Owner income$145K

Owner income$145KHow Much Environmental Control Systems Owners Make at $145K Plus

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145K  Net margin19%–45%

Net margin19%–45% Revenue for target pay$2.26M

Revenue for target pay$2.26M Business difficultyHard

Business difficultyHard

4

Key Takeaways

- Qualified projects drive revenue only when crews and cash align.

- Better pricing and procurement protect gross margin.

- Recurring service smooths income, but only if priced right.

- Working capital and overhead decide owner take-home.

Owner income$145KNet margin19%–45%Revenue for target pay$2.26MBusiness difficultyHardWant to test your owner pay case?

Owner income calculator

Estimate pre-tax owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue mix, payroll load, debt, reserves, and execution.

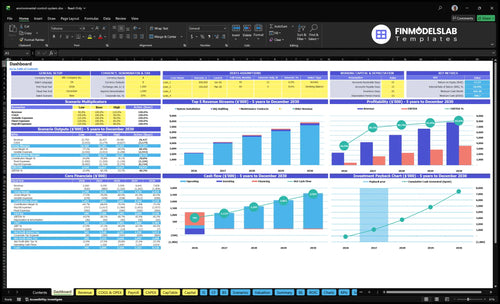

How does owner income change in the Environmental Control Systems model?

The screenshot shows owner take-home assumptions, plus revenue from about $449K to $497M, variable cost load from 30% to 24%, and EBITDA to about $186M in Year 5. Open the Environmental Control Systems Financial Model Template. Planning tool, not a promise.

Owner-income model highlights

- Owner take-home outputs

- Revenue and margin trends

- Scenarios, costs, debt

Can an environmental control systems business pay an owner without the owner doing every job?

Yes, Environmental Control Systems can pay an owner without that owner doing every job, but the break-even point rises as fieldwork drops. In the managed-team case, payroll starts at $600K in Year 1 and grows to $1.435M by Year 5, so the business needs enough backlog, service contracts, and labor use to cover that load. Short-term owner income can dip, but recurring maintenance moving from 40% to 95% customer allocation helps steady cash flow.

Owner model shift

- Owner billable hours keep payroll lean

- Less fieldwork means higher break-even

- Sales and project management can replace installs

- Utilization must stay high across the team

Cash flow drivers

- Year 1 payroll is $600K

- Year 5 payroll reaches $1.435M

- Maintenance mix rises from 40% to 95%

- Backlog must fund the added payroll

How much revenue does an environmental control systems business need to pay the owner?

Environmental Control Systems needs about $1.41M in revenue before owner distributions to support a $145K salary, using a $986K cost base and a 70% contribution margin. Year 1 revenue of about $449K is well short, so owner pay has to come from funding or lower overhead. Year 3 revenue of about $2.06M gets much closer, but cash for distributions still stays tight after reserves.

Target pay math

- $145K owner salary target

- $986K fixed cost base

- 70% contribution margin

- $1.41M break-even revenue

What the model says

- $449K Year 1 revenue falls short

- Pay needs funding or lower overhead

- $2.06M Year 3 is much closer

- Reserves still cut take-home

How much can an environmental control systems owner make?

An Environmental Control Systems owner can make $145K in an owner-led setup only if startup capital covers early losses; in the larger Year 5 case, EBITDA reaches about $186M before debt, taxes, reserves, and distributions. For setup context, see How To Launch Environmental Control Systems Business?.

Owner earnings by size

- Small: $145K owner-manager salary target

- Year 1: $449K revenue

- Year 1: $986K payroll, overhead, marketing

- Year 3: $206M revenue, near break-even EBITDA

What drives take-home

- Protect contribution margin: 735% listed model input

- Build capacity without bloated overhead

- Shift mix toward higher-margin projects

- Add recurring service contracts for stability

Want the six income drivers at a glance?

1

$2.3M-$7.8MProject Volume

More installs and larger contracts drive revenue from $2.26M in Year 1 to $7.83M in Year 5, which is the main path to owner take-home.

2

70%-76%Gross Margin

Keeping equipment, materials, labor, and subcontractor costs tight protects contribution, so more of each job turns into profit.

3

40%-95%Recurring Service

More maintenance, monitoring, and inspection work smooths cash flow and adds repeat revenue after the install is done.

4

12.5-18.0Crew Utilization

Higher billable hours per active customer spread payroll across more revenue, while idle field time cuts owner take-home fast.

5

$2.66MOverhead Load

The fixed expense base is about $2.658M a year, so extra admin and project management cost comes straight out of profit.

6

$399KWorking Capital

The model needs a $399K cash floor in Month 6, so weak reserves, callbacks, or retainage can delay owner distributions.

Environmental Control Systems Core Six Income Drivers

Project Volume And Average Contract Value

Project Volume and Contract Value

When more installation, retrofit, upgrade, maintenance, and IAQ audit jobs are qualified before crews are booked, revenue grows and owner pay can rise. The model starts at $185 per installation hour with 160 installation hours and 85% installation allocation in Year 1, then moves to $210, 140 hours, and 65% by Year 5 as service mix grows.

Here’s the catch: higher sales only help if deposits, procurement, scheduling, and field execution keep pace. If work is sold faster than crews and cash can deliver, backlog turns into delay, overtime, and weak cash flow. That can squeeze gross profit and push owner draws down even when top-line revenue looks strong.

Qualify Work Before You Book It

Track booked hours, contract value per job, and crew capacity each week. Keep the quote tied to the real mix: installation, retrofit, maintenance, and audit work all need different labor, parts, and timing. One clean rule: don’t sell the next project until deposits, materials, and start dates are locked.

Use a simple gate for every deal: scope approved, margin checked, deposit collected, and procurement cleared. That protects cash and keeps owner income tied to profitable work, not just busy crews.

- $185 to $210 per hour

- 160 to 140 hours per install

- 85% to 65% installation mix

1

Gross Margin On Equipment And Labor

Equipment and Labor Gross Margin

This driver is the gap between the bid and the real cost of hardware, sensors, field labor, commissioning, subcontractors, and warranty fixes. When the job is priced right, the same revenue turns into more owner cash instead of getting eaten by materials, labor, and callbacks.

Here’s the quick math: equipment and hardware cost drops from 185% to 155%, and field supplies drop from 45% to 25% across the model. Sales commissions stay at 4%, so the margin lift has to come from better procurement, fewer change-order misses, and tighter crew productivity.

Price the Full Job

Build the quote from the work, not just the visible gear. Include design time, calibration, testing, commissioning, subcontractors, and a warranty reserve before you price. If any of those are left out, gross margin leaks fast and the owner ends up paying for it out of profit.

- Track bid-to-bill on every job.

- Separate hardware, labor, and warranty cost.

- Quote change orders before work starts.

- Review callbacks against each crew.

Watch actual cost versus quote by bucket: hardware, field supplies, labor, and rework. If calibration or testing keeps running over plan, raise the rate or tighten scope. Better margin does not just improve accounting profit; it gives the owner more room to pay themselves without starving payroll or cash reserves.

2

Recurring Maintenance Revenue

Recurring Maintenance Revenue

Service contracts smooth cash flow between installs, so owner income depends less on chasing new projects. In this model, maintenance allocation rises from 40% in Year 1 to 95% in Year 5, with pricing moving from $145 to $170 per hour and hours per contract from 8 to 10. That lifts technician utilization and steadies revenue when install work slows.

The catch is simple: recurring revenue only helps pay the owner if it covers labor, travel, parts, callbacks, scheduling, billing, and account management. Underpriced service contracts create busy crews, not profit. If the hourly rate does not clear fully loaded service cost, the work fills the calendar but does not raise take-home pay.

Price Service Time, Not Just Visits

Track billed hours versus worked hours, plus callbacks, travel, and parts use on every contract. If a 10-hour agreement at $170 per hour does not cover the real cost of dispatch, labor, and admin, reprice it before renewal. One clean rule: if the contract is busy but not profitable, it is too cheap.

- Measure callback hours each month.

- Separate travel from wrench time.

- Renew only after cost review.

- Bundle account management into pricing.

Use service plans to keep techs busy between installations, but forecast them as margin work, not just volume work. When contract hours rise from 8 to 10, owner income improves only if dispatch stays tight and rework stays low. Otherwise, the extra hours just add payroll drag.

3

Field Labor Utilization

Field Labor Utilization

Field labor utilization is the share of installer, controls tech, and service time that turns into billed work or protected margin. In this model, the field team grows from 2 lead installation technicians in Year 1 to 6 by Year 5, plus design engineers and smart systems specialists. Payroll rises from about $600K to $1435M, so idle crews cut owner income fast.

Here’s the quick math: if jobs slip, payroll still runs, but revenue waits. If crews are overbooked, overtime, rework, and warranty callbacks eat gross profit, so the owner takes home less even when sales look strong. The owner’s job shifts from doing field work to managing backlog, commissioning, quality control, and service dispatch.

Track Hours, Not Hope

Measure billable hours versus available hours, plus overtime, callback rate, and schedule slippage by crew. Keep utilization tied to project timing, since this business wins when install, controls, and service labor are booked in the right order. One clean rule: do not add headcount unless backlog and commissioning slots can keep the team busy.

- Track weekly billable hours

- Flag overtime above target

- Review callbacks by technician

- Match hires to backlog

Use staffing plans that separate install labor from service labor, because each has different demand swings. If service contracts soften, shift hours into maintenance and dispatch before hiring again. That protects gross margin, keeps cash steadier, and leaves more profit for owner pay.

Overhead And Management Load

Overhead And Management Load

Fixed overhead takes a direct bite out of owner pay. In this model, it runs $22,150 per month, or about $265,800 per year, before online marketing or payroll growth. That covers warehouse and office rent, insurance, hosting, software, utilities, communications, and brand management. One line is clear: if gross profit does not grow faster than this load, the owner’s draw gets squeezed.

Online marketing adds $120K in Year 1 and rises to $220K by Year 5. Payroll is the biggest fixed load, so the real risk is hiring ahead of revenue density. Necessary overhead helps with estimating, compliance, and project management, but adding it too early can erase take-home even when sales look healthy on paper.

Watch Fixed Load Before You Hire

Track fixed overhead as a share of gross profit, not just revenue. Use a simple rollup: rent, insurance, software, utilities, communications, marketing, and salaried payroll. If one more hire does not raise booked work, utilization, or recurring service hours fast enough, delay it. That keeps cash free for deposits, field work, and owner pay.

Here’s the quick math: if overhead is $22,150 a month plus marketing, the business needs enough monthly gross profit to cover that base before the owner takes a draw. A clean rule: hire when backlog and repeat service demand can support the new cost for several months, not just one good sales month.

5

Cash Reserves And Working Capital

Working Capital Buffer

Cash reserves are not extra money here. They cover payroll, equipment deposits, supplier bills, warranty work, retainage delays, and job timing gaps, so the owner can keep crews moving even when profit has not turned into cash yet.

In Year 1, revenue is about $449K, but equipment cost alone is 185% of revenue, or about $831K before supplies, commissions, vehicles, payroll, and rent. That means paper profit can look fine while cash is tight, so owner pay has to wait until deposits and billed work fund the next round of materials and labor.

Track Cash by Job, Not Just by Month

Here’s the quick math: start with projected contract deposits, then map purchase timing, payroll dates, and retainage. If deposits do not cover the next materials order and payroll cycle, the business is funding growth with the owner’s cash. That is where take-home income gets squeezed.

Watch cash on hand, days cash cover, unpaid retainage, and warranty reserve needs every week. Keep a simple forecast for deposits, supplier payments, and callbacks, and only draw profit after those are funded. One clean rule: no owner distribution until the next job wave is paid for.

- Track deposits against purchase orders

- Match payroll to billing dates

- Reserve cash for callbacks and warranties

- Delay draws during seasonal slowdowns

6

Compare low, base, and high owner income scenarios

Owner income scenarios

Income shifts fast in this model because staffing, billable hours, and fixed overhead scale together. Year 1 is cash tight, while Year 5 can support a much larger owner pay range.

| Scenario | Low CaseStartup | Base CaseStable operator | High CaseScaled team |

|---|---|---|---|

| Launch model | This is the startup ramp case, with Year 1 revenue and thin cash room. | This is the middle case, with Year 3 scale and stronger operating spread. | This is the scaled case, with Year 5 volume and the highest modeled earnings. |

| Typical setup | The model runs install-heavy work, $2.26M revenue, about $655k payroll, and $265.8k fixed overhead. | The model reaches $5.51M revenue, about $1.11M payroll, and a more balanced service mix. | The model reaches $7.83M revenue, about $1.49M payroll, and fuller maintenance and IAQ work. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $440kStartup case | $2.2MStable case | $3.5MScaled case |

| Best fit | Use this to test what happens if ramp-up stays slow and cash stays tight. | Use this for planning a normal path with steady demand and a growing service book. | Use this to test a stronger path with fuller crews and more recurring work. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Environmental Control Systems Porter's Five Forces Analysis

- Environmental Control Systems BCG Matrix

- Environmental Control Systems Business Model Canvas

- What Are The 5 KPI Metrics For Environmental Control Systems Business?

- Environmental Control Systems Business Plan Template in Pre-Written Word

- How Increase Environmental Control Systems Profitability?

- How Increase Environmental Control Systems Profitability?

- Environmental Control Systems Startup Costs: $422K CAPEX Plan

- Environmental Control Systems Financial Model Template in Excel

- How to Open an Environmental Control Systems Business in 3–6 Months

- How To Write An Environmental Control Systems Business Plan?

- Environmental Control Systems Marketing Mix

- Environmental Control Systems Marketing Plan

- Environmental Control Systems Business Proposal

- Environmental Control Systems PESTEL Analysis

- Environmental Control Systems Pitch Deck Example Editable PPTX

- Environmental Control Systems Business SWOT Analysis

- Environmental Control Systems Value Proposition Canvas

Frequently Asked Questions

Early take-home should be conservative because the model shows about $449K Year 1 revenue against $600K payroll, $2658K fixed overhead, and $120K marketing before debt, taxes, and reserves The $145K owner-manager salary line may be possible only with startup funding or lower overhead Distributions are not safely supported in the early ramp-up