Owner income$1.31M to $29.04M

Owner income$1.31M to $29.04MHow Much Can an Ethical Hacking Course Owner Make? Year 1 $13M

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.31M to $29.04M  Net margin49% to 80%

Net margin49% to 80% Revenue for target pay$198k to $3.01M

Revenue for target pay$198k to $3.01M Business difficultyMedium

Business difficultyMedium

An ethical hacking training course owner can make strong money, but revenue is not owner income In the researched assumptions, Year 1 revenue is $2371M and EBITDA is $1167M after payroll, lab hosting, instructor commissions, marketing, software, rent, insurance, and admin costs If the owner is also the CEO, modeled owner economic capacity is about $1312M before taxes, reserves, debt service, and reinvestment By Year 5, revenue reaches $36113M and EBITDA reaches $28899M, driven by more corporate cohorts, public cohorts, advanced modules, and higher pricing

Owner income$1.31M to $29.04MNet margin49% to 80%Revenue for target pay$198k to $3.01MBusiness difficultyMediumWant to test your ethical hacking course owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, operating costs, reserves, and target pay.

Planning note: This is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Ethical Hacking Training Course model?

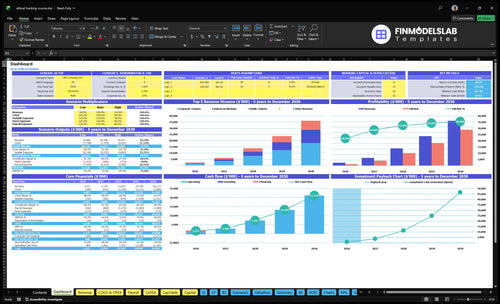

This screenshot shows revenue, margin, costs, reserves, and owner pay in the Ethical Hacking Training Course Financial Model Template. It also shows revenue growth from $2,371M to $36,113M, EBITDA from $1,167M to $28,899M, with break-even in Month 1 and payback in 1 month—open the model.

Owner-income model highlights

- Owner pay is explicit

- Revenue and EBITDA track

- Month 1 break-even

How much does an ethical hacking training course owner make?

An Ethical Hacking Training Course owner doesn’t make tuition revenue; in the researched model, Year 1 owner capacity is $1.312M if the owner is CEO, made up of $1.167M EBITDA plus a $145,000 CEO salary. For the operating metrics behind that gap, see What Are The 5 KPIs For Ethical Hacking Training Course?, because actual take-home cash still depends on taxes, reserves, debt service, reinvestment, and board or lender rules.

Owner Pay

- Year 1 revenue: $2.371M

- Year 1 EBITDA: $1.167M

- CEO salary: $145,000

- Owner capacity: $1.312M before cash claims

What Moves It

- Year 5 capacity: $29.044M

- Year 5 EBITDA: $28.899M

- Key levers: cohorts, pricing, lab costs

- Risk levers: staffing and marketing efficiency

What costs reduce ethical hacking training course owner income?

If your Ethical Hacking Training Course is under-earning, the biggest drag is usually instructors, labs, payroll, marketing, and required infrastructure. In Year 1, cloud lab hosting can hit 70% of revenue, instructor commissions 50%, marketing 60%, and payment fees 20%; for profit fixes, read How Increase Ethical Hacking Training Course Profits?

Main cost drains

- Cloud labs: 70% of revenue

- Instructor commissions: 50%

- Marketing: 60%

- Payment fees: 20%

Fixed cost load

- Monthly overhead: $14,150

- Payroll: $145k CEO

- Payroll: $130k lead instructor

- Capex: $232k setup spend

Can an ethical hacking training course scale without the owner teaching every class?

Yes—Ethical Hacking Training Course can scale without the owner teaching every class, but the business shifts from owner labor to systems, instructors, and quality control. Owner-led classes help margin early, yet they cap capacity; once you add hired instructors, costs rise through $130,000 lead instructor FTEs and external instructor commissions of 50% in Year 1, easing to 30% by Year 5.

How it scales

- Self-paced modules grow from 100 to 1,200.

- Public cohort tuition rises from $2,800 to $4,000.

- Corporate cohorts scale from 15 at $18,000 to 70 at $24,000.

- Live cohorts keep premium pricing intact.

What can break it

- Support burden grows with seat count.

- Lab reliability must stay tight.

- Curriculum updates need to keep pace.

- Quality control has to be repeatable.

Want the six drivers of ethical hacking course income?

1

$1.2M-$28.9MEnrollment Volume

More paid seats drive EBITDA from $1.167M to $28.899M as revenue scales from $2.371M to $36.113M.

2

15-70Corporate Cohorts

B2B cohorts are the fastest way to add high-value revenue because each contract brings a large ticket with limited extra selling cost.

3

$199-$24KPackage Mix

Rising prices across public cohorts, advanced modules, and corporate cohorts lifts revenue per sale without the same jump in headcount.

4

45%-88%Occupancy

Higher occupancy across 20 to 22 billable days a month turns the same teaching team into more billable output and better margin.

5

12%-8%Cost Control

Cloud hosting and instructor commissions fall from 12% of revenue to 8%, so more gross profit reaches the owner.

6

6%-4%Marketing Efficiency

Lead acquisition spend drops from 6% to 4% of revenue, which protects margin as the course base grows.

Ethical Hacking Training Course Core Six Income Drivers

Enrollment Volume

Enrollment Volume

Enrollment volume is the number of filled student seats across public cohorts, corporate cohorts, and advanced modules. In this model, revenue grows as occupancy rises from 450% in Year 1 to 880% in Year 5, while billable days move from 20 to 22 per month. More seats only help if they are paid seats; empty seats still carry payroll, fixed overhead, software, and lab readiness costs.

The revenue swing is big: public cohorts grow from 30 to 150, corporate cohorts from 15 to 70, and advanced modules from 100 to 1,200. That means the owner’s take-home income depends on converting interest into qualified enrollments, not just traffic. Vanity leads do not pay the bills unless they fill seats and hold attendance long enough to finish the cohort.

Track fills, not clicks

Measure seats sold, fill rate, and billable days per month before adding ads or staff. If one cohort is underfilled, the fixed cost burden lands on fewer students, so gross margin drops fast. One simple rule: don’t scale capacity until the next cohort has enough confirmed enrollments to cover its live delivery and lab support.

- Track seats sold by cohort type.

- Watch fill rate by month.

- Separate paid leads from inquiries.

- Test conversion before buying traffic.

- Protect margin with minimum class size.

Forecast by cohort, then compare actual fills against plan each month. If lead volume is high but confirmed seats lag, cut weak channels and tighten follow-up. That keeps payroll, software, and lab costs matched to real revenue instead of hopeful demand.

1

Pricing And Package Mix

Pricing And Package Mix

Price per enrollment sets the ceiling for contribution margin. In this model, corporate cohorts rise from $18,000 to $24,000, public cohorts from $2,800 to $4,000, advanced modules from $199 to $299, and certification exam fees from $450 to $550. Bundle live instruction, lab access, mentoring, and certification prep, because the package, not just the seat, drives take-home income.

Higher tuition only helps if conversion, completion, and perceived value hold. Here’s the quick math: a better price lifts revenue per seat, but low pricing can fill seats and still leave too little room for instructors, labs, support, and owner pay. The key inputs are seats sold, package mix, add-on attach rate, and delivery cost per cohort.

Bundle Value, Then Test Price

Track pricing by cohort type, not as one blended number. Watch fill rate, refund rate, completion rate, and gross margin on each offer. If public cohorts convert well at $2,800 to $4,000, test the top end first. If corporate buyers want proof, use private cohorts and role-based labs to support the $18,000 to $24,000 range.

- Measure conversion by package.

- Track margin per enrolled student.

- Test add-ons before discounting.

- Price exam prep separately.

Use bundles to protect cash flow. A stronger package mix can lift revenue without adding many more students, but only if support load stays controlled. If discounts are needed to close deals, cut scope first, not price. That keeps the owner’s draw safer because each seat leaves more room after teaching, labs, and admin costs.

2

Delivery Model And Instructor Utilization

Delivery Mix and Instructor Use

Delivery choices decide how much tuition turns into gross margin, meaning revenue left after direct delivery costs. If cloud lab hosting takes 70% of revenue in Year 1, only 30% is left before overhead; by Year 5, hosting at 50% and external instructor commissions falling from 50% to 30% give the owner far more room to pay themselves.

Owner-led cohorts usually protect margin best, while hired instructors scale capacity. Hybrid labs and recorded modules cut repeated teaching, and office hours keep completion up without full live time. The risk is simple: underused instructors create payroll drag, but weak support can hurt completion and slow future enrollments.

Track Lab Cost and Teaching Load

Measure fill rate, lab hosting cost per seat, instructor commission %, and live teaching hours per cohort. Here’s the quick math: every $100 of revenue kept from direct delivery costs matters more than adding extra seats if the class is still half empty.

Use owner-led delivery for premium cohorts, then move repeat content into recordings so instructors handle only labs and office hours. Keep support tight enough for completion, but don’t keep staff on the schedule when seat demand is light, or the owner’s draw gets squeezed fast.

3

Marketing Efficiency

Marketing Efficiency

Marketing efficiency matters more than raw lead count because profit comes from cost per enrollment, not traffic volume. In this model, digital marketing and lead acquisition run at 60% of revenue in Year 1 and 40% in Year 5, while payment and sales fees stay at 20%. That means every filled seat has to carry enough margin to cover teaching, labs, and owner pay.

At $2,800 public tuition, every 1 percentage point of acquisition cost equals about $28 less contribution per student. Paid traffic can scale losses fast if the students do not enroll, complete, or renew, so the real question is not how many leads you buy. It’s which channel turns into paid seats at a low enough cost.

Track Cost Per Enrolled Student

Measure lead-to-enrollment conversion, cost per enrollment, payment fees, and refund rate by channel. Use search content, webinars, professional networking, partnerships, and email follow-up to raise conversion before adding more ads. One clean rule: if a channel brings leads but not seats, it is a cost center, not a growth engine.

- Track cost per paid seat.

- Compare channels weekly.

- Test follow-up speed.

- Cut weak paid traffic.

What this hides: low-cost leads still hurt if they no-show, drop out, or need heavy support. So watch show-up rate, completion rate, and repeat purchase rate together. If those fall, marketing spend can rise while owner income falls, even when total leads look strong.

4

Corporate And Group Training Contracts

Corporate Training Cohorts

Corporate contracts are the highest-value order in this model. They include team packages, annual refresh training, private cohorts, and role-based labs. Here, corporate cohorts rise from 15 at $18,000 in Year 1 to 70 at $24,000 in Year 5, so revenue gets larger and cash flow gets steadier. One closed cohort can cover more fixed overhead than several public enrollments, but custom work can quietly squeeze margin.

Track contract value, cohort size, close time, instructor hours, and lab customization. If a deal needs extra prep or extra support, gross margin falls even when topline looks strong. B2B sales cycles are longer, so delayed closes can push owner pay out by weeks. The real test is not just landing the deal, but keeping delivery tight enough that the higher price turns into profit.

Protect Margin Per Cohort

Measure booked cohorts, days to close, and gross margin per cohort. Set one standard package with fixed labs, seats, and support, then charge extra for custom requests. That keeps $24,000 contracts from turning into low-margin projects and helps each cohort carry more of the monthly fixed overhead.

Forecast cash by cohort start date, not just signed leads. Watch scope creep on private cohorts and role-based labs, because extra instructor time can erase the gain from a bigger order. If payment terms slip, owner draws should wait until the cohort cash is in.

5

Operating Cost Control And Reserves

Protect Cash Before Owner Pay

Owner pay should come after required operating costs and a real reserve floor. This model needs $14,150 in monthly fixed overhead covered and $874k in Month 1 cash on hand. Even if Year 1 EBITDA turns positive after modeled expenses, cash still has to fund the $232k capex and reserve buffer. Pulling distributions too early can leave labs, support, and sales underfunded.

Track Costs and Reserve Floor

Build the reserve test around lab infrastructure, software licenses, insurance, accounting, legal, IT support, curriculum updates, and admin tools. If those items push cash below the reserve floor, owner pay stops until the buffer is rebuilt. That keeps teaching quality and sales capacity intact instead of starving the next cohort.

- Track fixed overhead monthly.

- Refresh the reserve floor often.

- Delay draws until cash clears.

- Separate capex from operating cash.

Watch for hidden creep in support tools and curriculum refreshes. Small overruns matter when fixed costs are already $14,150 a month, because they hit cash before revenue ramps. If the reserve cushion slips, cut discretionary spend first, not instructor support or lab uptime.

6

Compare lean, base, and high ethical hacking course income scenarios

Owner income scenarios

Income shifts with occupancy, billable days, and cohort volume. The same course can stay lean in Year 1 or scale hard by Year 5.

| Scenario | Lean LaunchLean launch | ScalingScaling | Mature PlatformMature platform |

|---|---|---|---|

| Launch model | This is the low owner-income path, modeled on Year 1 utilization and smaller cohort volume. | This is the modeled middle case, where utilization and cohort count reach a steadier scale. | This is the stronger earnings path, with the platform running at mature Year 5 scale. |

| Typical setup | The business runs at 45.0% occupancy, 20 billable days per month, $2.371M revenue, and $1.167M EBITDA before taxes and reserves. | The business runs at 75.0% occupancy and 21 billable days, with $13.923M revenue and $10.112M EBITDA in Year 3. | The business reaches 88.0% occupancy and 22 billable days, with $36.113M revenue and $28.899M EBITDA. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $1.31MLean launch | $10.26MScaling | $29.04MMature platform |

| Best fit | Use this to test launch-year downside and slower sales ramp. | Use this as the core planning case for budgeting and hiring. | Use this to test upside if demand, pricing, and delivery capacity all hold. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Ethical Hacking Training Course Porter's Five Forces Analysis

- Ethical Hacking Training Course BCG Matrix

- Ethical Hacking Training Course Business Model Canvas

- What Are The 5 KPIs For Ethical Hacking Training Course?

- Ethical Hacking Training Course Business Plan Template in Pre-Written Word

- How Increase Ethical Hacking Training Course Profits?

- What Are Operating Costs Of Ethical Hacking Training Course?

- Ethical Hacking Training Course Startup Costs: $874K Launch Plan

- Ethical Hacking Training Course Financial Model Template in Excel

- How To Open An Ethical Hacking Training Course In 8-16 Weeks

- How To Write An Ethical Hacking Training Course Business Plan?

- Ethical Hacking Training Course Marketing Mix

- Ethical Hacking Training Course Marketing Plan

- Ethical Hacking Training Course Business Proposal

- Ethical Hacking Training Course PESTEL Analysis

- Ethical Hacking Training Course Pitch Deck Example Editable PPTX

- Ethical Hacking Training Course Business SWOT Analysis

- Ethical Hacking Training Course Value Proposition Canvas

Frequently Asked Questions

Online delivery can be profitable when labs, support, and completion quality are controlled In the model, revenue grows from $2371M in Year 1 to $36113M in Year 5, while cloud lab hosting falls from 70 percent to 50 percent of revenue Owner take-home still depends on payroll, reserves, and reinvestment