Owner incomeYear 1: $3.41M

Owner incomeYear 1: $3.41MHow Much Faraday Cage Design Business Owners Make On $645M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeYear 1: $3.41M  Net margin52.9%

Net margin52.9% Revenue for target payYear 1: $6.45M

Revenue for target payYear 1: $6.45M Business difficultyHard

Business difficultyHard

A Faraday cage design and installation business owner can make meaningful income, but only after project costs, overhead, reserves, and reinvestment are covered In the researched first-year assumptions, the firm produces $645M in revenue and about $493M in gross profit before sales commissions, freight, and fixed overhead After listed sales commissions, freight, and known fixed overhead, the pre-tax owner-pay pool is about $434M, before unspecified marketing, payroll, taxes, debt service, warranties, and retained cash Treat that as planning capacity, not guaranteed take-home

Owner incomeYear 1: $3.41MNet margin52.9%Revenue for target payYear 1: $6.45MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed salary, tax advice, or owner distribution advice.

Need the full forecast view for owner income?

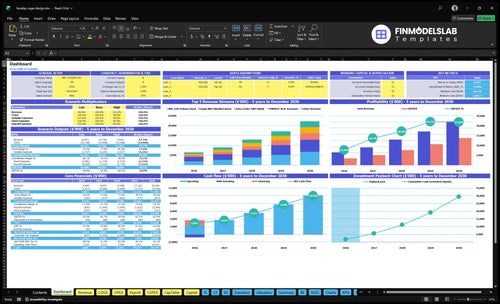

The screenshot shows dashboard outputs, assumptions, scenario tests, revenue build, margins, costs, owner pay, and reserves in the Faraday Cage Design and Installation Financial Model Template. It connects $645M Year 1 revenue to $22,206M Year 5, so open the model.

Owner-income model highlights

- Owner pay and reserves

- Revenue and margin mix

- Scenario assumptions

How much revenue does a Faraday cage business need to pay the owner?

For Faraday Cage Design and Installation, don’t start with sales. Start with the owner’s target pay: after the known $234k annual overhead, every $100k of owner pay needs about $141k of contribution revenue at roughly 71% contribution margin.

Pay stack

- Add $234k overhead first

- Separate salary from draw

- Keep dividends separate

- Plan for taxes and reserves

Quick math

- $100k pay needs $141k revenue

- Use contribution revenue, not vanity sales

- Include debt service and reinvestment

- Work backward from target owner pay

Is a Faraday cage design and installation business profitable?

Faraday Cage Design and Installation can be profitable, but it’s not an automatic yes; the model lists $645M Year 1 revenue, $1,517M COGS, 765% gross margin, and about 710% contribution, so validate the math against What Are Operating Costs For Faraday Cage Design And Installation? before treating profit as cash.

Profit drivers

- Win large technical contracts

- Price specialized engineering work

- Control testing scope tightly

- Reduce rework before delivery

Cash limits

- Fund warranty reserves

- Pay debt and taxes

- Cover payroll before distributions

- Confirm missing fixed expenses

Can a Faraday cage design business scale?

Faraday Cage Design and Installation can scale, but scale does not automatically raise owner income. Here’s the quick math: revenue grows from $645M in Year 1 to $22,206M in Year 5 as volume expands across rooms, racks, test boxes, secure enclosures, and data center shields, while the owner shifts from selling and engineering to managing estimators, installers, project managers, quality control, and cash timing.

Growth drivers

- $645M Year 1 revenue

- $22,206M Year 5 revenue

- More rooms and racks

- More test boxes and shields

Scale risks

- Overhead grows with volume

- Hiring lag and travel load rise

- Quality escapes drive warranty exposure

- Collections stretch cash cycles

Want the six income drivers?

1

$6.45MProject Mix

Bigger rooms and higher-value enclosures lift revenue fastest, so mix drives owner take-home more than low-ticket jobs.

2

71%Margin Control

Every point of margin matters because materials, testing, and labor can eat profit fast in shielded builds.

3

6-16 FTEEngineering Utilization

Keeping engineers on billable work turns salary cost into output, and idle time cuts profit quickly.

4

$22.21MSales Pipeline

A full pipeline keeps build slots sold out, and revenue rises from $6.45M in year 1 to $22.21M in year 5.

5

$195K/moOverhead Structure

With overhead near this level, the shop has to stay busy or fixed cost will eat owner income.

6

$1.09MCash Reserves

A $1.09M cash floor in month 1 helps cover long build cycles and capex before owner draws get safe.

Faraday Cage Design and Installation Core Six Income Drivers

Project Size And Contract Mix

Project Size and Contract Mix

Project size drives take-home fast. Year 1 jobs can range from $65k RF test boxes to $185k MRI shielded rooms, so one large room can move revenue more than many small boxes. The mix matters because the model shows 12 large rooms at $222M versus 120 test boxes at $780k. Bigger work can lift owner pay, but only if compliance, testing, and closeout stay under control.

Price the mix you can deliver

Track contract value, project count, acceptance timing, and change orders by job type. Price testing, documentation, and field integration as separate scope, because high-spec work adds labor and rework risk. If a secure room takes longer to certify than planned, cash flow slips and owner draws should wait. Do not assume access to regulated or government work.

- Track mix by room type.

- Bill testing as separate scope.

- Watch days from install to sign-off.

- Limit work you cannot certify.

1

Gross Margin Control

Gross Margin Control

Owner take-home depends on keeping direct costs inside the bid. In Year 1, the model shows gross margin at about 765% after unit costs and revenue-based COGS, with cost pressure coming from copper mesh, steel panels, conductive gaskets, filters, doors, ventilation treatment, validation, logistics, and field integration. If subcontractors or failed verification tests slip, profit drops fast.

Here’s the quick math: at $645M revenue, each 1 margin point is worth $645k before overhead and reserves. That means small cost overruns can wipe out a lot of owner pay. What this estimate hides: rework, warranty claims, and late acceptance can lock up cash even when the project looks profitable on paper.

Hold Direct Costs Inside the Bid

Track bid cost versus actual cost by job, and break out labor, materials, testing, and field integration. The owner should know the margin on each enclosure before work starts, not after delivery. If a job needs extra validation or a subcontractor change, price it as a change order so gross margin does not get donated away.

- Measure actual cost by cost code.

- Require test sign-off before closeout.

- Log every scope change and leak.

2

Billable Engineering Utilization

Billable Engineering Utilization

When engineering time gets buried in unpaid estimating, owner income drops fast. The core metric is billable utilization: billable engineering hours divided by total engineering hours. Price the work that creates value, like priced drawings, simulations, field reviews, testing plans, and change orders, and keep design fee revenue separate from installation revenue and sales engineering.

Track quoted hours vs. actual hours, rework hours, and customer-driven scope changes. Unpaid revisions drag on the model’s stated 710% Year 1 contribution margin assumption and crowd out billable work, so the owner’s take-home depends on how much engineering time is actually invoiced, not just how busy the team looks.

Bill Every Scoped Engineering Hour

Use a clean rule: if the engineering work creates a deliverable, it gets a line item. That means the quote should list priced hours for drawings, simulations, reviews, testing plans, and change orders, then compare those hours to actuals on every job. One line: if it’s not billed, it’s margin loss.

- Track billable vs. total hours.

- Log rework by job and cause.

- Compare quoted hours to actuals.

- Invoice scope changes fast.

What this hides: utilization can look healthy while profit slips if scope keeps moving. Tight scope language, signed change orders, and weekly review of unbilled engineering time protect cash flow and keep the owner from funding customer revisions out of pocket.

3

Qualified Sales Pipeline

Qualified Sales Pipeline

A clean pipeline keeps crews and engineers busy. With 210 units planned across five project types, weak lead quality can leave installation crews idle and engineering time underused. That hurts owner income twice: revenue slips, and fixed overhead still runs at least $195k/month.

Qualified demand should come from labs, manufacturers, healthcare sites, defense-adjacent facilities, data security buyers, and testing environments. The real test is fit, not volume: if the bid is wrong, close rate falls, backlog stays thin, and take-home pay drops even when the top line looks active.

Track Fit Before You Bid

Track bid fit, close rate, average contract value, backlog months, and delivery capacity. Better-fit bids raise win rate only if the team can still build and test on schedule. Don’t overpromise any marketing channel; one weak source can flood the team with low-value bids.

- Score each lead by project fit.

- Match bids to open capacity.

- Watch close rate by source.

- Reject low-value project types.

- Update backlog before quoting.

4

Fixed Overhead And Staffing

Fixed overhead

Fixed overhead is the monthly nut before profit: facility lease, simulation software, and insurance. The source puts that at at least $195k/month. It also lists $234k/year, so confirm the annual rollup before you use it in break-even math. This cost sits above direct project COGS, so it has to be covered before the owner can pay themselves.

Hiring engineers, installers, estimators, and project managers can expand capacity, but it also raises the break-even point. If project volume slows or the mix shifts to smaller jobs, the same overhead gets spread across less revenue, which cuts cash for reserves and owner draw. One clean rule: if overhead rises faster than booked work, take-home income falls.

Control the monthly burn

Track fixed costs by category and keep them separate from direct job costs. Use one monthly view for lease, software, insurance, payroll, benefits, professional services, vehicles, travel, certification support, and management layers. The key test is simple: can booked work cover $195k/month before any owner draw?

- Track fixed cost by category.

- Separate overhead from COGS.

- Hire against booked backlog.

- Watch overhead per active project.

Add staff only when new work lifts contribution faster than overhead grows. If utilization slips, cut nonessential layers first, because idle payroll turns a good gross margin into weak cash flow and smaller owner pay.

5

Cash Reserves And Working Capital

Cash Reserve Discipline

Profitable work can still block owner pay when deposi ts, progress payments, retainage, and long material lead times tie up cash. The model shows about $434M Year 1 pre-tax owner-pay capacity before reserves and missing costs, but that is not safe take-home. Cash, not profit, also funds warranty work, testing failures, and equipment purchases.

Track Cash, Not Just Profit

Measure reserve percentage, cash conversion (how fast work turns into collected cash), deposits collected, payables timing, warranty claims, and equipment replacement needs. If a job needs cash before final billing, owner distributions should wait until the reserve is funded.

- Match deposits to material orders.

- Bill progress work on time.

- Track retainage by job.

- Ring-fence warranty cash.

That keeps owner take-home tied to real collections, not booked profit.

6

Scenario objective: compare lean, base, and high owner-income planning cases

Owner income scenarios

Owner income swings with project timing, install volume, and fixed overhead. The three cases show a slow ramp, the planned base case, and a stronger year-five scale-out.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path if project starts slip and margins compress. | This is the modeled earnings path if execution stays on plan. | This is the stronger earnings path if volume scales and pricing holds. |

| Typical setup | Year 1 volume is 210 units and revenue is $6.45M, with about 76.5% gross margin, about 71.0% contribution margin, and at least $234k known fixed overhead. | Year 3 volume is 423 units and revenue is $12.968M, with about 77.6% gross margin, about 72.5% contribution margin, and an estimated pre-tax owner-pay pool of about $9.16M. | Year 5 volume is 693 units and revenue is $22.206M, with about 78.6% gross margin, about 74.2% contribution margin, and an estimated pre-tax owner-pay pool of about $16.24M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $4.34MLow Case | $9.16MBase Case | $16.24MHigh Case |

| Best fit | Use this to stress-test a slow launch, late installs, or weaker pricing. | Use this as the plan case for steady growth and controlled overhead. | Use this to test upside if demand lands and cost growth stays tight. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Faraday Cage Design and Installation Porter's Five Forces Analysis

- Faraday Cage Design and Installation BCG Matrix

- Faraday Cage Design and Installation Business Model Canvas

- What Five KPIs Should Faraday Cage Design And Installation Business Track?

- Faraday Cage Design and Installation Business Plan Template in Pre-Written Word

- How Increase Profitability Of Faraday Cage Design And Installation?

- What Are Operating Costs For Faraday Cage Design And Installation?

- Faraday Cage Design Startup Costs: $639K Monthly Burn Before CAPEX

- Faraday Cage Design and Installation Financial Model Template in Excel

- Start a Faraday Cage Design and Installation Business in 12–24 Weeks

- How To Write A Business Plan For Faraday Cage Design And Installation?

- Faraday Cage Design and Installation Marketing Mix

- Faraday Cage Design and Installation Marketing Plan

- Faraday Cage Design and Installation Business Proposal

- Faraday Cage Design and Installation PESTEL Analysis

- Faraday Cage Design And Installation Pitch Deck Example Editable PPTX

- Faraday Cage Design and Installation Business SWOT Analysis

- Faraday Cage Design and Installation Value Proposition Canvas

Frequently Asked Questions

The researched Year 1 model shows about $434M of pre-tax owner-pay capacity before taxes, debt, reserves, unspecified payroll, and missing marketing detail That comes from $645M in revenue, $1517M in listed COGS, $3548k in commissions and freight, and $234k of known fixed overhead It is not guaranteed take-home