Owner income$654k-$4.9M

Owner income$654k-$4.9MHow Much Can an Exposed Aggregate Concrete Owner Make at $16M?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$654k-$4.9M  Net margin41%-60%

Net margin41%-60% Revenue for target pay$234k

Revenue for target pay$234k Business difficultyHard

Business difficultyHard

Key Takeaways

- Leads matter only when crews can finish profitably.

- Better pricing beats chasing more low-margin jobs.

- Labor, materials, and callbacks decide true cash margin.

- Cash reserves must cover overhead and slow seasons.

Owner income$654k-$4.9MNet margin41%-60%Revenue for target pay$234kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, gross margin, labor, overhead, marketing, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

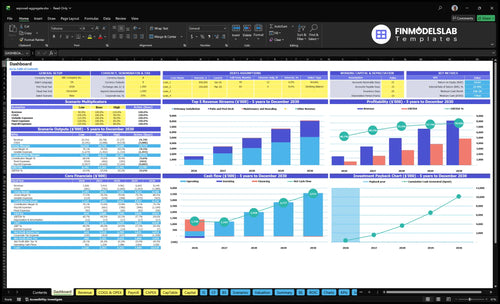

Want to check owner income in the financial model?

This dashboard shows revenue, margin, costs, reserves, and owner take-home for Exposed Aggregate Concrete Service Financial Model Template; open it.

Owner-income model highlights

- Revenue and EBITDA charts

- Billable hours and pricing

- Cash flow and capex

What is the profit margin on exposed aggregate concrete?

If you’re sizing an How Much To Start Exposed Aggregate Concrete Service Business?, use model margin, not a generic construction markup. In the Year 1 model, direct costs are 180% for specialty aggregate and ready mix, 45% for retardants and sealants, 40% for fuel and consumables, and 25% for disposal and waste; the stated gross margin is 710% and EBITDA margin is 407%.

This estimate hides the real drag from failed exposure, bad washout timing, waste, callbacks, and resealing work.

Margin drivers

- Specialty aggregate and ready mix set cost.

- Retardants and sealants add finish cost.

- Fuel and consumables hit every job.

- Disposal and waste must stay tight.

Take-home risks

- Failed exposure drives rework.

- Bad washout timing creates waste.

- Callbacks add labor fast.

- Resealing cuts owner pay.

How much can I make owning an exposed aggregate concrete business?

You can make $95k as an operator salary if you fill the general manager seat, plus owner distributions only after reserves, debt, taxes, capex, and reinvestment. In the How To Launch Exposed Aggregate Concrete Service? model, Year 1 shows $1.606M revenue and $654k EBITDA; Year 5 shows $8.149M revenue and $4.855M EBITDA.

Profit by scale

- Year 1 EBITDA margin: 40.7%

- Year 5 EBITDA margin: 59.6%

- Scale drives owner upside

- Crew density protects margin

Take-home reality

- Solo operator: higher labor risk

- Small crew: steadier cash flow

- Multi-crew: bigger overhead burden

- Distributions come after reinvestment

How many exposed aggregate jobs do I need to pay myself?

If you want to pay yourself from an Exposed Aggregate Concrete Service, there is no fixed job count from this data alone; your target owner pay, close rate, season length, and crew capacity set the number. Year one tickets are about $11,100 for driveways, $8,400 for patios and pool decks, and $960 for resealing, while fixed overhead is $77k/month and marketing is $15k at a $450 CAC, so weather delays and backlog timing can move the job count a lot.

Pay math

- Add owner pay to $77k overhead.

- Use gross profit per job, not ticket.

- Driveways average $11,100.

- Patios and pool decks average $8,400.

What moves the count

- $15k budget at $450 CAC buys about 33 acquisitions.

- Resealing adds smaller jobs at $960 direct cost load.

- Higher close rate cuts the lead count.

- Weather delays push pay timing back.

What drives owner take-home most?

1

$1.6MLead flow

Year 1 revenue is $1.606M, so every extra booked job spreads the truck, yard, and crew costs.

2

$120-$250/hrPricing

Rates run from $120/hr for resealing to $250/hr for patios by Year 5, so better quoting lifts income fast.

3

71%Gross margin

Direct costs on materials, chemicals, fuel, and waste stay near 29%, so each point saved drops straight to profit.

4

42-48 hrsCrew output

Billable hours per active customer rise from 42 to 48 a month, and tighter scheduling turns that into more revenue per crew.

5

$35K/moFixed burn

Shop rent, insurance, software, and core wages set a heavy floor, so lean staffing keeps cash from leaking when work slows.

6

Month 4Capacity use

The model breaks even in Month 4, so early pipeline and tight crew use matter more than late-season volume.

Exposed Aggregate Concrete Service Core Six Income Drivers

Project Volume And Lead Flow

Project Volume and Lead Flow

More exposed aggregate jobs only raise owner income when crews can finish them profitably. Here’s the quick math: Year 1 marketing is $15k and CAC is $450, so the budget supports about 33 customer acquisitions; by Year 5, $40k at $350 CAC supports about 114. Leads alone are not income if weather, backlog, or crew capacity blocks the pour.

Track booked work, not just leads

Measure leads, close rate, booked jobs, weather delays, backlog, and crew capacity every week. In the model, driveway share moves from 450% to 350%, while patio and pool deck rises from 350% to 450%, so mix affects how fast crews burn through days. If lead flow outruns production, cash gets tied up in marketing and overhead, not owner pay.

- Track leads by project type.

- Watch close rate by source.

- Cap bookings to crew capacity.

- Reforecast after weather delays.

1

Average Ticket Size And Pricing Quality

Pricing Quality

When the scope is tight, owner income rises faster than job count. In Year 1, a driveway at 60 hours × $185 is $11,100, a patio or pool deck at 40 hours × $210 is $8,400, and resealing at 8 hours × $120 is $960. Price has to reflect square footage, prep, access, borders, premium aggregate, sealing, and finish complexity.

Underpriced decorative work funds the customer’s upgrade with your margin. If the quote misses cleanup, hard access, or detailing, the same crew time brings in less take-home pay, and cash gets tight fast. Better pricing quality protects gross margin and leaves more room for owner draw after labor and overhead.

Price the Details

Build every estimate from the inputs that change labor and materials: square footage, prep, access, borders, aggregate choice, sealing, and finish complexity. Track quoted hours versus actual hours by job type, and compare driveway, patio, and reseal tickets so you can see where margin slips.

- Quote scope before price.

- Separate add-ons from base work.

- Review overruns by job type.

- Raise rates on hard access.

Here’s the quick math: if a “simple” job needs extra prep or detailing, that extra time comes straight out of profit unless the ticket was built for it. What this estimate hides is rework and callbacks, which can erase a strong-looking price fast.

2

Gross Margin On Job Costs

Gross Margin on Job Costs

Gross margin here is the cash left after direct job costs like ready mix, specialty aggregate, retardants, sealants, fuel, equipment consumables, disposal, and waste fees. With a 290% direct cost load in Year 1, the math is upside down: every $1.00 of revenue carries $2.90 of job cost, so gross margin is -190% before overhead. By Year 5, 242% is still -142%. That leaves very little room to pay the owner.

Finish quality drives the cash result. Failed exposure, uneven finish, late washout, and callbacks can turn a strong ticket into weak cash fast. Here’s the quick math: if estimating misses waste or rework, the job can look profitable on paper and still burn cash on site. Direct job costs are separate from overhead, so this driver must improve before owner draws feel safe.

Track Every Pour Cost

Build each bid from the actual job inputs, then compare estimate to job cost line by line. Track material waste, labor hours, disposal, washout timing, and callback cost on every project. If one pour day overruns on fuel, consumables, or rework, gross margin falls even when the ticket looks strong. The goal is simple: protect the margin before it gets eaten by cleanup and fixes.

Use a job-cost sheet with ready mix, aggregate, additives, sealant, and waste fees as separate lines. Review variance after each project and flag any pour with exposure failure or uneven finish. One clean rule: if the estimate cannot cover the real labor and material load, raise price or narrow the scope before you start.

- Track estimate vs. actual by line item.

- Price for waste, not just square feet.

- Log callbacks as job cost.

- Stop work if finish quality slips.

3

Crew Productivity And Scheduling

Crew Flow

For an exposed aggregate crew, owner pay rises when more of each day becomes billed work instead of idle time, overtime, or rework. Billable hours per active customer move from 420 a month in Year 1 to 480 in Year 5, a gain of 60 hours or 14.3%. That is pure capacity, so it feeds revenue and margin without needing a price increase.

This driver depends on sequencing prep, forms, pour, exposure, washout, cleanup, and sealing in order. Driveway hours fall from 60 to 55, patio hours from 40 to 35, and resealing from 8 to 6. Weather and access issues can break the schedule, so lost days quickly turn into lower cash flow and less owner draw.

Lock The Job Sequence

Track billable hours, idle hours, overtime, and rework by job type. If a driveway, patio, or reseal is running over its target hours, the labor plan is off and margin will leak. One clean rule helps: if the crew is not on a paid task, find out why before the day ends.

- Measure hours per active customer monthly.

- Separate driveway, patio, reseal time.

- Log weather and access delays.

- Schedule washout before cleanup.

- Flag rework before the next pour.

Use those numbers to forecast crew load and owner pay. If the same crew can produce 480 billable hours instead of 420, the business has more room to cover labor and still leave profit for the owner. The key is simple: protect the calendar, or the schedule will steal the margin.

4

Overhead, Equipment, And Fixed Costs

Fixed Costs Before Owner Pay

Monthly overhead is $77k, so owner draws are not safe until gross profit clears that base every month. The listed fixed costs include $32k yard rent, $11k liability insurance, $15k fleet insurance and maintenance, plus software, office overhead, and website and photography costs. If job volume slips, the owner’s pay gets pushed down first.

Track Cash Reserves, Not Just Sales

Use one simple rule: cover fixed overhead, fund repair reserves, then pay the owner. The startup equipment load is $165k, including a $65k truck and $45k skid steer, so bank cash is not all free cash. Here’s the quick math: if overhead is $77k/month, the shop needs that level of recurring gross profit before any draw feels safe.

- Track monthly overhead coverage.

- Separate reserve cash from pay.

- Watch equipment replacement timing.

5

Seasonality And Capacity Use

Seasonal Capacity Use

Seasonality decides whether peak work covers the slow stretch. For exposed aggregate concrete, rainy weeks, winter slowdown, and delayed sealing can push sales out of one month while payroll stays put, so owner pay must be based on conservative cash flow, n ot the best month. In this model, breakeven lands in Month 4, but the minimum cash need is $771k in Month 2.

The inputs that matter are market climate, crew availability, and backlog quality. If the backlog is thin or weather blocks pours and finishing, capacity use drops fast, and take-home income falls even when quoted demand looks strong. One clean rule: full crews do not equal full cash.

Protect Owner Draws From Slow Months

Track booked jobs by start date, not just signed revenue. Split the pipeline into pour-ready work, seal-ready work, and weather-risk work, then compare that to crew hours and payroll due. The goal is simple: keep enough work inside the next 30 to 60 days to cover fixed outflows before you move money to owner draws.

- Watch weather before committing draws.

- Map backlog to crew hours weekly.

- Delay draws until cash clears payroll.

- Price winter risk into schedule promises.

Here’s the quick test: if a rain shift delays sealing or pour dates, cash slips but wages do not. That gap is what breaks owner pay. Build the draw plan from the $771k Month 2 cash floor, then release profit only after the schedule is stable.

6

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income shifts with project mix, crew size, and pricing. The gap from launch year to mature year is wide because payroll and billable capacity scale fast.

| Scenario | Low CaseNon-guaranteed | Base CaseReserve-adjusted | High CaseBefore taxes |

|---|---|---|---|

| Launch model | This is the lower-earnings path with the owner still covering core management work. | This is the modeled middle path with steady growth and a fuller crew. | This is the stronger-earnings path with the business running at mature scale. |

| Typical setup | Year 1 lands at $1.606M revenue and $654k EBITDA, with about $328k payroll, $15k marketing, and the owner possibly filling the $95k GM role. | Year 3 reaches $4.962M revenue and $2.74M EBITDA, with about $636.5k payroll and stronger installed capacity. | Year 5 reaches $8.149M revenue and $4.855M EBITDA, with about $915k payroll and the highest billable load. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $654k EBITDABefore taxes | $2.74M EBITDAModeled case | $4.855M EBITDAUpside case |

| Best fit | Use this to stress test a lean launch where cash, hiring, and owner pay stay tight. | Use this as the planning case for normal growth, hiring, and pricing execution. | Use this to test upside if demand stays strong and the crew keeps up with volume. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. Figures are before taxes and should be reserve-adjusted.

Related Products

- Exposed Aggregate Concrete Service Porter's Five Forces Analysis

- Exposed Aggregate Concrete Service BCG Matrix

- Exposed Aggregate Concrete Service Business Model Canvas

- How Increase Profitability Of Exposed Aggregate Concrete Service?

- Exposed Aggregate Concrete Business Plan Template in Pre-Written Word

- How Increase Exposed Aggregate Concrete Service Profits?

- How Increase Profitability Of Exposed Aggregate Concrete Service?

- Exposed Aggregate Concrete Startup Costs: $165K CAPEX Plan

- Exposed Aggregate Concrete Service Financial Model Template in Excel

- How To Start An Exposed Aggregate Concrete Service In 6–12 Weeks

- How To Write An Exposed Aggregate Concrete Service Business Plan?

- Exposed Aggregate Concrete Service Marketing Mix

- Exposed Aggregate Concrete Service Marketing Plan

- Exposed Aggregate Concrete Service Business Proposal

- Exposed Aggregate Concrete Service PESTEL Analysis

- Exposed Aggregate Concrete Service Pitch Deck Example Editable PPTX

- Exposed Aggregate Concrete Service Business SWOT Analysis

- Exposed Aggregate Concrete Service Value Proposition Canvas

Frequently Asked Questions

The model shows $654k EBITDA on $1606M Year 1 revenue, but owner take-home is only the portion paid as salary or distributions If the owner fills the general manager role, $95k may be compensation inside payroll Extra cash should come after reserves, debt service, taxes, and reinvestment