Owner income$180k base

Owner income$180k baseHow Much Can an Entertainment Agency Owner Make With $180k Pay?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k base  Net margin405%

Net margin405% Revenue for target pay$44k

Revenue for target pay$44k Business difficultyHard

Business difficultyHard

An entertainment agency owner can model $180,000 in annual salary in this plan, but profit distributions are not supported in Year 1 because EBITDA is -$558,000 By Year 2, estimated EBITDA reaches $837,000, so owner upside may come from distributions after reserves, debt service, and business taxes Here’s the quick math: fixed overhead is $570,000 per year, Year 1 payroll is $835,000, and Year 1 revenue-linked costs are 290% of revenue These are researched planning assumptions, not promised earnings

Owner income$180k baseNet margin405%Revenue for target pay$44kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay. For this agency, the Year 1 cost base points to about $10,000 monthly marketing, $69,600 payroll, and $47,500 fixed overhead before owner pay starts.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. It uses modeled revenue, margin, payroll, overhead, marketing, and reserve inputs, and it excludes personal taxes, debt terms, and guaranteed salary.

Want to check owner income in the model?

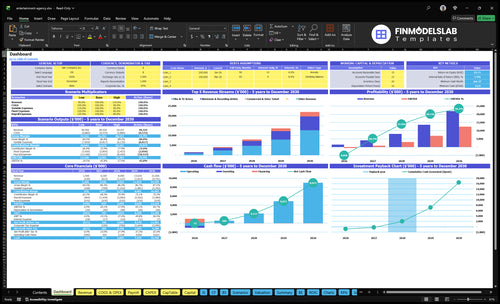

This dashboard shows revenue, EBITDA, cash, breakeven, payback, and owner pay; open the Entertainment Agency Financial Model Template.

Owner-income model highlights

- Month 14 breakeven

- Month 28 payback

- -$23k minimum cash

- $403k launch capex

- Scenario tabs test growth

How do entertainment agencies make money?

Entertainment Agency makes money from booking commissions, management fees, retainers, package fees, and project-based representation; the key is counting only agency commission or fees as revenue, not the performer’s full gross booking value, and tracking it through How Is The Overall Growth Of Your Entertainment Agency?.

Revenue sources

- Earn booking commissions on secured work

- Charge management fees for career support

- Use retainers for ongoing representation

- Sell package fees and project deals

Year 1 mix

- Film & TV Actors: 450%

- Musicians & Recording Artists: 350%

- Commercial & Voice Talent: 200%

- Owner income rises with commissionable bookings

How much revenue does an entertainment agency need to pay the owner?

The Entertainment Agency needs about $215 million in annual revenue to cover a $180,000 owner salary and reach Year 1 operating break-even. At modeled Year 1 revenue of about $136 million, EBITDA is still about -$558,000, so the owner pay only works at much higher scale.

Year 1 Math

- $1.525 million fixed cost base

- 7.10% contribution margin

- $136 million modeled Year 1 revenue

- -$558,000 EBITDA at Year 1 scale

Year 2 Check

- $180,000 founder salary target

- $215 million annual revenue needed

- 7.26% Year 2 contribution margin

- $270 million Year 2 break-even revenue

Can a solo entertainment agency owner make money?

A solo owner can keep overhead lower, but the Entertainment Agency model is built as a staffed agency from day one, with 2 senior talent agents, 1 junior agent, 1 talent manager, and support roles. That team can lift deal flow, but salaries and overhead have to be paid before owner take-home improves. In the model, breakeven lands at Month 14.

Scale helps

- 2 senior agents drive more bookings

- 1 junior agent adds coverage

- 1 talent manager supports clients

- Support roles free owner time

Cash comes first

- Salaries hit before owner pay

- Overhead must be covered first

- Month 14 is breakeven

- Solo work lowers cost, but caps scale

Want to see the main income drivers?

1

$1.4MBooking Volume

More commissionable bookings is the fastest way to move from -$558K Year 1 EBITDA to $837K in Year 2.

2

$320-$550Roster Quality

A stronger roster lifts hourly rates, and the model's price band runs from $320 to $550 per hour.

3

15.5%-12.5%Fee Mix

Lower talent commission payments and platform fees keep more of each booking, with revenue-linked costs falling over time.

4

15-28hAgent Productivity

More billable hours per talent spread payroll across more revenue, with Film & TV Actors rising from 15 to 28 hours.

5

35%-45%Client Retention

Keeping more Musicians & Recording Artists on roster matters because their share climbs from 35% to 45% by Year 5.

6

$570KOverhead Buffer

With about $570K of fixed overhead, 290% Year 1 revenue-linked costs, and a $180K founder salary, reserves decide how long you can absorb the -$558K Year 1 EBITDA gap before Year 2 turns to $837K.

Entertainment Agency Core Six Income Drivers

Commissionable Booking Volume

Commissionable Booking Volume

More paid work only helps if the agency actually earns commissions or fees. Do not book performer value as revenue; track the commissionable share, then measure annual booking value per client, active roster count, and effective commission rate.

This driver hits owner pay fast because the model assumes each extra $1 of agency revenue carries about 710% Year 1 contribution before payroll, overhead, and marketing. That makes booking volume a direct profit lever, but only when contracts convert into billable agency income.

Measure What Actually Pays

Build the model from active clients × annual booking value per client × effective commission rate. Track booked work by client, then strip out non-commissionable deals, held bookings, and gross performer pay. One clean metric: commissionable booking volume per active roster client.

Watch mix and retention too. A bigger roster with weak bookings can lower take-home cash, while a smaller active roster can pay better. If booking value rises but commission rate falls, owner income can still stall, so forecast revenue by fee type and review the contract terms that change the effective rate.

- Track: annual booking value per client

- Track: active roster count

- Track: effective commission rate

- Exclude: non-commissionable performer value

- Test: revenue by fee type

1

Roster Quality And Monetizable Client Mix

Roster Mix Drives Commission Income

This driver is the mix of active clients, not the raw roster count. In a commission model, only booked work pays, so a smaller active roster can beat a bigger inactive one if it books more often and matches buyer demand. Track revenue per active client, booking frequency, and effective commission rate; those are the inputs that move owner income.

- Active roster count

- Bookings per client

- Commissionable booking value

- Buyer demand by segment

- Revenue per active client

Use the disclosed mix benchmarks as your model: 450% Film & TV Actors, 350% Musicians & Recording Artists, and 200% Commercial & Voice Talent in Year 1, then 350%, 450%, and 200% by Year 5. If demand shifts toward music, the agency only earns more if the active mix shifts too.

Measure Active Revenue, Not Vanity Size

Forecast by cohort, not headcount. If a client has no bookings for 90 days, they are likely using time without creating commission income. That drags margin because admin, pitching, and follow-up still happen, but cash does not. One clean rule: if a segment does not book, it should not drive staffing or marketing spend.

Keep the roster weighted toward the segments with the highest repeat demand and the best booking frequency. That improves gross margin and owner pay because the same team can support more commission dollars. The quick math is simple: more booked clients at the same staff cost means more profit left after overhead, so the owner can draw more.

2

Commission Rate, Fees, And Revenue Mix

Effective Fee Mix

Owner income depends on the effective take rate, not just the headline commission. A contract may show one rate, but union terms, state rules, and legal review can reduce what you can actually charge, so model commission, retainers, project fees, package fees, and management fees as separate lines.

Here’s the quick math: agency revenue equals bookable client volume × effective rate. If the mix shifts toward lower-fee work, cash to cover payroll, marketing, and owner pay drops fast. Keep legal review out of revenue and flag it inside the $3,200 monthly insurance and legal line.

Track Net Rate by Fee Type

Build the model with separate inputs for commission rate, fee type, and client segment. Track booked work, average chargeable value, fee waivers, and the share of revenue that comes from each line, because a small drop in net rate can erase a lot of owner draw.

One clean test: compare headline rate vs. collected rate each month. If collected rate falls, tighten contract review, prune low-yield deals, and price management work so it pays for the time it takes. Use the legal and compliance bucket, not revenue, for review costs.

3

Agent Productivity And Staffing Model

Agent Productivity

Hiring more agents only lifts owner income if each producer covers their own pay. In Year 1, payroll is $835k, including $240k for 2 senior agents and $70k for 1 junior agent, so bookings have to rise fast enough to fund that base before the owner sees more take-home.

Here’s the quick math: each agent should be tied to revenue, contribution, and retained clients. The model also shows Year 2 payroll rising to $121m, so weak output turns growth hiring into lower owner pay, not higher profit.

Measure Producer Output

Track each agent by commission revenue per month, gross contribution after payroll, and the number of clients kept active. If one producer adds bookings but not enough margin to cover salary and support cost, the hire reduces cash flow and delays owner draws. One good agent should pay for themselves before the next hire.

- Revenue per active producer

- Contribution after payroll

- Retained clients per agent

- Bookings closed each month

- Payback before new hiring

4

Client Retention And Repeat Booking Relationships

Repeat Booking Relationships

Retained talent and repeat buyers reduce the need to keep replacing lost work, so commission income gets steadier and owner pay is easier to forecast. Here’s the quick math: CAC improves from $2,400 in Year 1 to $1,800 in Year 5, but the marketing budget still rises from $120k to $400k. That means retention has to do more than just “help”; it has to protect margin.

This driver includes active client retention, repeat booking rate, buyer return rate, commissionable booking volume, and effective commission rate. It does not create guaranteed recurring revenue, because each booking still depends on a new contract. If repeat work drops, the agency has to buy growth again through marketing, which hits cash flow and trims the owner’s draw.

- Track active clients each month.

- Measure repeat bookings per client.

- Watch buyer return rate.

- Compare CAC to commission margin.

Keep Clients and Buyers Coming Back

Measure retention by c lient, buyer, and month, then tie it to commission dollars, not vanity roster size. If a client books once and disappears, acquisition cost stays high and the agency never gets the full value of that relationship. The owner wins when retained talent keeps landing paid work and repeat buyers keep rebooking without another big spend spike.

Use a simple forecast: repeat bookings x commission rate x average booking value. Then compare that to marketing and payroll before paying out profit. If marketing keeps climbing toward $400k, weak retention can turn growth into a cash drain. Strong retention helps protect owner income, but the model still needs fresh bookings to stay healthy.

5

Overhead, Marketing, Compliance, And Reserves

Overhead, Marketing, Compliance, And Reserves

This line item covers lead generation, networking, legal review, software, travel, insurance, offices, and working capital held back for cash needs. At $47,500 per month or $570,000 per year, it cuts straight into commission income before the owner can take home profit.

Year 1 marketing is $120,000, launch capex is $403,000, and minimum cash reaches -$23,000 in Month 13. That means reserves are not profit; they must stay in the business before any owner distribution, or pay gets pulled from needed cash.

Track Cash Burn Before Owner Pay

Measure this as a monthly cash burn line, not a vague overhead bucket. The key inputs are fixed overhead, marketing spend, legal and insurance cost, and the reserve target needed to cover weak months and delayed client collections.

- Track overhead by month.

- Separate marketing from fixed cost.

- Hold reserves before distributions.

- Watch Month 13 cash closely.

Use the cash forecast to decide when owner pay starts. If spend stays at $47,500 a month plus $120,000 Year 1 marketing, the business needs enough booked commissions to cover that base cost and still leave cash after the $403,000 launch outlay.

6

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income changes with revenue scale because payroll, rent, marketing, and talent commissions stay heavy. These cases show when the founder gets only salary versus salary plus distributions.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path, with revenue near $136m and EBITDA still negative. | This is the modeled operating path, with revenue near $385m and modest positive EBITDA. | This is the stronger earnings path, with revenue near $753m and EBITDA widening fast. |

| Typical setup | Revenue is about $136m, EBITDA is about -$558k, cost load is about 290% of revenue, and the founder takes salary only. | Revenue is about $385m, EBITDA is about $837k, cost load is about 274% of revenue, and distributions start only after reserves are covered. | Revenue is about $753m, EBITDA is about $3.054m, cost load is about 260% of revenue, and the owner can draw salary plus larger distributions. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $180k salary onlyLow Case | $180k salary + distributionsBase Case | $180k salary + larger distributionsHigh Case |

| Best fit | Use this to stress-test the founder's income when growth is slow and distributions do not start. | Use this as the main planning case for normal growth and delayed owner payouts. | Use this to test upside if the agency wins more work and holds costs tighter. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions.

Related Products

- Entertainment Agency Porter's Five Forces Analysis

- Entertainment Agency BCG Matrix

- Entertainment Agency Business Model Canvas

- Tracking 7 Core KPIs for an Entertainment Agency

- Entertainment Agency Business Plan Template in Pre-Written Word

- Increase Entertainment Agency Profitability: 7 Actionable Strategies

- How Much Does It Cost To Run An Entertainment Agency Monthly?

- Entertainment Agency Startup Costs: $403K Setup Budget Guide

- Entertainment Agency Financial Model Template in Excel

- How To Open An Entertainment Agency In 8 To 16 Weeks

- How to Write an Entertainment Agency Business Plan: 7 Steps

- Entertainment Agency Marketing Mix

- Entertainment Agency Marketing Plan

- Entertainment Agency Business Proposal

- Entertainment Agency PESTEL Analysis

- Entertainment Agency Pitch Deck Example Editable PPTX

- Entertainment Agency Business SWOT Analysis

- Entertainment Agency Value Proposition Canvas

Frequently Asked Questions

The model sets owner salary at $180,000 per year In Year 1, EBITDA is -$558,000, so distributions are not supported by operations In Year 2, EBITDA is $837,000, which may create distribution capacity after reserves, debt service, and business taxes