Owner income$92k

Owner income$92kHow Much Dumbwaiter Installation Owners Make: $92k Pay Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$92k  Net margin21% to 56%

Net margin21% to 56% Revenue for target pay$440k

Revenue for target pay$440k Business difficultyHard

Business difficultyHard

A dumbwaiter installation business owner can plan around a $92k owner-manager salary in this researched case, plus possible profit distributions only if cash allows The business shows $832k in Year 1 revenue and $174k in EBITDA, which is a 209% EBITDA margin By Year 5, revenue reaches $5587M and EBITDA reaches $3132M, or 561%, but that is business profit before taxes, debt service, reserves, and reinvestment These are planning assumptions, not guaranteed owner take-home

Owner income$92kNet margin21% to 56%Revenue for target pay$440kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not a guaranteed salary, tax advice, or owner distribution advice. Actual owner income will depend on booked revenue, margin, payroll, taxes, debt, reserves, and timing.

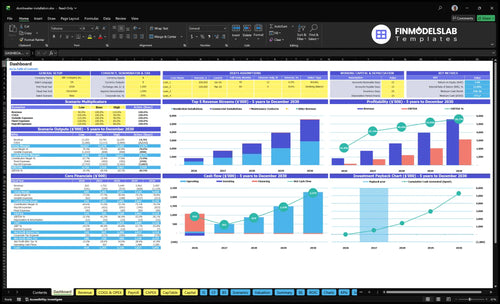

Want to see the full forecast for Dumbwaiter Installation Service?

This dashboard shows revenue, margin, costs, reserves, and owner take-home in the Dumbwaiter Installation Service Financial Model Template; open it.

Owner-income model highlights

- Owner pay capacity

- $832k revenue, $174k EBITDA

- $774k cash, 1177% IRR

How much does a dumbwaiter installation business owner take home?

A Dumbwaiter Installation Service owner can plan on taking home $92k in salary if they personally fill the General Manager role; any extra distributions come only from EBITDA after taxes, debt service, reserves, and reinvestment, which makes What Are The 5 KPI Metrics For Dumbwaiter Installation Service? critical to track. Year 1 shows $174k EBITDA on $832k revenue, or about 20.9%, but that is not automatic owner pay.

Owner Pay

- $92k planned General Manager salary

- Distributions only after cash needs

- Field work may add early savings

- Absentee owners need paid managers

Profit Limits

- Year 1 revenue: $832k

- Year 1 EBITDA: $174k

- Year 5 revenue: $5.587M

- Year 5 EBITDA: $3.132M

Can a dumbwaiter installation business scale?

Yes, the Dumbwaiter Installation Service can scale, but the owner stops being mostly an installer and becomes a scheduler, estimator, trainer, and cash manager. In the case data, revenue rises from $832k in Year 1 to $5.587M in Year 5, while payroll grows from $272k with four staffed roles to $710k with larger crews. That kind of growth only works if you control quality, permits, supplier reliability, vehicle capacity, and cash for inspection delays or rework.

Scale drivers

- Revenue grows to $5.587M by Year 5.

- Lead techs rise from 10 FTE to 30 FTE.

- Junior techs rise from 10 FTE to 50 FTE.

- Payroll climbs from $272k to $710k.

Scale risks

- Permits can slow start dates.

- Inspection delays tie up cash.

- Rework hurts margin fast.

- Vehicle and crew limits cap jobs.

How many dumbwaiter installations are needed to make a living?

There isn’t one universal install count for a Dumbwaiter Installation Service. Use target-pay logic instead: at $832k Year 1 revenue, that works out to about 159 residential-size job-equivalents or 83 commercial-size job-equivalents before mix and pricing shifts the math. The model reaches breakeven in 6 months and payback in 14 months, so close rate, inspection timing, crew capacity, job duration, and callbacks decide whether installs turn into owner income.

Residential job count

- $5,250 labor revenue per job-equivalent

- 159 residential-size job-equivalents

- Before maintenance mix adjustments

- Before equipment pricing changes

Commercial job count

- $10,075 labor revenue per job-equivalent

- 83 commercial-size job-equivalents

- 6 months to breakeven

- 14 months to payback

Want the six drivers that move owner income?

1

1 job/moInstall Volume

One completed install a month is the base unit; more jobs spread fixed overhead and lift owner take-home fastest.

2

$125-$175/hrProject Price

Residential, commercial, and maintenance pricing moves revenue directly, and small rate lifts scale across every booked hour.

3

71%-75%Gross Margin

Direct costs fall from 29% in Year 1 to 25% in Year 5, so every point of margin goes straight to EBITDA.

4

4-12 FTELabor Model

The opening team is 4 FTE and scales to 12 by Year 5, so the mix between owner work and hired crews determines what stays with the owner.

5

$7.5K/moOverhead Control

Fixed overhead is $7,500 a month, so weak utilization or loose spending can wipe out profit fast.

6

$774KCash Buffer

Keep cash back for callbacks and slow collections; the model needs a $774k minimum cash floor in Month 2.

Dumbwaiter Installation Service Core Six Income Drivers

Completed installation volume

Completed Installation Volume

This driver is the count of installs that get completed, inspected, billed, and collected. More closed jobs raise owner income only if each job keeps the 71% gross margin target after 29% direct costs. With $7,500 in monthly fixed overhead, slow volume cuts take-home pay fast. One clean rule: no billable close, no real income.

Track installs per month, annual job count, crew days, backlog, and inspection pass rate. The model reaches breakeven in 6 months, so early ramp speed matters. A permit delay or missing component can block billing even when the unit is physically installed, so revenue alone does not protect cash flow.

Lift Closeable Install Volume

Use a tight flow: booked job, ready site, installed, passed inspection, invoiced, collected. Measure close rate from estimate to signed work, then watch how many jobs stall at permits or missing parts. If billing slips, cash slips. The goal is not just more leads; it’s more jobs that reach cash without margin leakage.

- Track installs by week and month.

- Flag permit and parts delays fast.

- Match crew load to backlog.

- Review inspection pass rate weekly.

- Count billed jobs, not finished work.

When volume rises and margin holds, each added job lifts profit and owner draw. When labor, freight, or rework overruns hit a job, extra revenue can still reduce take-home income. Capacity has to match labor, vehicles, hoisting equipment, and scheduling discipline.

1

Average project price

Average project price

Average project price is the fastest revenue lever when a job shifts from a simple home install to a harder commercial one. In Year 1, residential labor revenue is $5,250 from 42 hours at $125, commercial labor revenue is $10,075 from 65 hours at $155, and maintenance is $275 per visit-equivalent from 25 hours at $110.

Floor count, shaft work, site conditions, permit complexity, and electrical coordination all move the quote. If freight, equipment, and coordination time are missed, the job can still look busy but weak on EBITDA. Bigger quotes only help when they cover the real crew hours, not hope.

Price from full scope

Build every quote from a scope checklist: floor count, shaft layout, access, electrical tie-ins, permit steps, and whether the client is residential or commercial. Then compare quoted labor to actual hours. One simple rule: if hours rise, price should rise too.

- Track estimate versus actual hours.

- Track quote-to-close by job type.

- Pass through freight and permits.

- Watch revenue per crew day.

- Split pricing by residential and commercial.

The goal is higher revenue per crew day and better cash flow, because price sets how much overhead each install can absorb. If commercial jobs stay near $10,075 in labor revenue and hour creep stays controlled, take-home income improves. If not, the owner just gets busier, not richer.

2

Job-level gross margin

Job-Level Gross Margin

Gross margin is what stays after direct job costs, not net profit or owner cash. In Year 1, direct costs are 29%, so gross margin is 71%; by Year 5, direct costs fall to 25%, so gross margin rises to 75%. A job that misses on freight, permits, or install labor can still look busy and leave too little to cover payroll and overhead.

Here’s the quick math: on $832k of revenue, a 1-point margin change is about $8.3k of gross profit, and a 10-point swing is about $83k. The main inputs are unit components, raw materials, freight, permitting, carpentry, electrical coordination, travel, and inspection rework. If any one of those gets underbid, owner pay gets squeezed fast.

Protect Margin Job by Job

Track each estimate against actuals by job type, not just by month. The goal is to keep direct costs near 29% in Year 1 and push toward 25% as the team gets sharper. Measure freight, permit fees, extra travel, and rework hours separately so you can see which line is eating the margin.

- Price freight before quoting.

- Separate permit and rework costs.

- Review carpentry and electrical hours.

- Test margins by floor count.

- Raise price when scope shifts.

If a job needs extra coordination or inspection fixes, build that into the quote up front. That keeps gross profit available for payroll, overhead, and owner draws instead of letting hidden job costs consume the cash.

3

Labor model and owner involvement

Labor Model

Owner-installed jobs can protect early cash because the owner keeps payroll light, but they also cap how many installs, estimates, and schedules can move at once. In this model, the question is not just revenue; it’s how much billable work one owner can personally convert into cash before growth stalls.

When employee crews replace owner-only labor, capacity rises, but so do payroll, training, insurance, supervision, and quality control. Year 1 payroll is $272k across the General Manager, Lead Installation Technician, Junior Technician, and Sales and Referral Coordinator. If the owner takes the $92k manager salary, that is planned pay, not leftover profit.

Track Capacity Per Paid Labor Dollar

Measure installs per crew month, estimate hours, close rate, and crew-day use before adding headcount. Here’s the quick math: if payroll goes up but installs do not, owner pay gets squeezed fast. The main inputs are booked jobs, technician utilization, rework rate, and how much owner time is still spent selling and scheduling.

- Track installs per month.

- Watch estimate-to-close rate.

- Measure rework and callbacks.

- Log owner hours on sales.

By Year 5, payroll reaches $710k with more lead and junior technicians, so the upside comes from higher throughput, not from leaner labor. What this estimate hides is the risk side: more people means more supervision, more quality checks, and more cash tied up before billing clears.

4

Fixed overhead and lead cost

Fixed overhead and lead cost

Fixed overhead is the monthly burn you pay even when installs are slow: $7,500, made up of $4,200 rent, $1,100 liability insurance, $850 vehicle maintenance, $450 software, $600 utilities and communications, and $300 office supplies. That cash comes out before owner pay, so a job can look profitable and still leave thin take-home if volume is light.

Lead cost matters too. Marketing rises from $12k in Year 1 to $45k in Year 5, while CAC moves from $450 to $350. Here’s the quick math: lower CAC helps, but the real win is enough booked installs to absorb fixed cost. The pressure is strongest in slow months, before install volume spreads overhead across more jobs.

Track booked installs and CAC

Measure cost per booked install, not just leads. Also track estimate-to-close rate, admin hours, vehicle downtime, and insurance renewals. If estimate-to-close slips, CAC can stay flat while booked jobs fall, and owner income drops because overhead still runs at $7,500 a month.

Use a simple test: divide monthly marketing by booked installs, then compare it with the $450 to $350 CAC path. If one more booked install does not cover its share of overhead and sales time, tighten follow-up, raise close rate, or pause weak channels. Slow months show the problem first, so watch the gap between pipeline and crew schedule.

5

Warranty reserves and cash protection

Warranty reserves and cash protection

Warranty reserves are the cash set aside for delayed payments, inspection fixes, supplier delays, callbacks, and rework. For a dumbwaiter installer, this cash should sit before owner distributions, because the model shows a $774k minimum cash need in Month 2. That makes early working capital a real income driver, not a side issue.

Here’s the quick math: cash gets tied up in two $45k service vans, $125k hoisting equipment, $8k diagnostic toolsets, $9k IT infrastructure, and a $15k showroom model. If a job needs rework or a supplier slips, the owner can still pay crew, fix defects, and keep selling. Cash buffer first, owner draw second.

Set the reserve before you pay yourself

Track reserve needs against open jobs, billed work, collected cash, and warranty risk. Use inputs like job count, payment timing, inspection pass rate, and callback frequency. If collections lag or a job needs rework, the reserve should absorb that hit so owner income does not get stripped out by one bad month.

Hold back reserve dollars before any profit draw and test the cash model against the $774k Month 2 floor. That matters most early, when capex is already committed and one delayed payment can force the owner to skip pay or delay repairs. Protected cash keeps the business alive through callbacks.

6

Compare low, base, and high owner-income cases

Owner income scenarios

Owner income moves with project mix, crew size, and marketing intensity. Early ramp, steady growth, and a larger field team leave very different cash after fixed costs.

| Scenario | Low CaseOwner-operated | Base CaseCrew-managed | High CaseScaled operator |

|---|---|---|---|

| Launch model | This is the early-ramp case with one crew, lighter volume, and the owner still covering the GM role. | This is the steady-growth case with a larger crew, repeat work, and a fuller sales funnel. | This is the mature case with a scaled crew, stronger backlog, and more work than one field team can carry. |

| Typical setup | Year 1 uses $832k revenue, $174k EBITDA, 20.9% margin, $12k marketing, $92k manager pay, and 29% direct costs. | Year 3 uses $2.649M revenue, $1.228M EBITDA, 46.4% margin, $25k marketing, $482k payroll, and about 27% direct costs. | Year 5 uses $5.587M revenue, $3.132M EBITDA, 56.1% margin, $45k marketing, $710k payroll, and 25% direct costs. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $92k-$174kOwner-op band | $482k-$1.23MCrew band | $710k-$3.13MScale band |

| Best fit | Use this to stress-test a small team that still depends on the owner for day-to-day control. | Use this as the middle case for a working crew with enough scale to support a salaried manager structure. | Use this to test upside when the business runs with a larger staff and a strong installed base. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. Taxes, debt service, reserves, and reinvestment can cut cash available to the owner.

Related Products

- Dumbwaiter Installation Service Porter's Five Forces Analysis

- Dumbwaiter Installation Service BCG Matrix

- Dumbwaiter Installation Service Business Model Canvas

- What Are The 5 KPI Metrics For Dumbwaiter Installation Service?

- Dumbwaiter Installation Business Plan Template in Pre-Written Word

- How Increase Dumbwaiter Installation Service Profits?

- What Are Operating Costs For Dumbwaiter Installation Service?

- Dumbwaiter Installation Startup Costs: $774K Cash Plan

- Dumbwaiter Installation Service Financial Model Template in Excel

- How To Start A Dumbwaiter Installation Business In 8 To 16 Weeks

- How To Write A Business Plan For Dumbwaiter Installation Service?

- Dumbwaiter Installation Service Marketing Mix

- Dumbwaiter Installation Service Marketing Plan

- Dumbwaiter Installation Service Business Proposal

- Dumbwaiter Installation Service PESTEL Analysis

- Dumbwaiter Installation Service Pitch Deck Example Editable PPTX

- Dumbwaiter Installation Service Business SWOT Analysis

- Dumbwaiter Installation Service Value Proposition Canvas

Frequently Asked Questions

The researched case supports a $92k owner-manager salary if the owner fills the General Manager role The business also produces $174k EBITDA on $832k Year 1 revenue, growing to $3132M EBITDA on $5587M Year 5 revenue EBITDA is not automatic take-home because reserves, taxes, debt service, and reinvestment come first