novelty, retention stays thin and ad spend keeps driving growth. Here’s the quick math: more retained customers × more months retained × more repeat orders means more revenue from the same first-order base, with less pressure on gross margin from acquisition costs.

Track Retention By Cohort

Measure repeat customer rate, months to second order, repeat orders per month, AOV, and gross margin by product line. Cohort tracking shows which items create profit, not just sales. If a product gets clicks but no second purchase, it is likely a low-retention item, not a long-term income driver.

Improve this driver with clear delivery updates, quality checks, and post-purchase follow-up. Tie owner pay forecasts to repeat revenue only after the trend holds for several months, because stable repeat buying lowers CAC drag and makes cash flow easier to plan.

4

Refunds, returns, and chargebacks

Refunds, Returns, and Chargebacks

Refunds cut cash before it can pay ads, payroll, or owner draws. In a dropshipping model, the loss is not just the refunded sale; you may also absorb return shipping, chargeback reserve needs, and support cost. With Year 1 EBITDA at -$107,000, this driver can tighten cash fast.

The model needs explicit inputs for refund rate, return shipping exposure, chargeback reserve, and support hours per dispute. Supplier reliability, delivery time, product photos, sizing, warranty terms, and support speed all shape dispute volume. That matters because Month 18 minimum cash need is $808,000, so a bad return pattern can delay recovery and owner pay.

Track Dispute Cost Per Order

Use a simple monthly watchlist: refund rate, return shipping cost, chargebacks, and support cost per order. Split disputes by cause so you can fix the real leak, not just the symptom. If poor photos or slow delivery drive most refunds, improve those first; if sizing or warranty terms cause disputes, tighten product pages before scaling ads.

- Log every refund reason.

- Reserve cash for chargebacks.

- Test supplier shipping speed.

- Rewrite weak product pages.

- Track support minutes per dispute.

Here’s the quick math: each disputed order lowers gross margin and also pulls cash away from growth spend. So if refunds rise, the owner may need to cut ad spend or draws even whe n revenue looks stable. The fix is to forecast dispute cost into the monthly model, not leave it as an afterthought.

5

Operating overhead and outsourcing

Separate Fixed Software From Payroll

This driver is the non-product cost base. Fixed software is $1,059 per month and covers the platform, marketing automation, analytics, support software, admin software, legal and accounting, virtual office, and cloud storage. That spend hits cash flow every month, even before one order ships.

Payroll starts at $80,000 founder pay plus part-time marketing and support, then expands into merchandising and operations roles. If those hires come before profitable order volume, sales can rise while owner distributions stay flat. One clean rule: headcount follows contribution, not hope.

Track Hires Against Gross Profit

Measure software, payroll, and order-related costs separately. Keep a monthly view of order volume, gross margin, and labor load, so you can see when added staff actually pays for itself. If a role does not lift gross profit enough to cover its cost, delay it.

- Track software at $1,059 monthly.

- Track founder pay at $80,000.

- Link hires to profitable order volume.

- Watch cash burn before outsourcing.

Outsourcing can lower the owner’s workload, but it can also delay distributions if you hire too early. Build the forecast with payroll, software, and order costs side by side, then test whether each added role speeds up cash generation or just adds overhead.

6

Owner income scenario planning objective

Owner income scenarios

Owner income moves fast here because ad spend, CAC, AOV, and repeat buying all change at the same time. The model shifts from a launch loss in Year 1 to a scaled profit by Year 5.

| Scenario | Low CaseFunded launch | Base CasePost-break-even | High CaseScaled retention |

|---|---|---|---|

| Launch model | This is the lower owner-income path, with growth still funded by marketing and the founder salary weighing on profit. | This is the modeled middle path, where unit economics have improved and the business is past break-even. | This is the stronger earnings path, where scale and repeat buying lift EBITDA sharply. |

| Typical setup | Year 1 is a funded launch: marketing is $25k, CAC is $25, AOV is about $85, and the founder salary keeps EBITDA negative. | Year 2 is the first post-break-even operating run: spend rises to $75k, CAC falls to $22, AOV is about $99, and EBITDA reaches about $90k. | Year 5 is the scaled retention run: spend is $350k, CAC is $17, AOV is about $136, and stronger repeat buying supports $9.525M EBITDA. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$107k EBITDACash burn | $90k EBITDAEarly profit | $9.5M EBITDAScale upside |

| Best fit | Use this to stress-test early cash needs and the first-year strain on owner pay. | Use this as the core planning case for hiring, cash flow, and owner pay. | Use this to test upside, staffing load, and how much profit scale can support. |

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Dropshipping Business Porter's Five Forces Analysis

- Dropshipping Business BCG Matrix

- Dropshipping Business Business Model Canvas

- 7 Core Financial KPIs to Track for Dropshipping Business Success

- Dropshipping Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Dropshipping Business Profitability

- How Much Does It Cost To Run A Dropshipping Business Monthly?

- Dropshipping Startup Costs: $28K CAPEX And $808K Cash Need

- Dropshipping Business Financial Model Template in Excel

- How to Start a Dropshipping Business in 2 to 6 Weeks

- How to Write a Dropshipping Business Plan: 7 Steps to Financial Clarity

- Dropshipping Business Marketing Mix

- Dropshipping Business Marketing Plan

- Dropshipping Business Business Proposal

- Dropshipping Business PESTEL Analysis

- Dropshipping Business Pitch Deck Example Editable PPTX

- Dropshipping Business Business SWOT Analysis

- Dropshipping Business Value Proposition Canvas

Frequently Asked Questions

In this model, planned founder pay is $80,000 per year, or about $6,667 per month before tax The store still posts -$107,000 EBITDA in Year 1, so early pay needs funding Profit improves to $90,000 EBITDA in Year 2 and $9525 million in Year 5 under the assumptions