Owner income$180k

Owner income$180kHow Much Do Environmental Consulting Owners Make? $180K Plan

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k  Net margin88%–91%

Net margin88%–91% Revenue for target pay$199,688

Revenue for target pay$199,688 Business difficultyHard

Business difficultyHard

Key Takeaways

- Rates only help when scope and collections stay tight.

- Utilization turns proposal time into paid client hours.

- Shift mix toward advisory, but protect margins.

- Fixed overhead and reserves can strain owner pay.

Owner income$180kNet margin88%–91%Revenue for target pay$199,688Business difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This output is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Results move with collections timing, payroll mix, and reserve policy.

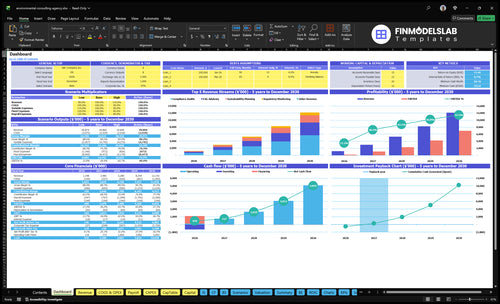

Checking owner income in Environmental Consulting?

The dashboard in the Environmental Consulting Financial Model Template shows revenue, gross margin, payroll, fixed overhead, and owner pay. Open the model.

Owner-income model highlights

- $180k owner salary

- 88%-91% gross margin

- $194.4k fixed overhead

How much can a solo environmental consultant make?

A solo Environmental Consulting owner can generate the model’s $199,688 Year 1 revenue from 50 acquired customers, but take-home pay is not the same as revenue; What Is The Current Growth Trend Of Your Environmental Consulting Business? is the growth check before assuming distributions. With staffed-model fixed overhead at $194,400 before payroll, the simple pre-payroll gap is only $5,288, so staffing data must be reviewed first.

Solo upside

- Keep more delivery margin

- Do the billable work yourself

- Limit payroll drag early

- Cap growth by personal hours

Scale tradeoff

- $1,754,700 Year 5 revenue

- Payroll expands materially

- More staff means more capacity

- Review distributions before planning

How much revenue does an environmental consulting firm need to pay the owner?

Environmental Consulting should treat a $180,000 owner salary as a result, not a starting point. Here’s the quick math: at $199,688 revenue and 88% gross margin, gross profit is $175,725, which still does not cover $194,400 fixed overhead plus $120,000 senior consultant payroll, before owner pay.

What revenue must fund first

- Direct costs come off first

- Variable costs reduce cash fast

- $194,400 fixed overhead is locked in

- Staff payroll must be paid before owner pay

What the year 1 math says

- $199,688 revenue yields $175,725 gross profit

- 88% gross margin still falls short

- $120,000 senior consultant payroll adds pressure

- Use owner pay as a planning output

Is an environmental consulting business profitable?

Environmental Consulting can be profitable, but Year 1 is tight: $199,688 of revenue sits against $194,400 of fixed overhead and $300,000 of payroll, so operations do not support owner distributions. Profit improves as revenue grows to $1,754,700 by Year 5 and gross margin reaches 91%. The catch is that long sales cycles, delayed receivables, regulatory complexity, liability exposure, and reliance on qualified technical staff can squeeze cash and slow scale-up.

Year 1 pressure

- $199,688 revenue in Year 1

- $194,400 fixed overhead

- $300,000 payroll cost

- No owner distributions from operations

Year 5 upside

- $1,754,700 revenue by Year 5

- 91% gross margin

- Owner shifts to sales and review

- Hire and quality control become key

What drives owner income most?

1

$150-$285Billing Rate

Higher hourly rates, from $150 to $285, lift pre-tax owner take-home because each billable hour turns into more gross profit.

2

8-35hUtilization

Moving more hours into billable work raises revenue without the same jump in overhead, so owner cash builds faster.

3

$194KOverhead

Holding fixed overhead near $194,400 a year protects cash, since every dollar of gross profit has less drag before breakeven.

4

1-5 FTEStaffing Leverage

Scaling staff in step with demand lets the firm sell more consulting hours than one owner can deliver alone.

5

45%-30%Project Mix

Shifting mix away from compliance audits and toward ESG advisory and planning improves the blended rate and take-home per project.

6

15%-30%Recurring Revenue

Growing monitoring work makes cash less lumpy and helps support owner pay before reinvestment.

Environmental Consulting Core Six Income Drivers

Billing Rate

Billing Rate

Billing rate is the hourly price charged for paid work, so it lifts revenue only when scope, collections, and delivery cost stay under control. In Year 1, model rates are $150 for regulatory monitoring, $175 for compliance audits, $200 for sustainability planning, and $225 for ESG advisory. By Year 5, they rise to $190, $215, $240, and $285.

That price ladder matters because a shift from lower-rate monitoring to higher-rate advisory raises revenue per billable hour. But if the team underquotes scope or clients pay late, the gain can disappear fast. The real driver is not just rate; it’s rate times billable hours, less rework, less write-off, and less cash tied up in receivables.

Raise Rate, Protect Margin

Track three things on every job: hours billed, hours spent, and cash collected. That shows whether the quoted rate is real or just paper. For example, a higher ESG advisory rate only helps if scoping stays tight and senior consultant time does not spill into unbilled revisions, travel, or extra review cycles.

Price by service line, not one blended rate, and update the mix as work shifts toward advisory. The question is simple: does the rate increase cover delivery cost and collection delay? If not, the owner may see more revenue but less take-home pay because payroll, overhead, and unpaid invoices eat the spread.

1

Utilization

Utilization

Utilization is the share of working time that turns into paid client work. In this model, one engagement can run 8 hours for regulatory monitoring or 25 hours for compliance audits in Year 1, then rise to 35 hours for audits and 30 hours for ESG advisory by Year 5. More billable hours lift revenue, but only if pricing keeps up with scope.

Every non-billable proposal, travel day, review cycle, and admin task cuts owner income unless it is built into the fee. A 35-hour audit uses about 4.4x the billable time of an 8-hour monitoring job, so low utilization can squeeze margin fast if the work is not scoped and billed well.

Raise Billable Hours

Track utilization by consultant, service line, and client each week. Split time into billable work, proposals, travel, reviews, and admin. That shows where paid capacity is leaking and which jobs are consuming labor without adding cash to the business.

- Log billable and non-billable hours weekly.

- Price travel and rework upfront.

- Cap audit hours before kickoff.

Set scope caps and charge for extra rounds, site visits, and rework. If a job needs more than planned hours, update the fee before the team starts the extra work. The goal is to keep paid hours high enough that payroll and owner draw stay covered after fixed costs.

2

Project Mix

Project Mix

Service mix changes revenue quality, not just revenue size. In Year 1, the mix is 45% compliance audits, 25% ESG advisory, 20% sustainability planning, and 15% regulatory monitoring. By Year 5, ESG advisory rises to 40% and sustainability planning to 35%, so the average project price can improve if scope stays tight and clients keep paying for the higher-end work.

What matters for owner income is the margin after labor, rework, and delay. Higher-rate work can pay better than monitoring, but it can also bring more liability, longer turnaround, and more senior time. With fixed overhead at $16,200 per month, the mix has to cover that cost first, then leave enough cash for the owner draw. No service line is automatically best.

Track mix by margin, not just sales

Measure each service by hours sold, realized rate, rework, and days to invoice. Use the model rates as the starting point: compliance audits from $175 to $215, ESG advisory from $225 to $285, sustainability planning from $200 to $240, and monitoring from $150 to $190.

Then test which mix gives the best cash result after delivery cost. A higher share of ESG advisory and planning can lift owner pay, but only if the team controls scope, keeps turnaround fast, and avoids underpricing. If a service needs expert review or creates heavy liability, price it like a premium job or keep the volume low.

- Track margin by service line.

- Watch scope creep weekly.

- Invoice fast after delivery.

- Price risk, not just hours.

3

Staffing Leverage

Staffing Leverage

Staffing leverage is when the owner stops doing every billable task and the team starts carrying client work. In Year 1, payroll is already $300,000 for a $180,000 CEO/Lead Environmental Consultant plus one $120,000 Senior Environmental Consultant, so revenue has to cover salaries before owner pay. If billable time slips or rework rises, payroll becomes a cash drain.

By Year 5, the known team is five senior consultants, three analysts, and two business development managers, before any junior consultant line. That helps only if senior staff stay billable, analysts absorb support work, and sales keep the bench full. One clean line: headcount raises profit only when hours are sold, not just staffed.

Make Payroll Pay

Track billable utilization, realized revenue per payroll dollar, and rework hours by role. Utilization means the share of working time that becomes paid client work. If a senior is spending time on admin or cleanup, the owner is paying premium wages for low-value work.

- Billable hours by person

- Rework hours and write-offs

- Revenue per payroll dollar

- Non-billable time by role

Use analysts for repeatable tasks, keep seniors on audits and advisory, and make business development fill the calendar early. The goal is simple: keep payroll tied to client work, so owner income grows with delivery volume instead of getting trapped in fixed salary cost.

4

Recurring Revenue

Recurring Compliance Revenue

Recurring compliance support, monitoring, reporting, and advisory work can smooth cash flow and cut the pressure to sell new work every month. In this model, regulatory monitoring rises from 15% of customers in Year 1 to 30% in Year 5, and ESG advisory rises from 25% to 40%. That usually helps owner pay stay steadier, but only if renewals and scope stay tight.

Here’s the catch: retainers improve predictability, not guaranteed income. If a few clients make up too much of recurring revenue, or if senior consultants spend too many hours on low-complexity monitoring, margin gets squeezed fast. Client concentration, renewal timing, scope creep, and senior-staff usage are the main risks to watch.

Track Renewals and Margin

Measure retainer count, renewal date, recurring revenue share, and hours by senior staff. The key inputs are customers on monitoring, advisory retainer price, renewal rate, and how much time each account uses each month. If a retainer needs constant partner time, it may feel stable but still hurt take-home profit.

Use a simple rule: recurring work should cover the labor it consumes and leave room for overhead and owner draw. Add clear service limits for reporting, monitoring, and advisory calls, then reprice when scope expands. More recurring work only helps if it stays efficient.

5

Overhead And Reserves

Overhead And Reserves

$16,200 a month in fixed overhead is the first claim on gross profit, before owner pay. That is $194,400 a year, with $8,500 rent, $2,200 professional insurance, $1,800 software subscriptions, and $1,500 accounting and legal services. If gross profit does not clear that base, take-home pay gets squeezed fast.

Reserves matter because cash leaves on a different clock than profit. This firm also needs room for payroll timing, tax reserves, equipment, and delayed receivables, so owner draw should stay separate from working capital and growth cash. One clean rule: profit is not spendable until the cash lands.

Protect Cash Before Owner Pay

Track overhead as a monthly run rate and compare it to gross profit each month. Here’s the quick math: $16,200 in fixed costs means every drop in collections hits owner pay quickly. Keep a separate reserve bucket for taxes, payroll, and slow-paying clients before moving money to the owner.

- Review rent, insurance, software monthly.

- Set tax cash aside on each invoice.

- Separate owner draw from reserves.

- Watch unpaid invoices every week.

If receivables slow or staff pay runs before client cash arrives, reserves have to bridge the gap. That’s why the key inputs are fixed overhead, expected collections timing, and near-term payroll. Control those three, and the firm keeps pay to the owner from getting trapped in the business.

6

Compare owner income scenarios without treating them as guarantees

Owner income scenarios

Owner income swings with margin, payroll, and how fast billable work ramps. The table shows a lean launch, a salary-target case, and a mature-year upside case.

| Scenario | Low CaseDifficult launch | Base CaseScaling plan | High CaseMature-year upside |

|---|---|---|---|

| Launch model | This is the lean launch case with Year 1-style revenue and no profit-funded owner draw. | This is the modeled case where the planned $180,000 owner salary is a target, but operating profit may not cover it yet. | This is the stronger case built off Year 5 revenue and a 91% gross margin, but payroll and reserves still cap owner take-home. |

| Typical setup | Revenue is about $199,688, gross margin is 88%, fixed overhead is $194,400, and payroll is $300,000, so cash stays tight. | The business is scaling service lines with growing payroll, so the owner salary still needs outside cash or stronger revenue support. | Revenue reaches $1,754,700, margins improve, and the team is larger, so the owner's upside depends on keeping reserves intact. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No profit drawDownside case | $180,000 salary targetSalary target | Reserve-limited upsideUpside case |

| Best fit | Use this to test launch cash if client work starts slowly or staffing costs run ahead of billings. | Use this for the operating plan if you want to hold the planned salary while growth is still catching up. | Use this to test mature-year capacity if demand holds and staffing stays efficient. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. They are directional and exclude personal taxes, debt service, and guaranteed payouts.

Related Products

- Environmental Consulting Porter's Five Forces Analysis

- Environmental Consulting BCG Matrix

- Environmental Consulting Business Model Canvas

- 7 Core KPIs to Track for Environmental Consulting Success

- Environmental Consulting Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Environmental Consulting Profitability Now

- How Much Does It Cost To Run Environmental Consulting Monthly?

- How Much It Costs To Start An Environmental Consulting Business: $640k CAPEX

- Environmental Consulting Financial Model Template in Excel

- How To Open An Environmental Consulting Agency In 8–16 Weeks

- How to Write an Environmental Consulting Business Plan

- Environmental Consulting Marketing Mix

- Environmental Consulting Marketing Plan

- Environmental Consulting Business Proposal

- Environmental Consulting PESTEL Analysis

- Environmental Consulting Pitch Deck Example Editable PPTX

- Environmental Consulting Business SWOT Analysis

- Environmental Consulting Value Proposition Canvas

Frequently Asked Questions

The model includes a planned $180,000 pre-tax CEO/Lead Environmental Consultant salary, but profit-funded take-home is not supported in Year 1 Revenue is $199,688, gross margin is 88%, and fixed overhead is $194,400 before payroll Treat the $180,000 as a target pay line, not a guaranteed distribution