Owner income$150k base

Owner income$150k baseHow Much Environmental Cleanup Owners Make: $150K Pay Target

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k base  Net margin-62% to 2%

Net margin-62% to 2% Revenue for target pay$6.9m

Revenue for target pay$6.9m Business difficultyHard

Business difficultyHard

In this researched base case, environmental cleanup business owner income is modeled as a $150,000 CEO / Lead Environmental Scientist salary before taxes, with distributions depending on reserves, debt, and reinvestment Revenue grows from about $576k in Year 1 to about $578m in Year 5 EBITDA after that owner salary is negative through Year 3, about $637k in Year 4, and about $293m in Year 5 So the business is not self-funding early, but mature remediation volume can create strong owner-pay capacity

Owner income$150k baseNet margin-62% to 2%Revenue for target pay$6.9mBusiness difficultyHardWant to test your cleanup owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on pricing, project volume, staffing, taxes, and reserves.

How do you check owner income in an Environmental Cleanup model?

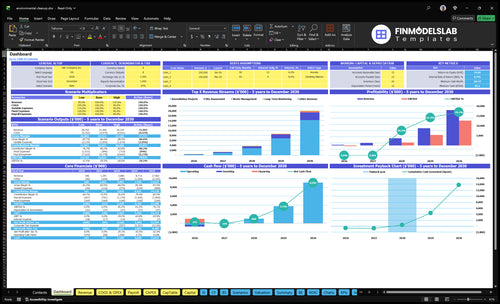

This Environmental Cleanup Financial Model Template dashboard shows revenue, gross margin, EBITDA, owner salary, and scenario outputs—open the model.

Owner-income model highlights

- Year 1 to Year 5

- Cost load drops 26% to 17%

- Test assumptions next

What environmental cleanup profit margin matters most?

For Environmental Cleanup, the margin that matters most is gross margin after subcontractor, equipment rental, lab analysis, and waste disposal fees; that’s the cleanest read on whether each job actually pays. For startup budgeting, see How Much Does It Cost To Open Your Environmental Cleanup Business? because the cost base drives the margin fast. Here’s the quick math: gross margin improves from 81% in Year 1 to 87% in Year 5, while combined direct-variable cost load falls from 26% to 17%.

Margin to watch

- 81% Year 1 gross margin

- 87% Year 5 gross margin

- 26% to 17% direct-variable load

- Watch each job, not just revenue

Biggest margin risks

- Disposal intensity can crush margin

- Hauling distance raises cost fast

- Sampling and PPE add hidden spend

- Underpriced bids leave no room

Can an environmental cleanup business scale?

Yes—Environmental Cleanup can scale, but the business gets heavier before it gets richer. In this model, Year 1 starts with 25 FTE-equivalent staff and owner-heavy leadership, then Year 5 reaches 16 FTE-equivalent staff while revenue rises from $576k to $578m as remediation mix hits 85% and acquired accounts reach 818. Scale adds payroll, equipment, insurance, and compliance oversight first, so poor utilization or one incident can erase owner distributions.

Growth math

- 25 FTE in Year 1

- 16 FTE in Year 5

- Revenue jumps to $578m

- Remediation mix reaches 85%

What can break it

- Payroll grows with crews

- Equipment needs cash up front

- Insurance and compliance add load

- Poor utilization cuts take-home

How much can an environmental cleanup business owner make?

An Environmental Cleanup owner is modeled at $150,000 before taxes through the CEO / Lead Environmental Scientist role, but extra take-home isn’t supportable until EBITDA turns positive after reserves; see What Is The Current Growth Trend For Environmental Cleanup? for the market-growth context. The model shows EBITDA after owner salary of -$5.116 million in Year 1, -$4.898 million in Year 3, $6.373 million in Year 4, and $293 million in Year 5, so owner income is a planning case, not a guaranteed wage claim.

Modeled owner pay

- $150,000 CEO / Lead Scientist salary

- Before taxes, not take-home pay

- Extra cash depends on EBITDA reserves

- No guaranteed wage claim

Main income drivers

- Win larger cleanup projects

- Control hazardous disposal burden

- Use crews efficiently

- Manage compliance and working capital

Want to see the main income drivers?

1

$134K-$706KContract mix

Shifting work from site assessment into remediation and monitoring lifts revenue per acquired account and moves owner take-home the fastest.

2

150-300hCrew utilization

More billable hours spread wages and travel across more revenue, so each crew dollar keeps more gross profit.

3

26%-17%Cost load

Keeping subcontractor, disposal, and travel spend down cuts the direct-variable load and leaves more cash after each project.

4

$1.692MOverhead load

Rent, insurance, training, and admin costs set a big fixed base, and the CEO / Lead Environmental Scientist salary at $150K adds to the hurdle before profit reaches the owner.

5

300hEquipment cap

More vehicles, field devices, and lab gear let the team take bigger remediation jobs without bottlenecks, which raises revenue capacity.

6

7%Pricing floor

Holding price discipline and cash reserves matters because the model only shows about 7% IRR, so weak pricing can erase owner upside fast.

Environmental Cleanup Core Six Income Drivers

Contract Value And Project Mix

Project Mix

When the work shifts from assessments to remediation, revenue per job rises fast. Site assessments usually take 25 to 35 hours at $180 to $200 per hour, while remediation jobs run 150 to 300 billable hours at $220 to $250 per hour.

Here’s the quick math: a 300-hour remediation project can bill $66,000 to $75,000 before disposal and subcontract costs. The provided benchmark shows annual revenue moving from $576k to $578m as remediation mix rises from 30% to 85%, but the tradeoff is more labor, insurance, compliance work, and working capital.

Price the Mix, Not Just the Hours

Track project type, billable hours, and hourly rate on every bid. Then add disposal, transport, and subcontractor costs before you set the price or owner draw. Bigger remediation jobs can lift gross profit, but only if the margin survives the extra cash tied up in payroll and payables.

- Separate assessment and remediation rates.

- Track hours by project type.

- Reserve cash for disposal delays.

- Test mix before adding staff.

One clean rule: more remediation only helps if you can fund labor, documentation, and site closeout without stretching cash. If working capital gets tight, owner pay gets tight too.

1

Crew Utilization And Labor Productivity

Crew Utilization

This driver is the share of paid crew time that turns into billable remediation work. When billable field hours cover payroll and travel time, owner income rises; when technicians and managers sit idle, the job still pays them. Payroll is modeled at $370k in Year 1 and $1.515m in Year 5, so small scheduling misses can wipe out margin fast.

The key split is billable remediation hours versus training, travel, safety meetings, admin work, and proposal time. Better utilization protects contribution margin and helps the business move from negative EBITDA (earnings before interest, taxes, depreciation, and amortization) to Year 4 profitability. The quick test is simple: if the crew is paid but not billing, owner draw gets pushed back.

Measure Billable Time Fast

Track utilization by role and by project. Use billable hours ÷ total paid hours and compare field crews, supervisors, and project managers each week. If travel and prep time are rising, tighten routing, batch site visits, and match crew size to job size so paid time stays close to revenue time.

- Log non-billable hours daily.

- Separate travel from remediation.

- Set weekly billable targets.

- Review schedule gaps before payroll.

- Price jobs for long travel.

What this estimate hides is site complexity. If safety or compliance work expands, some non-billable time is unavoidable, so the fix is better forecasting and tighter job sequencing, not forcing every hour onto the invoice. The owner wins when paid time turns into billed time before payroll runs.

2

Disposal, Transport, And Subcontractor Costs

Disposal, Transport, and Subcontractor Margin

This cost line sits in project gross margin, not generic overhead. In the model, subcontractor services and equipment rental move from 12% to 8% of revenue, lab analysis and waste disposal fees from 7% to 5%, and travel and logistics from 3% to 2%. Every point saved here lifts the pool that funds payroll, taxes, and owner draw.

Here’s the quick math: on a $250,000 project, cutting these direct costs from 22% to 15% keeps about $17,500 more in gross profit. What this estimate hides is job complexity. Testing requirements, hauling distance, disposal intensity, and specialist subcontractors can turn a strong bid into a thin-margin job fast.

Price the Hidden Job Costs

Build each bid from the job out: test count, waste volume, haul miles, disposal site fees, and specialty trade scope. Track these costs as a share of revenue and compare them to the 15% target. If actuals stay near 22%, the project may still look busy but owner pay will shrink because gross margin has to cover everything else.

- Track disposal cost per job.

- Track haul miles and trips.

- Track subcontractor scope changes.

- Add contingency when site data is weak.

3

Compliance, Insurance, And Safety Burden

Compliance Cost Load

Compliance keeps the license to operate, but it also pulls cash out before owner pay. The fixed load here is $3,000/month for environmental liability insurance, $800/month for certifications and training, and $1,200/month for legal and accounting, or $5,000/month and $60,000/year before permits, documentation, and safety systems.

That spend is not optional overhead; it is operating capacity. If the company trims it too hard, the risk is lost jobs, delayed approvals, and weak incident response, which can hurt cash flow and distributable income faster than the savings help it.

Protect The License

Measure compliance as a fixed monthly run rate plus job-by-job burden. Track insurance, training, legal/accounting, and the time and fees tied to permits, documentation, and prevention so you can see what sits inside gross profit and what hits operating profit.

Keep a separate budget line for safety systems and incident prevention, then test it against active projects and billable hours. If a site needs more reporting or training, price that into the bid instead of eating it in owner draw. One clean rule: compliance spend should be planned, not raided.

- Track the $60,000 fixed annual base.

- Separate job-specific permit costs.

- Protect safety spend before distributions.

4

Equipment Capacity And Utilization

Equipment Capacity And Utilization

Equipment capacity is how much cleanup work the fleet and gear can handle each month. In this business, the $2,500 per month fleet lease and maintenance runs even when trucks are idle, so weak use squeezes gross margin and cash flow. When equipment is underused, the owner sees less profit available for pay or draws.

As volume improves, subcontractor services and equipment rental are modeled to fall from 12% of revenue to 8%. That four-point drop equals $20,000 more gross profit on $500,000 of revenue. Owned equipment helps when jobs are steady; rentals protect cash when demand is uneven.

Track use before you buy more gear

Measure billable equipment days, rental spend as a share of revenue, and fleet cost per project. Track whether each truck or machine earns enough to cover its share of the $30,000 per year fixed fleet cost plus maintenance. If use is thin, keep renting and protect cash.

- Billable hours per machine

- Rental % of revenue

- Fleet downtime by job

- Reserve funding before draws

Build replacement reserves before owner distributions. Set aside cash so worn equipment can be replaced without debt stress. That keeps cleanup capacity available and stops maintenance spikes from cutting into take-home income.

5

Pricing Discipline And Reserve Planning

Pricing Discipline

Remediation estimating accuracy protects owner income before the crew starts. A 300-hour project at $220 to $250 an hour is $66,000 to $75,000 in labor revenue before disposal, subcontractors, travel, and contingency. Miss one of those inputs and gross margin drops, which hits cash and the owner’s draw.

The risk grows with project size. A small assessment is easier to absorb, but a bad bid on a large cleanup can erase profit fast. Use site assessment notes, conservative bids, and tight change-order discipline so extra scope gets billed, not donated.

Bid Controls and Reserves

Track each estimate by billable hours, hourly rates, service mix, disposal fees, subcontractors, travel, and contingency. Here’s the quick math: if any one of those is low, owner pay falls before payroll or insurance move. Reserve planning should sit in the bid, not after the job.

- Log scope changes daily

- Price disposal by project

- Approve extras before work

- Store site notes with bids

What this estimate hides: hauling distance, lab work, and specialist subs can swing margin hard, so the bid needs a cushion that still leaves room for profit.

6

Compare low, base, and high cleanup owner-income scenarios

Owner income scenarios

Owner income swings hard here because Year 1 is still in ramp, Year 4 is break-even-plus, and Year 5 has much more EBITDA to support pay.

| Scenario | Low CaseEarly ramp | Base CaseBreak-even-plus | High CaseMature scale |

|---|---|---|---|

| Launch model | This is the lower-earning ramp case, where the business is still covering startup overhead. | This is the modeled middle case, where scale starts to cover the full cost stack. | This is the stronger-earning case, where the business reaches mature-year operating leverage. |

| Typical setup | Year 1 scale, heavier site-assessment work, high fixed payroll and office load, and no steady distributions yet. | Year 4 scale, broader remediation mix, stronger monitoring and waste work, and enough volume to support positive EBITDA. | Year 5 scale, more remediation and monitoring work, the largest billable base, and the most spread across fixed costs. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$356kRamp loss | $5.3MScale case | $12.6MUpside case |

| Best fit | Use this to stress-test cash support if the launch year stays thin. | Use this as the planning case for budgeting, hiring, and debt capacity. | Use this to test upside if demand, staffing, and execution all stay tight. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Environmental Cleanup Porter's Five Forces Analysis

- Environmental Cleanup BCG Matrix

- Environmental Cleanup Business Model Canvas

- Key Performance Indicators for Environmental Cleanup Services

- Environmental Cleanup Business Plan Template in Pre-Written Word

- Increase Environmental Cleanup Profitability: 7 Key Strategies

- How Much Does It Cost To Run An Environmental Cleanup Business?

- Environmental Cleanup Startup Costs: Plan Around $370K CAPEX

- Environmental Cleanup Financial Model Template in Excel

- How to Start an Environmental Cleanup Business in 3 to 6 Months

- How to Write an Environmental Cleanup Business Plan (2026-2030)

- Environmental Cleanup Marketing Mix

- Environmental Cleanup Marketing Plan

- Environmental Cleanup Business Proposal

- Environmental Cleanup PESTEL Analysis

- Environmental Cleanup Pitch Deck Example Editable PPTX

- Environmental Cleanup Business SWOT Analysis

- Environmental Cleanup Value Proposition Canvas

Frequently Asked Questions

The model carries a $150,000 owner salary before taxes, but that does not mean the business funds it from operations in the first year Year 1 EBITDA is about -$5116k after that salary By Year 4, EBITDA reaches about $6373k, and Year 5 reaches about $293m before reserves, taxes, debt service, and reinvestment