Owner income$150K

Owner income$150KHow Much E-Commerce Owners Make: $150K Salary, Profit Varies

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150K  Net margin60.7%

Net margin60.7% Revenue for target pay$247K

Revenue for target pay$247K Business difficultyHard

Business difficultyHard

In this researched model, the e-commerce owner has a modeled $150,000 CEO salary, but that is not the same as business profit or cash distributions First-year revenue is about $2246K, yet the business shows an operating loss after marketing, fixed costs, and payroll, so owner distributions would be $0 before tax and reserves By the third year, revenue reaches about $384M, with roughly $216M of profit after the CEO salary before tax, debt, reserves, and reinvestment These are assumption-based estimates, not guaranteed income

Owner income$150KNet margin60.7%Revenue for target pay$247KBusiness difficultyHardWant to test your e-commerce owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This output is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll mix, fees, reserves, and how taxes are handled.

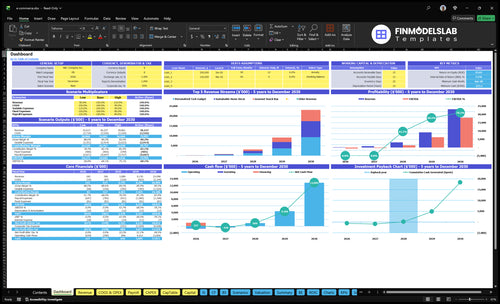

Want to check owner income in the E-Commerce Business model?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the E-Commerce Business Financial Model Template; open it to review pay capacity.

Owner-income model highlights

- Owner pay after costs

- Revenue and margin tabs

- Scenarios shape cash flow

Can an e-commerce business be passive income?

No—an E-Commerce Business is not passive income by default. If you staff a $150K CEO, a $90K curation and partnerships role, and a $120K technical lead, payroll alone is $360K before marketing, operations, support, reserves, and reinvestment. Owner-run models save cash but cost time, while outsourced models free time but add fees, control risk, and lower take-home.

Cash drains

- $360K payroll before extras

- Marketing adds more spend

- Operations and support add staff costs

- Fulfillment partners take fees

Payout rule

- Cover overhead first

- Pay payroll next

- Keep reserves in place

- Then distributions can grow

What is a good profit margin for e-commerce?

For an E-Commerce Business, a good profit margin is the one that still covers product cost, CAC (customer acquisition cost), fulfillment, returns, overhead, and payroll; for launch-cost context, see How Much Does It Cost To Open, Start, And Launch Your E-Commerce Business?. In this model, gross margin starts at 88.0%, drops to 83.0% before marketing, and lands at about 60.7% contribution after first-year marketing. That means the real test is whether paid traffic, reorder behavior, and fulfillment load still leave cash left over.

Margin math

- 88.0% gross margin starts it.

- 83.0% before marketing stays strong.

- 60.7% contribution is the key check.

- Product and fees come first.

What moves it

- CAC improves from $40 to $25.

- Repeat buyers rise from 250% to 550% of new customers.

- Paid traffic must match margin.

- Fulfillment load can eat profit fast.

What is the difference between e-commerce revenue vs profit and owner salary?

For an E-Commerce Business, revenue is the full sales top line, profit is what’s left after costs, and owner salary is a payroll decision. On $2.246M of first-year revenue, 120% product and partner costs already equal about $2.695M, before 50% fulfillment and payment fees, $50K marketing, $81K fixed overhead, and $560K payroll. So cash flow matters: inventory buys and reserves can drain cash before profit appears, and owner draws should wait until restocking, refunds, reserves, debt service, and taxes are covered.

Revenue vs profit

- Revenue is customer sales.

- Profit is sales minus costs.

- Salary is a payroll cost.

- $2.246M sales can still lose money.

Cash comes first

- $2.695M at 120% on product costs.

- $1.123M at 50% on fees.

- Add $50K marketing and $81K overhead.

- Pay owners after reserves and taxes.

What drives e-commerce owner income?

1

2.8K-150.7KOrders and AOV

More orders and a higher basket size lift revenue and the cash left for the owner.

2

88%-90.5%Gross Margin

A 12.0% to 9.5% all-in product cost keeps more of each sale.

3

$40-$25CAC

Lower customer acquisition cost lets the same marketing budget buy more customers.

4

3.0%-2.5%Shipping Cost

Every point saved on fulfillment and shipping drops straight into contribution.

5

25%-55%Repeat Sales

More repeat buyers cut paid-acquisition pressure and raise customer value over time.

6

$231KFixed Load

The $81K overhead plus the $150K CEO salary must be covered before owner pay improves.

E-Commerce Business Core Six Income Drivers

Sales Volume and Average Order Value

Orders and Average Order Value

Revenue = orders × average order value (AOV), so this driver sets the cash base for the whole business. At 2,750 orders × $82 AOV, sales are about $225.5K; at 150,720 orders × $152 AOV, sales are about $22.9M. More sales only help if gross margin survives customer acquisition and fulfillment first.

This is where owner pay gets made or lost. A higher AOV helps cover CAC (customer acquisition cost) and shipping faster, while discounting can lift order count but still squeeze cash. One clean rule: if each extra order adds less cash than it costs to win and ship, take-home income falls even when revenue rises.

Protect AOV Before You Chase Volume

Track orders, AOV, CAC, fulfillment cost, payment fees, and contribution per order. Here’s the quick math: contribution = order revenue - acquisition - shipping - payment fees - returns. If AOV rises faster than variable costs, owner pay capacity improves. If not, volume can hide a cash leak.

Test bundles, minimum order thresholds, and category mix before cutting prices. A small lift in AOV often pays back faster than buying more traffic. Watch whether discounting adds enough orders to offset the lower dollars per order; if it doesn’t, the extra sales do not improve owner income.

1

Gross Product Margin

Gross Product Margin

Your take-home pay starts with gross margin, because it funds ads, fulfillment, overhead, payroll, and then owner draw. In the model, year one shows 100% product acquisition cost plus 20% partner fees, with gross margin listed at 880%; mature year improves to 80% acquisition cost and 15% partner fees, lifting gross margin to 905%. Use the model as a mix and cost test, not just a sales test.

What this driver includes: product cost, partner fees, duties, packaging, damaged inventory, and returns. The key inputs are SKU mix, order volume, average order value, and loss rate from damage or returns. One line matters here: a weak margin can hide behind strong revenue, and each margin point matters more as revenue scales.

Track Margin by SKU and Return Rate

Measure gross margin at the SKU level, not just at the store level. Split out product acquisition cost, partner fees, duties, packaging, damaged inventory, and returns so you can see which items pay for growth and which ones only add volume.

Track gross margin per SKU.

Test margin by product mix.

Flag returns above model assumptions.

Watch margin before increasing ad spend.

If margin slips while sales rise, cash gets tight fast, because ads and payroll get paid before owner draw. Keep a monthly gross margin report tied to orders, AOV, and refunds, so you can see whether growth is actually improving the cash left for the owner.

2

Customer Acquisition Efficiency

Customer Acquisition Efficiency

Customer acquisition efficiency is how much it costs to bring in each new buyer. In this model, $50K of first-year marketing at a $40 CAC creates about 1,250 customers; in the mature year, $600K at $25 CAC creates about 24,000 customers. Lower CAC helps owner pay only if gross profit after product cost, fulfillment, payment fees, and returns stays above that spend.

Here’s the quick math: new customers = marketing spend ÷ CAC. The trap is paying for traffic before repeat orders arrive. If the first order does not cover enough gross profit, paid growth can lift sales and still reduce cash available for salary or profit draw. ROAS alone is not enough; you need CAC versus contribution margin, not just ad revenue.

Track CAC Against Gross Profit

Measure marketing spend, CAC, first-order gross profit, and repeat purchase timing by channel. A simple test: if CAC rises faster than gross profit per new customer, pause spend or fix landing pages, pricing, or product mix before scaling. The goal is not just more buyers, but buyers that leave enough margin to pay the owner.

- Track CAC by channel weekly

- Include returns in contribution

- Use first-order gross profit

- Watch repeat orders by cohort

- Cut spend when payback slows

Lower CAC usually raises owner pay capacity because each new customer needs less upfront cash to reach contribution break-even. If paid acquisition gets expensive before repeat orders catch up, the business can look busy and still feel tight on cash. That is the number to watch.

3

Fulfillment, Shipping, and Payment Costs

Order Fulfillment Cost

Fulfillment, shipping, packaging, and payment fees hit cash before owner pay. In year one, fulfillment and shipping run at 30% of revenue and payment processing at 20%, so 50% of sales is gone before product cost, overhead, or profit. In a mature year, that drops to 25% and 15%, which gives back margin without needing more orders.

This driver includes carrier rates, warehouse handling, pick-pack labor, packaging, and card fees. The key inputs are orders, average order value, shipping charge, actual carrier cost, warehouse cost, and payment fee rate. Customer-paid shipping is not pure profit if the real cost is higher, and free shipping can lift conversion while cutting cash per order. Every point saved here flows straight to take-home income.

Track Landed Cost Per Order

Measure all-in cost per order, not just the label price. Here’s the quick math: if fulfillment and shipping are 30% of revenue and payments are 20%, you need strong gross margin elsewhere just to keep contribution positive. Split the bill by channel, SKU, and ship zone so you can see where margin leaks. One bad zone can erase the gain from a high-AOV cart.

- Compare charge vs actual ship cost.

- Track pick-pack labor per order.

- Test free shipping thresholds.

- Review card fees monthly.

- Cut b ad zones or heavy SKUs.

If mature-year rates fall to 25% and 15%, contribution improves without adding ad spend. That matters because better fulfillment rates let the owner pay themselves from existing sales, not from hopes of more volume. Keep the target simple: lower cost per shipped order, and protect margin on every basket.

4

Repeat Purchase and Retention

Repeat Purchases

Repeat buyers raise lifetime gross profit because they buy for 8 to 24 months and place about 0.4 to 0.8 orders per month. In year one, repeat customers equal 250% of new customers; in the mature year, they reach 550%. That shifts income away from constant paid acquisition and makes owner pay less exposed to ad swings.

Here’s the quick math: if repeat buying slows, the business must keep replacing customers, so cash gets pulled into marketing instead of profit. What this hides: not every product category has natural reorder behavior, so retention only helps when the mix supports follow-on purchases.

Track Repeat Rate

Measure repeat customers by category, repeat order rate, and customer lifetime months. Compare each line to the 0.4 to 0.8 monthly order range and the 8 to 24 month lifetime benchmark, then cut spend on products that do not come back.

Use replenishment emails, loyalty offers, and bundles only where the product fits repeat buying. Strong retention spreads fixed costs over more orders, so more gross profit reaches owner draw instead of being spent on new traffic.

5

Fixed Overhead, Staffing, and Owner Role

Fixed Overhead and Payroll

Owner pay only starts after contribution covers the nut. Here, fixed overhead is $6,750 a month, or $81K a year, and payroll starts at $560K in year one, including a $150K CEO salary, then rises to $960K in the mature year.

The key inputs are monthly contribution, headcount, owner salary, and software spend. Hiring ahead of contribution can create losses even when gross margin looks strong, so lean staffing helps early cash pay, but it can also slow scale if the team gets too thin.

Track payroll before you add headcount

Set a hiring gate tied to contribution, not hope. A simple rule: do not add fixed staff until recurring contribution can cover $6,750 overhead plus the next payroll step and still leave room for owner pay.

Track three lines every month: owner salary, hired labor, and software costs. If payroll rises faster than contribution, owner draw gets squeezed fast. If staffing stays too lean, the store may protect cash now but cap future growth.

- Watch contribution after fulfillment.

- Separate owner pay from labor.

- Approve hires by payback period.

- Review overhead every month.

6

Compare lean, base, and high e-commerce owner income scenarios

Owner income scenarios

Owner income changes fast because marketing, CAC, repeat orders, and staffing scale together. The low case protects cash, while the base and high cases show what stronger margin and demand can support.

| Scenario | Low CaseCash strain | Base CaseMargin quality | High CaseStaffing complexity |

|---|---|---|---|

| Launch model | This is a lean year-one path with weak cash flow and no owner distributions. | This is the modeled mid-case path with positive owner earnings. | This is the stronger mature-year path with much higher owner earnings. |

| Typical setup | Year-one style economics stay loss-making, with $50,000 marketing, $40 CAC, $81,000 fixed overhead, $560,000 payroll, and only the modeled CEO salary. | Year-three style economics improve to positive EBITDA of $1,351,000, with $250,000 marketing, $30 CAC, 45% repeat customers, and a stronger mix of higher-priced products. | Year-five style economics reach EBITDA of $18,051,000, with $600,000 marketing, $25 CAC, 55% repeat customers, and heavier staffing across marketing, operations, and support. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $150,000Salary only | $1.35MEBITDA positive | $18.05MUpside case |

| Best fit | Use this to stress-test the business if growth is slow and cash must cover losses. | Use this as the main planning case for a business that reaches steady repeat demand. | Use this to test upside if repeat orders, pricing, and product mix all improve together. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- E-Commerce Business Porter's Five Forces Analysis

- E-Commerce Business BCG Matrix

- E-Commerce Business Business Model Canvas

- 7 Essential Financial KPIs for E-Commerce Business Growth

- E-Commerce Business Business Plan Template in Pre-Written Word

- How to Increase E-Commerce Business Profitability in 7 Steps

- How Much Does It Cost To Run An E-Commerce Business Monthly?

- E-Commerce Business Startup Costs: $117K Setup Plus Runway

- E-Commerce Financial Model Template in Excel

- How To Start An E-Commerce Business With A 4-8 Week Launch Plan

- How to Write a Business Plan for Your E-Commerce Business

- E-Commerce Business Marketing Mix

- E-Commerce Business Marketing Plan

- E-Commerce Business Business Proposal

- E-Commerce Business PESTEL Analysis

- E-Commerce Business Pitch Deck Example Editable PPTX

- E-Commerce Business Business SWOT Analysis

- E-Commerce Business Value Proposition Canvas

Frequently Asked Questions

In this model, the owner has a $150K CEO salary, but distributions depend on profit and cash First-year revenue is about $2246K, yet the business runs at a loss after $50K marketing, $81K fixed overhead, and $560K payroll By the third year, modeled profit after CEO salary is about $216M before tax and reserves